This marks the final Weekly Update of 2024 – time flies when you’re navigating the markets, doesn’t it? 😊 I’ll be taking the next two weeks off, but don’t worry, the scintillating commentary will return on January 3, 2025.

A heartfelt thank you for sticking with me through the ups and downs of the market this year. Here’s to hoping 2025 keeps the bull run alive that’s been charging ahead since early 2023. 😊 In the meantime, enjoy the Christmas holiday season as 2024 wraps up, and may the new year bring you health, happiness, and, of course, prosperity!

It is the final week before Christmas, and the markets kept us on our toes with a flurry of economic data. But rather than dive straight into the numbers, I thought a little Christmas spirit would set the tone for this Weekly Update. So, without further ado, here is an investing spin on a Christmas classic!

‘Twas the Night Before Christmas

”Twas the week before Christmas, and all through the Street,

The markets were stirring, not ready to retreat.

Investors were watching their tickers with care,

In hopes that a Santa Rally soon would be there.

The bulls were nestled, still dreaming of gains,

While whispers of rate cuts danced in their brains.

And I with my spreadsheets, all set for review,

Had just settled in to assess what I knew.

When out on the floor there arose such a clatter,

I sprang to the charts to see what was the matter.

Away to the data I flew like a flash,

Checking the headlines for signs of a crash.

The candles on charts with their flickering glow,

Gave a glimmer of hope to the bulls down below.

When what to my wondering eyes should appear,

But a strong rebound rally to close out the year.

With a savvy old trader, so sharp and so quick,

I knew in a moment it must be St. Nick.

More rapid than algo trades, upward they came,

And he whistled and shouted and called them by name::

“Now Apple! Now Tesla! Now Microsoft, too!

On Nvidia! On Amazon! On stocks breaking through!

To the top of the charts, to the highs we can see,

Dash away! Cash away! A green close is key!”

As dry powder’s deployed when opportunities call,

When buyers step in to prevent a freefall,

So up to the new highs the tickers they flew,

With portfolios rising and St. Nicholas, too.

And then, in a twinkling, I heard on the news,

The Fed’s steady stance calming Wall Street’s views.

As I refreshed my screen and was spinning around,

Down came St. Nick with a leap and a bound.

He was dressed like a trader from head to his feet,

And his suit was as crisp as the Nasdaq’s last beat.

A bundle of insights he had in his hand,

Ready to share with investors across the land.

His eyes – how they twinkled! His wisdom so cheery!

His forecasts were balanced, not overly dreary.

He spoke of the long game, of patience and care,

Of building portfolios designed to outlast a scare.

“The markets, my friend, can be fickle, it’s true,

But stay in the game, and returns will accrue.

Diversify wisely, avoid chasing the trend,

And remember, each dip can bring gains in the end.”

He finished his speech with a wink of his eye,

And soared from the market with gains flying high.

But I heard him exclaim as he vanished from sight,

“Happy investing to all, and to all a good night!”

While St. Nick and his rallying bulls might be a fun holiday vision, the real markets were not quite as magical this week. Let’s take a look at how the Fed – and Santa – shaped the markets as we head into the final stretch before Christmas.

Items that may only interest or educate me ….

Canadian Economic news, US Economic news,

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Government fiscal update

As many had expected, the fiscal update revealed that the federal government missed one of its key fiscal targets for the 2023/2024 budget, running a fiscal deficit of C$40 billion. However, what caught many off guard was just how badly they overshot their goal, with the deficit coming in at a whopping $61.9 billion—nearly 50% higher than projected.

The news was further shaken up by Finance Minister Chrystia Freeland’s sudden resignation just hours before the Fall Economic Statement. Her departure has left a significant void in the government, raising critical questions about the future direction of Canada’s economic policies. The timing – just before such an important fiscal update – has only deepened the uncertainty about the government’s ability to manage the country’s finances and fueled the political intrigue surrounding her unexpected exit.

Consumer price Index (CPI)

Statistics Canada reported that inflation remained flat in November, slowing from October’s 0.4% increase, and coming in slightly better than the expected 0.1% rise. On an annual basis, inflation stood at 1.9%, just shy of October’s 2.0% and the rate analysts had forecast.

Monthly data showed ‘Food’ prices rising the most with a 0.5% increase, while ‘Household operations, furnishings, and equipment’ saw the steepest drop, declining 0.9%. On a yearly basis, ‘Shelter’ costs, which include mortgages and rent, continued to cool but still posted the largest increase at 4.6%, down from October’s 4.8%. In contrast, prices for ‘Clothing and footwear’ had the sharpest annual decline, falling 3.8%. Inflationary pressures are easing overall but rising costs in key areas like food and shelter still weigh on consumers.

Core CPI, which excludes volatile the food and energy categories, also cooled. It dropped 0.1% month over month and slowed to a yearly growth rate of 1.9%, down from 2.3% in October.

With both the annual headline and core inflation rates dipping below the BoC 2% target, the central bank is likely to return to smaller, more conventional rate cuts of 0.25%, following the last two jumbo sized 0.5% reductions. However, December’s inflation data could shift the narrative – if the numbers come in higher than expected, the BoC might pause its rate-cutting to reassess.

For now, the BoC’s priority seems to be supporting economic growth, but it faces a tricky balancing act. On one hand, letting Canadian interest rates fall too far below US levels could weaken the loonie, driving up the cost of US imports and risking a new bout of inflation. On the other hand, keeping rates too high could stifle domestic growth, which the economy can ill afford.

Retail sales

Statistics Canada reported that retail sales in Canada rose by 0.6% in October, surpassing September’s 0.4% increase but falling short of analysts’ expectations of a 0.7% gain. On a year-over-year basis, sales grew by 1.5%, a stronger performance than the 0.8% increase in September, and ahead of the expected 0.8%.

At the sector level, the ‘Furniture, home furnishings, electronics, and appliances’ category saw the largest monthly gain, jumping 2.5%. On the flip side, ‘Food and beverage retailers’ experienced the biggest decline, down 0.7%. Year-over-year, ‘Motor vehicle and parts dealers’ posted the largest sales increase, up 3.6%, while ‘Gasoline stations and fuel vendors’ reported the biggest annual drop for the second consecutive month, down 5.9%.

Core retail sales, which exclude gasoline stations and fuel vendors and motor vehicle and parts dealers, rose 0.2% in October, a slowdown from September’s 1.4% increase. Annually, core sales were up 1.8%, slightly below the 1.9% growth in September.

This data suggests retail spending is beginning to slow, reflecting the broader trend of a cooling Canadian economy. Since retail sales account for nearly 40% of total consumer spending and are considered an early indicator of GDP growth, this slowdown may signal a slowdown in overall economic momentum. Statistics Canada also provided an early estimate for November, which will be published on January 23, 2025, indicating that the pace of retail sales was largely unchanged.

Canadian market volatility

Canada’s Volatility Index (VIXC) had a relatively calm week, starting at 9.23 before spiking to 11.90 on Wednesday following the US Federal Reserve’s announcement that they only expect to lower US rates twice in 2025. Investor anxiety fluctuated throughout the week, but the VIXC eased back slightly, closing at 11.66—on the lower end of what is considered normal market fluctuations.

Tracked under the ticker VIXI on the Toronto Stock Exchange (TSE), the VIXC measures investor expectations for market volatility. A reading below 10 signals a calm, stable market, while numbers between 10 and 20 indicate typical market fluctuations with moderate volatility. When the index rises above 20, it reflects increased uncertainty and the potential for a bumpier ride ahead.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

FOMC rate decision

At its final Federal Open Market Committee (FOMC) meeting of the year, Fed Chair Jerome Powell announced a widely expected 0.25% cut to the benchmark interest rate, lowering it to a range of 4.25%–4.5%. While the move itself did not surprise analysts or investors, the Fed’s updated forecast – predicting just two rate cuts in 2025, down from four projected in September – caught markets off guard. Investors interpreted this revised outlook as a potential signal of a pause in rate cuts as early as January.

The decision was not unanimous, with one member dissenting in favour of holding rates steady. This marks only the second instance during the Fed’s current rate-cutting cycle where a member did not agree with the majority decision. The latest adjustment is the third cut this year, following a 0.5% reduction in September and a 0.25% cut in November. The updated forecast reflects persistent concerns about stubborn inflation, which the Fed expects could remain elevated into the new year.

Future rate decisions will hinge on whether inflation resumes its downward trajectory after recent resistance. Adding to the uncertainty are the sweeping tax reforms and deregulation efforts promised by the incoming Trump administration, which could further complicate the Fed’s delicate balancing act between fostering economic growth and keeping inflation in check. As 2025 approaches, all eyes will be on the Fed to see how it navigates these competing pressures.

Retail sales

The Commerce Department’s Census Bureau reported a stronger-than-expected November 2024 Advance Monthly Retail Sales report, showing a 0.7% increase in retail and food services sales. This beat analyst expectations of a 0.5% rise and followed an upwardly revised 0.4% gain in October. On an annual basis, retail sales climbed 3.8%, improving on October’s revised growth of 2.9%.

The impact of lower interest rates was evident in the 2.8% surge in sales in the ‘Auto & Other Motor Vehicle Dealers’ category, marking the biggest monthly increase. Meanwhile, ‘Miscellaneous Store Retailers’ experienced the steepest drop, down 3.4% for the month. Year-over-year, ‘Nonstore Retailers’ (online shopping) led the pack with a 9.9% jump, while spending at ‘Gasoline Stations’ declined 3.9%, likely due to lower fuel prices.

Core retail sales – which exclude the volatile categories of motor vehicles, parts, and gasoline—rose modestly by 0.2% in November, following a 0.1% increase in October. Annually, core sales continued their steady climb, rising 3.9%, slightly higher than October’s 3.8% growth.

This latest report underscores the resilience of the American consumer, with lower interest rates, a strong labour market, and rising wages fueling increased retail sales. Car purchases, in particular, surged to their strongest level in three years, while robust Cyber Weekend sales gave online shopping a notable boost. Consumer confidence has also climbed since the presidential election, buoyed by expectations of lower rates and reduced taxes.

This latest data is unlikely to influence the Fed’s rate decision tomorrow, as higher holiday sales are typically expected. However, the stronger-than-anticipated figures are sure to grab their attention as they remain vigilant for signs of rising inflation. When combined with the potential impact of lower taxes, import tariffs, and the pro-growth agenda of the new administration, this retail sales momentum could prompt the Fed to reconsider further rate cuts in January.

Gross Domestic Product (GDP)

The final reading of third-quarter GDP revealed stronger-than-expected growth, with the economy expanding at an annualized rate of 3.1%. This marks an upward revision from the second estimate of 2.8% and exceeds analysts’ forecasts of 2.8%. The revision reflects improved data across key areas: exports, consumer spending, non-residential fixed investment, and federal government spending. These gains were partially offset by a decline in private inventory investment and a steeper drop in residential fixed investment.

With GDP accelerating from 1.6% in the first quarter to 3.0% in the second, and now 3.1% in the third quarter, the data suggests the economy will finish 2024 on a strong note. Analysts now turn to the advance estimate for fourth-quarter GDP, scheduled for release on January 30, 2025, to determine if this momentum carried through the year’s final stretch.

Personal Consumption Expenditures (PCE)

The Commerce Department’s Bureau of Economic Analysis reported that inflation, as measured by the PCE Price Index, slowed to 0.1% in November on a monthly basis, falling short of analysts’ expectations for a 0.2% rise and after two consecutive months of 0.2% increases. On an annual basis, the headline PCE (which includes all items) rose 2.4%, slightly below October’s 2.6% and the forecasted 2.5%.

Core PCE, the Fed’s preferred inflation gauge, which excludes the more volatile food and energy sectors, also came in softer than expected. It rose just 0.1% in November, down from October’s 0.3% increase. Year-over-year, core PCE eased to 2.8%, a noticeable drop from October’s 3.2%, and below the anticipated 2.9%.

After a series of reports showing inflation holding steady or rising slightly, this latest data suggests inflationary pressures are continuing to cool, providing the Fed with some breathing room. While the slowdown in price growth is a positive sign, the Fed remains cautious, as core inflation is still above their 2% target.

The December PCE is scheduled for release on January 31, 2025.

Consumer Sentiment Index (CSI)

The University of Michigan’s final Consumer Sentiment Index (CSI) for December landed at 74, matching expectations and reaching its highest level since April 2024. This marks a 3.1% boost from November’s 71.8 and a solid 6.2% improvement over December 2023, when it stood at 69.7. The December reading also marked the fifth consecutive monthly gain, highlighting a steady climb in consumer confidence.

Digging deeper, the Current Economic Conditions index – which measures how consumers feel about their present financial situation – surged to 75.1. This impressive 17.5% jump from November’s 63.9 contrasts with a more modest 2.5% increase compared to December 2023. Meanwhile, the Index of Consumer Expectations, which gauges optimism about the next six months, slipped 4.7% to 73.3 from November’s 79.9. Still, it remains 8.8% higher than last December’s 67.4.

The rise in overall sentiment appears to be driven by favourable buying conditions for big-ticket items like cars and appliances, supported by lower interest rates and a strong labour market. Many consumers are adopting a “buy now, avoid paying more later” mindset, anticipating the potential for rising interest rates or import tariffs to drive up costs in the future. Interestingly, political affiliation influenced expectations: Republicans were optimistic about improving conditions, while Democrats were more cautious.

American market volatility

The CBOE Volatility Index (VIX), known as the market’s “fear gauge,” started the week at 14.37 and gradually crept higher as investors anticipated the midweek FOMC rate decision. When the Fed announced fewer rate cuts for next year, the VIX spiked to 27.62, a dramatic 74% jump—its largest single-day surge since February 2018. Afterward, the VIX dipped just as sharply, only to rise again above 26 before tumbling back down on Friday, closing the week at 18.37.

For context, the VIX measures expected market volatility over the next 30 days. Readings below 12 signal a calm market, while values between 12 and 20 reflect normal market fluctuations. When the VIX rises into the 20-30 range, it indicates heightened investor anxiety, and anything above 30 typically signals market stress, often foreshadowing major turbulence or even a crisis.

Weekly Market Review

Monday: The week kicked off with a bit of mixed sentiment as the S&P 500 Index (S&P) and the Nasdaq Composite Index (Nasdaq) finished the day in the green, while the Toronto Stock Exchange Composite Index (TSX) and the Dow Jones Industrial Average (DJIA) closed lower. Investors were largely holding their breath ahead of the Fed’s midweek rate update, with most expecting a 0.25% rate cut. Meanwhile, oil prices took a dip, weighed down by weaker-than-expected Chinese retail sales data.

In Canada, the TSX was weighed down by lower oil price and the sudden resignation of the Finance Minister. In trading, Financials was the only sector to advance, while Communication Services had the worst day.

In the US, the Nasdaq soared on the backs of the heavyweight technology companies to another record high in anticipation of a rate cut later this week. On the downside, the DJIA dropped for the eighth straight session, its longest losing streak since June 2018. In trading, the Consumer Cyclicals sector rose the most, while the Energy sector saw the biggest decline.

Tuesday: after a mixed start yesterday, it got worse with all four indexes ending in the red as investors await the Fed’s rate decision tomorrow. Oil prices fell on poor economic reports from the world’s second and third largest economies, China and Germany, respectively.

In Canada, political uncertainty at the federal level, with lower commodity prices, and mixed inflation data combined to knock the TSX to its lowest point in four weeks. In trading, the Healthcare sector posted the biggest gain, while the Communication Services fell the farthest.

In the US, the markets fell after higher-than-expected retail sales data hinted a rate cut tomorrow could be the last cut for a while. The DJIA’s losing streak stretched to nine games, its longest losing streak since February 1978. The DJIA has been weighed down by profit taking in Nvidia (NASD: NVDA) after its recent run up, and UnitedHealth (NYSE: UNH) following the murder of their Chief Executive Officer. In trading, it was a day of wide-ranging losses with only the Consumer Cyclicals able to climb higher, while the Industrials sector dropped the most.

Wednesday: all four indexes were relatively flat prior to the Fed’s rate announcement but they plunged after the Fed announced they expected fewer rate cuts in 2025. Oil prices also fell on the news from the Fed.

In Canada, the TSX was dragged down by the US Fed announcement, sending the index to its lowest level in six weeks. It was a day of across-the-board losses in trading, with the Communication Services sector the best of the lot while the Technology sector fell the farthest.

In the USA, all three indexes reversed earlier gains following the Fed’s announcement. The DJIA extended its losing streak to 10 sessions, its longest since 1974 (50 years). In trading, all sectors lost ground. The Healthcare sector dropped the least while the Consumer Cyclicals sector fell the farthest.

Thursday: the markets started off on the right foot, rebounding from yesterday’s sell off, but at the end of the day only the DJIA remained in the green, making today slightly better than yesterday. Oil prices dropped on concerns that sticky inflation could slow rate cuts and eat into demand.

In Canada, worries over a more aggressive stance from the US Fed weighed heavily on the markets, pushing the Canadian dollar lower and extending the TSX’s losing streak to six straight sessions—its longest slide since October 2023. In trading it was another day of across-the-board losses, with Consumer Staples falling the least and Industrials falling the farthest.

In the USA, the DJIA snaps its longest losing streak in 50 years, barely getting into positive territory. In trading, the Utilities sector increased the most, while the Basic Materials (mining companies and fertilizer manufacturers) gave up the most ground.

Friday: the indexes had a rough start, but all four quickly bounced back after lower-than-expected inflation data from the PCE report, ending the day solidly higher. Oil was down slightly, weighed down by concerns over weaker global demand and an impending supply surplus.

In Canada, the TSX made a strong comeback after six straight losing sessions, boosted by higher commodity prices and lower inflation in the US. The Healthcare sector led the way with impressive gains, while Consumer Staples was the only sector to finish in the red.

In the US, a potential government shutdown was averted at the last minute, bringing relief to investors and employees alike. The three major indexes each posted gains of at least 1%, helped by the inflation data suggesting that price pressures are continuing to ease. It was a day of broad-based gains, with all sectors closing in the green, led by the Technology sector, while Consumer Staples lagged behind.

Weekly Market and Portfolio Review

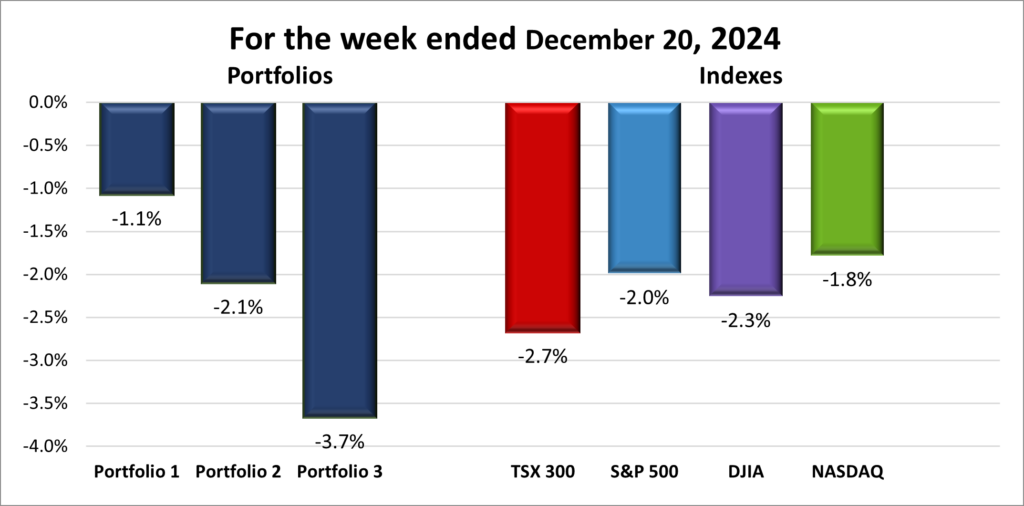

For the week, the TSX (SPTSX) plunged 2.7%, the S&P 500 (SPX) fell 2.0%, the DJIA (INDU) lost 2.3% and the Nasdaq (CCMP) sank 1.8%.

| Index | Weekly Streak |

| TSX: | 2 – week losing streak |

| S&P: | 2 – week losing streak |

| DJIA: | 3 – week losing streak |

| Nasdaq: | 1 – week losing streak |

![]() The Santa Claus rally seems to be struggling to take off this year. Despite a sharp rebound at the end of the week, all four major indexes still recorded weekly losses, as highlighted in the performance chart above.

The Santa Claus rally seems to be struggling to take off this year. Despite a sharp rebound at the end of the week, all four major indexes still recorded weekly losses, as highlighted in the performance chart above.

The week started on a rocky note, with Nvidia playing an outsized role in dragging down the three American indexes. A sharp 12% drop in Nvidia’s share price – marking a correction from its all-time high in early November – had a significant impact, as the heavyweight is a component of the S&P 500, Nasdaq, and DJIA. This alone set a negative tone, but things went from bad to worse after the Fed’s much-anticipated rate announcement.

While the Fed delivered a widely expected 0.25% rate cut, it was their guidance for 2025 that sent shockwaves through the markets. The Fed indicated it only expects to lower rates twice next year, a sharp contrast to their earlier forecast of four cuts. This cautious stance, driven by concerns over stalled inflation progress, triggered a broad sell-off in both the US and Canadian markets. The DJIA dropped over 1,100 points as investors processed the reality of slower rate relief. However, the American economy remains strong, and the Fed is unlikely to raise rates again anytime soon.

Adding to the mix, the looming threat of a government shutdown added a layer of volatility to the American markets. Political uncertainty of this kind rattles investors, especially as the budget impasse raises concerns about economic disruptions. With the second Trump term looming, markets are bracing for even more political drama.

In Canada, the TSX faced a rough start to the week, and things worsened after the Fed’s announcement of just two rate cuts in 2025. With last week’s cut behind us, it seems the Fed will likely pause further rate reductions for now. If US interest rates hold steady while Canada’s continue to fall, the Canadian dollar could weaken, making US imports more expensive for Canadians. A hawkish Fed typically strengthens the US dollar by attracting foreign capital, putting pressure on other currencies like the loonie. While a weaker loonie could spark inflation by driving up import costs, a stronger US dollar could make Canadian exports more attractive, potentially boosting demand for Canadian goods.

As we move into the final weeks of the year, market volatility is likely to persist as investors digest the latest inflation data and the Fed’s rate cut forecast. Hopefully, Santa’s got his reindeer ready to go, and the Santa rally finally makes an appearance next week! 😊

| Portfolio | Weekly Streak |

| Portfolio 1: | 2 – week losing streak |

| Portfolio 2: | 2 – week losing streak |

| Portfolio 3: | 2 – week losing streak |

![]() It was a rough week across the board for the three portfolios, mirroring the tough conditions in the markets. Unfortunately, none managed to eke out a gain, with all posting losses of at least 2%.

It was a rough week across the board for the three portfolios, mirroring the tough conditions in the markets. Unfortunately, none managed to eke out a gain, with all posting losses of at least 2%.

Portfolio 1 emerged as the “least worst,” limiting its losses to 1.1%. Only 13% of its holdings managed weekly gains, but Mitek Systems (NASD: MITK) stole the spotlight with a 30% surge following a strong earnings report. On the flip side, Innovative Industrial Properties (NYSE: IIPR) plummeted 28% after it was announced that it was being investigated for securities fraud, and Celsius Holdings (NASD: CELH) slid 13%. Alphabet (NASD: GOOGL) hit an all-time high early in the week before reversing to finish lower at the end of the week. Nvidia, the portfolio’s largest holding, chipped in a modest 1% gain, helping soften the blow and keeping the portfolio’s decline the smallest of the portfolios and the four indexes.

Portfolio 2 had the highest percentage of stocks posting gains, with 22% in the green—not exactly a high bar. Still, it wasn’t enough to avoid a weekly loss above 2%.

Portfolio 3 had a tough week all around, posting the largest percentage decline of the three portfolios. Only 13% of its holdings managed to post gains, and there was no standout performer to offset the broader losses. Unlike Portfolio 1, which benefited from Nvidia’s modest gain, Portfolio 3 lacked any significant holding to help limit the damage, resulting in a particularly rough showing.

Tough weeks like this are part of the investing journey. Let’s see what next week brings—hopefully, the Santa Claus rally will finally begin, bringing a brighter outlook for the portfolios! 😊

Companies on the Radar

This week, I stumbled upon a company that initially did not pass my Radar Check but still piqued my interest—Rubrik, Inc. (NASD: RBRK). Despite presenting a few red flags, including no net income, no operating income, and negative cash flow, I was intrigued by the company’s potential. Rubrik is a large American company in the rapidly growing cybersecurity industry, with over 3,000 employees across 22 global offices and a market cap of over US$13 billion. Founded in 2014 and going public just this past April, the company’s size and the sheer scale of the cybersecurity market have me curious enough to dig deeper.

This week, I stumbled upon a company that initially did not pass my Radar Check but still piqued my interest—Rubrik, Inc. (NASD: RBRK). Despite presenting a few red flags, including no net income, no operating income, and negative cash flow, I was intrigued by the company’s potential. Rubrik is a large American company in the rapidly growing cybersecurity industry, with over 3,000 employees across 22 global offices and a market cap of over US$13 billion. Founded in 2014 and going public just this past April, the company’s size and the sheer scale of the cybersecurity market have me curious enough to dig deeper.

On the flip side, I’ve decided to part ways with Domino’s Pizza (NYSE: DPZ), the giant pizza chain. While it is a well-established company, its relatively low dividend does not fit the income profile I am after, and its growth potential does not quite align with my goals for more aggressive, growth-oriented stocks.

With one company making its way onto my radar and another exiting, my list remains at four companies, including the ones listed below.

- On Holding AG (NYSE: ONON), a medium cap Swiss company, founder-run, sports products company.

- Topaz Energy Corp. (TSE: TPZ), a mid-cap Canadian energy investment firm that focuses on strategic investments in premium energy assets operated by top-tier Canadian companies, and currently pays a dividend in the 5% neighbourhood.

- Topicus.com Inc. (TSE.V: TOI), a mid-cap spinoff from Constellation in 2020, focusing on delivering vertical software solutions in the European Union market.

As always, these are not buy recommendations – be sure to do your own research and make decisions that align with your personal financial goals!

The Radar Check was last updated December 20, 2024.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended December 20, 2024: DOWN ![]()

- Alphabet’s Waymo autonomous car division announced they will start testing their robotaxis in Japan, starting in 2025. It will be Waymo’s first entrance into a foreign market.

- Walmart (NYSE: WMT) has teamed up with Chinese delivery giant Meituan to enhance its delivery services in China. Meituan, the country’s leading platform for quick delivery of everyday household goods, will now feature Walmart on its app. This partnership aims to accelerate Walmart’s e-commerce growth in the Chinese market by tapping into Meituan’s extensive customer base and efficient delivery network.

In other Walmart news, the company was named Yahoo Finance’s Company of the Year. The company has quietly morphed into a leader of utilizing technology, building up their capabilities in artificial intelligence (AI), online advertising through their acquisition of TV maker Visio, same day delivery service, not to mention inexpensive groceries. - Amazon.com (NASD: AMZN) employees at seven US fulfilment centres went on strike during the holiday shopping rush, over the company’s refusal to recognize the Teamsters Union.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Yellow Pages Ltd (TSE: Y)

Hammond Power Solutions (TSE: HPS.A)

Decisive Dividend (TSE: DE) DRIP

US $

Alphabet (NASD: GOOGL)

BSR Real Estate Investment Trust (TSE: HOM.U)

General Motors Co (NYSE: GM)

Quarterly Reports

Carnival Corporation & plc

Fourth quarter 2024 financial results on December 20, 2024

Portfolio 2

Portfolio 2 for the week ended December 20, 2024: DOWN ![]()

- Guardant Health (NASD: GH) announced they will be working with Boehringer Ingelheim, a German pharmaceutical company. The partnership aims to secure regulatory approval for Guardant’s cutting-edge Guardant360 CDx test as a companion diagnostic to identify non-small cell lung cancer patients who could benefit from one of Boehringer’s advanced cancer treatments.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

SmartCentres Real Estate Investment Trust (TSE: SRU.UN)

Supremex Inc. (TSE: SXP)

Hammond Power Solutions (TSE: HPS.A)

Alimentation Couche-Tard Inc (TSE: ATD)

Whitecap Resources Inc (TSE: WCP)

US $

No US$ dividends this past week.

Quarterly Reports

Mitek Systems, Inc.

Fourth quarter 2024 financial results on December 20, 2024

Birkenstock Holding plc

Fourth quarter 2024 financial results on December 18, 2024

Portfolio 3

Portfolio 3 for the week ended December 20, 2024: DOWN ![]()

- Enghouse Systems (TSE: ENGH), announced its United Kingdom division had purchased Aculab PLC, for an undisclosed price. Aculab specializes in on-premise and cloud-based communications solutions as well as AI driven answering machine technology.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

SmartCentres Real Estate Investment Trust (TSE: SRU.UN) DRIP

US $

Vertiv Holdings (NYSE: VRT)

Quarterly Reports

No quarterly reports this past week.