Items that may only interest or educate me ….

Canadian Economic news, US Economic news, US budget battle – round 3, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Canadian market volatility

The Canadian Volatility Index (VIXC), represented by the TSX 60 VIXI, ended the week at 12.76, down significantly from last week’s reading of 15.03. The 12.76 reading suggests that investors believe the Canadian markets have become less volatile. Consequently, their outlook has become more bullish because of the lower US inflation level and a sense that interest rates have reached their peak. In the context of the VIXC, a reading above 20 is considered high, while below 20 is deemed low.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Consumer Price Index (CPI)

The October rate of inflation, according to the Bureau of Labor Statistics, remained unchanged from September, but it increased 3.2% over the past 12 months. This was the smallest 12-month increase in headline inflation since September 2021. The increase was lower than analysts’ expectations of a 3.3% increase. The primary reason for the lower rate of inflation was the drop in fuel prices. On a monthly basis, inflation was unchanged in October, down from the 0.4% pace in September. Analysts were expecting a gain of 0.1%.

The sector with the largest monthly gains was utility gas services, up 1.2%, while the biggest decline was energy commodities, down 4.9%. Year over year, the biggest increase was in the transportation services, up 9.2% and the biggest decline was in the fuel oil sector, down 21.4%.

Headline inflation includes all the components of the CPI, whereas core CPI strips out the more volatile food and gas costs.

Core CPI, the Fed’s preferred measure of inflation, rose 4.0% over the past 12 months, matching the increase in September and the slowest pace since September 2021. The energy index decreased 4.5% for the 12 months ending October, and the food index increased 3.3% over the last year. Monthly core prices rose 0.2%, equaling September’s monthly pace. Analysts were expecting gains of 4.1% and 0.3%, respectively.

While core CPI slowed a bit from September, it suggests underlying inflation is hanging around, something the Fed is concerned about. In the last two weeks Fed officials had hinted sticky inflation could be a problem and said the interest rate may not be high enough to drive inflation down to their target of 2%. This latest core CPI data will catch their attention.

Regardless, investors took this as a sign the Fed will leave the benchmark rate unchanged at their next meeting in December. And, more importantly, that the Fed could be done raising interest rates.

American market volatility

During the week, the CBOE Volatility Index (VIX) fell to 13.80, down slightly from 14.17 the previous week. Investors have a bullish outlook on the stock markets, thanks to the lower-than-expected CPI report. The slight decline in the VIX suggests investors remain relatively unconcerned about volatility in the American stock markets.

Retail Sales

The Commerce Department reported retail sales decreased 0.1% in October, compared to a revised 0.9% increase in September. That was the first month-over-month decline since March. A lot of the decline is likely attributable to people spending less on gas.

Excluding automobiles, gasoline, building materials and food services, retail sales actually rose 0.1% in October after gaining 0.6% in September.

Economists had forecast a drop of 0.3% so American consumers are proving to be more resilient than analysts expected. The American consumer drives the economy so the Fed will be pleased with this report because while spending slowed, it still remained strong. Add in improving economic conditions, the Fed will be very pleased indeed.

US budget battle, round 3

In a positive development, the US was able to avoid a third round of budget brinkmanship when the Republican controlled US House of Representatives (House) passed a novel two step temporary spending bill that avoided a government shutdown. The bill received broad support from lawmakers from both parties, receiving more than two-thirds of the House support to fund the government for the next few months. The bill did not receive unanimous support of the Republicans but did garner enough votes from the Democrats to pass and make its way to the Seante.

The Senate swiftly approved the bill and passed it on to President Biden who then signed it into law. It was good to see this third budget standoff did not come down to the last minute to get resolved, unlike the previous two standoffs.

Other than a better-than-expected US inflation report the week was light on economic news and items that interested me. However, that does not mean the markets did nothing this past week. Let’s see what happened ….

Weekly Market Review

Monday: the indexes ended mostly flat ahead of Tuesday’s pivotal US CPI report. The Toronto Stock Exchange Composite Index (TSX) and the Dow Jones Industrial Average (DJIA) ended higher, while the S&P 500 Index (S&P), and the Nasdaq Composite Index (Nasdaq) ended slightly lower. If the CPI data is lower than expected, the chances increase that the Fed will leave the benchmark interest rate unchanged, leading to a surge in the markets. However, if the CPI data is higher than expected, the chances of a rate hike increase and a pullback in the markets. Oil ended higher when the Organization of Petroleum Exporting Countries (OPEC) raised their forecast for demand growth.

In Canada, higher oil prices helped propel the TSX into the green. In trading in the Canadian sectors, Technology and Energy gained the most, while Healthcare and Utilities dropped the most.

In the US of A, many investors adopted a wait and see attitude while they wait for Tuesday’s CPI report. In trading, Energy and Healthcare had the biggest gains, while Utilities and Technology suffered the biggest losses.

Tuesday: a Black Friday gift in the form of a lower-than-expected US inflation report came early, sending all four indexes soaring. If you are an owner of Nvidia, you had a good day as it had its tenth straight day of gains and briefly reached an all time high before pulling back.

In Canada, the TSX rode the good news out of the US to its fourth straight day in the green and an eight-week high. It was an all-around positive trading day for the Canadian sectors, led by Basic Materials (miners and fertilizer manufacturers) and Financials. Energy was the only sector to end in the red.

In the US, the DJIA gained 1.4% and it was the worst performer of the three. The Nasdaq and S&P had their best day percentage wise since late April. It was a good day for the American sectors with all sectors ending in the green. Leading the way were Utilities and Basic Materials, while Energy and Telecommunications Services trailed the pack.

Wednesday: following on yesterday’s good news inflation report, the markets started today strong but drifted downward throughout the day. Fortunately, they all still ended in the green. Investors now feel the Fed will leave the rate unchanged and start lowering the interest rate in the first quarter of 2024.

In Canada, the TSX posted a fifth straight day of gains thanks to a run on technology companies. Investors believe rate hikes have come to an end and have started moving into riskier stocks like Technology companies. In trading in the Canadian sectors, the Technology and Consumer Cyclicals posted the biggest gains, while Consumer Staples and Energy posted the biggest declines.

In the US, the October retail sales report recorded its first monthly drop since March, although its decline was less than analysts predicted. In trading, Consumer Cyclicals and Industrials had the biggest wins, while Energy and Utilities suffered the biggest losses.

Thursday: after a strong start to November the markets took a breather today, leaving the four indexes largely unchanged. The Nasdaq and S&P ended barely in positive territory while the TSX and DJIA ended slightly lower. Oil prices continued to drop, falling to a four-month low. Investors are concerned about a global drop in demand for oil, resulting from the slowdown in economies around the world.

In Canada, the TSX winning streak came to an end thanks to falling oil prices and doubts about Canada’s economic outlook. In trading, Basic Materials and Industrials had the biggest gains while Consumer Cyclicals and Energy had the biggest declines.

In the US, despite a slowdown in the markets, the Nasdaq rose to its highest closing value since early August. However, a disappointing forecast for the upcoming holiday season by retail giant Walmart (NYSE: WMT) put downward pressure on the markets. On Wall Street, Utilities and Technology advanced the most while Energy and Consumer Staples suffered the greatest drops.

Friday: after the market took a breather yesterday, it was good to see all four indexes regained the upward momentum to end the day higher than they started. Investors are taking favourable inflation and jobs data as signs the interest rates will remain unchanged in both countries for the rest of the year. Although oil prices rebounded sharply today, oil prices have entered a bear market, down more than 20% from their recent highs. The fall in oil prices, leading to lower gas prices, is another reason investors are feeling optimistic about the chances of a rate freeze and for interest rate cuts next year.

In Canada, the TSX reached an eight-week high as higher oil prices drove up the share prices of energy companies. In trading on Bay Street, Energy and Consumer Cyclicals advanced the most, while Consumer Staples and Basic Materials suffered the biggest declines.

In the US, a Fed official acknowledged that inflation is falling but dampened investor optimism when she said the Fed was not ready to rule out another rate hike just yet. On Wall Street, the Energy and Financials sectors posted the biggest gains of the American sectors. Technology and Consumer Staples were the only sectors to lose ground.

Weekly Market and Portfolio Review

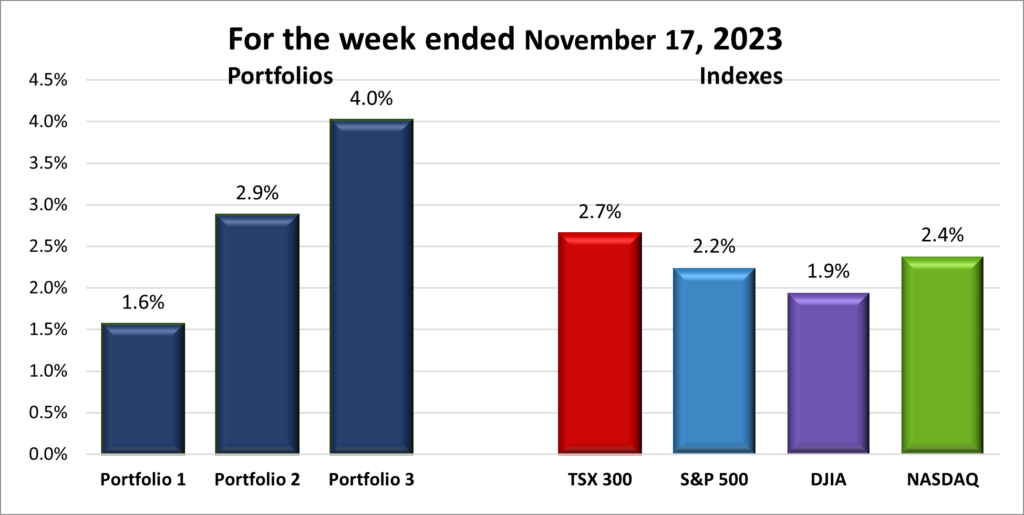

For the week, the TSX (SPTSX) jumped 2.7%, the S&P 500 (SPX) added 2.2%, the DJIA (INDU) rose 1.9% and the Nasdaq (CCMP) advanced 2.4%.

![]() As you can see in the chart above, another good week in the stock markets. All three major US indexes posted a third straight week of weekly gains, and the TSX returned to the weekly wins column. November is shaping up to be one of the best months for stocks this year.

As you can see in the chart above, another good week in the stock markets. All three major US indexes posted a third straight week of weekly gains, and the TSX returned to the weekly wins column. November is shaping up to be one of the best months for stocks this year.

The better-than-expected US CPI report played a big role in driving markets on both sides of the border. A drop in the interest rates of US government bonds also encouraged investors to jump back into the stock market. Signs of slower inflation, more layoffs, and sluggish job creation convinced investors that interest rate hikes might be over. Plus, lower oil prices have given investors hope for potential interest rate cuts next year.

![]() Looking at the chart below, the Portfolios also had a good week, with two of the Portfolios outperforming the top performing TSX. All three portfolios were lifted by the overall rising market. Portfolio 3 had a particularly good week, lifted by a surge in Shopify (TSE: SHOP), its largest holding, and Brookfield Renewables (TSE: BEP.UN). Portfolio 2 also beat the indexes thanks to Brookfield Renewables and Hammond Power Supply (TSE: HPS.A). While Portfolio 1 posted the smallest gain of the Portfolios and the indexes, it was still a gain and not a bad weekly gain at that. Portfolio 1 had several companies gain more than 10% but they were mainly smaller holdings, not big enough to really move the needle. Nonetheless, I am glad they made sizable gains and hope they continue to increase their percentage of the portfolio. Of the bigger positions, Docebo (TSE: DCBO) had a good week, up 10%, but if was offset by a 13.7% drop in Celsius Holdings (NASD: CELH).

Looking at the chart below, the Portfolios also had a good week, with two of the Portfolios outperforming the top performing TSX. All three portfolios were lifted by the overall rising market. Portfolio 3 had a particularly good week, lifted by a surge in Shopify (TSE: SHOP), its largest holding, and Brookfield Renewables (TSE: BEP.UN). Portfolio 2 also beat the indexes thanks to Brookfield Renewables and Hammond Power Supply (TSE: HPS.A). While Portfolio 1 posted the smallest gain of the Portfolios and the indexes, it was still a gain and not a bad weekly gain at that. Portfolio 1 had several companies gain more than 10% but they were mainly smaller holdings, not big enough to really move the needle. Nonetheless, I am glad they made sizable gains and hope they continue to increase their percentage of the portfolio. Of the bigger positions, Docebo (TSE: DCBO) had a good week, up 10%, but if was offset by a 13.7% drop in Celsius Holdings (NASD: CELH).

Overall, I am happy with the performance of all three Portfolios as they all increased in value. Much better than was happening in October. 😊 I hope the markets and the Portfolios continue this upward trend next week and for many weeks to come.

Companies on the Radar

There was some turnover in my Radar List this past week. Dollarama (TSE: DOL) left the list and went into Portfolio 2. Also leaving the list were Gibson Energy (TSE: GEI) and TerraVest Industries (TSE: TVK).

There was some turnover in my Radar List this past week. Dollarama (TSE: DOL) left the list and went into Portfolio 2. Also leaving the list were Gibson Energy (TSE: GEI) and TerraVest Industries (TSE: TVK).

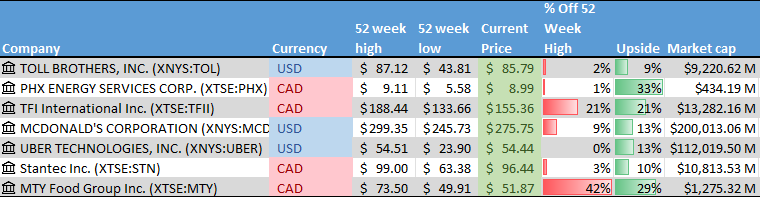

Joining the list are a few names you may recognize and some you will not. A mix of Canadian and American companies, ranging from small to very large companies, by market capitalization.

- McDonald’s (NYSE: MCD), the large cap American fast-food chain.

- Uber (NYSE: UBER), the large cap American ride hailing, delivery and freight handling company (I did not know they handled the logistics of shipping cargo).

- PHX Energy Services (TSE: PHX) a small cap Canadian company that provides drilling technology and services to oil and natural gas exploration companies throughout the world, but mainly in North America.

- Stantec (TSE: STN), a mid size Canadian company that provides a wide range of engineering and construction services to customer throughout North America.

Those four companies join the holdovers listed below:

- Toll Brothers Inc. (NYSE: TOL), a mid cap American company that builds luxury homes throughout the US.

- TFI International Inc. (TSE: TFII), a mid-sized Canadian transportation and logistics company operating across North America.

- MTY Food Group Inc. (TSE: MTY), a small cap Canadian consumer cyclical company that operates and franchises quick service and casual dining restaurants throughout North America and internationally.

The Radar Check was last updated November 17, 2023.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended November 17, 2023: UP ![]()

- Another week, another round of job cuts at Amazon (NASD: AMZN). This time it was their games and Alexa divisions. On the games side, the losses, approximately 18 positions, were the second round of cuts this year. In the Alexa division, it is expected several hundred positions will be cut. Amazon is trimming its losses in unprofitable units to focus their resources on developing and implementing artificial intelligence (AI) across high revenue business units, such as Amazon.com online commerce and Amazon Web Services.

- After investing in the trading app Robin Hood (NASD: HOOD) when it was a startup a few years ago, Alphabet (NASD: GOOGL) announced they had sold all of their shares in the company. No word on if they made money on the transaction but they likely did.

In other Alphabet news, their Google business unit announced a delay of the release of its AI software Gemini AI to the first quarter of 2024. - Celsius Holdings (NASD: CELH) executed a 3 for 1 stock split. Each shareholder of record at the close of business on Nov. 13, 2023, will receive two additional shares of Celsius common stock for each share held as of that date.

- General Motors (NYSE: GM) purchased private company Tooling & Equipment International. Who are they you ask? They are they company the helped Tesla (NASD: TSLA) with gigacasting – the process of casting large body parts for cars to save time and money. The deal should help GM catch up with electric vehicle (EV) leader Tesla.

In other GM news, the United Auto Workers union ratified their deal with GM. - Apple (NASD: AAPL) is working on incorporating a standard that will allow text messaging to operate more smoothly between their iPhones and Android devices. No word if this means iPhone users will receive confirmation their text messages have been received by Android devices.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSE: DIR.UN)

US $

BSR Real Estate Investment Trust (TSE: HOM.U)

Apple Inc.

Costco Wholesale Corp (NASD: COST)

Quarterly Reports

Boston Omaha Corporation

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 13, 2023

- Revenue of $24,548,101 for the three months ended September 30, compared to $21,447,546 for the same period in 2022. An increase of almost 15%.

- Net loss of $1,642,506 for the three months ended September 30, compared to a net loss of $1,408,521 in the same period in 2022.

- Diluted loss per ordinary share of $0.05 for the three months September June 30, compared to a loss of $0.05 per share for the same period in 2022.

- Revenue of $71,580,280 for the nine months ended September 30, compared to $58,635,509 for the same period in 2022. An increase of over 22%.

- Net loss of $3,422,048 for the nine months ended September 30, compared to net earnings of $3,397,733 in the same period in 2022.

- Diluted loss per ordinary share of $0.11 for the nine months ended September 30, compared to earnings of $0.11 per share for the same period in 2022.

Home Depot, Inc.

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 14, 2023

- Revenue of $37,710 for the three months ended September 30, compared to $38,872 for the same period in 2022. A decrease of almost 3%.

- Net income of $3,810 for the three months ended September 30, compared to net income of $4,339 in the same period in 2022.

- Diluted earnings per ordinary share of $3.81 for the three months September June 30, compared to earnings of $4.24 per share for the same period in 2022.

- Revenue of $39,452 for the nine months ended September 30, compared to $40,852 for the same period in 2022. A decrease of over 3%.

- Net earnings of $12,342 for the nine months ended September 30, compared to net earnings of $13,743 in the same period in 2022.

- Diluted earnings per ordinary share of $12.28 for the nine months ended September 30, compared to earnings of $13.37 per share for the same period in 2022.

WELL Health Technologies Corp.

All currency listed in thousands of Canadian dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 14, 2023

- Revenue of $204,461 for the three months ended September 30, compared to $145,789 for the same period in 2022. An increase of over 40%.

- Net loss of $4,482 for the three months ended September 30, compared to net income of $611 in the same period in 2022.

- Diluted loss per ordinary share of $0.03 for the three months September June 30, compared to a loss of $0.02 per share for the same period in 2022.

- Revenue of $544,808 for the nine months ended September 30, compared to $412,623 for the same period in 2022. An increase of over 32%.

- Net loss of $17,125 for the nine months ended September 30, compared to a net loss of $3,409 in the same period in 2022.

- Diluted loss per ordinary share of $0.12 for the nine months ended September 30, compared to a loss of $0.09 per share for the same period in 2022.

SEA Limited

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 14, 2023

- Revenue of $3,310,168 for the three months ended September 30, compared to $3,155,951 for the same period in 2022. An increase of almost 5%.

- Net loss of $569,275 for the three months ended September 30, compared to a net loss of $143,978 in the same period in 2022.

- Diluted loss per ordinary share of $1.01 for the three months September June 30, compared to a loss of $0.26 per share for the same period in 2022.

- Revenue of $9,446,932 for the nine months ended September 30, compared to $8,998,121 for the same period in 2022. An increase of over 73%.

- Net loss of $2,080,610 for the nine months ended September 30, compared to net earnings of $260,466 in the same period in 2022.

- Diluted loss per ordinary share of $3.73 for the nine months ended September 30, compared to earnings of $0.44 per share for the same period in 2022.

Global-e Online Ltd.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 15, 2023

- Revenue of $133,605 for the three months ended September 30, compared to $105,556 for the same period in 2022. An increase of almost 27%.

- Net loss of $33,091 for the three months ended September 30, compared to a net loss of $64,551 in the same period in 2022.

- Diluted loss per ordinary share of $0.20 for the three months September June 30, compared to a loss of $0.41 per share for the same period in 2022.

- Revenue of $384,545 for the nine months ended September 30, compared to $269,184 for the same period in 2022. An increase of almost 43%.

- Net loss of $111,707 for the nine months ended September 30, compared to a net loss of $166,934 in the same period in 2022.

- Diluted loss per ordinary share of $0.68 for the nine months ended September 30, compared to a loss of $1.07 per share for the same period in 2022.

Portfolio 2

Portfolio 2 for the week ended November 17, 2023: UP ![]()

- Guardant Health (NASD: GH) announced that it is working with Samsung Medical Center in South Korea on a blood-based colorectal cancer screening test, ShieldTM.

In separate Guardant news, the company announced it intends to appeal an earlier verdict related to intellectual property claims brought against Guardant. The company is confident that it did not infringe any of the patents in question. - Alimentation Couche-Tard Inc. (TSE: ATD) has partnered with Nayax (NASD: NYAX), a global payments and loyalty platform company, to enable ATD customers to purchase products through various cashless and contactless payment options at their locations throughout North America.

Activity

Bought: Dollarama: Dollarama is a well-established Canadian company that is founder led with a proven record of success. The company has been operating for over 30 years and has consistently generated strong revenue and profits, suggesting the company has a solid business model and is well-positioned for long-term growth.

As a defensive stock, Dollarama is less likely to be affected by economic downturns than other types of riskier, high growth stocks. The company will benefit from increased demand for value-oriented products. This is because consumers are more likely to continue spending at discount retailers like Dollarama even when times are tough. While it will never have explosive growth like riskier technology companies, it is unlikely to experience dramatic swings in share price. Instead, it is a stable and reliable company that will continue to grow my investment.

Dollarama has a strong growth strategy in place. The company continues to expand its store network in Canada while exploring new growth opportunities, such as online sales. It has also expanded into Colombia, Guatemala, El Salvador, and Peru. As well, the company has a history of generating attractive returns for investors through share price appreciation and dividends.

As for the financial numbers, the company has shown impressive financial performance in recent years, with steadily increasing revenue, profitability, Earnings Per Share, and free cash flow.

The risks include facing increased competition from rivals like Walmart and other discount retailers, as well as online marketplaces like Amazon. The company could stumble on its expansion into Central and South America, dragging down the profitability of its overall operations. However, they have a track record of success of competing against major rivals, expansion, and thriving in in tough economic conditions.

Overall, Dollarama is a stable and reliable company, offering diversity to the portfolio. It is a resilient company that has done well in the good times and bad, like the high-interest-rate environment we are currently experiencing.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

SmartCentres Real Estate Investment Trust (TSE: SRU.UN)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week, except for per share data.

Portfolio 3

Portfolio 3 for the week ended November 17, 2023: UP ![]()

- Microsoft (NASD: MSFT) announced they were designing their own semiconductors to help with their AI plans. The chips, the Maia 100 AI accelerator and the Cobalt 100 Arm chip, should help Microsoft lower the cost of building out their internal AI capabilities. Currently there are no plans to sell the chips to other companies.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

SmartCentres Real Estate Investment Trust (TSE: SRU.UN) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

Real Matters Inc.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their fourth quarter 2023 financial results on November 17, 2023

- Revenue of $163,914 for the year ended September 30, compared to $339,642 for the same period in 2021. A decrease of almost 52%.

- Net loss of $6,196 for the year ended September 30, compared to a net loss of $9,265 in the same period in 2022.

- Diluted loss per ordinary share of $0.08 for the year ended September 30, compared to a loss of $0.12 share for the same period in 2022.