Items that may only interest or educate me ….

Canadian Economic news, US Economic news, OpenAI’s Chaotic Leadership Change ….

At the start of each week, I wonder if there will be any investing events that pique my interest enough to write about. The last two weeks have been thin on interesting events, at least to me. However, starting on November 17 it came out that OpenAI’s Chief Executive Officer was unexpectedly let go. And then rehired five days later. I thought this would be a short paragraph or two, but it took on a life of its own. But first …

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Canadian fiscal update

As expected, Canada’s deficit spending exceeded the government’s initial forecast when they originally released their budget in March. And the debt to Gross Domestic Product (GDP) ratio is projected to increase for another year before gradually declining. The debt to GDP ratio is a key indicator of a country’s economic health. A high debt-to-GDP ratio can limit a country’s fiscal flexibility and potentially hinder economic growth.

The Fall Economic Statement (FES) updated the government’s fiscal projections, forecasting a deficit of C$ 40 billion in 2023-24. This was higher than the previously forecast deficit of C$ 32.1 billion, due to the implementation of additional spending measures. Moreover, the FES revealed the cost to service Canada’s debt has risen to C$52.4 billion from March’s forecast of C$ 46 billion. To put that into perspective, the cost of servicing Canada’s debt has now surpassed the budget allocated to Canada’s Armed Forces (C$ 28.9 billion), more than twice what the government will spend on the Employment Insurance program, and enough to cover the money spent on healthcare.

With such a substantial portion of the budget allocated to interest payments, the government says it does not expect to post a balanced budget for the foreseeable future. No where in the FES did the government make a commitment to balance the budget and it is unlikely that the government can resist spending more money in the future, especially with an election coming within two years. Perhaps the government still believes that the “budget will balance itself.” 😊

Despite the growing debt burden, the government has announced a number of new housing initiatives to promote housing construction. However, many of these policies will not kick in for at least another year. While these initiatives may have long-term benefits, they may not provide immediate relief for the current housing crisis Canada is currently experiencing.

Consumer Price Index

October inflation, as measured by Canada’s Consumer Price Index (CPI) rose 0.1%, in line with analysts’ expectations. This follows a 0.1% drop in the monthly pace of inflation in September. On a year over year basis, inflation was up 3.1% in October, lower than analysts’ prediction of a 3.2% increase and significantly lower than September’s 3.8% pace. Core inflation, which excludes the more volatile energy and food prices, rose 0.5% from September to October and 3.4% year over year.

The slowdown in inflation is mostly due to lower gas prices, which fell 6.4% on a monthly basis and is down 7.8% from a year ago. The cost of food also declined monthly, down 0.1%, but food prices are still up 5.4% from October 2022.

This latest data is good news for the BoC in its quest to bring inflation down to its 2% target. However, we are not out of the woods yet. Inflation is still well above the BoC’s target, and there is still a long way to go to get it back down.

The BoC will likely keep interest rates on hold for a while longer to ensure inflation continues to slow down. If it does, we could see interest rates start to fall sometime in early 2024. That would be great news for borrowers and the economy as a whole.

Overall, things are looking up on the inflation front, but we still have some work to do. The BoC appears to be on the right track, and if we can keep inflation on a downward trajectory, we will be in decent shape.

Canadian market volatility

The Canadian Volatility Index (VIXC), represented by the TSX 60 VIXI, ended the week at 13.06, up slightly from last week’s reading of 12.76. Despite the slight increase, investors remain bullish about the markets because of a sense that interest rates in Canada and the US have reached their peak. In the context of the VIXC, a reading above 20 is considered high, while below 20 is deemed low.

Retail Sales

Statistics Canada’s September Retail Trade report indicates a positive shift in retail sales, increasing by 0.6% following a 0.1% dip in August, easily beating analysts’ expectations of a flat outcome. Of the nine subsectors, ‘Motor vehicle and parts dealers’ led in monthly gains, up 1.5%, while the ‘Sporting goods, hobby, musical instrument, book, and miscellaneous retailers’ subsector suffered the largest sales decline, dropping 1.6%.

On a yearly basis, retail sales grew a solid 2.7%. Once again, ‘Motor vehicle and parts dealers’ had the biggest increase, up 7.1%. Conversely, ‘Building material and garden equipment and supplies dealers’ experienced a substantial downturn, with sales falling by 5.7%.

Core retail sales, which excludes gasoline stations, fuel vendors, motor vehicle and parts dealers, fell 0.3% in September, but was up 1.7% year over year.

Contrary to recent indicators suggesting an economic downturn, the September retail data, coupled with an advanced estimate for October indicating a 0.8% increase in sales, is a good sign for the economy. As long as people are still willing to spend money, that’s good news for the economy.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

FOMC minutes

The minutes from the Federal Open Market Committee’s last meeting on October 31 – November 1 were released this past week. In the minutes, members acknowledged progress was being made in bringing inflation down, but it still remained significantly above their 2% target. They recognized the risk of reigniting inflationary pressures if interest rates were lowered too quickly, leading to a stronger-than-expected economic recovery. On the other hand, continued interest rate hikes could pose risks of slowing economic growth or even triggering a recession.

They indicated a cautious approach to future interest rate decisions but suggested a slower pace of monetary tightening (raising interest rates) in the near future. However, they provided their usual caveat that they remain committed to bringing inflation down and will continue to assess incoming data to determine the appropriate path for policy.

American market volatility

By the end of the week, the CBOE Volatility Index (VIX) fell to 12.46, its lowest snice January 2020, down slightly from 13.80 the previous week. The belief that the Fed will leave the benchmark rate unchanged has investors feeling bullish about the stock markets. The slight decline in the VIX suggests investors remain relatively unconcerned about volatility in the American stock markets.

Consumer Sentiment Index

The final reading of the University of Michigan’s Consumer Sentiment Index (CSI) fell to 61.3 in November from a reading of 63.8 in October. However, it was still up 8.1% from November 2022’s 56.7.

This is the fourth month in a row that the CSI has fallen. A less favourable view of business conditions, which fell 15% to its lowest point since July 2022, offset an improved view of personal financial situations.

OpenAI’s Chaotic Leadership Change

OpenAI is a non-profit research company focused on developing safe and beneficial artificial general intelligence (AGI). The company created the artificial intelligence (AI) chatbot ChatGPT, funded in large part by a US$ 13 billion investment from Microsoft (NASD: MSFT).

On November 17, OpenAI’s board of directors abruptly fired Sam Altman as Chief Executive Officer (CEO), citing a lack of transparency and communication regarding critical company decisions. Company president Greg Brockman resigned in protest when OpenAI’s Board of Directors fired Altman. The board consists of prominent AI researchers and entrepreneurs who felt Altman needed to slow down the rollout of AI before it reached a point of no return. They clearly had a different philosophical vision of AI, seeing it as a potentially dangerous technology while Altman and employees view AI as a commercial opportunity (which would make them rich).

Just hours after Altman’s ouster, Microsoft announced that he would join the company as the head of a new AI research division. Brockman and other top researchers from OpenAI were also scooped up by Microsoft. This move was considered by many as a strategic acquisition of top talent in the AI field. It also kept them from joining Microsoft’s competitors.

Altman’s departure from OpenAI sparked a revolt among the company’s employees. Feeling blindsided by the board’s decision and concerned about the loss of their respected leader, 700 of 770 of OpenAI’s workforce threatened to resign and join Altman at Microsoft.

In response to Altman’s dismissal, OpenAI employees penned a letter to the board, stating they were “unable to work for or with people that lack competence, judgment and care for our mission and employees.” Ouch! They demanded Altman’s reinstatement and the resignation of the board members responsible for his removal. They expressed concerns about the company’s future direction and the impact of the board’s actions on OpenAI’s mission. That would have effectively been the end of OpenAI.

The OpenAI board responded to the employee outcry by acknowledging their concerns and promised to review its governance practices. However, they maintained their decision to remove Altman, citing the need for clear leadership and a unified vision for the company’s future.

Before the dust from Altman’s firing even settled, OpenAI’s board began talking to him about returning to the company. Microsoft was OK with this, saying “irrespective of where Sam is, he’s working with Microsoft.”

Sure enough, after a series of intense negotiations and pressure from employees, investors (primarily Microsoft who own 49% of OpenAI), and the public, Altman returned as CEO to OpenAI on November 22. This reversal of the board’s earlier decision reflects the significant impact Altman’s removal had on the company and the widespread support he continues to hold.

OpenAI also established a new board of directors that includes Bret Taylor, formerly co-CEO of Salesforce and Larry Summers, former US Treasury Secretary, along with two directors from the board that dismissed Altman – Quora CEO Adam D’Angelo and OpenAI chief scientist Ilya Sutskever. Previous board members Tasha McCauley, and Helen Toner are out.

Both Altman and Microsoft came out stronger. Altman has consolidated his power and now has fewer checks on his power, although his reputation was tarnished by his abrupt dismissal. Microsoft have secured their relationship with OpenAI, its researchers, and stand to benefit from their further developments in AI. The changes seemed to resonate with investors as Microsoft’s share price rose each of the three trading days during the drama.

OpenAI also came out of this stronger with new leadership that is expected to bring stability and continuity to the company. Governance reforms and a renewed commitment to transparency will also be crucial to ensure the company’s long-term success and maintain public trust as they attempt to commercialize more of their research. Ultimately, the long-term winners will depend on how OpenAI manages its leadership transition, addresses governance issues, and continues to advance its AI research in a responsible and transparent manner.

Despite Altman’s reinstatement, the underlying issues leading to his removal remain unexplained by the previous board. If his prioritization of commercializing AI was indeed the cause, it aligns with OpenAI’s investors’ goals, including Microsoft’s interest in swift technology monetization. However, this revelation may not satisfy those advocating for a more measured approach to AI progress. The long-term success of OpenAI hinges on effectively managing this leadership transition and ensuring responsible, transparent advancement in AI research. I hope one day soon OpenAI is transparent and provides a reason for his dismissal and subsequent triumphant return.

As OpenAI moves forward, it will face the ongoing challenge of balancing innovation with responsible AI development. The company must continue to push the boundaries of AI research while ensuring that its technologies are developed and utilized in a way that benefits society as a whole. The recent drama has highlighted the importance of clear leadership, transparent communication, and alignment between the board, management, and employees in pursuit of this shared mission. By addressing the underlying issues that led to the turmoil and maintaining a commitment to responsible AI development, OpenAI can emerge as a stronger and more respected organization, playing a positive role in shaping the future of AI.

It was Thanksgiving in America this past week. Time for turkey, football, and family. Ok, may be not in that order. 😊 In any event, while the Canadian markets were open for business all week, the American markets were closed on Thursday and closed early on Friday. Besides the drama at OpenAI, let’s see what else happened this shortened week….

Weekly Market Review

Monday: the markets extended their November rally another day, with all four indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – moving upward. Investors continued to respond positively to a better-than-expected earnings season and economic data that showed inflation was falling and are now contemplating when interest rates will start to fall. Oil prices rose after the Organization of Petroleum Exporting Countries (OPEC), plus other major non-OPEC oil exporting countries (together they form OPEC+) consider additional cuts to the supply of oil.

In Canada, the TSX reached its highest point since mid September as investors are betting the Canadian and US central banks have ended their respective rates hikes. In trading in the Canadian sectors, Technology was the big winner, followed by Healthcare. Consumer Staples and Telecommunications Services were the only sectors to end lower.

In the US, last week’s signs of cooling inflation and an impressive performance from Microsoft propelled the US markets higher. Microsoft (temporarily) hired the two top executives at OpenAI, spurring a rally in other technology companies associated with AI. It was no surprise to see Technology as the top performing American sector, followed by Telecommunications Services. Utilities was the only sectors to slip.

Tuesday: the November rally took a breather today with all four indexes closing in negative territory. The minutes from the last Fed meeting revealed that higher interest rates in the US will be staying for longer. The benchmark rate will not come down “until inflation is clearly moving down sustainably toward the Committee’s objective.” Investors’ belief that the US interest rate has reached its peak sent gold prices to a two-week high.

In Canada, the October CPI report indicated inflation fell more than anticipated. Normally I would expect a mini rally on this good news, however, it appears some investors took some gains after the recent runup in the Canadian markets. Lower oil prices led to a downdraft for energy stocks, putting pressure on the TSX. In trading, it was a dismal day for the Canadian sectors with Basic Materials (mining companies and fertilizer manufacturers) the only sector to advance. Among the sectors that fell, Consumer Staples and Consumer Cyclicals dropped the most.

In the US, the Nasdaq and S&P both saw their winning streaks come to an end. The DJIA also ended lower as many investors decided to book gains going into the American Thanksgiving holiday. In trading, Basic Materials and Healthcare posted the biggest gains, while Technology and Consumer Cyclicals suffered the biggest falls.

Wednesday: the markets resumed their November rally with all four indexes ending in the green as the American markets prepare to shut down for the Thanksgiving holiday. Oil prices dropped after a meeting of the OPEC+ nations was pushed back a few days. Analysts suggested the rescheduling was so all member nations could get on the same page about future production cuts.

In Canada, after hearing BoC Governor Tiff Macklem suggest interest rates may have peaked, investors now believe the BoC will leave interest rates unchanged at their upcoming meeting. Rising expectations that we have seen the last of rate increases has left investors in a good mood, and a good mood usually means markets move higher. In trading, the Consumer Staples and Technology sectors had the biggest gains of the Canadian sectors, while Energy and Consumer Cyclicals suffered the biggest declines.

In the US, slowing demand for labour and a slowdown in business spending on equipment suggests the economy is gradually slowing. However, the economy remains strong enough to avoid a recession. This latest economic news has left investors with a sense of optimism that the Fed has finished with rate hikes. On the last trading day before the Thanksgiving holiday, the Consumer twins – Staples and Cyclicals posted the biggest gain, while Energy, Basic Materials, and Telecommunications Services were the only sectors to end lower.

Thursday: It was a slow day for the North American stock markets as the American exchanges were closed for the US Thanksgiving Day holiday. However, for the Canada’s stock exchanges it was just another day at the office, albeit with less trading volume thanks to the American holiday. The TSX was in positive territory for the entire day before a late minute slide left the index barely in the green, having gained 0.01%. Industrials and Energy had good days, while Consumer Staples fell back after yesterday’s rally.

Friday: trading volume was light in both countries today as the US markets closed early as part of the American Thanksgiving holiday. In the shortened trading session, it was a mixed day that saw the TSX and the Nasdaq end the day lower, while the S&P and DJIA advanced. Oil prices continued to fall because of a dispute between OPEC+ members. Saudi Arabia wants more production cuts while African members do not.

In Canada, retail sales for September came in higher-than-expected retail but investors still feel the BoC will hold interest rate at its current 5.0% level at their upcoming meeting. In a slow day of trading on Bay Street, Healthcare and Basic Materials made the largest advances, while Utilities and Technology posted the heaviest losses.

In the US, the Nasdaq was dragged down by technology heavyweights Nvidia (NASD: NVDA) and Google’s parent Alphabet (NASD: GOOGL). Otherwise, it was a quiet but good day in trading that saw almost all sectors end higher, led by the Energy and Healthcare sectors. The only sector to not post a gain was Technology.

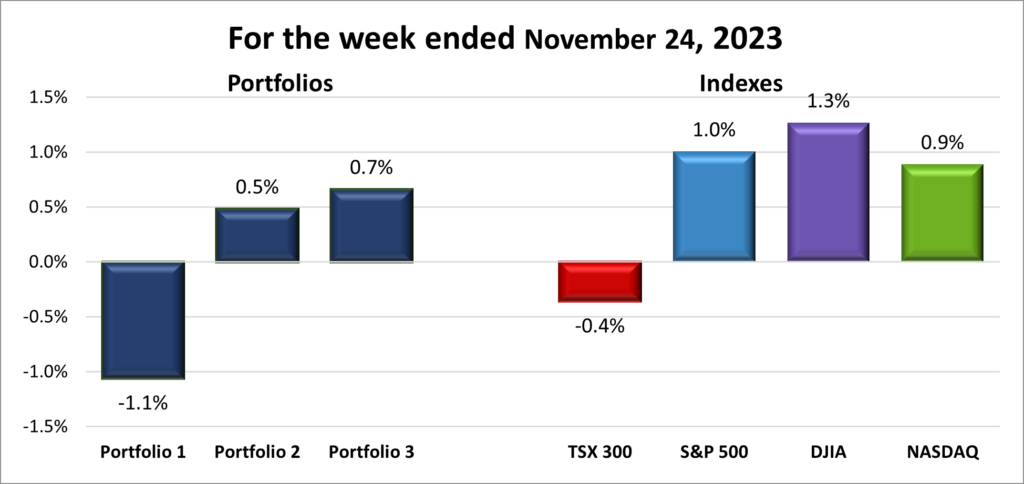

Weekly Market and Portfolio Review

For the week, the TSX (SPTSX) fell 0.4%, the S&P 500 (SPX) advanced 1.0%, the DJIA (INDU) rose 1.3% and the Nasdaq (CCMP) gained 0.9%.

| Index | Weekly Streak |

| TSX: | 1-week losing streak |

| S&P: | 4-week winning streak |

| DJIA: | 4-week winning streak |

| Nasdaq: | 4-week winning streak |

![]() After another positive week, the three major American indexes extended their winning streaks to four weeks, while the TSX narrowly missed extending its winning run. The DJIA is on track for its best month since October 2022, while the Nasdaq and S&P 500 are poised for their best months since July 2022. The main driving force behind the bullish sentiment this week was strong earnings reports from some of the largest U.S. companies, which boosted investor confidence. Additionally, comments from Fed officials suggesting a potential slowdown in the pace of interest rate hikes further fueled investor optimism.

After another positive week, the three major American indexes extended their winning streaks to four weeks, while the TSX narrowly missed extending its winning run. The DJIA is on track for its best month since October 2022, while the Nasdaq and S&P 500 are poised for their best months since July 2022. The main driving force behind the bullish sentiment this week was strong earnings reports from some of the largest U.S. companies, which boosted investor confidence. Additionally, comments from Fed officials suggesting a potential slowdown in the pace of interest rate hikes further fueled investor optimism.

Despite the positive news on inflation, the resource heavy TSX retreated due to a decline in energy prices. While inflation continues to drop, this largely stems from lower gas prices.

![]()

![]() The portfolios had a mixed performance this week, with the percentage gains of Portfolios 2 and 3 slightly outweighing the percentage loss of Portfolio 1. Portfolio 1, apart from an 11% gain by Cargojet (TSE: CJT), had gains and losses that were roughly evenly split. However, it was weighed down by Nvidia, the largest holding, after the company delayed the sales of AI chips designed for the Chinese market to comply with US export restrictions. Portfolio 2 recorded a 5% gain from MongoDB (NASD: MDB) along with declines from the energy companies, otherwise companies whose share price gained slightly outnumbered the companies whose share price dropped. Portfolio 3 had no significant moves either way. Fortunately, the companies that advanced were more than the companies that fell.

The portfolios had a mixed performance this week, with the percentage gains of Portfolios 2 and 3 slightly outweighing the percentage loss of Portfolio 1. Portfolio 1, apart from an 11% gain by Cargojet (TSE: CJT), had gains and losses that were roughly evenly split. However, it was weighed down by Nvidia, the largest holding, after the company delayed the sales of AI chips designed for the Chinese market to comply with US export restrictions. Portfolio 2 recorded a 5% gain from MongoDB (NASD: MDB) along with declines from the energy companies, otherwise companies whose share price gained slightly outnumbered the companies whose share price dropped. Portfolio 3 had no significant moves either way. Fortunately, the companies that advanced were more than the companies that fell.

Its likely that if it were not for the drop by Nvidia, all three portfolios would have posted weekly gains. However, with Nvidia having increased over 225% so far in 2023 its hard to object to a 5% drop this week. 😊

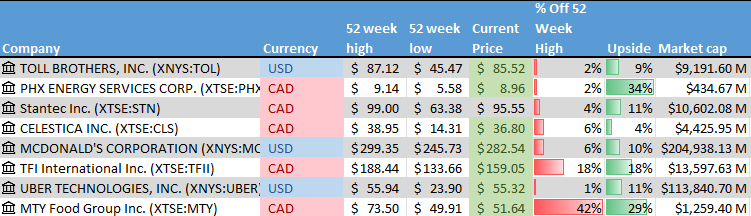

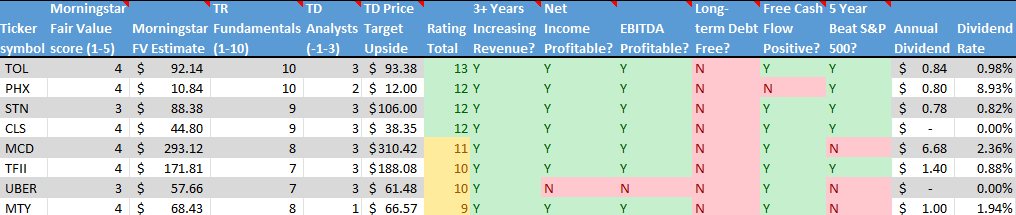

Companies on the Radar

For some reason, most companies that appear on my radar come from the Technology sector. All three portfolios are already biased towards technology, so I try to find companies from other sectors to diversify and improve the resilience of the portfolios. Try as I might, technology companies keep popping up on my radar and this past week was no exception.

For some reason, most companies that appear on my radar come from the Technology sector. All three portfolios are already biased towards technology, so I try to find companies from other sectors to diversify and improve the resilience of the portfolios. Try as I might, technology companies keep popping up on my radar and this past week was no exception.

Coming onto my radar was Celestica Inc. (TSE: CLS), a medium sized Canadian company that manufactures electronic products and provides supply chain services to companies around the world.

Celestica joins the seven companies from last week, listed below:

- Toll Brothers Inc. (NYSE: TOL), a mid cap American company that builds luxury homes throughout the US.

- PHX Energy Services (TSE: PHX) a small cap Canadian company that provides drilling technology and services to oil and natural gas exploration companies throughout the world, but mainly in North America.

- Stantec (TSE: STN), a mid size Canadian company that provides a wide range of engineering and construction services to customer throughout North America.

- McDonald’s (NYSE: MCD), the large cap American fast-food chain.

- TFI International Inc. (TSE: TFII), a mid-sized Canadian transportation and logistics company operating across North America.

- Uber (NYSE: UBER), the large cap American ride hailing, delivery and freight handling company (I did not know they handled the logistics of shipping cargo).

- MTY Food Group Inc. (TSE: MTY), a small cap Canadian consumer cyclical company that operates and franchises quick service and casual dining restaurants throughout North America and internationally.

The Radar Check was last updated November 24, 2023.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended November 24, 2023: DOWN ![]()

- General Motors’ (NYSE: GM) Cruise self driving unit is looking for new leadership. Co-founder and chief product officer Daniel Kan resigned a day after Cruise CEO Kyle Vogt quit. This comes as Cruise’s autonomous electric vehicles (EV) are undergoing a safety review by the National Highway Traffic Safety Administration (NHTSA).

- Nvidia, the leader by a country mile in AI chips, delivered once again on its revenue forecast. Revenues were up 206%, net income up 1,259%. However, the share price dropped on concerns US government restrictions would negatively impact sales in Nvidia’s third largest market going forward. Nvidia has told customers in China that the launch of a new artificial intelligence chip has been delayed until the first quarter of 2024. The H20 chip was designed for its Chinese customers to comply with US export rules.

- Docebo (TSE: DCBO) announced their current CEO Claudio Erba will resign as the CEO and a director and become the company’s Chief Innovation Officer, effective February 28, 2024. Current President and Chief Operating officer Alessio Artuffo will become the interim CEO on March 1. The board of directors is likely to name Artuffo as the permanent CEO but is going through a proper due diligence process for the next CEO.

- On the busiest shopping weekend of the year, Amazon (NASD: AMZN) was hit by strikes at multiple fulfillment centres across Europe. Strikes were to take place in over twenty countries from Black Friday through Cyber Monday. Amazon said 86% of its European workforces had shown up for work on Black Friday and so far, strikes have had no impact.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Pulse Seismic Inc.

US $

No US$ dividends this past week.

Quarterly Reports

Nvidia Corporation

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on November 21, 2023

- Revenue of $18,120 for the three months ended October 29, compared to $5,931 for the same period in 2022. An increase of almost 206%.

- Net income of $9,243 for the three months ended October 29, compared to net income of $680 in the same period in 2022.

- Diluted earnings per ordinary share of $3.71 for the three months ended October 29, compared to earnings of $0.27 per share for the same period in 2022.

- Revenue of $38,819 for the nine months ended October 29, compared to $20,923 for the same period in 2022. An increase of over 85%.

- Net earnings of $17,475 for the nine months ended October 29, compared to net earnings of $2,954 in the same period in 2022.

- Diluted earnings per ordinary share of $7.01 for the nine months ended October 29, compared to earnings of $1.17 per share for the same period in 2022.

Portfolio 2

Portfolio 2 for the week ended November 24, 2023: UP ![]()

- Microsoft temporarily hired Sam Altman, the former CEO of OpenAI, and former OpenAI President Greg Brockman who resigned in protest when OpenAI’s Board of Directors fired Mr. Altman. However, both returned to OpenAI within a few days.

- TC Energy (TSE: TRP) received approval from the US Federal Energy Regulatory Commission for their Virgina Reliability Project (VRP). The VRP is an expansion project to replace two segments of the existing pipeline system. The project is scheduled to start by April 2024 and will create 3,500 jobs in Virginia.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSE: DIR.UN) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week, except for per share data.

Portfolio 3

Portfolio 3 for the week ended November 24, 2023: UP ![]()

- The takeover bid by Brookfield Asset Management’s (TSE: BAM) for Australia’s Origin Energy was postponed after the BAM led group revised its offer to try and satisfy Origin’s largest shareholder, AustralianSuper. Brookfield’s bid was likely to fail, and the revised bid does not look much better than the previous bid. AustralianSuper controls 17% of the outstanding shares in Origin and have said they will vote against BAM’s offer.

Activity

Sold: Fortuna Silver Mines (TSX: FVI) This was a relic of my earlier investing days when you had to use a stockbroker to buy and sell stocks. Since I know nothing about mining, I followed his recommendation. My mistake was going outside my circle of competence. The stock was never going back to get back to the purchase price, so I decided to unload it.

This experience reminds me of a valuable lesson I learned a while ago: never invest in something you do not understand. As a result of making this mistake once too often, I developed my own due diligence process which I go through when considering investing in a company.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

No quarterly reports this past week.