I hope everyone enjoyed the Labour Day long weekend, as well as the short work week.

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, Oil production cuts, A sales dip for consumer cyclical companies, …

Canadian Economic news

Bank of Canada pauses interest rate hikes

As widely anticipated, the Bank of Canada (BoC) maintained Canada’s benchmark interest rate at 5% following two consecutive 0.25% hikes in June and July. The central bank acknowledged an unexpected economic contraction in the second quarter, primarily influenced by various domestic and global factors. There was an unexpected slowdown in China, leading to a decline in global economic growth. However, the American economy remains strong led by strong consumer spending.

On the domestic front, several factors contributed to the economic contraction, including reduced consumer spending, wildfires across the country, a softening labour market, and the impact of higher interest rates. Despite this economic contraction, inflation inched higher, driven primarily by increased gas prices, partially attributable to additional carbon taxes imposed by the federal government. A declining economy and high inflation is not a good combination.

The BoC is particularly worried that prolonged high inflation could complicate efforts to bring it down to the bank’s 2% target. The bank has chosen to maintain the current rate for now as the previous hikes work their way through the Canadian economy. The impact of interest rate adjustments often takes up to 18 months to be felt and it has been nearly 18 months since the BoC first started increasing the rate. While the rate remains unchanged, the bank has left the door ajar for potential future rate hikes.

The BoC’s benchmark rate serves as the foundation for Canada’s borrowing costs, influencing the lending rates set by the country’s banks. When the BoC increases the benchmark rate, these banks subsequently raise the rates at which they lend money to consumers and businesses.

Labour Force Survey

Statistics Canada released the Labour Force Survey (LFS) for August 2023, showing that the Canadian economy added 40,000 jobs during the month. This figure doubled analysts’ expectations, as they had predicted an increase of only 20,000 positions.

Upon closer examination of the data, a slightly different picture emerges. Canada’s population grew by 100,000 individuals, resulting in a 0.1% drop in the employment rate, which now stands at 61.9%. To merely keep up with this population growth, Canada would need to generate 50,000 new jobs.

Despite job gains in each of the previous three months, the unemployment rate remained unchanged at 5.5%. Analysts had expected a fourth consecutive increase that would have pushed it to 5.6%.

Finally, average hourly wages for August recorded a 4.9% increase, slightly lower than the 5.0% gain seen in July.

The LFS is a monthly survey that collects information on the labour market, employment, unemployment, and various other labour-related data in Canada. It plays a key role in helping policymakers and analysts understand the dynamics of the Canadian labour market, identify trends, and make data-driven decisions.

US Economic news

Last week, several reports that the Federal Reserve (Fed) relies on for its decision-making process were released. This week, there were no headline economic reports closely followed by the Fed, nor myself. However, one piece of news that would have undoubtedly caught the Fed’s attention is the increase in energy prices, which could potentially result in rising inflation, as discussed in the following report.

Oil production cuts

Saudi Arabia and Russia have announced an extension of their oil production cutbacks for an additional three months, bringing the total duration to six months. In this arrangement, Saudi Arabia will continue with its 1 million barrels per day production cut until December, keeping production at a historically low 9 million barrels per day (bpd). Simultaneously, Russia will maintain its export cutbacks by 300,000 bpd. The primary goal behind these measures is to bolster oil prices, a strategic move intended to benefit the economies of both nations.

This extension carries significant implications. For consumers, it will likely mean rising gasoline prices, as tighter oil supplies generally result in increased prices at the pump. Additionally, businesses dependent on transportation could face higher fuel costs, potentially affecting their bottom line. Furthermore, home and business heating expenses could rise, impacting household budgets. Moreover, products and services linked to oil, such as food and plastics, might see price hikes, adding to increased consumer expenses.

From an investor’s perspective, the cutbacks will have a mixed impact. On one hand, higher oil prices can boost the profits of oil producers like Canadian Natural Resources (TSX: CNQ) and Chevron (NYSE: CVX), as they command more money for their oil. On the other hand, industries sensitive to energy costs, such as airlines and transportation firms, may face increased expenditures on fuel, impacting their profitability. Additionally, there is the prospect of an adverse impact on stock markets in general. Rising oil prices can trigger inflation, increasing operational costs for businesses and potentially curbing consumer spending. This, in turn, can hamper economic growth and affect stock markets. Just as important, the BoC and the Fed are in the midst of trying to bring inflation back to their respective 2% target. After the upheaval caused by higher interest rates, the last thing we need is for inflation to start to rise.

Overall, the decision by Saudi Arabia and Russia to extend the oil production cutbacks is a significant development that could have a major impact on the global economy and the stock markets.

A sales dip for consumer cyclical companies?

Consumer cyclicals companies are concerned that their sales could take a hit come October when US student debt payments resume. Many individuals, during the debt repayment freeze, redirected their funds that were initially designated for debt payments towards spending on various goods and services, from clothing and dining out to travel.

Now, as they must resume student debt payments, this extra spending cash will return to servicing their debts. The exact amount of these monthly debt payments and the number of individuals affected remain unknown, but this shift is expected to withdraw a substantial sum from the economy, potentially impacting the companies that benefited from the debt repayment freeze.

It was short week in the North American markets but that does not mean nothing happened. Let’s see what moved the markets this past week….

Weekly Market Review

Monday: The Canadian and American exchanges were closed for the Labour Day holiday.

Tuesday: All four indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – ended lower as concerns about the global economy have investors looking for less risky opportunities. Oil prices were a lone bright spot, ending higher after Saudi Arabia and Russia announced they would extend their production cuts another three months through the end of 2023.

In Canada, investors await tomorrow’s BoC’s decision on whether they will hold or raise the benchmark interest rate. The Healthcare, Energy and Consumer Staples were the only Canadian sectors to end in the green. Basic Materials (miners and fertilizer manufacturers) and Telecommunications Services dropped the most.

In the US, investors are still digesting last week’s array of economic data. They are pretty confident the Fed will hold off on an increase this month but are looking for clues to the next meeting of the Fed. The Technology and Energy sectors were the only American sectors to register a gain, while Basic Materials and Industrials had the biggest declines.

Wednesday: The four indexes stretched their losing streaks another day as investors become cautious after reports of a slowing European economy which would lead to lower demand.

In Canada, despite the BoC leaving the benchmark interest rate at 5.0%, the TSX still ended lower on concerns the rate could remain at that level for longer. It was a day where every Canadian sector ended in the red. Consumer Staples and Healthcare dropped the least, while Utilities and Industrials had the biggest plunges.

In the US, investors are concerned about lingering inflation after data showed stronger than expected growth in the services sector hitting a six-month high. Investors are worried interest rates could remain elevated much longer than originally thought, and possibly move higher at the Fed’s November meeting. In trading, the defensive sector Utilities was the only sector to advance, barely making it into the green. On the losing side, the interest sensitive Technology and Consumer Cyclicals had the worst days.

Thursday: The DJIA was the only index to finish the day in the green as the September slump continues. Investors are worried interest rates will remain high as the latest US economic data shows the US economy continues to fire on all cylinders. After nearly two weeks of pushing higher, oil prices fell on data suggesting weaker demand was on the horizon.

In Canada, BoC Governor Tiff Macklem said interest rates may not yet be high enough to bring inflation down to the 2% target, sending the TSX lower. In trading, Utilities and Healthcare were the only Canadian sectors to post gains, while Consumer Cyclical and Consumer Staples declined the most.

In the US, Apple (NASD: AAPL) dragged down the Nasdaq and S&P after China banned the use of iPhones by government officials. As Apple’s share price tumbled, it started to drag down some of the other mega cap technology stock prices. In trading, the defensive sectors Utilities, Healthcare and Consumer Staples were the only American sectors to end higher. The Basic Materials and Technology sectors dropped the most.

Friday: A mixed day in the markets that saw the TSX end lower while the American indexes ended slightly higher. The good news was the Fed hinted it could hold off on an interest rate hike in September, overriding concerns that the strong US economy will lead to interest rates remaining higher for some time. Outside of the US, investors are concerned about a slowdown in the global economy. Oil rebounded from Thursday’s pullback on concerns of tighter supplies.

In Canada, the TSX was weighed down by better-than-expected employment data which caused investors to worry about higher interest rates. In trading on Bay Street, the Healthcare and Consumer Staples sectors led all Canadian sectors, while the Technology and Industrials sectors suffered the biggest drops.

On Wall Street, investors were worried interest rates will stick around longer than anticipated. In trading, the Utilities and Energy sectors led the advance, while the Industrials and Telecommunications Services declined the most.

Weekly Market and Portfolio Review

For the week, the TSX (SPTSX) added 3.1%, the S&P 500 (SPX) gained 3.5%, the DJIA (INDU) grew 3.2% and the Nasdaq (CCMP) rose 3.4%.

![]() If you thought the end of last week would generate some upward momentum for the North American stock markets, you would have been wrong. As you can see in the graph above, the TSX fell the most among the four major indexes. While the Bank of Canada (BoC) opted not to raise the Canadian benchmark interest rate, concerns persisted that the current elevated rates might remain in place for an extended duration. The following day, the BoC Governor hinted that the rate might need to climb further if they were to reach their 2% inflation target.

If you thought the end of last week would generate some upward momentum for the North American stock markets, you would have been wrong. As you can see in the graph above, the TSX fell the most among the four major indexes. While the Bank of Canada (BoC) opted not to raise the Canadian benchmark interest rate, concerns persisted that the current elevated rates might remain in place for an extended duration. The following day, the BoC Governor hinted that the rate might need to climb further if they were to reach their 2% inflation target.

Across the border in the US, market performance did not fare much better. The robust US economy prompted worries among investors that inflation could linger, thereby extending the period of high interest rates. The S&P and Nasdaq experienced further declines when China implemented a ban on Apple devices for government employees. This move raised concerns, not only due to the ban itself but also because of the potential implications for Apple’s sales and operations in China. China is the company’s largest international market and a crucial production hub. Apple is the largest component of both the Nasdaq and the S&P, which explains its significant impact on these indexes. It is not a member of the DJIA, which probably accounts for why the DJIA had a better week than the other two. Fortunately, on Friday, all three snapped their respective losing streaks.

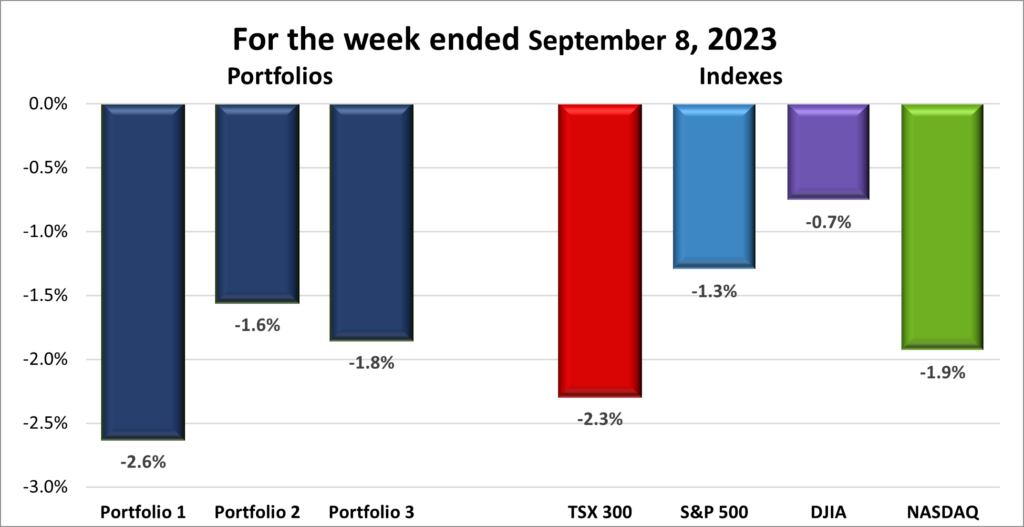

![]() The three Portfolios had another challenging week, as depicted in the chart below. The overall market downturn had a significant impact on all three portfolios. However, Portfolio 1 suffered the biggest losses due to its holdings in Apple shares. While Portfolios 2 and 3 do not have any Apple shares, they were not immune to the broader sell-off in technology companies. This sell-off was triggered by Apple’s disappointing news, as outlined above. As a result, all three portfolios had a miserable week.

The three Portfolios had another challenging week, as depicted in the chart below. The overall market downturn had a significant impact on all three portfolios. However, Portfolio 1 suffered the biggest losses due to its holdings in Apple shares. While Portfolios 2 and 3 do not have any Apple shares, they were not immune to the broader sell-off in technology companies. This sell-off was triggered by Apple’s disappointing news, as outlined above. As a result, all three portfolios had a miserable week.

Companies on the Radar

No new companies came onto my radar this past week. However, I dropped Walmart (NYSE: WMT) from the list because I’m looking for a bit more growth potential at this time. Otherwise, five holdovers from last week remain on my radar:

No new companies came onto my radar this past week. However, I dropped Walmart (NYSE: WMT) from the list because I’m looking for a bit more growth potential at this time. Otherwise, five holdovers from last week remain on my radar:

- Dollarama (TSX: DOL), a large Canadian company that operates dollar stores across Canada.

- Deere & Company (NYSE: DE), a large American company that manufactures and sells agricultural equipment worldwide.

- Restaurant Brands International Inc. (TSE: QSR): A large cap Canadian consumer cyclical company that operates in the North American quick serve restaurant industry. The company owns Tim Horton’s, Burger King, and Popeye’s Louisiana Kitchen among others.

- MTY Food Group Inc. (TSE: MTY): A small cap Canadian consumer cyclical company that operates and franchises quick service and casual dining restaurants throughout North America and internationally.

- Crown Castle Inc. (NYSE: CCI), a large cap American company that owns and operates cell towers throughout America. The company is currently at its lowest price in five years and offers a 6+% dividend.

The Radar Check was last updated September 8, 2023.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended September 8, 2023: DOWN ![]()

- Apple signed a deal with British chip designer and manufacturer Arm Holdings that will supply chip technology to Apple to at least 2040. Many of Apple’s products are based on or utilize Arm based technologies. This deal will secure access to Arm products for a long time. Arm develops chips for phones and tablets and licenses the technology to semiconductor manufacturers.

Separately, China banned the use of Apple iPhones, and other foreign devices, from government workplaces. It will be interesting to see how this plays out since almost all of Apple’s devices are made China. As well, China accounts for about 20% of Apple’s revenue. - Tesla (NASD: TSLA) has delayed start of production at their new Mexican plant. It was originally scheduled to start production in 2025 but has been pushed back to 2026 – 2027.

- It appears General Motors (NYSE: GM) and its unions are at loggerheads over their ongoing contract negotiations. GM offered a 10% wage increase, plus two additional 3% annual lump sum payments over four years. The union is asking for a 46% wage increase.

- Nvidia (NASD: NVDA) announced they will partner with India’s Tata Group to build an artificial intelligence (AI) supercomputer. Nvidia plans to use its latest GH200 Grace Hopper Superchip, as well as an AI cloud. Tata plans to use the infrastructure and capabilities to boost the company’s AI guided transformation.

Activity

Sold ZIM Integrated Shipping Services Ltd. (NYSE: ZIM) I invested in Zim when supply chains were congested, and shipping companies were charging a premium for their services. ZIM also offered dividends based on their quarterly net income, which were quite substantial due to their excellent earnings.

Fast forward two years, and many of the supply chain issues have been resolved. However, the marine shipping industry has entered a downturn with no signs of improvement on the horizon. The share price has plummeted by nearly 80%, and the company is no longer generating net income, resulting in the suspension of dividends.

This is another instance where waiting too long to sell the shares proved unfortunate. 😞 Fortunately, the dividends collected over the last two years mitigate some of the loss, resulting in a net loss of 34%. Not good, but better than an 80% loss.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Nuvei Corp (TSX: NVEI)

US $

Costco (NYSE: COST)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended September 8, 2023: DOWN ![]()

- Airbnb (NASD: ABNB) was added to the S&P, forcing any funds that track the S&P to purchase shares.

- Brookfield Infrastructure (TSX: BPI.UN, BIPC) announced their acquisition of Triton Internationals (NYSE: TRTN) was approved by Triton’s shareholders. Triton sells and leases intermodal containers to shipping lines and freight forwarding companies. The deal is expected to close in the next few months.

- Guardant Health (NASD: GH) announced that the Geisinger Health Plan now provides coverage for the Guardant Reveal blood test that detects circulating tumor DNA in blood after cancer treatment, including surgery. It is the first blood-only liquid biopsy test commercially available for minimal residual disease testing. These tests help oncologists identify cancer patients with residual or recurring disease who may benefit most from additional therapy or surveillance.

Separately, the Japanese Ministry of Health, Labour, and Welfare approved Guardant’s Guardant360(R) CDx liquid biopsy test for use as a companion diagnostic to select patients with inoperable advanced or recurrent non-small cell lung cancer.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

Mitek Systems, Inc.

All currency listed in thousands of US dollars.

Selected highlights from their first quarter 2023 financial results on September 5, 2023.

- Revenue of $45,703 for the three months ended December 31, compared to $32,473 for the same period in 2022. An increase of almost 41%.

- Net income of $4,730 for the three months ended December 31, compared to net income of $3,124 in the same period in 2022.

- Diluted earnings per ordinary share of $0.10 for the three months ended December 31, compared to earnings of $0.07 per share for the same period in 2022.

Alimentation Couche-Tard Inc.

All currency listed in millions of US dollars.

Selected highlights from their first quarter 2024 financial results on September 6, 2023

- Revenue of $15,623.2 for the twelve weeks ended July 23, compared to $18,657.7 for the twelve weeks ended July 17, 2022. A decrease of over 16%.

- Net income of $834.1 for the twelve weeks ended July 23, compared to net income of $872.4 for the twelve weeks ended July 17, 2022.

- Diluted earnings per ordinary share of $0.86 for the twelve weeks ended July 23, compared to earnings of $0.85 per share for the twelve weeks ended July 17, 2022.

Portfolio 3

Portfolio 3 for the week ended September 8, 2023: DOWN ![]()

- Microsoft’s (NASD: MSFT) bundling of software is being looked at by the US Federal Trade Commission as well as regulators in the European Union for anticompetitive practises. Zoom Video Communications (NASD: ZM) has accused Microsoft of giving preference to its own products at the expense of competitors.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

Enghouse Systems Limited

All currency listed in thousands of Canadian dollars.

Selected highlights from their third quarter 2023 financial results on September 7, 2023

- Revenue of $110,997 for the three months ended July 31, compared to $102,111 for the same period in 2022. An increase of almost 9%.

- Net income of $17,567 for the three months ended July 31, compared to net income of $18,081 in the same period in 2022.

- Diluted earnings per ordinary share of $0.32 for the three months ended July 31, compared to earnings of $0.33 per share for the same period in 2022.

- Revenue of $330,893 for the nine months ended July 31, compared to $319,525 for the same period in 2021. An increase of over 3%.

- Net earnings of $47,126 for the nine months ended July 31, compared to net earnings of $57,549 in the same period in 2022.

- Diluted earnings per ordinary share of $0.85 for the nine months ended July 31, compared to earnings of $1.03 per share for the same period in 2022.