Items that may only interest me ….

For some analysts, semiconductor (chips) manufacturers are considered a proxy for economic growth. That is not good news as lately chipmakers have issued ominous warnings about the economy. Last week, AMD and Samsung both revealed that demand for their chips has plunged — a bad omen for the entire tech sector.

Adding further to weakness in the semiconductor industry, the US imposed export controls to deprive China of advanced chips used for artificial intelligence, supercomputers, and weapons, as well as the tools needed to make them. The new rules not only require US companies to get special permission to send the chips to China, but they also ban countries worldwide from selling to China if they are made with US equipment. The loss of the Chinese market can only hurt semiconductors manufacturers.

On the other hand, there is still tremendous demand for chips as automakers are still desperate for chips to complete the manufacture of their respective vehicles. As well, some of the biggest technology companies such as Amazon (NASD:AMZN), Microsoft (NASD:MSFT) and Google (NASD:GOOGL) are rapidly building out data centres to support their growing cloud computing and artificial intelligence initiatives. All these data centres require a tremendous number of advanced semiconductors to supply the needed computing power for these projects. These two industries will not pick up all the slack caused by the loss of the Chinese market, but it will consume a considerable amount.

While there may be a glut of chips on the market for devices that benefited from the ‘stay at home’ and remote working spawned by the global pandemic (personal computers, mobile devices), there does not appear to be a slowing of demand for the more advanced chips required by big technology companies nor the automotive industry.

Recent market declines have been tied in part to increasing fears among investors that aggressive rate hikes and the pace of the hikes (from almost zero in March to today’s 3.00% – 3.25% range) by the US Federal Reserve Bank (Fed) could tip the world’s largest economy (the US economy) into a recession. Add a spike in COVID-19 cases in China, leading to more lockdowns and less demand for products, have led to growing pessimism in the markets.

This past week, investors are reacting to a few items this week that will not make them nor the Fed happy:

- The US Producer Price Index (PPI) report, measures the change in wholesale prices, showed prices rose 0.4% in September on a month-on-month basis. Analysts were expecting a 0.2% increase. On an annualized basis, the PPI rose 8.5% in September, higher than expected, but slightly lower than August’s 8.7%. The PPI report is considered a forward-looking measure of inflation. If this is correct, inflation will remain high.

- The US Consumer Price Index for September came in at 8.2% year over year and 0.4% month over month. This is well over the Fed’s target of 2% so they can be expected to act forcefully in their fight against inflation.

- US Federal Reserve Bank (Fed) members are unanimous in their need to maintain aggressive interest rate hikes and the need to keep the benchmark interest rate high long enough to allow the hikes to kick in and start lowering inflation.

The Fed has been banging the drum all summer that the cost of taking too little action outweighs the cost of taking too much action. With stronger-than-expected US PPI and CPI, and the Fed’s desire to maintain a high interest rate, the Fed is signalling they will not only raise the US benchmark interest rate by at least 0.75% at their November 2 session, but they plan to keep the interest rate high to drive down prices.

These are challenging times not only for the Fed, but also Canada’s Bank of Canada (BoC). Each central bank has two primary tasks to perform in their respective countries. The first is to limit inflation, which requires restraining the growth of the economy. This is what they are currently attempting to do by raising interest rates. The other task is to support employment, which calls for economic growth. These two tasks are in opposition to each other. A delicate balancing act is required to pull it off, but currently the Fed is prepared to sacrifice the latter for the former.

In Canada, the news is not good but its better than in the USA. The Canadian job market is slowing down, as are average hourly wages. Both signs that the BoC’s interest rate hikes are slowly kicking in. Next week the Statistics Canada will present the Canadian CPI numbers and they will shine a light on the current rate of inflation in Canada. If the key inflation data – CPI and Core CPI (CPI without food and fuel costs factored in) – are lower, hopefully the BoC will be able to throttle back the next interest rate increase to 0.5% rather than the 0.75% increase they have done the last four times.

Unfortunately, the Canadian economy is not in a vacuum and the higher-than-expected US inflation prompted analysts to raise their expectations for how high the BoC will raise the Canadian interest rate. Some are predicting Canada’s benchmark interest rate may reach 4.25% by the middle of 2023, which would be the highest level since 2008. I can already feel the sting of higher interest payments. ☹

Enough of the doom and gloom, let’s see what mischief the markets got up to this past week….

Weekly Market Review

Monday: The Canadian markets were closed for Thanksgiving. In the US, the stock markets were open for business on Columbus Day. The S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) all ended the day lower, with the Nasdaq closing at its lowest since July 2020. Fears of higher interest rates sending the US into a recession and a slide in semiconductors were the main causes of all three Indexes ending lower. Semiconductors dropped because of US government restrictions on selling advanced chips to China. The Consumer Staples and Basic Materials (natural resources and fertilizers) sectors were the only sectors to finish higher, while Energy and Technology sectors had the biggest declines.

Tuesday: The week got off to a tough start for the North American stock markets as only DJIA was able to limp into positive territory. Investors were skittish over concerns of a global recession induced by aggressive interest rate hikes. It did not help that China increased their Covid-19 restrictions, due to a rise in infections, which could lower demand for oil and other resources.

In Canada, the Toronto Stock Exchange Composite Index (TSX) fell to its lowest point since March 2021. Consumer Staples was the only sector to end the day higher, while the Technology, Energy and Financial sectors all fell more than 2%.

In the US, as investors wait for this week’s Producer Price Index (PPI) and the Consumer Price Index (CPI) to reveal the latest inflation numbers, they were hit with news the International Monetary Fund predicting a dismal 1.6% growth of the American economy for 2022.

Wednesday: The four major North American Indexes all ended lower, barely in the red, essentially flat with a slight downward tilt. The big news of the day, actually two news items, was the US PPI came in higher than expected; and the notes from the US Federal Reserve Bank’s (Fed) last meeting showed the Fed members were determined to remain aggressive in their fight against high inflation. Analysts and investors now await tomorrow’s US CPI report.

Meanwhile, in the Canadian markets, the TSX ran its losing streak to five sessions despite six of the eleven sectors ending slightly higher. The Consumer Staples, Healthcare and Consumer Cyclicals sectors led the upward push, minimizing the drag caused by the Utilities, and Telecommunications Services sectors.

In the US, the three major American indexes continue to drift lower as investors fret about another aggressive rate hike by the Fed. The S&P posted its sixth consecutive loss, dropping down to its lowest point since November 2020. In the stock market, three of the eleven sectors edged into positive territory – Consumer Staples, Energy and Consumer Cyclical.

Thursday: After an early morning plunge, all four Indexes rebounded to end the day well in the black. The cause of the morning drop was the US CPI report for September showed inflation came in higher than expected at 8.2% year over year (compared to an estimated 8.1%), and 0.4% month over month (compared to an estimated 0.2%). The Core CPI (excludes volatile energy and food prices) rose 6.6% since last September, its highest level since 1982, and rose 0.6% from August to September.

In Canada, the TSX end higher as all Canadian sectors ended on the winning side, led by the Energy sector which was propelled higher by rising oil prices. TSX investors also helped lift the Index higher as they covered their short positions (see ‘Short a Stock’ on the Investing Terms page, under ‘Terms heard in the investing world’ section) they had placed in anticipation of high inflation numbers driving down the share price of numerous companies.

In the US it was a similar story to Canada, investors were covering short positions led to a broad-based surge across all three American Indexes. The mid day surge helped the S&P break into the win column after six straight losing days.

Friday: The day started out strong in the major North American Indexes but quickly reversed itself, ending the day firmly lower. Every sector, in both the Canadian and the American markets, ended the day in the red. In Canada, the resource heavy TSX was weighed down by losses in the Basic Materials (lower commodity prices) and Energy (lower oil prices) sectors.

In the US, inflation concerns and worries about future interest rate hikes by the Fed weighed on the markets. The biggest drags on the American Indexes were the Basic Materials, Consumer Cyclicals, and Energy sectors all dropped more than 3%.

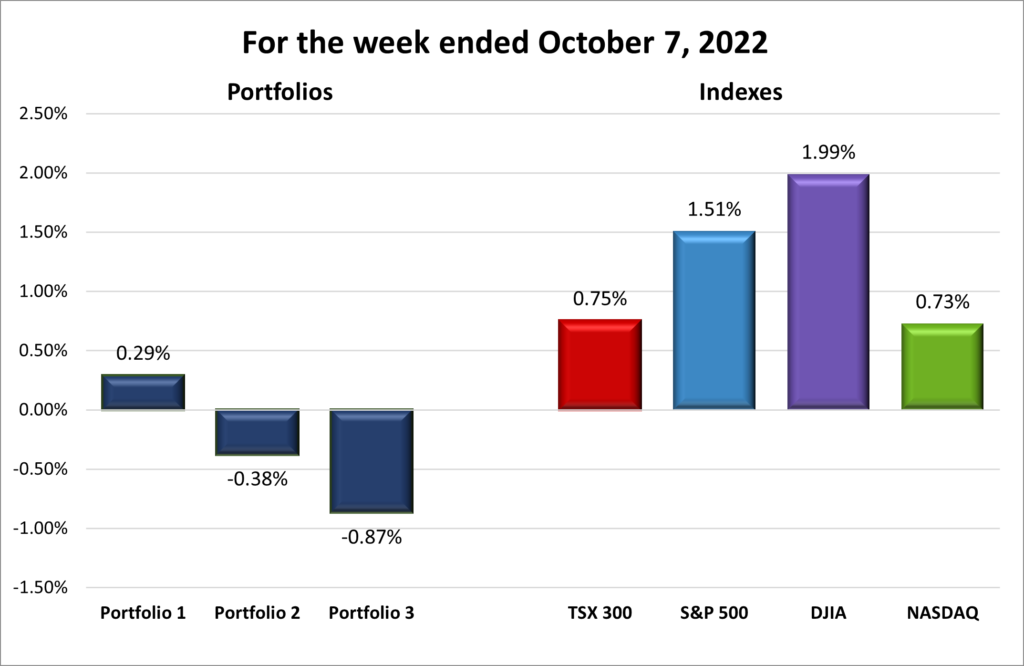

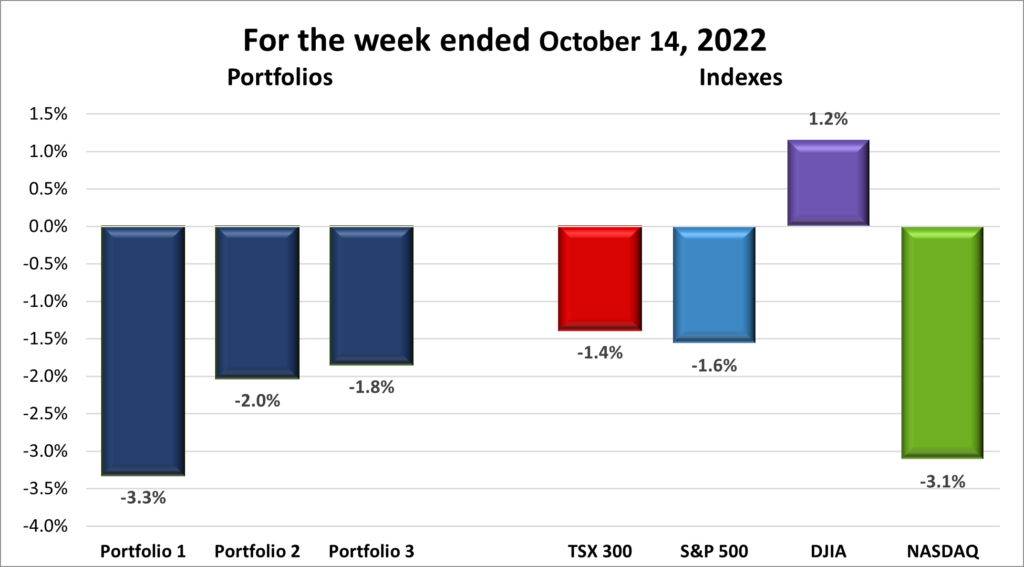

For the week, the TSX dropped 1.4%, the S&P 500 lost 1.6%, the Dow gained 1.2% and the Nasdaq tumbled 3.1%.

Weekly Portfolio Review

Looking at the above chart reminded me of the famous groundhog Wiarton Willie and Groundhog Day. Legend has it Willie the ground hog would stick his head out of his winter hibernation hole and if he saw his shadow, there would be six more weeks of winter. In this case, its like Mr. Market wakes up, pops his head up, does not like what he sees and decides to go back to sleep. In the chart above, all four Indexes were drifting downward, they popped up for a day, and they dove back down. This seems to be a common occurrence in 2022 – the occasional upward surge, only to retreat and continue the downward trend of 2022.

Once again, the Nasdaq and the S&P, with their growth-oriented stocks fell the hardest as higher and rising interest rates take a bite out of growth companies. Lower prices for oil and natural resources dragged the TSX into the red while the DJIA collection of 30 large, blue-chip companies was able to limit Friday’s pullback and keep the Index in the black.

As for the three Portfolios, going into Friday, all were barely underwater, down less than 1%. As you can see in the chart below, Friday’s sell off pushed all three considerably lower, especially Portfolio 1 with its preponderance of Nasdaq listed companies. Portfolio 2 is still being dragged down by (NASD:MDB). As for Portfolio 3, no big drop by any of the companies, just caught up in the overall direction of the stock market.

Companies on the Radar

One company moved off the radar and into a Portfolio, making way for a new company on the radar.

STMicroelectronics N.V. (NYSE:STM), a European manufacturer of semiconductors (chips) for the automotive industry, recently came on my radar. Given the four automotive companies held in the Portfolios are all claiming sales are down due to a shortage of chips, I see plenty of opportunity for STM. The first step is put the company through my Radar Check.

Otherwise, with the markets continuing their downward spiral, I am going to sit on the sidelines waiting to take advantage of dips like the one this past week. Amazon remains on the radar.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended October 14, 2022: DOWN ![]()

- General Motors (NYSE:GM) is getting into the energy storage business. GM’s new energy division, GM Energy, is leveraging their Ultium battery technology and will offer two new stationary storage solutions – Ultium Home and Ultium Commercial – as well as solar panels and hydrogen fuel cells. GM will now be competing with Tesla (NASD:TSLA) in the energy services industry as well as electric vehicles.On a side note, the Ultium power unit was the primary reason I decided to invest in GM. The addressable market for energy storage and management is estimated to be US$ 120 billion or more. If their Ultium battery technology is as good as they say it is, it will be the powerplant for most of their electric vehicles, they will be able to license it to other car manufacturers, and I can see them grabbing a good piece of the emerging energy storage industry.

- Once again Alphabet is being dragged in front of the European Commission, the European Union’s competition bureau. This time Alphabet’s Google business unit is being investigated for its digital advertising practises. If the Commission finds against Alphabet, they could face their fourth billion euro fine.

Activity

Bought: Ferrari (NYSE:RACE) Purchased a few shares in Ferrari when the market dipped upon the release of the US CPI report that consumer prices rose more then expected. I have always wanted to own a Ferrari but never able to purchase an actual Ferrari, so instead I decided to become an owner of the legendary Italian car maker. 😊

Aside from being able to say one owns a Ferrari, investing in the company is a bit of a sleeper investment. Ferrari is a powerful brand with tons of racing history and prestige, providing it with a competitive advantage that very few other car makers can claim. To maintain the prestige of the brand, Ferrari limits the production and sale of their cars to maintain exclusivity and pricing power. On the financial side, revenues, net income, and margins are all increasing. In June 2020, the company started a share buyback program. As well, Ferrari has recently entered the SUV market with their Purosangue SUV. Finally, they have released two hybrid models and have announced a fully electric Ferrari for 2025. Given the price tag of existing Ferrari sports car, I expect these SUVs, hybrids and electric cars will carry hefty price tags, and more importantly for investors, a sizable margin to add to the bottom line. 😊

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Yellow Pages Ltd (TSX:Y)

US $

Innovative Industrial Properties Inc (NYSE:IIPR)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended October 14, 2022: DOWN ![]()

- Cameco (TSX:CCO) and Brookfield Renewable Partners (TSX:BEP.UN and TSX:BEPC) partnered to acquire nuclear power plant equipment maker Westinghouse Electric for almost US$ 8 billion. When the deal closes, Brookfield will own 51% of Westinghouse with Cameco controlling the remaining 49%. The deal comes amid renewed interest in nuclear energy as the world looks for energy alternatives. Cameco is one of the largest miners and suppliers of uranium fuel, while Brookfield Renewables manages many renewable power facilities throughout the world. This partnership and acquisition seem like a natural for all parties.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Summit Industrial Income REIT (TSX:SMU.UN)

Brookfield Renewable Partners LP (TSX:BEP.UN)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended October 14, 2022: DOWN ![]()

- The Royal Bank of Canada (TSX:RY) is being investigated by Canada’s Competition Bureau for alleged ‘greenwashing’ or exaggerating their environmental record. Banks have started to find themselves in the crosshairs of activists for their support of oil and natural gas companies. The Royal Bank believes the complaint is without merit. I suspect other Canadian banks that deal with energy companies will see similar complaints come there way.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

goeasy Ltd (TSX:GSY)

Alvopetro Energy Ltd (TSXV:ALV)

Brookfield Renewable Partners LP (TSX:BEP.UN)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.