Fractional shares….

And so ends the third quarter of 2022. After a rally to start the quarter, the markets ended with a thud! The Toronto Stock Exchange Composite Index (TSX) is doing the best of the four major North American Indexes, and it is in a market correction (down more than 10% from recent highs). The three major American exchanges – the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – are each in bear markets (down more than 20% from recent highs).

While it is great to see the end of September, historically the worst month for investing, October is not a whole lot better. Although there are no facts to back this up, October is perceived to be when share prices will fall, if not crash. This perception is called the “October Effect.” Looking back, Black Tuesday occurred October 29, 1929, and triggered the Great Depression; and Black Monday, the stock market crash that saw the DJIA fall 22% in one day, occurred October 19, 1987. Let us hope there is not a similar stock market crash instore for us this October, but if there is I hope you have some investing cash available to take advantage of the companies that go on ‘sale.’

The big economic news this past week came from across the Atlantic. In the United Kingdom, the British government announced plans to lower taxes with no corresponding spending reductions, plunging the UK into a self-inflicted financial crisis. The British pound fell to its lowest ever exchange rate with the US dollar, and the cost of government debt soared. It also sparked a sell-off of stocks and bonds traded on the London Stock Exchange (LSE), wiping out at US$ 500 billion in combined value. As a result, the Bank of England intervened and bought British government bonds to stem the fall in British financial assets.

As I am not invested in any companies on the LSE it did not directly impact the companies I own, but it did send out ripples that were felt globally. The North American stock markets had a roller coaster ride this past week and one of the causes was what occurred in the UK. I bring this up to illustrate how actions in one part of the world can ripple across the world and impact the stock markets here in Canada and the USA.

Staying in Europe, inflation for the 19 member European Union is expected to be above 10% for September, up from 9.1% in August. Already high inflation that continues to rise all but guarantees the European Central Bank will need to aggressively raise interest rates to get inflation down to their 2% target.

The summer rally is gone, the Indexes are back at their June lows, and the bottom is not in sight. Given the ongoing interest rate hikes the central banks (Bank of Canada and the US Federal Reserve) are implementing to battle inflation, I am not surprised a vast majority of investors believe their investments will be worth less by the end of 2022. I am one of those. My question, what are the other investors seeing that leads them to believe they will make a profit on their investments this year? 😊

With a disappointing third quarter in the rear-view mirror, we now turn our attention to the final quarter of 2022. I do not expect the markets to make a furious comeback to end in positive territory, but I would like to see them bottom out to set the stage for a better 2023. But before we get ahead of ourselves (what could possibly go wrong? 😊), let’s take a look back at this past week….

Weekly Market Review

Monday: The week got off to a bumpy start with all four major North American Indexes finishing lower. Canada’s Toronto Stock Exchange Composite Index (TSX) fell to an 18-month low as energy (lower oil prices) and natural resources companies dropped on concerns of ongoing interest rate hikes.

In the US, those same concerns over interest rates sent the S&P 500 Index (S&P) to its lowest point since December 2020, and the Dow Jones Industrial Average (DJIA) into bear market territory (drop of 20% or more from recent highs). Oddly, the growth-oriented Nasdaq Composite Index (Nasdaq) was the best of the three American Indexes even though it declined as well (0.6%).

Tuesday: Ongoing concerns about rising interest rates, worsened by the European energy crisis, led to another day of losses for three of the four Indexes. Surprisingly (at least to me), it was the high growth-oriented Nasdaq that was the lone bright spot.

In Canada, the TSX had its sixth straight losing session, closing at its lowest point since March 2021. Despite a strong showing from the Energy sector, thanks to rising oil prices, it was not enough for the TSX to break its losing streak.

In the US, members of the US Federal Reserve (Fed) were talking about the need for additional rate hikes, possibly as much as 1% by the end of 2022. Talks of higher interest rates did not help the S&P as it fell for the sixth straight session, its longest decline since February 2020. The Nasdaq was the only Index to advance thanks to gains by some of its biggest names such as Tesla (NASD:TSLA), Nvidia (NASD:NVDA) and Apple (NASD:AAPL).

Wednesday: After the Nasdaq broke into positive territory yesterday, the other three major North American Indexes finally got back on the winning side with big gains today. In Canada, the TSX had its best day in four months thanks to strong performances from the Energy (higher oil prices), Basic Materials (Natural resources and fertilizers) and Technology sectors.

In the US, the S&P snapped its six-day losing streak thanks to its best day since early August. A broad-based rally that saw all eleven S&P sectors rise also helped the DJIA break its six-session skid and the Nasdaq to start a winning streak (albeit two days).

Thursday: Well, that was a short rally – one day – only to see most of Wednesday’s gains disappear thanks to a broad-based sell off today. In Canada, the TSX fell on losses in the Technology and Utilities sectors. Even higher oil prices were unable to lift the TSX into the black.

In the US, fears the Fed is prepared to put the US economy into a recession to bring down inflation sent share prices tumbling. On the S&P, the share prices of almost 20% of the companies that make up the S&P 500 reached new 52-week lows. Nasdaq approached its lowest levels since June 2022.

Friday: The week went out with a whimper today as all three American Indexes ended lower and the TSX barely squeaked over the line, gaining 0.01%. In Canada, the TSX started strong but fell back to earth, ending the day essentially flat. If it were not for the dominance of the Energy and the Basic Materials sectors on the TSX, the TSX would be down a similar amount as its American cousins. It was a mixed bag for the Canadian sectors as four of eleven sectors ended in the black, led by the Basic Materials sector. Of the 7 sectors that ended in the red, Consumer Staples fell the most.

In the US, in morning trading, all three Indexes were in the black before diving into the red in afternoon trading. All eleven sectors ended lower as the S&P posted its sharpest September decline in 20 years. On the DJIA, all 30 companies ended the day lower.

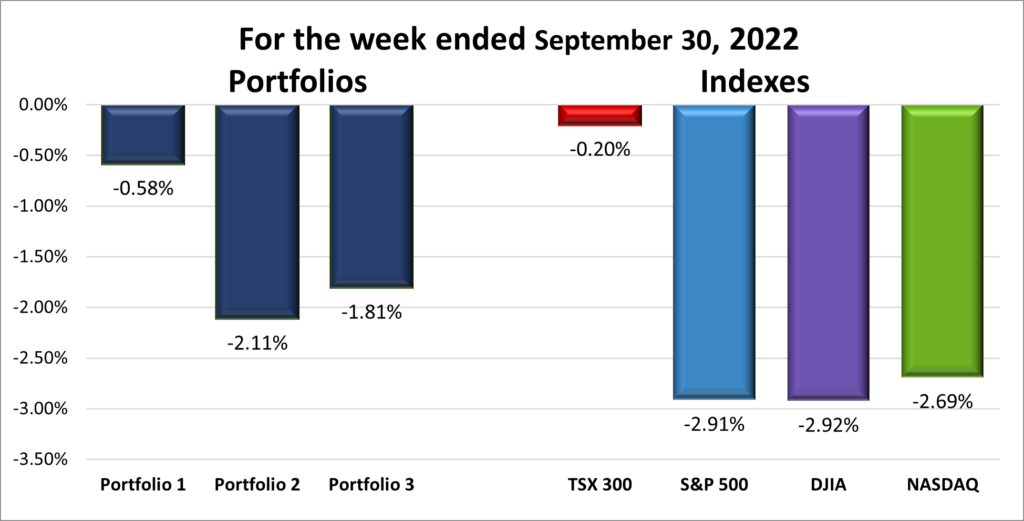

For the week, the TSX dropped 0.20%, the S&P 500 fell 2.89%, the Dow lost 2.91% and the Nasdaq sank 2.69%.

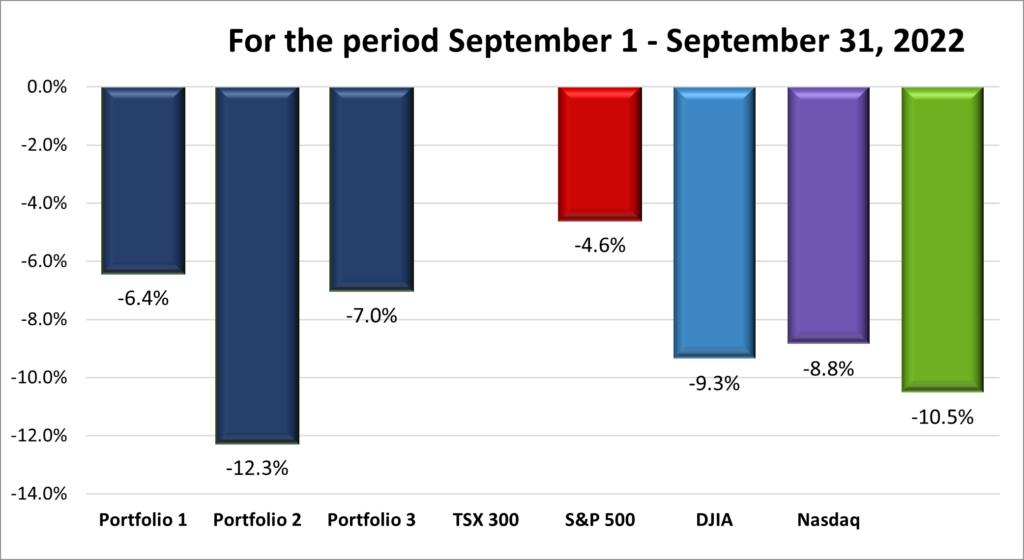

For September, the TSX dropped 4.59% and all three American indexes posted their second consecutive monthly losses. The S&P 500 fell 9.3%, the Dow dropped 8.8% and the Nasdaq plunged 10.5%.

Weekly Portfolio Review

Well, that was not a pleasant week. All three American Indexes declined almost 3%, leaving the TSX as the best of a bad lot. The TSX continues to benefit from being heavy with oil, natural gas and natural resource companies, keeping it from falling as far as its American cousins. In the US, it was not so much the US interest rate hike from the previous week as it was the concerns the Fed would continue their aggressive rate hikes that drove the markets down. Analysts are already talking about US interest rate hikes going north of 4% by the end of the year, with additional hikes to follow in 2023. For companies with significant debt this is not good news and investors reacted accordingly. Surprisingly, for me anyway, the growth-oriented Nasdaq did not fall the farthest.

As for the portfolios, as long as the Indexes keep retreating there is nothing to do but hang in until the stock market turns upward. The good news is none of the Portfolios fell as far as the American Indexes. Not exactly a compliment. 😊 Earlier in the year I was impressed how Portfolio 2 seemed to fair better than the more aggressive Portfolios 1 and 3. However, this has been twice in the last three weeks it has dropped the most of the Portfolios. Not sure what to make of that.

If last week was bad, the chart for September looks even worse! The interest rate hikes and talks of additional, aggressive hikes and fears of a recession in both Canada and the USA certainly took a bite out of all four Indexes.

As for the Portfolios, not a good month, not a good month at all. I was hoping to say, ‘at least the Portfolios didn’t drop as hard as the American Indexes,’ but Portfolio 2 blew up that plan. It was a shock to see Portfolio 2 down by 12%. Drilling down, I saw that the portfolio’s big winner for the last two years, MongoDB (NASD:MDB), dropped 38% in September. I am guessing if I took MongoDB out of the equation, Portfolio 2 would be more in line with the other two portfolios. The good news, analysts are still very high on the company with an average upside estimate of 82% increase in share price. 😊

Let us hope that the October Effect proves to just be a perception and there are no negative surprises. Stay tuned!

Companies on the Radar

Given the freefall of the various North American stock markets, I plan to sit on the sidelines for a bit and let things play out. As you can see on the charts below, Amazon (NASD:AMZN) and Ferrari (NYSE:RACE) have been trending downward since late 2021 highs. I am hoping the share price for Amazon and Ferrari continue their downward trajectory so I can buy lower, and I will be able to save a few bucks. I know I should not be playing this game of timing the market, but I do not see the economy suddenly turning around sending share prices higher.

Both the Amazon and Ferrari charts show their respective share price since September 30, 2021, to September 20, 2022, the 50-day moving average share price, and the 200-day moving average share price. Both companies respective share prices are below both the 50 day and 200-day average. Generally, I want to see the share price moving towards or higher than the averages.

As well, if you look at either the Amazon or Ferrari chart, starting at the highest point (late 2021), then draw a line touching the top of the other peaks, you will see the line is heading down, to the right. This is my trend line and I generally want the trend to be going up, to the right. However, since I am looking at buying both companies, I do not mind it going down to the right. If/once I buy ownership in Amazon or Ferrari, I want it going up to the right faster than a Ferrari on a straight away. 😊

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended September 30, 2022: DOWN ![]()

- General Motors’ (NYSE:GM) self-driving start-up Cruise is forgoing a partnership with Nvidia to develop its own processors that will be deployed in Cruise vehicles by 2025.

- Despite the recent completion of upgrade to their Shanghai gigafactory, Tesla has indicated they plan to run at 93% capacity for the rest of the year. They will produce 20,500 units a week. Still an impressive number.

- Cargojet (TSX:CJT) plans to increase its fleet of aircraft to 40 by the end of 2022. With the six additional planes, Cargojet’s overnight network will now reach 16 Canadian cities and over 90% of the Canadians.

- Apple has cancelled plans to increase production of its new iPhone 14s this year after an expected surge in demand failed to materialize.

Activity

Sold AcuityAds (TSX:AT) Bought these shares under C$2, watched it run up to C$ 32 and fall back to its current levels. I have not been impressed with the last two quarterly reports as revenues seem to be moving from their old system to their new system. Management had been talking up how their new ad management system would drive organic growth, but revenues seem to be largely coming from their old generation ad system. I kept thinking they would rebound but they never have and with the economy going in the tank I want to book some gains.

I was once told that when a company’s share price takes off without any significant underlying improvement by the company (as was the case with Acuity), sell the shares and take the money. The share price will fall back once the herd moves onto the newest shing object. I should have heeded that warning. I will next time.

Lesson: when investor sentiment pushes the share price well ahead of the company’s underlying performance, take at least some money off the table.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Canadian National Railway Co (TSX:CNR)

Shaw Communications Inc (TSX:SJR.B)

US $

NVIDIA Corp (NASD:NVDA)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended September 30, 2022: DOWN ![]()

- Recently, the Bank of Nova Scotia (TSX:BNS) has undergone a few changes at its highest levels. Scott Thomson, a board member for six years, will takeover from existing Chief Executive Officer Brian Porter starting December 1. Mr. Porter will stick around in an advisory role until April 30, 2022. Mr. Thomson is currently the CEO of Finning International (TSX:FTT), a company worth 1/20 the market value of BNS. I am not so concerned about the changes at the executive level, I am more focused on the company’s valuation and the banks long term prospects.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Brookfield Infrastructure Partners LP (TSX:BIP.UN)

Brookfield Infrastructure Corp (TSX:BIPC)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended September 30, 2022: DOWN ![]()

- Shopify (TSX:SHOP) is going into the hardware business. The company announced POS Go, a point-of-sale hardware device that allows merchants to accept payments, monitor sales and manage their inventory.

- Forrester Research named Cloudflare (NYSE:NET) as a Leader in The Forrester Wave: Web Application Firewalls, Q3 2022 report. Cloudflare received full marks in 10 criteria.

- Brookfield Renewable Partners (TSX:BEP.UN) continues to invest in renewable energy companies. It closed on its acquisition of Standard Solar and their 500 Megawatts (MW) of assets; and bought Scout Clean Energy and their 1,200 MW of wind assets and a over 22,000 MW of wind, solar and storage capacity over 24 states. This brings Brookfield’s US assets almost 60,000 MW of energy capability.

- As of September 30, Ethereum was trading at C$ 1,834.57. A far cry from the purchase price of a small amount in November 2021 at C$ 6137.23. ☹ Glad it was only a very small amount. 😊

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Brookfield Asset Management Reinsurance Partners Ltd (TSX:BAMR)

Brookfield Renewable Corp (TSX:BEPC)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.