When I originally wrote about these two topics in May 2022, the three American Indexes – the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – were trending downward since the start of 2022. As you can see in the chart below, there had been mini rallies in February and mid March, but if you were to draw a line connecting the tops of any rally you would see the downward trend, especially at the end of March. This is even more noticeable if you connect the bottoms.

In mid April, the Toronto Stock Exchange Composite Index (TSX) joined the downward trend. As of May 13, 2022, the TSX had fallen almost 5.8%, the S&P was down over 16%, the DJIA dropped 12% and the Nasdaq had plunged over 27%. I would rather not know the losses of the three portfolios, so I did not bother calculating their losses. Since they are all more technology oriented, I would guess they were closer to the Nasdaq’s performance (and they have not gotten any better since I originally wrote this five months ago). ☹ Rather than lament my losses on paper, I decided I would write about two characteristics I look for when investing in companies.

So, without further ado, …. my lightly edited take on how tailwinds and headwinds can impact the growth of companies.

With the markets maintaining a downward trajectory its hard to stay engaged in investing and it can be downright depressing. I know I am not following the markets as much as in the past because its discouraging watching my money disappear.

This week, rather than talk about the market, I have decided to talk about one of the things I look for when searching for companies to own – tailwinds.

Tailwinds

If you have ever flown, you have probably heard the terms headwinds and tailwinds. Tailwinds propel a plane forward faster, helping them burn less fuel and possibly arriving at their destination sooner. Headwinds slow the plane down, causing it to burn more fuel and possibly arriving late at their destination. In investing, tailwinds are conditions or trends that will continue through economic ups and downs and help boost a company’s revenues, profitability, and share price. Headwinds, on the other hand, function as a drag on a company and can slow down or even cause growth to decline. Obviously, you want to invest in companies that are benefiting from one or more tailwinds and avoid headwinds as much as possible. Unfortunately, some headwinds you cannot avoid. Let us take a look at how these ‘winds’ can impact your wealth generation plans. This week I am going to talk about how I have looked for tailwinds when selecting companies to invest in.

The tailwind is your friend, an even better friend when you can ride multiple tailwinds.

When I got back into investing in 2018, before I started looking for companies to invest in, I looked for tailwinds, or industries that had trends that could boost a company’s earnings and share price. Once I identified a few tailwinds, I looked for the best companies to take advantage of those tailwinds. If the company was riding more than one tailwind, all the better.

One of the first tailwinds I came across was the demand for chips (of the silicon variety, not the potato kind). Cloud computing was and remains all the rage, artificial intelligence was and continues to improve and expand, the growing demand for electric and autonomous vehicles, the rollout of 5G networks, and the metaverse is supposedly the next big thing (each of these can be seen as a tailwind). Rather than try to pick a top company in each area, I focused on what they had in common – semiconductors, or chips. With that in mind I went looking for semiconductor companies. I ended up investing in Nvidia (NYSE:NVDA), Skyworks Solutions (NASD:SWKS) and Lattice Networks (NASD:LSCC). The tailwinds behind the semiconductor industry are tremendous and all three companies have done very well, and I expect them to continue to ride the numerous tailwinds that drive the demand for semiconductors.

Another industry that has quietly picked up a tailwind is cybersecurity. Cybersecurity was on my radar but not really front and centre. It came to the forefront in mid 2020 when a friend was almost the victim of a computer fraud attack. With increased numbers of people working from home (work from home tailwind) during the Covid-19 pandemic, governments, companies, and individuals suddenly had many more systems to protect. Cyberattacks range from malware to ransomware to state sponsored hacking. The Russian invasion of Ukraine has only heightened the threat of cyberattacks and the need for governments and businesses to up their security game.

After identifying the cybersecurity tailwind, I contacted a friend in the computer security industry to get some insight into the top cybersecurity companies. I decided to become a minority owner 😊 of Crowdstrike (NASD:CRWD) and Cloudflare (NYSE:NET). Crowdstrike has evolved into a cloud-based security platform (there is that cloud trend again, another trend within the cybersecurity trend) with multiple market opportunities. Cloudflare also provides network security solutions, as well as Content Delivery Services (CDN), a geographically distributed group of computer systems which “work together to provide fast delivery of Internet content.” Its like bringing YouTube videos closer to you to reduce the time to access and stream them. I even started using Cloudflare’s free Virtual Private Network (VPN) client Warp 1.1.1.1 to protect my data when I access the Internet. Both companies continue to ride the tailwind for the need to secure remote workers, within the larger cybersecurity tailwind. So far 2022 has been a rough year for all technology companies, including cybersecurity companies, but the demand for cybersecurity remains.

In summary, I try to identify tailwinds and then find the top companies riding those tailwinds. Great companies will do well in the long run but if they can ride a tailwind or two, they will generate better earnings and their share price will rise higher, faster. Next time I will talk about headwinds which can slow the growth of investments and even cause your portfolio to decline.

Rather than dwelling on the pain of 2022, I am going to talk about the conditions I look to avoid when selecting companies to own. Last week I talked about tailwinds that can accelerate the growth of companies when looking for investment opportunities. Headwinds are the opposite of tailwinds. They are unseen forces that drive down growth and earnings of companies. Obviously, you want to avoid companies with their own unique headwinds, but there are other headwinds you cannot avoid. These headwinds are the ones I am going to talk about today.

Headwinds

Unfortunately for us investors, in 2022 the markets in general have been facing the opposite of tailwinds – headwinds. There has been no shortage of headwinds facing the economy and the stock market for a while now. At the end of 2021, investors were concerned about how COVID-19 and its numerous variants would impact the economy. They were also worried about rising inflation and how it would inevitably lead to higher interest rate which would cut into revenues as companies are forced to pay more to service their debt. More money to pay down debt means less money to grow the company and earnings, or to go to shareholder friendly actions such as raise dividends or share buyback programs. In 2022, another headwind was added to Covid-19 and inflation concerns – the Russian invasion of Ukraine.

The Covid-19 pandemic continues to impact the global economy. In North America we are learning to live with it but in China many cities are under lockdown. Currently in China, people are forced to stay home, and factories sit idle, unable to produce many of the parts global industries rely on. This leads to ongoing supply chain issues, a phrase we have become all too familiar with over the last two years. In a nutshell, fewer workers lead to higher demand for workers, which leads to higher wages to attract workers. As well, fewer components mean more demand for those components and more demand leads to higher prices for those components. Higher wages and higher materials costs combine for higher prices for the finished products. Leading to inflation.

Both the Bank of Canada (BoC) and the US Federal Reserve Bank (Fed) aim for an Inflation rate of 2 – 3%. However, the inflation rate in Canada is above 6% and, in the US, its over 8%. In an effort to drive down inflation, the BoC and the Fed have both become aggressive in their respective fights to drive inflation back to their respective targets. This leads to our next headwind – rising interest rates.

One of the tools the central banks (the BoC and the Fed) use to fight inflation is to raise interest rates. Already this year we have seen rate hikes of .25% and .5% in both countries, and both central banks have indicated they could keep hiking in .5% increments until interest rates reach 2%. The higher the interest rates, the more money is required to pay down debt and loans. If you have any form of debt, you should already be experiencing higher debt payments. This is the same for companies with high levels of debt. The additional cash to service their debt could have been used to grow the company. In the case of high growth companies like technology companies, this slows their growth. When high growth companies do not create high growth, their share price gets hammered, as we are seeing in 2022 (and as my Portfolios can attest).

If Covid-19, inflation, and higher interest rates are not enough, the Russian invasion of Ukraine further disrupted energy and food supplies, adding to inflationary and supply chain problems. Russia is the third largest producer of oil, second largest producer of natural gas, and third largest wheat producer. Ukraine is the seventh largest producer of wheat. With these two major suppliers removed from the supply system (Russia due to sanctions, Ukraine busy defending itself), we are already experiencing higher food and energy costs. Not only are we seeing higher prices at the gas pumps, but we are also seeing higher prices in almost everything we consume thanks to higher production costs and transportation costs to get those products to market. Higher energy costs and higher food costs only add to inflation.

Finally, a recent headwind we are now seeing is irrational investor psychology. With the markets in a downdraft since the start of 2022, investors are simply selling to get out. They are ignoring companies that are performing well and selling their shares simply because the market is declining. This is irrational. People cannot wait for Boxing Day sales or Black Friday sales, because prices are lower. However, when the stock markets decline, investors unload their shares even though they know that over time the market goes up. This is one of the few times where people do not want to buy when items go on sale.

So, there you have it, five headwinds currently battering the stock market:

Covid-19

Inflation

Higher interest rates

War in Ukraine

Irrational investor psychology

As with all market declines, these will pass, and the markets will resume their march higher. There is nothing we can do about it but ride out the storm.

… lest we forget, more Canadian rate hikes, American October CPI, US mid-term elections, semiconductors. Let’s begin …

Thanks to surprisingly huge jobs gains in Canada in October (108,000 new jobs, more than ten times the number economists expected), analysts believe the Bank of Canada (BoC) can justify another 0.75% increase to Canada’s benchmark interest rate. As part of Canada’s Fall Economic Statement, the Canadian government said it plans to spend an additional C$ 6.1 billion on Canadians. While I like receiving money, I am not sure giving people free money is the best idea as that is what has led to our current high inflation rate. Throwing more money at Canadians is unlikely to help the BoC get inflation down to their target range of 1% – 3%.

Sidenote: there is no such thing as free money from a government because governments only get money from taxes (in one form or another). ‘Free’ money is giving you and I back a small portion of the money we originally earned and making it sound like they are doing something special for us.

The US October Consumer Price Index (CPI) report showed the year over year rate of inflation for October was 7.7%, down from September’s 8.1%. This was the first time in eight months American consumer prices rose less than 8%. The Core CPI (CPI less food and energy prices) rose 6.3 percent over the last 12 months. Analysts were expecting a CPI rate of 7.9% and a Core CPI rate of 6.5%. While inflation is heading in the right direction, there is a long way to go to get down to the Fed’s target of 2%.

The report was a strong sign that inflation was cooling, but the US Federal Reserve (Fed) will continue to increase interest rates well into 2023. However, investors are hoping this latest report opens the door for the Fed to lower the size of the next interest rate increase scheduled for December.

After the good news of dropping inflation, the markets in both Canada and the USA reacted positively to this news, sending the indexes sharply upward. Many of the technology companies spread across the three portfolios had double digit percentage gains after the October CPI announcement. More than 90% of stocks in the S&P were in the black.

Before getting too excited, keep in mind the mini rallies this year that turned out to be bear traps. Bull markets have generally not started until roughly a year after the Fed had reversed course and started reducing interest rates. With interest rate increases projected to continue well into 2023, the first interest rate cut is a long way away.

As of November 11, the results of the US mid-term elections had not been decided. It is likely that the Republicans will win the House of Representative and possibly the Senate. With a Democratic president in the White House, that potential result could lead to gridlock until the 2024 US election. From an investing viewpoint, a split government is generally seen as favorable to the stock markets over the long run because major changes to taxes or other laws are likely off the table, as well as any sort of big spending policies.

While it appears unlikely at this point, if the Democrats somehow retain control of Congress, it could spook the markets due to concerns about big budget spending that could add fuel to existing inflation, and tighter tech-sector regulation which could slow the growth of high growth technology companies.

I was going to say a benefit of the mid-term elections being over is the removal of uncertainty caused by mid-term elections, but the outcome is still uncertain as of this writing. 😊

Tale of two Semiconductors. I keep reading that there is a glut of semiconductors (also known as chips) as well as supply issues caused by a lack of semiconductors (particularly in the automobile industry). How can there be a glut and a shortage at the same time? Turns out there are two main classes (for lack of a better word) of semiconductors – ‘leading edge’ chips and ‘lagging edge’ chips.

It is the semiconductors used in personal computers where there is a glut. There was a huge demand for these more powerful ‘leading edge’ chips at the beginning and during the pandemic as many companies implemented work from home strategies. Now that the pandemic is largely over as we have learned to live with covid-19, the demand for personal computers has slowed (plus everyone who needed a new computer already purchased one).

It is the older, less sophisticated ‘lagging edge’ or ‘trailing edge’ chips that are used in automobiles, manufacturing, networking technologies and other industrial uses. The shortage of these chips has a trickle-down effect because many industrial companies manufacture components that use these chips, which in turn are needed by other downstream companies. This is the case in the automotive industry as cars are waiting for these less sophisticated chips to be installed before they can be shipped to car dealers.

At this point you may be wondering why not simply re-purpose the advanced chips to take the place of the lesser chip. I know I was but, apparently the advanced chips simply cannot be used in place of the less advanced chips. I could not find a good explanation why they could not, but I assume it has to do with size of the chip, and how it interfaces with other components, but I am sure there are other reasons. In any event, as the demand for technology products continues to grow, there is growing demand for the trailing edge chips in almost every industry and market.

Eventually the supply chain of lagging edge chips will sort itself out, which in turn will relieve many of the supply chain issues faced by other downstream companies, such as automobiles, robotics, and appliances. I am sure once the semiconductor manufacturers pivot to producing these lesser, commodity style chips, it will cause a shortage of leading edge or even ‘bleeding edge’ semiconductors.

Before your eyes glaze over from all the talk about interest rates, let’s switch gears to what happened in the markets this past week….

Weekly Market Review

Monday: Two bits of news were front and centre for investors: the upcoming US mid-term elections, and the upcoming US Consumer Price Index (CPI) report for October inflation numbers. All four major North American indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – ended higher thanks to a broad-based rally that lifted big blue-chip companies and small businesses alike.

In Canada, strong third quarter corporate earnings continue to keep the TSX inching upwards. In the TSX, the Technology and Industrials sector led the way while the defensive Utilities sector was the only Canadian sector to lose ground today.

In the US, thoughts of political gridlock after the mid-term elections gave the American indexes a lift. This was reflected in the marketplace where the Technology and Energy sectors were the best performers of the eleven US S&P sectors, while only the Utilities and Consumer Cyclical sectors ended lower.

Tuesday: All four indexes ended the day higher. In Canada, the TSX hit its highest level in two months thanks to higher gold and copper prices. The Basic Materials sector (natural resources, such as gold and copper, and fertilizer manufacturers) three times higher than the second best performing Canadian sector (Utilities).

In the US, all three American indexes rose as investors bet that the US mid-term elections would leave the US with political deadlock that would stall any significant Democratic policy initiatives (read tax increases or additional spending). The market likes a stalemate since its very unlikely any major policies will be announced for a few years.

In the marketplace, the DJIA has slowly clawed its way out of market correction territory (when an index or stock falls 10% or more from its recent high). That is a good sign, but I would be happier if the S&P or Nasdaq had climbed back to single digit declines, but I will have to wait a few more months. 😊 In the market, the Basic Materials and Technology sectors pulled the S&P higher, while the Energy and Consumer Cyclical sectors were the only two sectors to lose ground.

Wednesday: All four indexes took it on the chin today, falling at least 1.6%, giving back much of the gains from the last two days. In Canada, lower oil prices caused the share prices of Energy sector companies to drop. The Basic Materials and Technology sectors were also big losers on a day that saw only the Telecommunications sector end above water.

In the US, all three American indexes fell sharply on the lower oil prices and disappointing earnings ahead of the October Consumer Price Index (CPI) inflation report due Thursday. Analysts and investors were also digesting the mixed message of the US mid term elections where the Democrats did better than expected. The market expected a stronger showing from the business friendlier Republicans. In trading, the Energy, Consumer Cyclicals and Technology sectors fell the hardest in what was a broad-based pullback where none of the eleven S&P sectors broke into the black.

Thursday: A great day for all four major North American indexes thanks to a better-than-expected US October CPI report that showed inflation was finally cooling. The rate of inflation for October came in at 7.7%, down from September’s 8.1%. Analysts had been expecting 7.9%. Analysts and investors believe this opens the door for the Fed to lower the size of the next interest rate increase, scheduled for December. Investors celebrated by sending the markets soaring, especially the Technology sector which soared over 8% in both Canada and the US.

In Canada, the TSX had its biggest gain since April 2020 thanks to gains in every Canadian sector. The big winners were the Technology, Basic Materials, and Consumer Cyclicals sectors.

In the US, the Nasdaq soared over 7%, and the S&P jumped 5.5%, their respective largest daily percentage gain since April 2020. In addition, the DJIA gained more than 1,000 points today. In the marketplace all eleven S&P sectors rose at least 2%. The big winners were the Technology, Consumer Cyclicals and Basic Materials sectors.

Friday: The excitement and enthusiasm of yesterday carried over into the markets today as all four indexes ended the day and the week higher. In Canada, China relaxed some of their Covid-19 restrictions leading investors to think that would increase the demand for oil in the world’s second largest economy, pushing the price of oil higher. Higher oil prices, combined with hopes of cooling inflation in the US helped the Technology, Energy and Consumer Cyclicals sectors pull the TSX into positive territory.

In the US, following Thursday’s CPI report, investors could not resist the call of the stock market, especially the technology companies. Strong days from Amazon (NASD:AMZN), Apple (NASD:AAPL) and Microsoft (NASD:MSFT) helped push the Nasdaq and S&P to another positive day, while a soft day in the Healthcare sector prevented the DJIA from having a better day. In the market today, Basic Materials, Consumer Cyclicals and Energy led the S&P sectors.

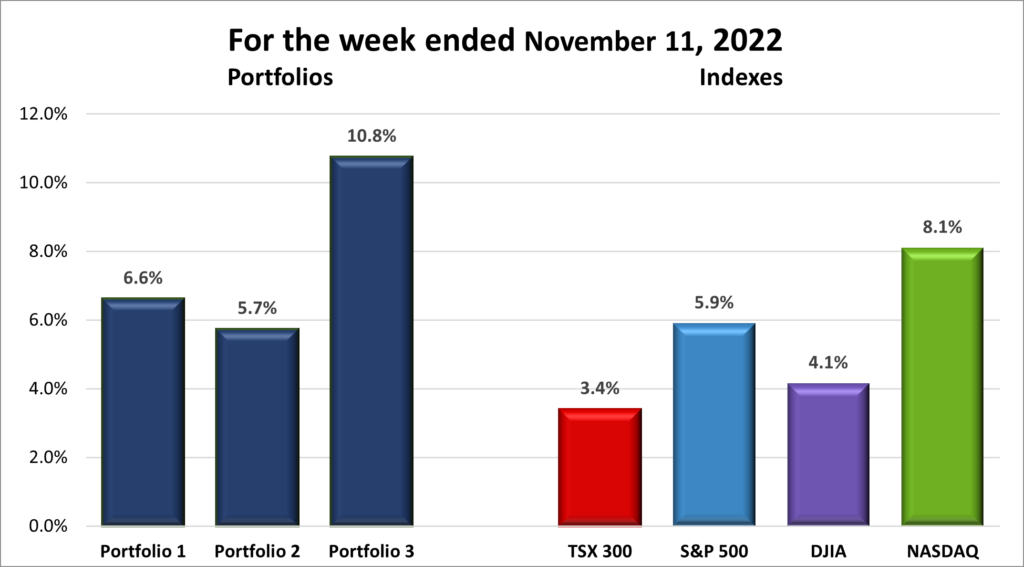

For the week, the TSX rose 3.4%, the S&P 500 gained 5.9%, the Dow advanced 4.1% and the Nasdaq jumped 8.1%.

Weekly Portfolio Review

Its amazing what a little bit of news can do. Last week, suggestions the Fed’s final interest rate could be higher than estimated caused the American markets to drop, especially the Nasdaq which dropped sharply. This week, news that the US CPI report came in lower than expected sent the American markets soaring, with Canada’s TSX getting lifted by the rising tide. The Nasdaq was the biggest beneficiary with gains more than offsetting the previous week’s losses.

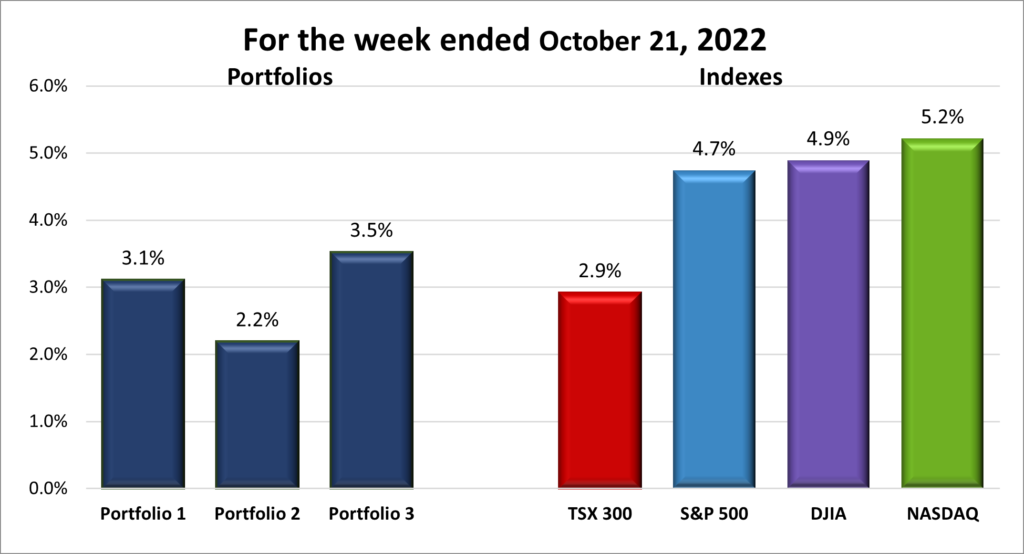

Since it was a good week for all four indexes, it was a good week for the Portfolios. All three portfolios benefitted from having a technology bias, especially Portfolio 3. Shopify (TSX:SHOP) and Microsoft had good weeks, pushing Portfolio 3 to the #1 performer. Portfolio 1 was carried higher thanks to investors moving strongly back into the market, particularly the Technology sector. While not as good as the other two portfolios, Portfolio 2 had an impressive week rising almost 6%. When all three portfolios come close to beating the S&P, which had a good week itself, I call that a great week. Still a long way to get back to where they were a year ago, and there will be more pain along the road, but it is a step in the right direction.

Weekly Portfolio & Index performance for the week ended November 11, 2022.

Companies on the Radar

No company has stood out for me, so I am just sitting on cash, waiting for the appropriate time to deploy it. Since I was looking at Alvopetro Energy (TSXV:ALV), I decided to look at two other energy companies within the portfolios, Crew Energy (TSX:CR) and International Petroleum (TSX:IPCO). Turns out they all look decent. I like that Alvopetro provides a 6% dividend, even though Crew and IPCO score slightly higher in the Rating Total column (the total of TR Fundamentals and TD Analysts scores). Outside of energy companies, I still like STMicroelectronics N.V. (NYSE:STM), Alphabet (NASD:GOOGL).

STMicroelectronics N.V.: European manufacturer of semiconductors (chips) for the automotive industry.

Alphabet: clear leader in online search and online advertising (Google and YouTube); leader in mobile phone operating systems (Android); one of the top cloud computing platforms (Google Cloud); producer of computer hardware and software (Chrome); plus, expanding into other areas, such as health.

Alvopetro Energy: a Canadian natural gas company developing natural gas projects in Brazil.

Crew Energy: a Canadian oil and gas company with interests in British Columbia.

International Petroleum: a Canadian company with oil and gas assets in Canada, Malaysia, and France.

Below are my Radar Checks on these companies, updated November 11, 2022.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended November 11, 2022: UP

Tesla (NASD:TSLA) has applied to the Canadian Radio-television and Telecommunications Commission for a license for its vehicles to transmit and receive telemetry data, infotainment services, control vehicle operations and connect with emergency services. The license would be similar to the license GM (NYSE:GM) has for their OnStar service.

Tesla is facing a recall of 40,000 Model S and Model Y vehicles that could suffer a loss of power steering when driving over bumpy roads.

Tesla is mulling over the idea of exporting cars from their Shanghai facility to North America. This would allow Tesla the benefit of a widening cost advantage from manufacturing vehicles in China rather than in the USA. A speed bump in this plan is getting North American regulators to sign off on Chinese made components. A bigger speed bump would be the political fall out of replacing North American made cars with cars made in China and the resulting jobs situation.

In other Tesla related news, founder Elon Musk sold US$ 3.95 billion worth of Tesla shares despite stating in November 2021 that he would no longer sell any more Tesla shares. When he breaks his promise, he breaks his word big time.

In an effort to maintain its Chinese market after the US introduced new leading edge technology export rules, Nvidia (NASD:NVDA) developed a new advanced chip for China. The A800 semiconductor is Nvidia’s response at creating an advanced chip for China that stays within the rules set by the US government.

Rivian (NASD:RIVN) has delivered more than one thousand of their electric vans to Amazon during the last year. Not bad for a company that a year ago had $0 in sales. Amazon is a major investor in Rivian as well as their largest customer. Rivian has an order to deliver 100,000 Rivian EV vans by 2030.

Apple and Amazon have been accused of fixing to raise the price of iPads and iPhones sold on Amazon.

In a move to cut costs, Amazon is currently reviewing all unprofitable business units, including Alexa’s devices unit and robotics unit. Employees can look for work in other profitable units or will be reassigned to fit Amazon’s needs. Could this mean Siri is the last digital voice sanding? 😊

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Bank of Nova Scotia (TSX:BNS) DRIP

US $

Apple Inc (NASD:AAPL)

Quarterly Reports

Andlauer Healthcare Group Inc.

All currency listed in thousands of Canadian dollars, except Earnings/Loss per share numbers

Revenue of $666,724 for the three months ended September 30, compared to $528,575 for the same period in 2021. An increase of over 26%.

Net loss of $207,335 for the three months ended September 30, compared to net loss of $39,421 in the same period in 2021.

Diluted loss per ordinary share of $0.29 for the three months ended September 30, compared to a loss of $0.05 for the same period in 2021.

Revenue of $2,026,680 for the nine months ended September 30, compared to $1,690,640 for the same period in 2021. An increase of over 19%.

Net loss of 217,059 for the nine months ended September 30, compared to net earnings of $42,144 in the same period in 2021.

Diluted loss per ordinary share of 0.21 for the nine months ended September 30, compared to earnings of $0.13 for the same period in 2021.

Portfolio 2

Portfolio 2 for the week ended November 11, 2022: UP

Summit Industrial Income REIT (TSX:SMU.UN) soared 25.5% after Dream Industrial REIT (TSX:DIR.UN) said they were buying the company. Partnering with Dream is GIC, Singapore’s sovereign wealth fund.

Take-Two Interactive (NASD:TTWO) slumped almost 14% after the videogame publisher lowered its annual sales outlook.

Disney’s (NYSE:DIS) streaming service took a big bite out of revenues, costing Disney US$ 1.5 billion. As a result of Disney’s poor earnings report this week the company announced some jobs would be eliminated and a hiring freeze, with the only new hires limited to their most critical business units

TC Energy (TSX:TRP) plans to raise funds for new projects by selling C$ 5 billion worth of assets.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Bank of Nova Scotia (TSX:BNS) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

Take Two Interactive Software, Inc.

All currency listed in millions of US dollars, except Earnings/Loss per share numbers

Revenue of $5,751,558 for the three months ended September 30, compared to $3,734,193 for the same period in 2021. An increase of over 54%.

Net loss of $2,546,960 for the three months ended September 30, compared to net loss of $2,509,638 in the same period in 2021.

Diluted loss per ordinary share of $0.03 for the three months ended September 30, compared to a loss of $0.03 for the same period in 2021.

Revenue of $16,499,162 for the nine months ended September 30, compared to $9,238,312 for the same period in 2021. An increase of over 79%.

Net loss of $9,607,108 for the nine months ended September 30, compared to net loss of $8,308,792 in the same period in 2021.

Diluted loss per ordinary share of $0.12 for the nine months ended September 30, compared to a loss of $0.11 for the same period in 2021.

Portfolio 3

Portfolio 3 for the week ended November 11, 2022: UP

Microsoft faces another European Union antitrust complaint, this time over its cloud computing services. It is alleged Microsoft uses its dominant position in productivity software (Office products) to leverage its Office 365 users towards Microsoft’s Azure cloud services to the detriment of Amazon, Google, and other European cloud providers.

Brookfield Asset Management (TSX:BAM.A) partnered with MidOcean Energy to buy out Australia’s second largest power producer Origin Energy with an offer of $11.8 billion. Origin Energy has backed the proposal which would see Brookfield acquire Origin’s energy markets business while MidOcean would control Origin’s integrated gas business.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

Fortuna Silver Mines Inc.

All currency listed in thousands of US dollars, except Earnings/Loss per share numbers

This week: Canada’s Fall Economic Statement, latest US interest rate hike, UK interest rate hike, OPEC, world’s strongest dollar. Let’s begin.

This week, Canada’s Fall Economic Statement showed Canadian finances have improved thanks to a windfall of revenue from the oil and gas energy and taxes from higher prices of most goods and services raking in more money. However, analysts fear that the increased revenue and shrinking deficit will not be here for long as the threat of a recession in Canada grows larger. Analysts suggest Canada could enter a recession in early 2023, when growth slows thanks rising interest rates that pinch consumer and business spending alike.

One thing that stood out for me was the government’s plan to place a 2% tax on corporate share buyback programs, starting January 1, 2024. A share buyback is when a company repurchases its own shares on the open market and then puts them back in their treasury or they destroy them. The buyback reduces the total number of outstanding shares, thus driving up the earnings per share. Share buyback programs are one way to increase shareholder value when companies generate excess cash (another way is to pay dividends to shareholders).

Besides generating more revenue for the government with this new tax, the government argues that this tax will encourage companies to invest in their employees and their businesses. However, the tax will not be rolled out until 2024, providing a window of opportunity for companies to buyback their shares before the tax goes into effect. Once the tax is in effect, I would not be surprised to see companies channel excess profits towards special dividends and increasing their regular dividends. I can see the argument that this would be better for more than just the shareholders, but this sounds more like a calculated political move aimed at higher corporate profits given the huge profits by the Canadian banks in 2021 and now the Canadian oil and gas companies.

Statistics Canada latest Labour Force Survey showed a surge in hiring and wage growth of 5.6%, surpassing September’s 5.2% increase. That makes it five consecutive months that wages have risen by more than 5%. That will not make the Bank of Canada (BoC) happy, not happy at all as they seek to bring down inflation to their 2% target. Analysts are now expecting 0.5% rate increase to Canada’s benchmark interest rate at the BoC’s next session in early December.

The US Federal Reserve Bank (Fed) continued its battle with the worst inflation levels seen in America in 40 years by raising the benchmark US interest rate by 0.75% for the fourth consecutive time. This brings the US interest rate to 3.75%, its highest in 15 years. In an announcing the hike, the Fed hinted at the possibility of lower increases in the future as it hopes to thread the needle between stubbornly high inflation and the strains on the US economy caused by higher interest rates. The markets reacted with a brief rally before the other shoe dropped – the Fed said it was not done raising interest rates and the interest rate could go higher than the 4.75% estimated at their last session in September. This news caused a sharp drop on both the American and Canadian markets on the day of the announcement.

While the Fed feels there are more hikes in the works, they want to assess how the “cumulative effect” of their previous hikes have affected the US economy before determining the size and pace of future hikes. One of the key pieces of data the Fed will use to determine the size of future rate hikes is the US non-farm employment numbers. Good news for workers is not necessarily good news when it comes to the Fed’s battle with inflation since a strong labour market tends to lead to companies paying more for labour, which is passed on to consumers in the form of higher prices. Higher prices and higher wages can become an upward spiral that drives inflation. Since forcing inflation down from its current 8% to 2% is the Fed’s number one objective, the Fed may extend its rate hikes longer and higher than expected. Which means more pain for US consumers.

There is a saying, when the US sneezes, Canada catches a cold. Alas, I think the Feds battle with inflation will give Canadians a cold. ☹

In the United Kingdom, the Bank of England (BoE) raised their benchmark interest rate by 0.75%, the largest increase since 1989, to 3.0%. Just as important was the forward guidance they provided. The BoE suggested Britain faced a recession and the British economy may remain stagnant or decline over the next two years. However, in contrast to the Fed and BoC, the BoE suggested the British benchmark interest rate was likely to go up less than originally expected.

The Organization of the Petroleum Exporting Countries (OPEC), whose thirteen countries depend on oil income, raised its forecasts for world oil demand in the medium and longer term in its annual World Oil Outlook that was released October 31. The report indicated $12.1 trillion of investment is needed to meet this demand despite the energy transition to renewables.

As a result of an expected strong recovery in 2023 and a focus on energy security, the report said world oil demand will reach 103 million barrels per day (bpd) in 2023, up 2.7 million bpd from 2022, leading to a slower substitution of oil by other fuels such as natural gas.

By 2030, OPEC sees world demand averaging 108.3 million bpd, up from 2021, and lifted its 2045 figure to 109.8 million bpd from 108.2 million bpd in 2021. Oil is expected to “retain the highest share in the global energy mix during” through to 2045, with its share in the energy mix dropping from 31% to just under 29%. The combined market share of oil and gas in the global primary energy mix is expected to remain above 50% through to 2045.

The US dollar continues to grow stronger against other currencies, including the Canadian dollar as investors (both the pros and us retail investors) often turn to the US dollar as a safe haven during periods of uncertain global economic conditions, a flight to safety if you will. Interest rate hikes only make the US dollar more attractive to domestic and foreign investors.

Foreign investors typically use the American dollar when moving money into US stocks and bonds, which in turn also boosts the strength of the US dollar. The Wall Street Journal Dollar Index, which weighs the US dollar against sixteen other currencies, is up nearly 16% so far this year.

A stronger US dollar not only makes everything more expensive for those of us outside the USA, but it also lowers revenues of American based businesses. American products are more expensive outside the US because of the foreign exchange, possibly leading to lower sales. And those foreign revenues lose value when they are converted back to US dollars, making sales and profits appear lower than they are.

As an owner of many technology companies that do business globally, I have seen many quarterly earnings pointing to the strong dollar as one of the causes of lower revenues. As a consumer, I notice higher prices every time I consider a product or service from the US.

Enough about higher interest rates and what a stronger US dollar are doing to our buying power, lets take a look at what moved the markets, and they impact it had on the Portfolios…

Weekly Market Review

Monday: No treats on Hallowe’en in the North American stock markets as all four major indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – lost ground today. In Canada and the USA, investors were apprehensive ahead of an anticipated 0.75% gain by the US Federal Reserve Bank (Fed) later this week. Just as important will be comments coming out of the Fed’s meeting regarding the December interest rate hike where a 0.25% – 0.5% hike is projected. Hawkish comments would not be well received, while dovish comments would be well received.

In Canada, only two sectors, Healthcare (jump in Canopy Growth’s share price thanks to their plan to enter the US market) and Energy (higher oil prices), were able to inch higher.

In the US, the three US indexes ended October with a whimper despite having a strong month. In the market, Only the Energy sector was able to gain ground while the heavyweight technology companies continue to drag the Technology sector down which was once again the worst performing sector.

Tuesday: The day started out on the right foot, but the American indexes turned south on news of an unexpected rebound in job openings which led to speculation the Fed will maintain its aggressive round of interest rate increases. As a result, only the TSX was able to move higher while the US indexes finished slightly lower.

In Canada, the TSX was buoyed by rumours China will ease its strict covid-19 measures which have slowed down China’s manufacturing capabilities and limited Chinese consumer demands. In the marketplace, once again Basic Materials (natural resource miners and fertilizer manufacturers) and Energy companies led the TSX, while the Utilities, Industrials and Healthcare sectors were the only sectors to end lower.

In the US, a report showing strong demand for workers threw cold water on hopes the Fed would lower their planned December interest rate hike. Tomorrow, all eyes will be on the Fed, both for the November interest rate hike and any signs the December rate hike will be lower. In the markets, Basic Materials and Energy were the biggest gainers while Technology and Consumer Cyclical sectors dropped the most.

Wednesday: A tough day in the North American marketplace as all four indexes fell sharply. The market moving news was the Fed announced the expected 0.75% interest hike and hinted smaller hikes could start as early as their next meeting in December. This caused a brief 45-minute rally on all four indexes before the rally turned into a sharp decline when the Fed also stated the benchmark interest rate could go higher than expected.

No sector was spared in Canada or the US, as all lost ground. In Canada, Basic Materials and Technology were the worst performing sectors, while in the US, it was the same two sectors only they flipped positions with the Technology the worst performing S&P sector.

Thursday: All four indexes continued to slide as investors continued to fret over future interest rate increases after the Fed said hikes were far from over. In Canada, the Energy, Industrials and Healthcare sectors were the only Canadian sectors to end on the plus side. In the US, the Energy, Basic Materials and Utilities were the only S&P sectors to advance.

Friday: All four major North American Indexes had a good day to end the week, but not good enough to salvage what was a volatile week. Analysts and investors continued to weigh the impact of a mixed US employment report on the size and pace of future interest rate hikes. The report showed slowing job growth, but hourly rates rose more than expected. However, investors did take some solace in reports China may relax its Covid-19 restrictions. China has a voracious appetite for natural resources so with the Covid-19 restrictions removed, there should be pent up demand for commodities to fuel its manufacturing industry. Thanks to these rumours, the Basic Materials sectors in Canada and the US both had strong days, advancing over 5% in both countries. Many of the world’s commodity companies are part of the Basic Materials sector.

In Canada, Statistics Canada jobs data showed Canada adding ten times more than the expected number of jobs (108,000 added, 10,000 expected), and the average hourly wage rose 5.5% since last October. Good for workers, not good for lower interest rates. On the TSX, the Basic Materials sector led the TSX in a broad rally that brought it within striking distance of breaking even for the week. The interest sensitive Technology sector was the only Canadian sector to end the day in the red.

In the US, the three American indexes ended their respective four day losing streaks thanks to s strong rally that saw all eleven S&P sectors end the day in the black. The S&P Basic Materials sector was the big winner on the day, advancing more than twice as much as the second-best performing Financials sector.

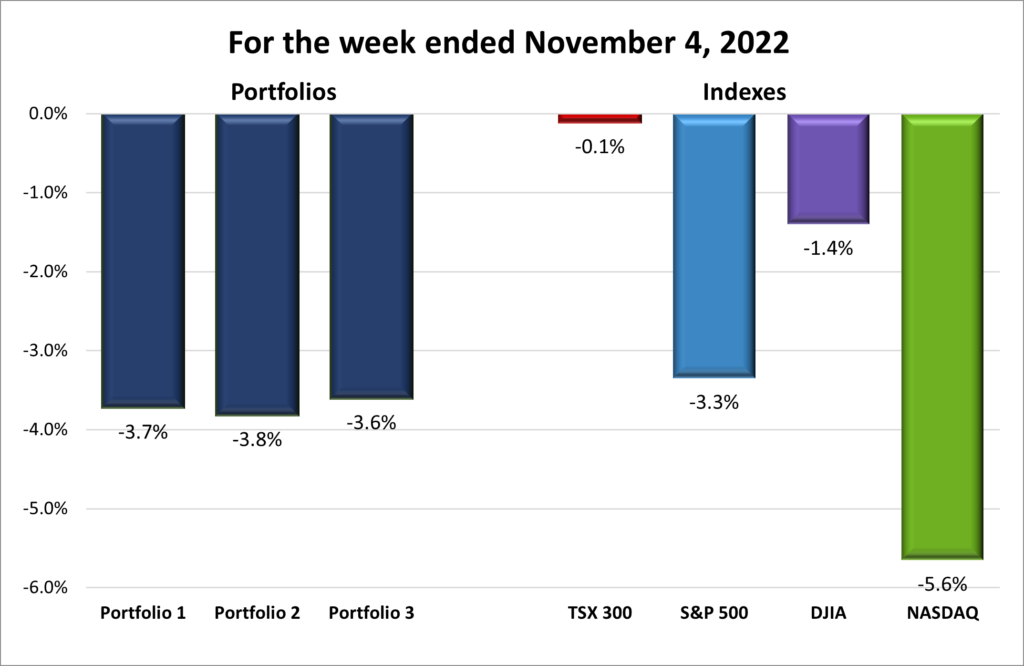

For the week, the TSX slipped 0.1%, the S&P 500 dropped 3.3%, the Dow fell 1.4% and the Nasdaq plunged 5.6%, its biggest weekly decrease since January.

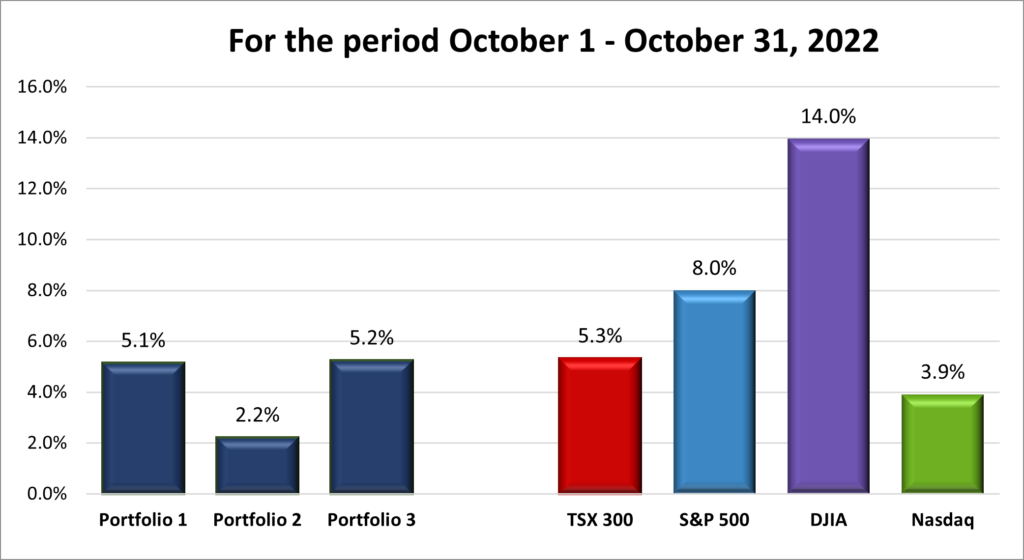

October was a good month for investors, the TSX had its best month since November 2020, rising 5.3 %; the S&P 500 jumped 8.0 %; the Dow had its best October in over 100 years, soaring 14.0 %; and the Nasdaq climbed 3.9 %.

Weekly Portfolio Review

After a strong October in the marketplace (see the chart above), November fell flat on its face with this past week’s performance. The Nasdaq, home of many interest sensitive, growth-oriented companies, got beaten down by the Fed’s hints that interest rates could exceed estimates. To a lesser extent the S&P suffered the same fate as the Nasdaq, as many of the heavyweight companies are in both indexes, but the S&P also contains more traditional companies that held up better than the technology companies that dominate the Nasdaq. The TSX is kept afloat by higher commodity prices that benefit Basic Materials sector companies as well as oil and gas companies, while the DJIA limited the damage thanks to being composed of strictly large blue-chip companies.

Before looking at the weekly performance chart below, I expected Portfolio 2 to be the best performer, or rather, have the smallest decline, followed by Portfolio 1 and Portfolio 3 bringing up the rear. However, it was essentially a dead heat with all three portfolios dropping 3.6% to 3.8%. This week, Portfolio 3 was the best of a bad lot.

Weekly Portfolio & Index performance for the week ended November 4, 2022.

October was a great month for us investors. July was the last time all four indexes advanced as much as they did in October. Normally an 8% advance by the S&P would be the big news but it was unseated by the DJIA which had its largest one month gain since January 1976. Yes, since before 1900 thanks to its concentration of companies in the Energy and Industrials sectors. The TSX had its best month in two years thanks to higher oil prices. Bringing up the rear, the Nasdaq was held back by the higher interest rates which slowed the growth rate of the many growth-oriented companies in the index.

This is one of the few times I wish the Portfolios were DJIA centric. However, they are not, and I do not plan for them to become more DJIA oriented. I plan to stick with my growth-oriented approach which aligns more with Nasdaq and the S&P. Nonetheless, 5+% gains by Portfolios 1 and 3 are quite acceptable. 😊 I would have preferred Portfolio 2 post a 5% gain during a hot month but that is the trade off for not dropping as much during poor months, which there have been plenty in 2022.

Monthly Portfolio & Index performance for October 2022.

Companies on the Radar

I am still considering becoming an owner STMicroelectronics N.V. (NYSE:STM), or increasing my ownership of Alphabet (NASD:GOOGL) or Alvopetro Energy (TSXV:ALV):

STMicroelectronics N.V.: European manufacturer of semiconductors (chips) for the automotive industry.

Alphabet: clear leader in online search and online advertising (Google and YouTube); leader in mobile phone operating systems (Android); one of the top cloud computing platforms (Google Cloud); producer of computer hardware and software (Chrome); plus, expanding into other areas, such as health.

Alvopetro Energy is a Canadian natural gas company developing natural gas projects in Brazil.

Below are my Radar Check on these two companies, updated November 4, 2022.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended November 4, 2022: DOWN

The TMX Group (TSX:TMX), the parent company of the TSX, suffered a glitch which led to a halt of all equities trading on Tuesday morning. All TSX platforms lost connectivity around 10:10 ET but were back online with full functionality by 11:20 ET.

Rogers (TSX:RCI.B) and Shaw (TSX:SJR.B) have been asked by a federal judge to address concerns from Canada’s Competition panel in order to resolve their dispute. Hopefully the two sides can work out a deal that is amenable to both sides although I do not see how reducing the competition by a major player, such as Shaw, will improve competition.

PayPal (NASD:PYPL) did not have an impressive third quarter earnings report, revenues increased only 11% during the third quarter and 9% for the nine months. Growth companies are supposed to grow revenues more than that. The share price also took a hit when the company warned of a slower holiday season as people cut back on their discretionary spending.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Toronto-Dominion Bank (TSX:TD) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

CargoJet Inc.

All currency listed in millions of Canadian dollars

Revenue of $172,509 for the three months ended October 1, compared to $131,911 for the three months ended October 2, 2021. An increase of over 30%.

Net earnings of $46,359 for the three months ended October 1, compared to net income of $26,739 for the three months ended October 2, 2021.

Diluted earnings per ordinary share of $0.33 for the three months ended October 1, compared to earnings of $0.19 for the three months ended October 2, 2021.

Revenue of $434,396 for the nine months ended October 1, compared to $373,532 for the nine months ended October 2, 2021. An increase of almost 30%.

Net earnings of $126,969 for the nine months ended October 1, compared to net earnings of $67,390 for the nine months ended October 2, 2021.

Diluted earnings per ordinary share of $0.90 for the nine months ended October 1, compared to earnings of $0.47 for the nine months ended October 2, 2021.

Revenue of $224,813 for the three months ended September 30, compared to $156,690 for the same period in 2021. An increase of over 43%.

Net loss of $152,648 for the three months ended September 30, compared to net loss of $105,851 in the same period in 2021.

Diluted loss per ordinary share of $0.82 for the three months ended September 30, compared to a loss of $0.74 for the same period in 2021.

Portfolio 2

Portfolio 2 for the week ended November 4, 2022: DOWN

Disney (NYSE:DIS) has had many of its iconic brands added to a list of brands that can be imported into Russia from third party countries, such as China, without the permission of the company. Russia created this list when many Western companies, including Disney, suspended operations in Russia, or completely exited the country in response to Russia’s invasion of Ukraine.

Canadian Natural Resources (TSX:CNQ) announced a 13% increase to its dividend thanks to higher prices for its crude oil. The quarterly dividend is now C$ 0.85.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

TC Energy Corp (TSX:TRP)

US $

No US$ dividends this past week.

Quarterly Reports

Canadian Natural Resources Limited

All currency listed in millions of Canadian dollars

Revenue of $1,105 for the three months ended September 30, compared to $966 for the same period in 2021. An increase of over 14%.

Net loss of $77 for the three months ended September 30, compared to net loss of $154 in the same period in 2021.

Diluted loss per ordinary share of $0.25 for the three months ended September 30, compared to a loss of $0.21 for the same period in 2021.

Revenue of $3,515 for the nine months ended September 30, compared to $3,005 for the same period in 2021. An increase of almost 17%.

Net income of $78 for the nine months ended September 30, compared to a net loss of $99 in the same period in 2021.

Diluted loss per ordinary share of $0.44 for the nine months ended September 30, compared to a loss of $0.58 for the same period in 2021.

Telus Corporation

All currency listed in millions of Canadian dollars

Selected highlights from their third quarter 2022 financial results on November 4, 2022

Revenue of $4,671 for the three months ended September 30, compared to $4,251 for the same period in 2021. An increase of almost 10%.

Net income of $551 for the three months ended September 30, compared to net income of $358 in the same period in 2021.

Diluted earnings per ordinary share of $0.37 for the three months ended September 30, compared to earnings of $0.25 for the same period in 2021.

Revenue of $13,354 for the nine months ended September 30, compared to $12,386 for the same period in 2021. An increase of almost 8%.

Net earnings of $1,453 for the nine months ended September 30, compared to net earnings of $1,035 in the same period in 2021.

Diluted earnings per ordinary share of $0.99 for the nine months ended September 30, compared to earnings of $0.75 for the same period in 2021.

Portfolio 3

Portfolio 3 for the week ended November 4, 2022: DOWN

Microsoft (NASD:MSFT) did not offer any solutions to European Union antitrust regulators’ concerns about their acquisition of Activision Blizzard (NASD:ATVI). The regulators are expected to begin a full-scale probe of Microsoft’s purchase of the leading gaming company.

Telus International (TSX:TIXT) has added to its collection of digital solutions with the acquisition of WillowTree Inc., a full-service digital product company focused on mobile applications and unified web interfaces.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

More interest rate hike news, a reversal of fortunes for the Energy and Technology sectors, the city of tomorrow, and lucky investing

In Canada the Bank of Canada (BoC) hiked its benchmark interest for the sixth time this year, this time by 0. 5%, bringing the Canadian benchmark rate to 3.75%. Analysts and investors were expecting an increase of 0.75%. While that is good news, do not forget that the rate was 0.25% back in March before the BoC started this series of rate hikes. These rate hikes have been one of its fastest series of increases in the BoC’s history, with another potential 0.25% coming in December. On a positive note, the BoC said it was nearing the end of its historic rate increases.

The BoC rate is the amount that regular banks (that consumers like you and I use) are charged for short-term loans. This filters down into our economy by affecting the lending rates. Of course, these banks, and other lenders, add a few percentage points to this rate to arrive at the amount consumers pay for any type of borrowing. In other words, mortgages, loans, and lines of credit have gotten even more expensive.

The good news is the Canadian Consumer Price Index (CPI) has fallen over the last three months from 8.1% to the current 6.9%. The higher interest rates are working. The BoC stated in their announcement that an improving global supply chain and lower commodity prices should bring inflation down to 3% by the end of 2023, eventually dropping to the BoC’s target of 2% by the end of 2024. Those lower rates cannot get here soon enough!

In the US, the US Federal Reserve Bank (FED) is likely to raise American interest rates by 0.75% for the fourth straight time at their next session on November 2. Analysts are suggesting the central banks should not slow down or pause their respective hikes until inflation falls to roughly half of where it currently is. However, the Fed has hinted on lowering the amount of the December interest rate hike.

With both the BoC lowering the amount of the latest interest rate hike and the Fed hinting at a lower rate hike in December, perhaps the worst is behind us. The trick for both central banks is to bring down inflation without blowing up their respective economies and markets. An exceptionally fine balancing act.

The European Central Bank (ECB), the central bank for the 19 countries that use the Euro, raised its interest rate by 0.75% to 1.5% in its attempt to fight off 9.9% inflation amongst European Union members. While here in North America we would be happy with an interest rate of 1.5%, the ECB interest rate had been below 0% for eight years until the ECB started raising the rate in July. In their announcement, the ECB hinted that more interest hikes were likely. Analysts are estimating the ECB interest rate will top out in the neighbourhood of 2.6%.

Back in 2020, oil prices were at rock bottom, and no one wanted anything to do with oil company stocks (me included). The S&P Energy sector fell 37.3%. The high flyers were found in the S&P Technology sector, which rose 42.2%. Now, thanks to inflation and rising interest rates, as well as the Russian invasion of Ukraine, the tables have turned. The Energy sector is the only sector to advance in 2022, thanks to higher oil prices. In fact, the S&P Energy sector is up more than 62% so far this year. While the Technology sector is down 25%, year to date.

Saudi Arabia has been using petrol dollars generated from the higher oil prices to position itself as a global supply chain hub, and a centre of ‘green’ manufacturing. They have targeted vast sums of money at the manufacturing of ‘green’ metals (metals made with lower levels of carbon dioxide), green hydrogen production devices (hydrogen generated from renewable energy sources), and advanced recycling industries. Oh yeah, and the city of tomorrow pet project– Noem. The Saudi leadership intends for the city to be 100% powered by renewable energy; a global gateway for trade; a hub of innovation where business and industry are part of communities; essential infrastructure (utilities and transportation) will be built below the surface; and a pedestrian first approach to planning so all amenities are within a 5-minute walk. On paper, er, on the website, it sounds very impressive. I wonder how the plan will react when it runs into reality.

This is a great example of using money generated from a country’s oil and gas industry to fund the development of green industries, healthcare solutions and other benefits for its citizens.

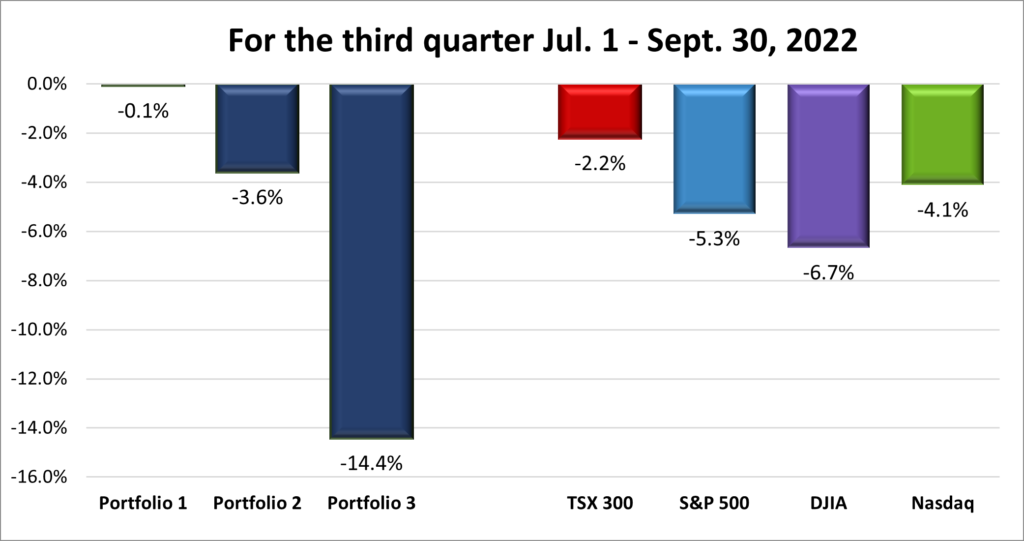

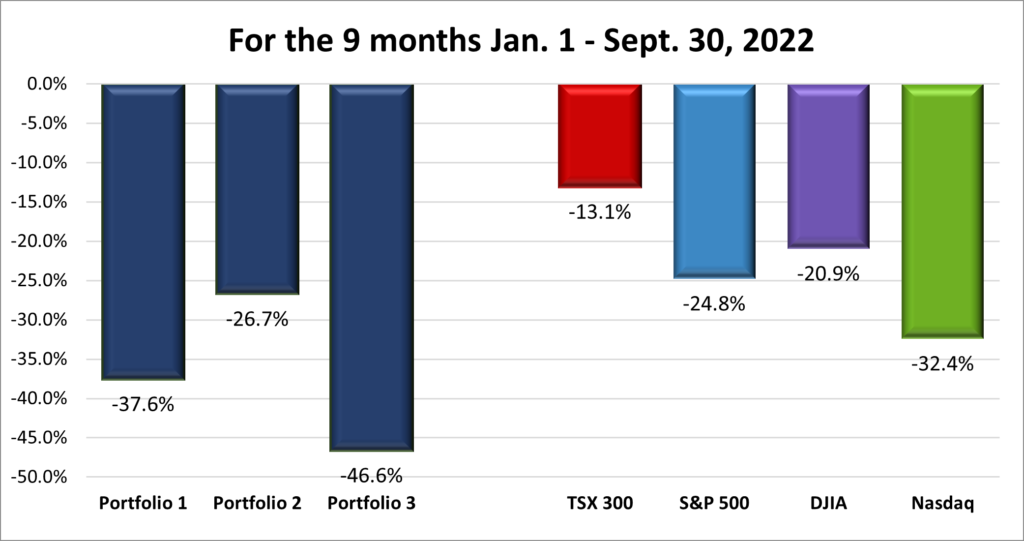

According to a report from JPMorgan Chase, individual investors’ portfolios have tumbled 44% from the beginning of January. As of September 30, my three portfolios are down 37.6%, 26.7% and 46%. Does that make me a better than average investor, or just lucky? I like to think it is the former but suspect there is a great deal of the latter involved. 😊

And now, lets take a look at the past week in the markets and the portfolios…

Weekly Market Review

Monday: All four major North American indexes – Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index, the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – continued Friday’s rally as investors prepare for some of the world’s biggest companies to report their earnings this week. Investors are focused on upcoming earnings to see if the blue-chip companies are still able to deliver profits despite their margins being squeezed by inflation. Despite a second day of solid advances, analysts still see this as a bear rally rather than the start of a new bull market run.

In Canada, the TSX was essentially flat as investors in Canadian listed companies prepare for another anticipated 0.75% interest rate hike by the Bank of Canada (BoC). In the market, all but two Canadian sectors ended in the black. Basic Materials and Healthcare were the only Canadian sectors to end in the red.

In the US, economic data released today indicated the US Federal Reserve’s (Fed) interest rate hikes are starting to slow down the US economy. However, that was not enough to but a damper on the S&P as more than 80% of stocks in the S&P rose. As with Canada, all but two of the S&P sectors ended the day higher. Basic Materials (mining and fertilizer companies) and Energy were the two laggards, ending the day lower. In contrast to Canada where Healthcare ended lower, the Healthcare sector in the US was the second-best performing sector.

Tuesday: The rally continues for all four Indexes. Weaker economic data indicated the Fed’s interest rate hikes were kicking in, giving investors hope that the Fed will ease off on the planned December rate increase.

In Canada, investors rode the optimism of American investors and pushed the TSX higher. All the Canadian sectors ended higher, led by Healthcare and Technology.

In the US, positive investor sentiment and strong earnings posted by some of the biggest blue-chip companies propelled the Nasdaq and S&P higher. All S&P sectors advanced led by the growth-oriented Consumer Cyclical and Technology sectors.

Wednesday: It was a mixed bag with the growthier oriented S&P and Nasdaq retreating, while the more traditional TSX and DJIA advanced. In the case of the DJIA, it barely squeaked into the black, ending 0.01% higher. In Canada, the TSX was able to keep its winning streak going thanks to the BoC interest rate hike coming in lower (0.5%) than expected (0.75%) and indicating it was nearing the end of its historic string of interest rate increases. Canada’s benchmark interest rate now sits at 3.75%. On the TSX, the Canadian Technology sector was the only sector to end lower.

In the US, the lower-than-expected rate height by the BoC added to US investors’ hopes the Fed will follow suit with a lower interest rate height next week. Unfortunately, disappointing earnings result from heavyweights Alphabet (NASD:GOOGL) and Microsoft (NASD:MSFT) pulled the Nasdaq and S&P down, ending their winning streak at three days. In the markets, the S&P Energy, and Healthcare sectors led the gainers while the Technology, Consumer Cyclical and Utilities sectors were the only ones to fall back.

Thursday: Another mixed bag day with the TSX and DJIA advancing and the S&P and Nasdaq retreating. In Canada, the big news was Shopify’s (TSX:SHOP) strong earnings report that showed the company beat analysts estimates for revenue and a smaller than anticipated loss. Thanks to Shopify’s impressive performance, the Canadian Technology sector more than offset four of the eleven sectors ending lower and carried the TSX into the black.

In the America, investors digested recent economic data and mixed earnings as the big technology companies reported less than impressive earnings. Meanwhile, companies in other S&P sectors posted solid earnings reports. The Industrials sector pushed the DJIA higher, while the Technology sector weighed down the S&P and Nasdaq.

Friday: All four major North American Indexes advanced as investors’ optimism the BoC and the Fed might be nearing the end of their respective interest hikes overrode a mixed bag of earnings reports from the heavyweight technology companies.

In Canada, the TSX winning streak stretched to six as many Canadian companies posted strong earnings for the last quarter. On the Bay Street (the financial heart of Canada), only the Canadian Basic Materials sector failed to end the day higher. Leading the way were the Technology and Consumer Cyclical sectors.

In the US, positive economic data, visions of milder rate hikes ahead, and strong earnings from companies outside the Technology sector helped boost investor optimism, pushing the S&P, DJIA and Nasdaq firmly into positive territory for the day and the week. On Wall Street (the financial heart of the US), it was a similar story as in Canada, with the Basic Materials sector the only sector to fall back. Leading the charge were the Technology and Telecommunications sectors.

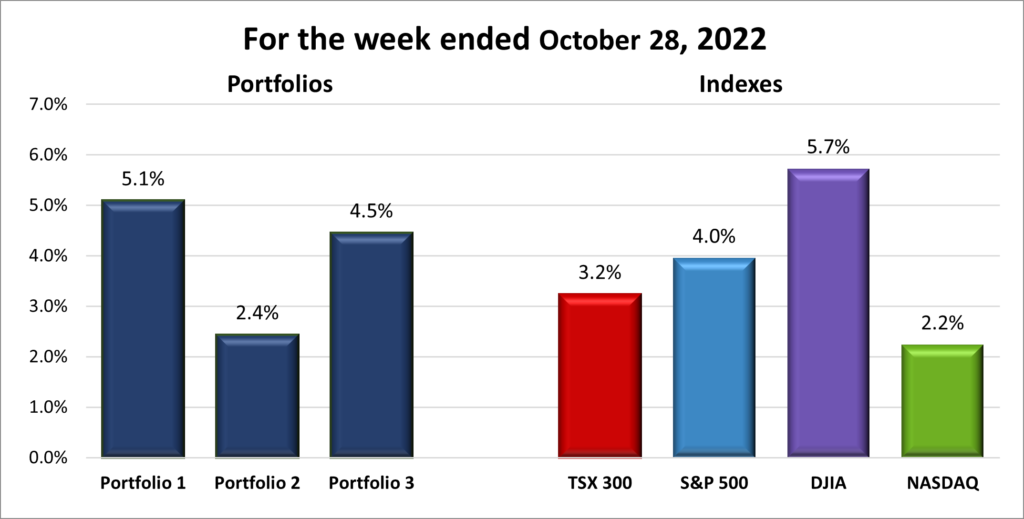

For the week, the TSX rose 3.2%,the S&P 500 gained 4.0%, the Dow jumped 5.7% and the Nasdaq advanced 2.2%.

Weekly Portfolio Review

Despite a mixed week in terms of economic data and quarterly earnings, all four indexes advanced at least a 2%. The big names in Technology – Apple (NASD:AAPL), Amazon (NASD:AMZN), Microsoft, Alphabet (Google) had a so-so week, but non technology companies had solid earnings reports. Strong earnings from oil and gas companies not only pushed the normally staid DJIA up over 5%, but they also caught the eye of the government (and not in a good way). Both governments are making noises about taxing ‘excess’ earnings. The S&P and Nasdaq were held back by less than impressive earnings reports and guidance going forward by the big technology companies mentioned above. The TSX benefitted from a smaller interest rate hike and solid earnings from many of its bigger names.

Another positive week in the markets generally means a good week for the three portfolios. And so it was. With the Nasdaq being the laggard of the indexes, I was surprised to see Portfolios 1 and 3 gaining over 4%. Many of the non technology companies in Portfolio 1 had a good week while Portfolio 3 is the benefactor of a strong earnings report by Shopify which saw its share price jump 18%. Meanwhile, Portfolio 2 just to keeps moving forward, generally never too high, and never too low.

Weekly Portfolio & Index performance for the week ended October 28, 2022.

Companies on the Radar

Another company on the radar was knocked off when Amazon dropped 19% after reporting their third quarter earnings and suggesting revenues will be sluggish over the holiday season. Otherwise, I am still following the companies below:

STMicroelectronics N.V. (NYSE:STM): European manufacturer of semiconductors (chips) for the automotive industry.

Alphabet: clear leader in online search and online advertising (Google and YouTube); leader in mobile phone operating systems (Android); one of the top cloud computing platforms (Google Cloud); computer hardware and software (Chrome); plus, expanding into other areas, such as health.

Below are my Radar Check on these two companies, updated October 28, 2022.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended October 28, 2022: UP

Tesla (NASD:TSLA) announced it was reducing prices up to 9% in China on its Model 3 and Model Y electric vehicles. While Tesla said it was a result of lower expenses, it appears to be getting in a price war with other Chinese electric vehicle manufacturers. In this battle for the Chinese electric vehicle market, Tesla is the ‘visiting team’ and the home team likely has considerable home field advantages.

It turn out Tesla has been under investigation by the US Department of Justice (DOJ) since 2021 over the company’s claims their vehicles can drive themselves. Tesla has often touted its Autopilot driver assistance system, however, more than a dozen accidents, some deadly, involving the Autopilot system would suggest its not as good as they claim. The DOJ is investigating to see whether Tesla has misled buyers, investors, and regulators.

A strong earnings and confirmation of its outlook for next year by General Motors (NYSE:GM) gave GM’s share price a nice jolt. Good.

Alphabet earnings showed the technology giant’s revenue growth slowed for the fifth consecutive quarter. The main causes for the slowing revenue were the strong US dollar and lower ad spending due to the ongoing economic uncertainty. Not good.

The Rogers (TSX:RCI.B) – Shaw (TSX:SJR.B) merger is inching toward a conclusion. Canada’s Industry Minister provided the conditions required to approve the merger, providing a starting point for negotiations between Rogers – Shaw and Canada’s Competition Tribunal.

Activity

Bought: Amazon

When Amazon presented their third quarter earnings report, they warned of sluggish sales for the upcoming holiday season. This news caused investors to dump shares, resulting in a 19% plunge in the share price in after hours trading (from 1:00 PT – 5:00 PT). I was able to pick up a few shares at less than $100. I am aware the share price could fall further, but I am also aware the share price is likely to be significantly higher within a year or two.

Amazon has tremendous optionality. They are the second largest global retailer (amazon.com); the largest and leading cloud services provider (Amazon Web Services); a leader in the emerging streaming industry (Amazon Prime), developing and producing award winning shows, and live broadcasts; and a manufacturer of numerous electronic devices and services. They are also involved in healthcare, autonomous vehicles and other areas.

While Amazon is no longer directly led by its founder, he remains as the Executive Chairman, it is led by people who have been with Amazon for ten years or more. As well, revenues and earnings per share have been growing steadily for years (although this year could be a speed bump). Amazon has a significant competitive advantage thanks to their well-known brand, buying power The Amazon brand Finally, they have proven, experienced management who I feel are capable of leading Amazon through this current phase of high inflation and rising interest rates.

Put this all together and I feel the reward well outweighs the risk.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Revenue of $2,178 for the three months ended September 30, compared to $8,932 for the same period in 2021. A decrease of almost 75%.

Net loss of $1,675 for the three months ended September 30, compared to net income of $3,164 in the same period in 2021.

Diluted loss per ordinary share of $0.03 for the three months ended September 30, compared to net earnings per share of $0.06 for the same period in 2021.

Revenue of $7,131 for the nine months ended September 30, compared to $32,845 for the same period in 2021. A decrease of over 78%.

Net loss of $5,959 for the nine months ended September 30, compared to net earnings of $13,356 in the same period in 2021.

Diluted loss per ordinary share of $0.11 for the nine months ended September 30, compared to net earnings per share of $0.25 for the same period in 2021.

Revenue of $158,641 for the three months ended September 30, compared to $128,141 for the same period in 2021. An increase of almost 24%.

Net loss of $24,827 for the three months ended September 30, compared to net loss of $9,311 in the same period in 2021.

Diluted loss per ordinary share of $0.19 for the three months ended September 30, compared to a loss per ordinary share of $0.07 for the same period in 2021.

Revenue of $456,876 for the nine months ended September 30, compared to $365,941 for the same period in 2021. An increase of over 25%.

Net loss of $73,385 for the nine months ended September 30, compared to net earnings of $33,684 in the same period in 2021.

Diluted loss per ordinary share of $0.56 for the nine months ended September 30, compared to a loss per ordinary share of $0.27 for the same period in 2021.

Revenue of $611,402 for the three months ended September 30, compared to $521,658 for the same period in 2021. An increase of almost 18%.

Net loss of $73,476 for the three months ended September 30, compared to net loss of $83,340 in the same period in 2021.

Diluted loss per ordinary share of $0.45 for the three months ended September 30, compared to a loss per ordinary share of $0.53 for the same period in 2021.

Revenue of $1,769,131 for the nine months ended September 30, compared to $1,478,472 for the same period in 2021. An increase of over 20%.

Net loss of $9,849,460 for the nine months ended September 30, compared to net loss of $417,808 in the same period in 2021.

Diluted loss per ordinary share of $61.09 for the nine months ended September 30, compared to a loss per ordinary share of $2.68 for the same period in 2021.

Revenue of $1,346 for the three months ended September 30, compared to $1,375 for the same period in 2021. A decrease of 2.1%.

Net income of $203 for the three months ended September 30, compared to net income of $354 in the same period in 2021.

Diluted earnings per ordinary share of $0.41 for the three months ended September 30, compared to $0.70 for the same period in 2021.

Revenue of $4,091 for the nine months ended September 30, compared to $4,132 for the same period in 2021. A decrease of over 18%.

Net earnings of $595 for the nine months ended September 30, compared to net earnings of $734 in the same period in 2021.

Diluted earnings per ordinary share of $1.19 for the nine months ended September 30, compared to $1.44 for the same period in 2021.

Portfolio 2

Portfolio 2 for the week ended October 28, 2022: UP

Microsoft had decent first quarter earnings, however, the guidance they provided on future growth was below expectations. The market does not like surprises, especially negative ones, so the stock was punished, sending the share price down. The company has not changed, just the share price.

Microsoft has partnered with Meta (NASD:META) to integrate Microsoft’s productivity applications (Office, Teams, etc.) and Xbox gaming platform with Meta’s virtual reality (VR) headset. The theory is employees will be able to interact with colleagues around the world in a completely unique way. I am interested to see people respond to wearing a headset while working and how this whole VR experience plays out.

In an attempt to capture a part of a multi billion-dollar industry, Microsoft is building up its supply of Chinese video game content and helping to grow the number of Chinese game and content developers.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Revenue of $2,553 for the three months ended September 30, compared to $2,196 for the same period in 2021. An increase of over 16%.

Net income of $371 for the three months ended September 30, compared to net income of $342 in the same period in 2021.

Diluted earnings per ordinary share of $0.68 for the three months ended September 30, compared to earnings of $0.62 for the same period in 2021.

Revenue of $7,875 for the nine months ended September 30, compared to $6,865 for the same period in 2021. An increase of over 22%.

Net earnings of $1,094 for the nine months ended September 30, compared to net earnings of $1,034 in the same period in 2021.

Diluted earnings per ordinary share of $2.01 for the nine months ended September 30, compared to earnings of $1.92 for the same period in 2021.

Portfolio 3

Portfolio 3 for the week ended October 28, 2022: UP

Despite posting a net loss for the third quarter and the first nine months of 2022, Shopify grew revenue by 22% year over year, whereas revenue growth was 16% a year ago. It is a good sign when your revenue growth is accelerating. Shopify also posted a net loss of US$ 0.02 for the quarter, beating analysts’ expectations of a $0.07 loss.

Kneat.com (TSX:KSI) has signed a three-year agreement with one of the world’s largest healthcare companies. kneat.com’s Kneat Gx software platform will be used to manage the healthcare company’s validation lifecycle of up to fifty IT systems across eight countries.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Statistics Canada data released this week showed Canada’s Consumer Price Index (CPI) year over year inflation rate for September rose to 6.9%, decelerating from 7% in August (analysts were expecting 6.8%). That is the third successive month that the year over year CPI has dropped. As well, Canada’s core CPI (CPI without gas and food prices) was up slightly from 5.3% in August, year over year, to 5.4% year over year in September.

While a drop in the overall CPI is a good sign inflation is moving in the right direction (down), it is still well above the BoC’s target of 2%. This latest data, combined with the Bank of Canada’s (BoC) commitment to getting inflation under control, leads analysts to believe they will raise the Canadian benchmark interest rate by 0.75% next week, raising the rate to 4.0%, a 14 year high. Anyone with any type of debt that has a variable interest rate is feeling the bite of these increasing rates. To make matters worse, analysts increasingly believe the pace of the rate hikes, with the likelihood there are more to come, will push Canada into a recession (a period of negative economic growth). We do not want a recession as they can cause businesses to fail, fewer job opportunities and lower wages.

On the other hand, some analysts believe the upcoming rate hike will be 0.5% as the BoC attempts to avoid a recession. We shall see next week.