Fractional shares….

As expected, the Bank of Canada (BoC) raised the benchmark interest rate in Canada by 0.75%, bringing the Canada’s benchmark interest rate to 3.25%, a 14 year high. The new rate is now above their target range of between 2% – 3%. The BoC said they will maintain their aggressive stance and the rate will continue to rise as they battle inflation, approaching a 40 year high. The only question is how much but rumours have ranged up to 4%. COVID-19, supply-chain issues and Russia’s invasion of Ukraine continue to boost prices of goods and services which contributes to high inflation rates.

Of course, Canadian banks immediately announced an increase in their Canadian prime rate by 0.75% basis points to 5.45%, effective September 8, 2022. Where the benchmark rate is what the BoC (or any nation’s central bank) lends out at to banks, the prime rate is the interest rate the Canadian banks use to set their interest rates to customers for loans, lines of credit and mortgages. The prime rate closely follows the BoC’s benchmark rate.

Inflation reached across the Atlantic where the Bank of England forecasts inflation in the United Kingdom will peak above 13%, the highest since the early 1980s. However, some analysts believe inflation could reach 22% in the UK, closer to the 1975 postwar record. Across the channel, in the European Union, the European Central Bank (ECB) cranked up the interest rate by 0.75%, the largest raise since the ECB came into existence, bringing the EU benchmark (what the central bank lends out at to banks) rate to 1.25%. As well, the ECB suggested there could be several similar moves in the future as part of the ECB’s fight against inflation.

The big driver of inflation in the UK and Europe is Russia’s invasion of Ukraine. In response to European sanctions, Russia has turned off the taps of their natural gas pipelines which is used to heat many homes and run many factories. Despite requests from various European governments, the Canadian government says there is no business case to supply natural gas and oil to Europe. Hmmm.

Ethereum blockchain is undergoing a potentially transformative software update this. Called the Merge, it is expected to decrease the energy used to create new coins and validate transactions by 99.95%. The Merge is designed to make Ethereum more competitive in price and usability compared to the king of cryptocurrency – Bitcoin. Investors in Ethereum, like me, hope the changes will lead to significant rise in the price of Ethereum. For more information on Ethereum, check out the Ethereum.org

While it is not investing related news, Queen Elizabeth II passed away this past week. Her reign of 72 years was longest in Britain’s history. With her passing, Prince Charles becomes King of the United Kingdom and 14 other countries. The British national anthem was updated, and it will now be ‘God Save the King.’ Bringing it back to wealth through investing, I admit a tenuous tie, does Canada and every other nation that has Queen Elizabeth II on their currency have to print new currency featuring King Charles III? And what happens to existing currency featuring Queen Elizabeth? 😊

While we ponder those big questions, let’s check out the week that ended September 9…..

Weekly Market Review

Monday: The stock markets in both Canada and the USA were closed for Labour Day.

Tuesday: The shortened week got off to a rocky start with all four North American Indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – ending lower. In Canada, all Canadian sectors ended the day lower as investors await the latest interest rate hike from the Bank of Canada (BoC), due later this week. Many analysts expect a 0.75% hike, but it could be a second 1.0% as Canada’s central bank continues its fight to stamp down inflation.

In the US, interest rates, energy supply concerns and Covid-19 lockdowns in China all weighed down the markets. Nasdaq pushed its losing streak to seven straight sessions, as higher interest rates continue to take their toll on the big tech companies and other growth, interest rate sensitive companies.

Wednesday: I would like to think the BoC limiting their interest rate hike to 0.75% was the reason all four of the major North American Indexes ended the day higher, but the BoC is not influential enough to impact the American markets. And I am sure Americans would agree with that. 😊 In Canada, all the Canadian sectors ended higher, except Energy, which sank as the price of oil fell almost $5 today.

In the US, it was a similar story as ten of the eleven S&P sectors posted a gain, with the Energy sector being the lone exception. I do not see today’s rally as anything but a bounce since the US Federal Reserve (Fed) is signalling another interest rate hike at their next meeting in late September. Fears of the size of the upcoming hike will likely send the markets lower. However, the rally was enough for the Nasdaq to get back into the win column.

Thursday: With all four Indexes closing higher today, a winning streak has been established. Its only two, but it is a start. 😊 In Canada, the Basic Materials (mining companies), Financials (banks) and Technology sectors led the way, with only Telecommunications, Consumer Staples and Healthcare sectors ending lower.

In the US, the chairman of the Fed confirmed the Feds’ aggressive stance on fighting inflation, signalling another significant interest rate hike is in the works later this month. In the stock markets, the Utilities, Consumer Cyclicals, and Healthcare sectors led the way higher, while the Telecommunications, Consumer Staples and Utilities sectors were the only sector that failed to end higher.

Friday: The week ended on a fine note with all four Indexes ending higher for the day, and for the week. In Canada, the TSX had its largest gain since May 2022 as Basic Materials companies (mining and fertilizer companies) led broad-based gains, with all the Canadian sectors ending in the black. The Canadian Technology, Consumer Staples, and Basic Materials sectors were the frontrunners on the TSX.

In the US, investors went on a shopping spree, pushing all eleven S&P sectors upward. Leading the way were the Basic Materials, Energy, and Technology sectors. Analysts and investors now turn their focus to Tuesday’s August Consumer Price Index (CPI) report for an indication if the higher interest rates are having an impact on slowing consumer spending.

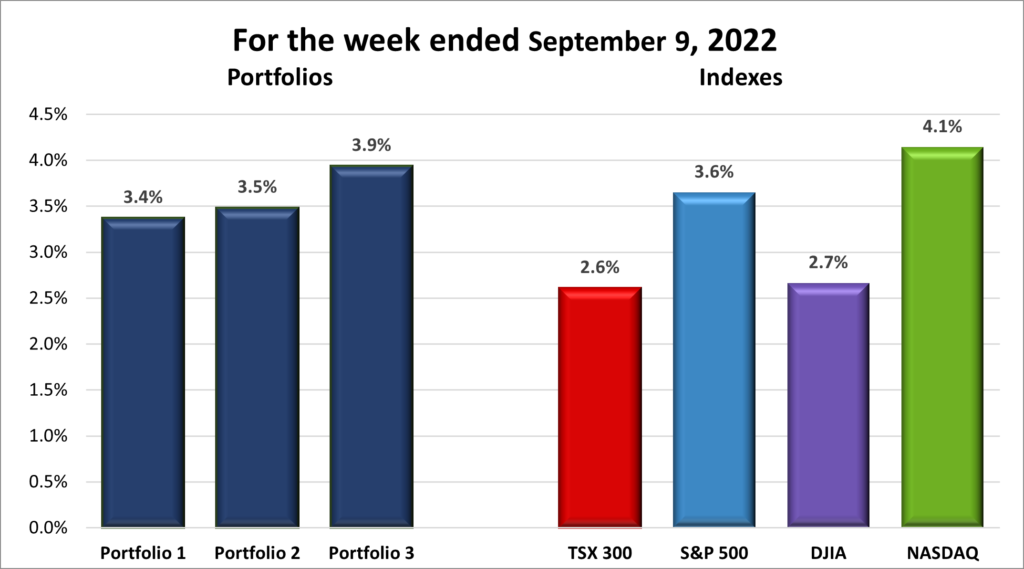

For the week, the TSX gained 2.6% ,the S&P 500 gained 3.6%, the Dow rose 2.7% and the Nasdaq climbed 4.1%.

Weekly Portfolio Review

A bit of a surprising week in the North American stock markets. All four Indexes snapped a three-week slump and recovered some of the losses of the previous weeks. With recent aggressive interest rate hikes and talks of equally aggressive rate hikes in the future for both Canada and the USA, I thought the Indexes would be essentially flat at best. Once again, I prove to myself that on any given day, I’ve no idea which way the market will go. 😊

As for the three Portfolios, again I was expecting all three to lose ground this week, so I am pleasantly surprised to see they all ended the week higher. Once again, I am impressed to see the more balanced Portfolio 2 essentially keeping pace with the more aggressive Portfolios 1 and 3. I will take the wins this week, but we are in for a bumpy ride for the next while.

Companies on the Radar

Amazon (NASD:AMZN), Ferrari (NYSE:RACE) and Brookfield Select Opportunities (TSX:BSO.UN) remain on my Radar List, and have been joined by two new companies.

XPEL, Inc. (NASD:XPEL): XPEL provides paint and interior protection products for vehicles, watercraft, homes, and commercial buildings. They are one of the top suppliers of films to protect paint, windows, and interiors to the automotive industry and are expanding into the marine, home and building markets, as well as expanding globally. They company has shown strong revenue and profitability growth.

WESCO International (NYSE:WCC): Originally the distribution arm of Westinghouse, Westinghouse Electric Supply Company (WESCO) was spun off in 1993. After numerous acquisitions, including Anixter International in 2020, WESCO now provides business-to-business distribution, logistics services, supply chain solutions, network & security solutions, electrical & electronic solutions, and utility power solutions. I like that Wesco has multiple revenue sources in multiple markets.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended September 9, 2022: UP ![]()

Portfolio 1 commentary with links to each company the first time mentioned.

- Alphabet’s (NASD:GOOGL) YouTube’s has become an economic powerhouse the last few years thanks to ad sales that grew 254% in the years since 2017. YouTube is watched on smart devices and televisions, with over 700 million hours watched on smart TVs alone in January 2022. As well, in 2019, at least 500 hours of footage are uploaded to YouTube every minute. I am sure this number has gone up considerably since then. With all these eyeballs constantly checking out content on the platform, it is only a matter of time before Google starts to increase the monetization of YouTube.

- Lightspeed Commerce Inc. (TSX:LSPD), announced the launch of Lightspeed Restaurant — a “unified hospitality commerce and point-of-sale (POS) platform.” The platform will be introduced in Australia before expanding to other countries.

- Canada’s competition watchdog said the sale of Shaw Communications Inc (TSX:SJR.B) unit Freedom mobile division to Quebecor Inc (TSX:QBR.B) was not enough to eliminate antitrust concerns with the proposed C$20 billion merger of Shaw and Rogers Communications Inc. (TSX:RCI.B). This means the merger will drag on longer as Shaw and Rogers negotiate with the Canadian regulators to approve the merger.

- Its anticipated Apple (NASD:AAPL) will ask the Federal court to toss the decision to award US$ 502 million to VirnetX Holdings over infringing on their Virtual Private network (VPN) patents. One of the reasons Apple will cite is the patents were invalid during the period between the trial and a retrial.

- Electric car maker Tesla (NASD:TSLA), cranked up their deliveries in China, almost tripling its July sales. This sounds amazing but one needs to remember the July numbers were down due to the plant being closed for upgrades. Nonetheless, nearly 77,000 Tesla’s sold in August is an impressive number.

- In other Tesla news, Tesla may add mining company to its list of capabilities. The company is considering building a lithium refinery on Texas’s gulf coast. The lithium refinery would secure the supply of one of the key resources required in the development of electric batteries used in electric vehicle. If the refinery goes ahead, Tesla will be the first vehicle manufacturer to also be a mining company.

- In related news, General Motors (NYSE:GM) has seen sales in China drop by a third over the last five years as the Chinese clamour for electric cars, especially from Chinese companies. To turn the tide, GM will launch ‘experience centres’ in major cities, where invited guests can view GM’s prospective electric vehicles.

- In a sign that supply chains are slowly returning to normal, cargo shipping rates are tumbling. The cost of shipping a 40-foot container on various south east Asian routes is down as much as 60%. On one hand, this should ease some of the inflationary pressures caused by high shipping rates. On the other hand, it explains why ZIM Integrated Shipping (NYSE:ZIM) has seen its share price cut in half.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

Docusign, Inc.

All currency listed in thousands of US dollars

Selected highlights from their second quarter 2023 financial results on September 8, 2022

- Revenue of $622,184 for the three months ended June 30, compared to $511,844 for the same period in 2021. An increase of over 21%.

- Net loss of $45,078 for the three months ended June 30, compared to net loss of $25,501 in the same period in 2021.

- Diluted earnings per ordinary share of $0.22 for the three months ended June 30, compared to $0.13 for the same period in 2021.

- Revenue of $1,210,876 for the six months ended June 30, compared to $980,923 for the same period in 2021. An increase of over 23%.

- Net loss of $72,451 for the six months ended June 30, compared to net loss of $33,855 in the same period in 2021.

- Diluted earnings per ordinary share of $0.36 for the six months ended June 30, compared to $0.17 for the same period in 2021.

Portfolio 2

Portfolio 2 for the week ended September 9, 2022: UP ![]()

- Guardant Health (NASD:GH) announced they will present data showing how the “use of Guardant Health’s blood tests and real-world evidence dataset to advance cancer therapy trials, predict and monitor patient response to therapy, and identify genomic mechanisms of acquired resistance to cancer therapy.”

- Alimentation Couche-Tard (TSX:ATD) changed their stock symbol from ATD.A to ATD.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

No C$ dividends this past week.

US $

Microsoft Corp (NASD:MSFT)

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended September 9, 2022: UP ![]()

- Shopify (TSX:SHOP) is shaking up its C level management. Kaz Nejatian takes over immediately as their new Chief Operating Officer, taking over from retiring Toby Shannan. As well, Chief Financial Officer Amy Shapero is stepping down after Shopify’s third quarter 2022 earnings announcement in late October. Her replacement, Jeff Hoffmeister comes over from Morgan Stanley’s Technology Investment Banking group.

- In their letter to shareholders, Enghouse Systems (TSX:ENGH) stated they had C$229 million in cash, cash equivalents and short-term inventory with no external debt, cash flows of $29.8 million, and bought back $9 million of shares. Not bad. Now to get their share price moving upward again.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

No C$ dividends this past week.

US $

Microsoft Corp (NASD:MSFT)

Quarterly Reports

Enghouse Systems Ltd.

All currency listed in thousands of Canadian dollars

Selected highlights from their third quarter 2022 financial results on September 8, 2022

- Revenue of $102,111 for the three months ended June 30, compared to $117,644 for the same period in 2021. A decrease of almost 13%.

- Net income of $18,081 for the three months ended June 30, compared to net income of $21,227 in the same period in 2021.

- Diluted earnings per ordinary share of $0.33 for the three months ended June 30, compared to $0.38 for the same period in 2021.

- Revenue of $319,525 for the nine months ended June 30, compared to $354,078 for the same period in 2021. A decrease of 10%.

- Net earnings of $57,549 for the nine months ended June 30, compared to net earnings of $62,608 in the same period in 2021.

- Diluted earnings per ordinary share of $1.03 for the nine months ended June 30, compared to $1.12 for the same period in 2021.