Loose change….

A busy week of earnings for the three Portfolios with 17 companies across the Portfolios announcing their respective quarterly results. I was not sure if the light at the end of the tunnel was going to be the end of the tunnel or an approaching train. It turns out it was light at the end of the tunnel. 😊

A busy week of earnings for the three Portfolios with 17 companies across the Portfolios announcing their respective quarterly results. I was not sure if the light at the end of the tunnel was going to be the end of the tunnel or an approaching train. It turns out it was light at the end of the tunnel. 😊

Many of the companies listed on the North American exchanges (including the aforementioned 17 companies) had earnings reports that were viewed as positive by analysts and the market in general, soothing investor fears. As well, the US Federal Reserve (Fed) made history when it raised its benchmark interest rate 0.75%, as anticipated, for the second time in as many months. The Fed said a future 0.75% interest rate hike was possible but did commit to any specific rate hike. This wiggle room provided investors hope for a slower pace of rate hikes.

Speaking of rallies, have you noticed the S&P 500 Index is chipping away some of the losses from the first half of 2022. The Index is up over 9% in July. A good start to the second half of the year.

The energy company heavy Toronto Stock Exchange continues to benefit from the surge in oil prices caused by the world reopening after the lifting of Covid-19 restrictions, and the Russian invasion of Ukraine squeezed supplies even tighter. The Energy sector is one of the few sectors to gain ground in 2022. However, the good times in the energy sector probably will not last.

July was not all roses as interest rate hikes in Canada and the USA mean the cost of borrowing money has gotten higher. For companies, this means more money is required to service their debt rather than growing their company. For us consumers, it means mortgages, lines of credit, credit cards, and loans will all get steeper.

Looking at the bounce in share prices this past month, I cannot help but wonder, “Is the market correction/bear market over?” I hope August is as good to investors as July. In the meantime, while we ponder whether the stock market has finally bottomed, lets take a look at the past week ….

Weekly Market Review

Monday: Earnings week has begun in both Canada and the United States. To mark the start of a busy week of earnings reports, the four major North American Indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – ended the day …. relatively flat. The TSX ended the day higher thanks to a rise in Canadian listed oil companies.

In the US, the Indexes bounced up and down as investors await earnings reports from the big technology companies, and for the US Federal Reserve (Fed) meeting later this week where they will announce their latest interest rate hike. A 0.75% rate hike is anticipated but a full 1% raise is not out of the question.

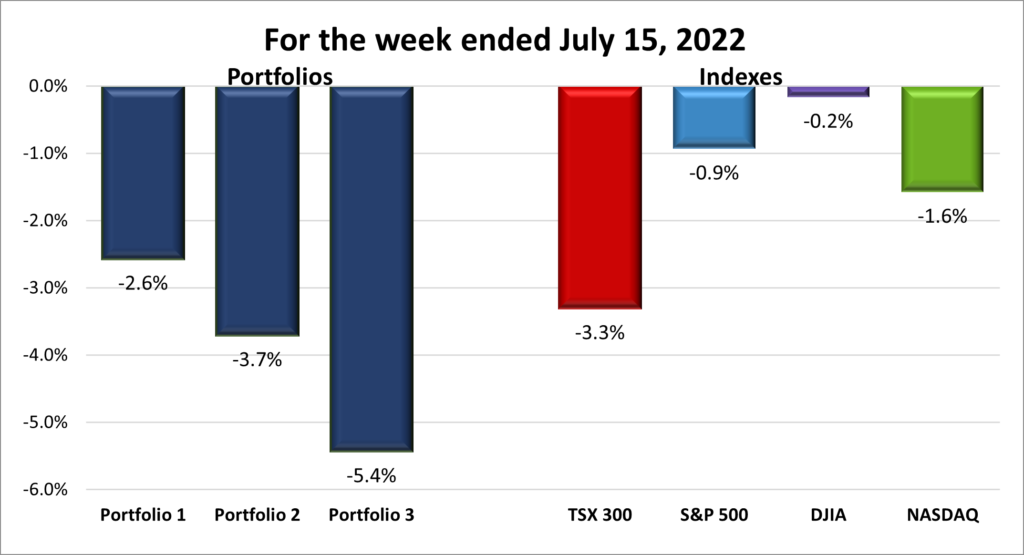

Tuesday: Monday’s relatively flat performance by all four Indexes is looking rather good after today’s poor performance. The TSX was the best performer, ‘only dropping’ 0.69%. The main culprit was the Canadian Technology sector which was dragged down by Shopify’s (TSX:SHOP) 13.6% fall after announcing they would layoff 10% of their workforce. Portfolio 3 is going to feel the pain of that drop.

In the US, all three Indexes slid backwards after Walmart (NYSE:WMT) lowered its profit forecast, causing the value of its shares to fall 7.6%, as well as the share price of other retail companies to drop. Most retailers are part of the Consumer Discretionary sector. The only good news for me was Amazon (NASD:AMZN) share price dropped 5.2% today. Because of Amazon’s market capitalization size (its huge) it was the biggest anchor on Nasdaq.

Tomorrow is a big day as the Fed will announce its latest interest rate hike. Will the Fed stick with a 0.75% hike or be more aggressive in its battle to control inflation and raise the interest rate a full 1%? We shall see.

Wednesday: Nothing like good news to lift the Indexes. The Fed raised interest rates 0.75% rather than the feared 1%. Combined with strong earnings reports from big technology companies, investors spirits were raised, and they jumped back into the markets. In Canada, the TSX was lifted by strong reports from Shopify, despite an earlier announcement of upcoming layoffs, and CN Rail (TSX:CNR), among other reporting companies. The Canadian Technology sector led the way in a broad-based rally where only the Non-Cyclical Consumer Goods & Services sector failed to gain ground.

In America, it was also a broad-based rally with all eleven S&P sectors gaining ground. Nasdaq rose 4% and the S&P rose 3.9%, both biggest one day gains since April 2020. The big driver for both Indexes was the Technology sector which was buoyed by strong earnings reports from Microsoft (NASD:MSFT), Alphabet (NASD:GOOGL) and others. Nothing like seeing companies you own mentioned as drivers of Index gains. 😊

Thursday: All four Indexes posted a second straight day of gains. In Canada, the TSX hit its highest point in six weeks as all Canadian sectors edged higher. In the US, all three Indexes ended at least 1% higher as investors began to speculate the Fed may not be as aggressive in raising the benchmark interest rate. The upbeat mood led to another broad-based rally sending the Indexes higher.

Friday: The stock markets ended the day on an upbeat note as today’s gains meant all four Indexes ended the week on a positive note. In Canada, the combination of strong earnings reports from Energy and Basic Materials sector companies, and initial data indicating Canada’s economy continues to expand, propelled the TSX higher.

In the US, solid earnings from the technology mega cap companies, and hope that the Fed will be less aggressive with future interest rate hikes led to a rally in the American stock markets. Healthcare, and Non-Cyclical Consumer Goods & Services were the only sectors not to end the day in the black.

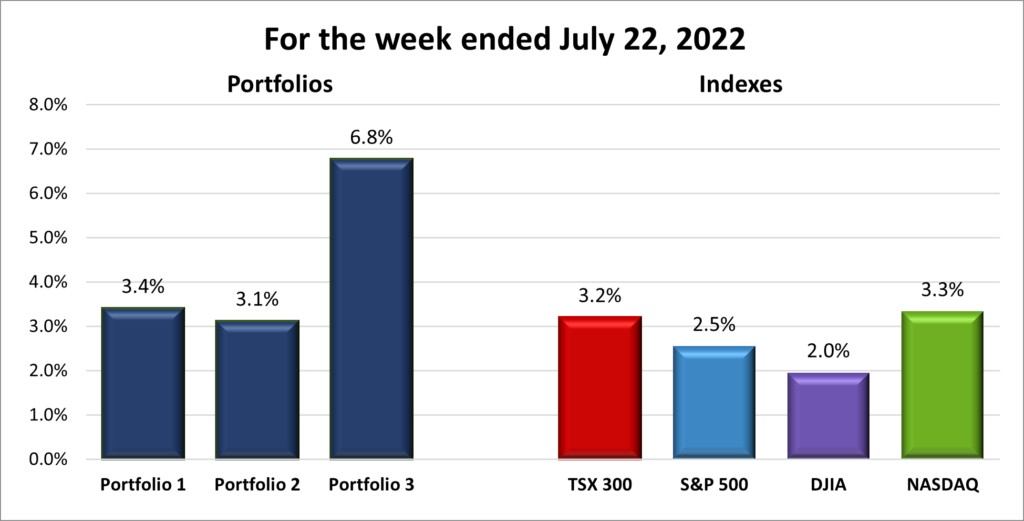

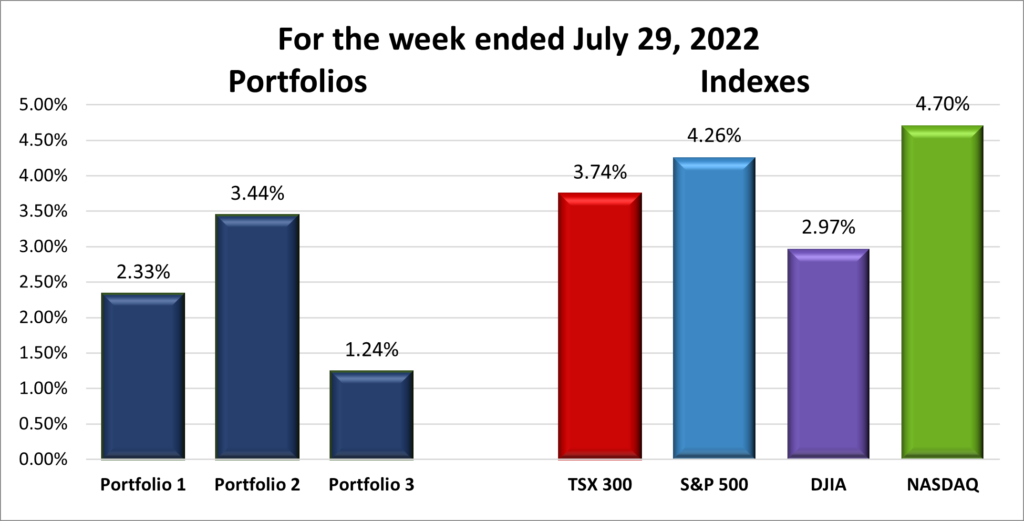

For the week, the TSX grew 3.74%, the S&P gained 4.26%, the DJIA advanced 2.97%, and the Nasdaq climbed 4.70%.

It has been a while since all four major North American Indexes ended a month higher than they started. July quietly turned out to be the best month for the S&P since November 2020, and the Nasdaq had its strongest performance since April 2020. For the month, the TSX advanced 4.4%, the S&P jumped 9.12%, the DJIA rose 6.73%, and the Nasdaq out did them all, rising 12.3%.

Weekly Portfolio Review

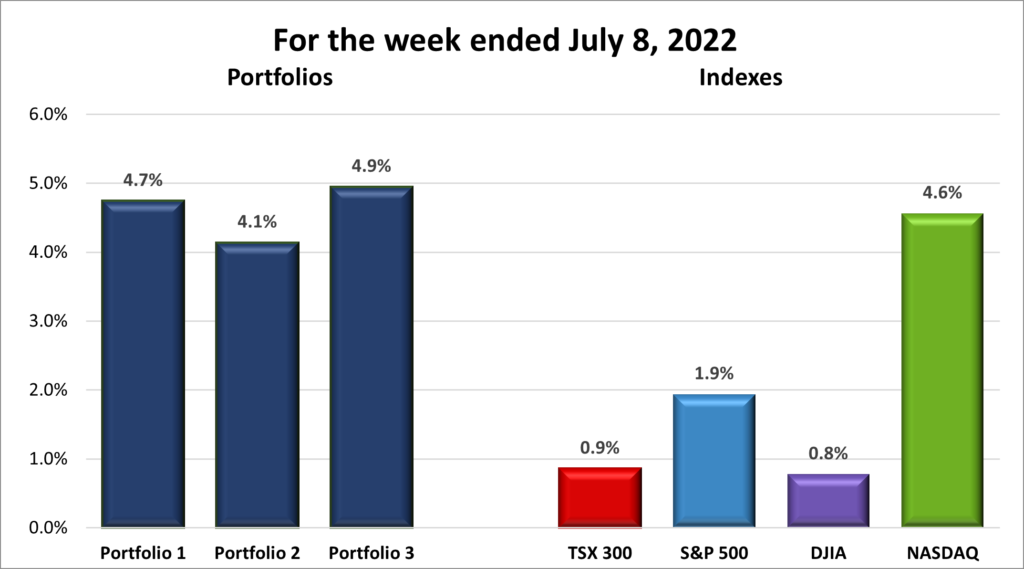

Another good week in the stock markets, with all four major North American Indexes ending the week higher. Even more impressive, all four Indexes gained at least 4% for July. I cannot remember the last time that happened. Certainly not in 2022.

As for the Portfolios, for the second consecutive week all three ended the week in the black. That is three of the four weeks in July they have gained ground. Not as much as last week, but gains are gains. With the Nasdaq having a great month its no wonder the Portfolios are slowly climbing out of the hole created by the 2022 bear market. Portfolio 1 continues to benefit from the big technology companies, as well as the energy companies picked up in late 2021. Portfolio 2 is the most balanced of the three portfolios. It does not have any one company driving the portfolio, but neither does it have any companies dragging it down. It also benefits from many of the companies paying a decent dividend. Finally, Portfolio 3 is largely technology driven with Shopify being the biggest holding. As Shopify goes, so goes Portfolio 3. Many of the other holdings, including technology companies, are smaller, Canadian companies that do not get the same growth rate as American based companies. Something I need to investigate. For now, after six months of watching the Portfolios lose ground, I am happy to see all the Portfolios finally end a month higher.

Companies on the Radar

Amazon and Ferrari (NYSE:RACE) continue as the only companies on my Radar. I am still regretting not buying these companies at the end of June when both were cheaper. Trying to out think the market appears to have failed, again. Argh! ☹

I still need to run both companies through my Multibagger Analysis.

- Amazon: scored a 6 out of 13 on my Radar Check test.

Figure 1: Radar Check of Amazon

- Ferrari: scored a 9 out of 13 on my Radar Check test.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended July 29, 2022: UP ![]()

- Amazon announced Rivian (NASD:RIVN) electric vans are now delivering packages in select cities and they (Amazon) plan to have them making deliveries in 100 cities by the end of the year. Amazon first started making deliveries in Rivian vans in late summer 2021. It would be interesting to know how many Rivian vans Amazon has received, how many are making daily deliveries, and any issues with the vehicles.

- To increase production at its Gigafactory’s in Austin, Texas and Berlin, Germany, Tesla (NASD:TSLA) plans to raise its capital spending by US$ 1 billion.

- GM (NYSE:GM) announced the US Energy Department has agreed to loan GM US$ 2.5 billion to help build GM’s Ultium battery cell facilities in the US. This will be the government’s first loan for a battery cell manufacturing project under the vehicle program.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

- Shaw Communications Inc (TSX:SJR.B)

US $

No US$ dividends this past week.

Quarterly Reports

Alphabet Inc.

All currency listed in millions of US dollars

Selected highlights from their second quarter 2022 financial results on July 26, 2022

- Revenues of US$ 69,685, up 13% year over year.

- Operating margin of 28%, compared with a margin of 31% in the previous year.

- Net income of US$ 16,002.

CN Rail

All currency listed in millions of Canadian dollars

Selected highlights from their second quarter 2022 financial results on July 26, 2022

- Record revenues of C$4,344 million, an increase of C$746 million or 21%.

- Record operating income of C$1,769 million, an increase of 28%.

- Free cash flow for the first six months of 2022 was C$1,568 million compared to C$1,280 million for the same period in 2021.

General Motors Co.

All currency listed in millions of US dollars

Selected highlights from their second quarter 2022 financial results on July 26, 2022

- Revenue of $35.8 versus 34.2, a ~5% increase year over year.

- Net income of $1.7 compared to $2.8 in the same period last year.

- First and only company to operate a commercial, driverless ride hail service in a major US city.

- Building out a nationwide electric vehicle fast charging network.

- Binding agreements in place to secure ALL battery raw material supporting GM’s goal of 1 million units of annual capacity in North America in 2025.

Visa Inc.

All currency listed in billions of US dollars

Selected highlights from their third quarter 2022 financial results on July 26, 2022

- Revenues of $7.3, up 19% compared to the same period last year.

- Net income of $3.4, up 32% compared to the same period last year.

- Returned $3.3 of capital to shareholders in the form of share repurchases and dividends.

- Total processed transactions, for the three months ended June 30, 2022, were 49.3 billion, a 16% increase over the prior year

Upwork Inc.

All currency listed in millions of US dollars

Selected highlights from their second quarter 2022 financial results on July 27, 2022

- Revenue grew 26% year-over-year to $156.9 in the second quarter of 2022.

- Gross profit was $116.0 for the second quarter of 2022, or 74% of revenue, compared with 73% of revenue in the prior quarter and 73% of revenue in the year prior.

- Net loss was $(23.8) in the second quarter of 2022 compared with GAAP net loss of $(16.5) million in the second quarter of 2021.

- Gross Services Volume in the second quarter of 2022 was just over $1 billion, with continued strong year-over-year growth of 19%.

- Guiding third-quarter 2022 revenue to be between $156 million and $158 million, which is 23% year-over-year growth at the midpoint.

Teladoc Health Inc.

All currency listed in thousands of US dollars

Selected highlights from their second quarter 2022 financial results on July 27, 2022

- Second quarter revenue grows 18% year-over-year to $592.4 million.

- Net loss of 3,101,461 compared to a net loss of 133,819 in the same quarter in the previous year, primarily driven by non-cash goodwill impairment charge of $3.0 billion.

- Gross margin, which includes depreciation and amortization, was 68.2% for the second quarter of 2022, compared to 67.9% for the second quarter of 2021.

- For the third quarter, anticipate revenues of $600 – 620 million and a net loss of $0.85 – $0.60 per share.

- For fiscal 2022, anticipate revenues of $2,400 – $2,500 million and a net loss per share of $62 – $61 thanks to the impairment charge mentioned in bullet 2.

Cargojet Inc.

All currency listed in Canadian dollars

Selected highlights from their second quarter 2022 financial results on July 27, 2022

- Revenues for the quarter were $246.6 million compared to second quarter 2021 Revenues of $172.1 million.

- Net income for the quarter was $160.9 million (net income of $26.2 million excluding warrant valuation gain) compared to net loss of $11.1 million in 2021 (net income of $23.6 million excluding warrant valuation loss).

Roku, Inc.

All currency listed in thousands of US dollars

Selected highlights from their second quarter 2022 financial results on July 28, 2022

- Revenue grew 18% year over year to $764 million for the three months ended June 30.

- Net loss of $110,513 for the three months ended June 30.

- Total net revenue of $1,498,105 for the six months ended June 30.

- Net loss of $134,003 for the six months ended June 30.

- Added 1.8 million incremental active accounts to reach 63.1 million.

- Average Revenue Per User grew to $44.10 (trailing 12-month basis), up 21% year over year.

Apple Inc.

All currency listed in millions of US dollars

Selected highlights from their third quarter 2022 financial results on July 28, 2022

- Posted a June quarter revenue record of $83.0 billion, up 2 percent year over year.

- Net income of $19,442 for the three months ended June 30, 2022, compared to $21,744 for the same period in 2021.

- Net income of $79,082 for the nine months ended June 30, 2022, compared to $74,129 for the same period in 2021.

- Generated nearly $23 billion in operating cash flow and returned over $28 billion to shareholders.

- Declared a cash dividend of $0.23 per share of the Company’s common stock.

TMX Group Ltd.

All currency listed in millions of Canadian dollars

Selected highlights from their second quarter 2022 financial results on July 28, 2022

- Revenue of $286.1, up 17% from $245.0 in Q2/21, including $27.3 from acquisition of voting control of BOX on January 3, 2022.

- Net income attributable to equity holders of TMX Group in Q2/22 was $92.1, compared with a net income attributable to equity holders of TMX Group of $77.3, for the second quarter of 2021.

- Revenue of $573.2 for the six months ended June 30, 2022, up 15% from $497.0 in the same period in 2021.

- Net income attributable to equity holders of TMX Group in the six months ended June 30, 2022, was $35.9.5, up 107% from $173.7, for the same period in 2021.

- Declared a dividend of $0.83 on each common share outstanding.

Portfolio 2

Portfolio 2 for the week ended July 29, 2022: UP ![]()

- Pushed by an activist investor, Suncor (TSX:SU) announced they were reviewing their investment in gas stations. One possible suitor is Alimentation Couche-Tard Inc. (TSX:ATD) since they have a strong Balance Sheet. The acquisition of Suncor’s gas stations would dramatically increase Couche-Tard’s footprint in Canada. However, I have two concerns. First, they get a good deal on the acquisition. Second, a sizable majority of these stations must be easily converted to what I call energy stations, where drivers can fuel up or charge up. Based on their record, I am confident they can get a fair deal. As for the second concern, Couche-Tard would need to perform a great deal of due diligence, plus an ability to read the political tea leaves to determine how much incentive there is to add charging stations to these properties.

- Microsoft missed analyst expectations for the quarter, however, they suggested their next fiscal year looked good, and that forecast was enough to send the share price higher. Microsoft received a boost from its growing advertising revenue stream this past quarter, and that should only get better thanks to the recently announced deal to manage streaming advertising for Netflix.

- Telus (TSX:T) was named Canada’s fastest mobile network by Ookla for the 10th consecutive time. Telus has also been recognized by UK based Opensignal and New York based JD Power for network excellence.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

- TC Energy Corp (TSX:TRP)

US $

No US$ dividends this past week.

Quarterly Reports

Microsoft Corp.

All currency listed in US dollars

Selected highlights from their fourth quarter 2022 financial results on July 26, 2022

Fourth quarter highlights

-

- Revenue was $51.9 billion and increased 12% (up 16% in constant currency)

- Operating income was $20.5 billion and increased 8% (up 14% in constant currency)

- Net income was $16.7 billion and increased 2% (up 7% in constant currency)

- Diluted earnings per share was $2.23 and increased 3% (up 8% in constant currency)

Fiscal year highlights

-

- Revenue was $198.3 billion and increased 18% (up 19% in constant currency)

- Operating income was $83.4 billion and increased 19% (up 21% in constant currency)

- Net income was $72.7 billion GAAP and increased 19%, and $69.4 billion non-GAAP and increased 15% (up 16% in constant currency)

- Diluted earnings per share was $9.65 GAAP and increased 20%, (up 17% in constant currency)

TC Energy Corporation

All currency listed in millions of Canadian dollars

Selected highlights from their second quarter 2022 financial results on July 28, 2022

- Net income attributable to common shares of $0.9 billion compared to a net income of $1.0 billion in 2021.

- Declared a quarterly dividend of $0.90 per common share for the quarter ending September 30, 2022.

Fortis Inc.

All currency listed in millions of Canadian dollars

Selected highlights from their second quarter 2022 financial results on July 28, 2022

- Second quarter net earnings of $284, an increase of $31 compared to the same period last year.

- Year to date earnings of $634, an increase $26 compared to the same period last year.

- A dividend of $0.535 per common share of the Corporation, payable on September 1, 2022.

Mitek Systems Inc.

All currency listed in US dollars

Selected highlights from their third quarter 2022 financial results on July 28, 2022

- Total revenue increased 24% year over year to $39.3 million in a record third quarter.

- Net loss was $0.9 million, or $0.02 per diluted share.

iAG Financial Group

All currency listed in US dollars

Selected highlights from their second quarter 2022 financial results on July 28, 2022

- Net income attributed to common shareholders of $222 million.

- Return on common shareholders’ equity for the trailing twelve months of 12.5%.

- Approved a quarterly dividend of $0.6750 per common share payable in the third quarter of 2022, an increase of 8%, or $0.05, from the previous dividend paid.

Portfolio 3

Portfolio 3 for the week ended July 29, 2022: UP ![]()

- Shopify is laying off 10% of its workforce (approximately 1,000 employees) as the company contends with slowing growth caused by a drop in online shopping. Shopify benefitted greatly from a surge in demand during the Covid-19 pandemic but is feeling the pain now as shoppers return to in-store shopping. Shopify gambled that online shopping would continue to grow at a rapid pace even after the pandemic and hired up accordingly. They gambled wrong and as a result, they will have to downsize like a lot of other companies that increased their respective workforces during the pandemic. Online shopping/e-commerce will continue to grow, just at a slower pace than they predicted. Shopify is making the necessary changes to its business to adjust to the shifting landscape.

- Adyen (OTCM:ADYEY) has teamed up with Etsy (NASD:ETSY) to allow US buyers on the Etsy platform to round up their purchase total and that difference will be donated to the Brooklyn Community Foundation fund. The fund is used support people who face barriers to building their businesses.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

Microsoft Corp.

All currency listed in US dollars

Selected highlights from their fourth quarter 2022 financial results on July 26, 2022

Fourth quarter highlights

-

- Revenue was $51.9 billion and increased 12% (up 16% in constant currency)

- Operating income was $20.5 billion and increased 8% (up 14% in constant currency)

- Net income was $16.7 billion and increased 2% (up 7% in constant currency)

- Diluted earnings per share was $2.23 and increased 3% (up 8% in constant currency)

Fiscal year highlights

-

- Revenue was $198.3 billion and increased 18% (up 19% in constant currency)

- Operating income was $83.4 billion and increased 19% (up 21% in constant currency)

- Net income was $72.7 billion GAAP and increased 19%, and $69.4 billion non-GAAP and increased 15% (up 16% in constant currency)

- Diluted earnings per share was $9.65 GAAP and increased 20%, (up 17% in constant currency)

Shopify Inc.

All currency listed in US dollars

Selected highlights from their second quarter 2022 financial results on July 27, 2022

- Total revenue in the second quarter grew 16% year over year to $1.3 billion, which represents a three-year compound annual growth rate of 53%.

- Gross Merchandise Volume for the second quarter was $46.9 billion, which represents a three-year compound annual growth rate of 50% and an increase of $4.7 billion, or 11% over the second quarter of 2021.

- Monthly Recurring Revenue1 as of June 30, 2022, was $107.2 million. MRR increased 13% year over year, up from $95.1 million as of June 30, 2021.

- Net loss for the second quarter of 2022 was $1.2 billion, compared with net income of $0.9 billion, for the second quarter of 2021.

Real Matters Inc.

All currency listed in millions of US dollars

Selected highlights from their third quarter 2022 financial results on July 28, 2022

- Revenues of $78.7 for the three months ended June 30, down 39.2% from the same period last year.

- Net loss of $1.4 for the three months ended June 30, compared to net income of $5.3 for the same period last year.

- Revenues of $281.4 for the nine months ended June 30, down 25.6% from the same period last year.

- Net income of $.7 for the nine months ended June 30, compared to net income of $24.0 for the same period last year.

- Purchased 6.1 million shares under our normal course issuer bid at a cost of $27.2 million during the nine months ended June 30.