Loose change…

This past week Canada’s June inflation rate came in at 8.1%, the highest since 1983. I know I’m feeling the bite of inflation. Higher gasoline prices are driving (pun intended) a lot of that increase, but prices across the board are up – food, housing and transportation are all up. The last time inflation was this high (in 1983), the prime minister was Pierre Trudeau , the father of the current one. A coincidence? 😊

Don’t look now but thanks to a rally in technology companies, the S&P 500 Index, the Dow Jones Industrial Average, and the Nasdaq Composite Index have hit their highest levels since June. As an owner of several technology companies (granted, very, very, very small ownership stake), its great to see the American Indexes, led by technology companies, have a sustained upward march, but the question is whether a bottom has been established or is this just a bear rally (which sputters out and resumes the downward momentum).

On the other side of the Atlantic, the European Central Bank followed the path set by the US and Canada and finally raised interest rates. The 0.5% raise was the first interest rate hike in 11 years.

Finally, as a tech heavy investor, next week will be a big week as the big US tech companies report their quarterly earnings. If the big players can at least meet analysts’ expectations, and the Fed delivers a 0.75% interest rate hike as expected, it should be a good week in the stock markets of North America (but, I’ve been wrong before 😊). In the meantime, let’s look at the week ended July 22……

Weekly Market Review

Monday: The markets got off to a mixed start this week with Canada’s Toronto Stock Exchange Composite Index (TSX) ending the day higher, while all three American Indexes – the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – ended the day slightly lower.

The TSX was pulled higher by a rise in commodity prices that boosted the Basic Material (natural resources) and Energy (oil) sectors. Canadian analysts and investors have their eyes focused on this week’s upcoming consumer price data which is anticipated to indicate inflation is above 8%, a 40-year high.

In the US, all three Indexes spent the morning in positive territory but then fell in late afternoon trading with nine of the eleven S&P sectors falling back into negative territory.

Tuesday: You know it is a good day in the market when the worst performing Index was up almost 2%. And so it was, with the Nasdaq leading the way and the TSX bringing up the rear at 2%. On the TSX, investors seem to have digested last week’s surprise interest rate hike by the Bank of Canada as the Financial sector rebounded from last week’s drop. The Canadian Utilities sector was the only sector not to post a gain for the day.

In the US, earnings are coming in higher than the analysts’ lowered expectations, causing the three American Indexes to have a nice little rally. However, the fact remains earnings estimates are still being adjusted downward and inflation remains high. Next week the US Federal Reserve (Fed) will announce their latest interest rate hike and send signals of future hikes.

Wednesday: Not as good a day as yesterday for the four Indexes, but a good day none the less as all four inched higher. North of the border, the rate of inflation rose to 8.1% for June, up from 7.7% in May. As high as that was, the Canadian market was expecting an even higher number so the report eased fears of another aggressive hike by the Bank of Canada (BoC) later this year. Depending how the rest of the summer plays out, I expect a hike somewhere between 0.5% and 0.75%.

With inflation coming in lower than expected and chances of a smaller interest rate hike on the horizon, the Canadian technology sector had a great day jumping up over 5%. The Healthcare and Consumer Cyclical sectors also rose by over 1%.

In the US, many of the big, high growth companies that are part of the Nasdaq had a good day, helping the Nasdaq lead the way upward as all three American Indexes ended the day in the black. Continued strong earnings was the big catalyst with the main benefactors being the Technology and Consumer Discretionary sectors.

Thursday: Yet another good day to be invested as all four Indexes ended higher, not much but at least its in the right direction. In Canada, the TSX was lifted by gains in the Technology and Industrials sectors that more than offset a decline in the Energy sector.

In the US, continued strong earnings reports led to a late rally, particularly in the big technology growth stocks (including Amazon (NASD:AMZN), Apple (NASD:AAPL) and Tesla (NASD:TSLA)), which helped boost the three American Indexes into the black.

Friday: All good things must come to an end and so it was for all four Indexes as they all ended the day in the red. In Canada, only the defensive sectors (Utilities, Telecommunications, and non-cyclical goods) were able to pull out a minor gain today.

In the US, the string of strong earnings which had propelled the three American Indexes higher this past week lost momentum as lower earnings from social media and ad technology companies failed to impress investors. The lower earnings, in combination with investors preparing for next week’s interest rate hike announcement by the Fed, led to the three Indexes losing ground. Only the S&P defensive sectors (Utilities, and Communications) were able to make it into positive territory.

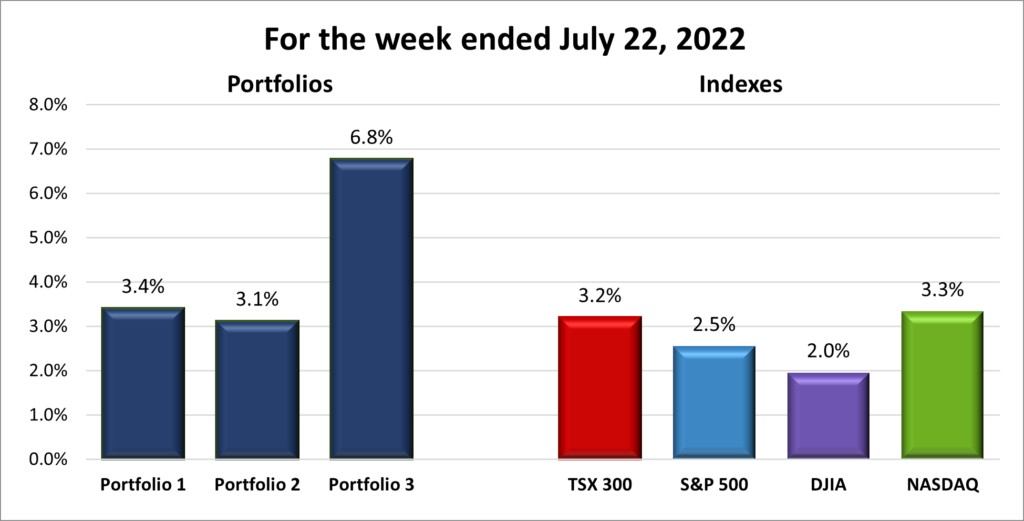

For the week, the TSX grew 3.2%, the S&P gained 2.56%, the DJIA climbed 1.96%, and the Nasdaq rose 3.33%.

Weekly Portfolio Review

Another good week in the North American stock markets as all four Indexes ended at least 2% higher. With the technology sector in the US having another good week I was surprised to see the TSX finish the week as the second-best performing Index, 0.1% behind frontrunner Nasdaq. This week’s rally in the Canadian Technology sector, combined with continued strength in Energy (oil), and Basic Materials (natural resources), must be what gave the TSX that extra boost this past week.

With the Nasdaq turning in another good week, that usually means the Portfolios will be in the black for the week. And they were. Portfolio 3 had an outstanding 6.8% gain, followed by Portfolio 1 with a 3.4% gain. Portfolio 2 was barely edged out of the top three by the Nasdaq but still managed an impressive 3.1%. Another good week for all three Portfolios but it will take considerably more weeks like this to get back to where they were at the start of the year. I’m keeping my fingers crossed. 😊

Companies on the Radar

Amazon and Ferrari (NYSE:RACE) continue as the only companies on my Radar. However, I may have blown my opportunity with Amazon. Instead of buying it when it was under US$ 105, I thought it would drop further and wanted to get it below US$ 100. Not my best decision as it closed this week at US$ 122.42. ☹ Note to self: don’t get greedy and try to time the market.

The jury is still out on Ferrari. The heart is willing, but the brain is not convinced. 😊

I still need to run both companies through my Multibagger Analysis.

- Amazon: scored a 6 out of 13 on my Radar Check test.

Figure : Radar Check of Amazon

- Ferrari: scored a 9 out of 13 on my Radar Check test.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended July 22, 2022: UP ![]()

- Disney (NYSE:DIS) announced that it chose The Trade Desk (NASD:TTD) as its advertising partner. The Trade Desk will be its primary demand-side platform connecting advertisers and agencies with Disney’s ad inventory properties: Disney+, Hulu, ABC, and ESPN.

- Apple joined the trend of companies that are slowing their hiring pace and reducing their spending growth rate next year in the event of an economic downturn, or worse, a recession, hits the world’s largest economy. The slowdowns will be targeted rather than across the board.

- Alphabet’s (NASD:GOOGL) Google is going to trial in the United Kingdom over allegations that the company abused its position to charge up to a 30% commission for games sold through its Google Play app store.

Alphabet executed a 20-for-1 split on July 18. My piece of the pie did not change percentage wise, but I hope the lower share price entices more investors to buy Alphabet shares and push the price higher. 😊

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

- Algonquin Power & Utilities Corp (TSX:AQN) DRIP

- BCE Inc (TSX:BCE) DRIP

- Brookfield Select Opportunities Income Fund (TSX:BSO.UN) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

Tesla, Inc.

All currency listed in millions of US dollars

Selected highlights from their second quarter 2022 financial results on July 20, 2022

- Total revenues of $16,934, up 42% year over year.

- Net income attributable to common stockholders $2,259.

- Operating income improved YoY to $2.5B in Q2, resulting in a 14.6% operating margin.

- Free cash flow of $621.

- Produced over 258,000 vehicles and delivered over 254,000 vehicles, despite ongoing supply chain challenges and factory shutdowns beyond Tesla’s control.

- Solar deployments increased by 25% YoY in Q2 to 106 MW, the strongest quarterly result in over four years

- Energy storage deployments decreased by 11% YoY in Q2 to 1.1 GWh.

Portfolio 2

Portfolio 2 for the week ended July 23, 2022: UP ![]()

Nothing particularly newsworthy for the companies in Portfolio 2 this past week. I am quite happy for these companies to quietly go about their business, increase their earnings and grow the value of the Portfolio 2 by 3% every week. 😊

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

- Alimentation Couche-Tard Inc (TSX:ATD)

- Dream Industrial Real Estate Investment Trust (TSX:DIR.UN) DRIP

- Brookfield Select Opportunities Income Fund (TSX:BSO.UN) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended July 23, 2022: UP ![]()

- Shopify (TSX:SHOP) announced a partnership with Alphabet’s YouTube to allow Shopify creators and merchants to sell their products across YouTube’s various channels. The partnership builds on Shopify’s existing relationship with Google and will allow their merchants to integrate their online stores with YouTube, which reaches over two billion monthly users. For YouTube viewers, they will be able to make a purchase from a Shopify merchant directly from within YouTube. For Shopify’s merchants, they will be able to sell their products through live streams, videos, as well as a store tab.

I believe this is a good deal for both companies and will help Shopify counter the post-pandemic slowdown in online shopping. Hopefully, the market also views this deal positively for both companies and their respective share prices return to the levels seen in the summer of 2021. That would make me very happy. Very happy indeed! 😊

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

- Brookfield Select Opportunities Income Fund (TSX:BSO.UN) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.