Electric Vehicle sales reach tipping point

Electric Vehicles (EV) surpassed the magical 5% mark of the total auto market this past quarter, according to a report from Cox Automotive. Why is 5% important you ask? Well, I will tell you. Historically, once a product reaches 5% of a total market it reaches the tipping point where it goes from niche product to mainstream product. As a result, sales increase rapidly as EVs go from being a novelty to commonplace. Based on my experience, a few years ago there was no EVs on our block. Now there are four EVs across twelve houses (2 Tesla (NASD:TSLA and 2 Hyundai (OTC:HYMTF).

Before you go and invest in EV companies (there are many to choose from), keep in mind that there are two big challenges still facing the EV industry. First, the average cost of an EV is US$ 20,000 more than then average price for new gasoline-based cars. Second, a lack of lack of charging stations, especially outside urban areas.

As productivity and competition increase in the EV market, the first challenge should disappear or at least become less of an issue. The second hurdle is why so many EV companies are planning to build out their own charging networks. Tesla already has a network of Tesla only charging stations, and GM (NYSE:GM) recently announced plans to increase the number of fast charging stations in the US by 20% by 2025. Rivian (NASD:RIVN) also has plans to build out fast charging stations and I imagine other EV, energy, and battery companies have their own plans in the works.

This sounds like a repeat of the build out of gas stations in the early 20th century (that makes it sound so long ago but it was well before my time). It will be interesting to see how the whole EV sector plays out and what comes first: abundant charging stations throughout North America, and globally, to increase sales of EVs, or a critical mass of EVs to entice existing service stations and other companies make fast charger stations as ubiquitous as gas stations. We shall see.

In the meantime, lets take a look at the past and see what happened this past week.

Weekly Market Review

Monday: The excitement of last week ended with a thud today as all four major North American markets – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – ended lower. In Canada, the main catalyst for the drop in the TSX was a downdraft in the commodity prices for natural resources (precious and base metals) and oil, the Basic Materials and Energy sectors, respectively.

In the US, the market drifted lower ahead of the release of key inflation related information (consumer prices, retail sales and factory output). The main culprits for the slide were the top growth stocks which pulled all three American Indexes lower. It appears Investors are being cautious ahead of the next meeting of the US Federal Reserve (Fed) in late July. In the event the interest rate hike is 0.75% rather than 0.5%, they would rather be sitting on cash than stocks.

Tuesday: last week’s rally is emphatically in the rear-view mirror as all four Indexes ended lower again. The TSX fell as the price of oil fell, sending Energy companies lower. Anticipation of a 0.75% interest hike by the Bank of Canada (BoC) Wednesday also put a damper on the TSX. It will be interesting to see how the TSX reacts to tomorrow’s announcement.

In the US, the main downforce was fears of a recession as the US Federal Reserve (Fed) attempts to reign in high inflation. The US Consumer Price Index (CPI) report for June will be announced Wednesday. It is hoped the “core CPI” (strip out the volatile food and gas prices) indicates inflation has peaked and its possible the Fed will increase interest rates by only 0.5%. On the other hand, if the CPI and “core CPI” are near 9% or higher, the Fed is most likely to raise the interest rate by 0.75% that they have signalled for the last two months. If the Fed is too aggressive with their interest rate hikes, it could tip the world’s largest economy into a recession which will most likely negatively impact the Canadian economy. Let us hope, the “core CPI” numbers are low, allowing the Fed to limit their hike to 0.5%.

Wednesday: Wednesday got off to the wrong kind of bang with the BoC surprising everyone and raising interest rates by 1%. In the US, the news was just as bad as the CPI came in higher than expected at 9.1%. Since the markets do not like bad news surprises, all four Indexes ended the day lower, although they recovered a bit late in the afternoon.

In Canada, the TSX had its fourth day of losses bringing it to its lowest level since March 2021. South of the border, the Indexes dove early and then slowly recovered as investors digested the news. The inflation rate of 9.1% was the highest since November 1981. If food and energy prices are removed from the CPI report, the core CPI actually fell slightly from 6% in May to 5.9% in June.

Thursday: All three American Indexes fell sharply to start the day and then clawed back to where they started. The Technology sector was the best performer of the eleven S&P sectors, pushing the Nasdaq into positive territory. Meanwhile, the S&P and DJIA ended the day slightly lower.

In Canada, the TSX dropped sharply and stayed down for the rest of today’s session. Falling oil prices, weaker metal prices and the higher interest rates announced Wednesday pushed the TSX down to a 16-month low.

Friday: The week ended on a positive note with all four Indexes ending the day higher, but not enough to save the week from ending lower. In Canada, higher oil prices lifted the Canadian Energy sector which in turn pulled the TSX higher.

In America, it was a broad-based rally with the S&P and DJIA each ending 5 day losing streaks, and the Nasdaq getting back in the winning column. Strong earnings by US banks, strong economic data and comments from the Fed indicating the upcoming rate hike will most likely be 0.75% rather than a full one percent, eased fears of a larger interest rate hike later this month.

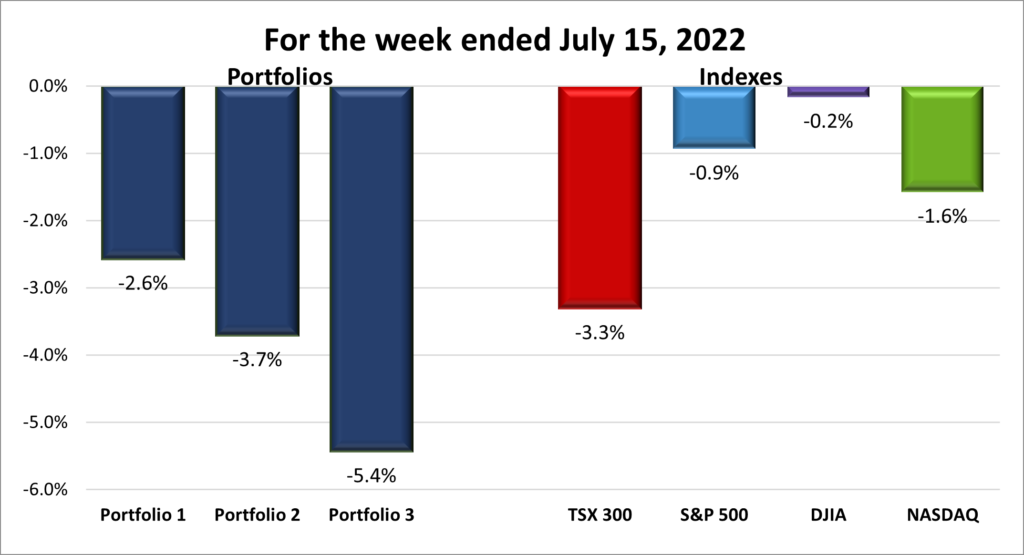

For the week, the TSX plunged 3.3%, the S&P dropped 0.93%, the DJIA slipped 0.16%, and the Nasdaq dropped 1.57%.

Weekly Portfolio Review

The higher-than-expected interest rate hike in Canada, combined with a high US CPI report for June essentially guaranteed the markets, Indexes and Portfolios would end the week lower than they started. The TSX fell the hardest of the four Indexes as a drop in commodity prices (natural resources and energy) weighed the Index down further. Of the US Indexes, the DJIA faired the best, slumping only 0.2% thanks to its focus on 30 of the biggest blue chip American companies which are much less volatile than growth stocks that inhabit the Nasdaq and the S&P.

After last weeks performance (each Portfolio up over 4%), this week was a downer, literally and figuratively. The Portfolios almost managed a clean sweep of the bottom three positions, saved by Portfolio 1 outperforming the TSX. I am a bit surprised the more balanced Portfolio 2 was not the best performer as it is the least volatile of the three Portfolios. In any event, when all the Indexes and Portfolios are down on the week, I prefer the Portfolios to not drop as far as the Indexes so I can say “at least I didn’t do as bad as the Indexes.” I realize lower is lower but psychologically I feel slightly better with the thought I did ‘better’ than the Indexes. 😊 Here is hoping the markets get back on the winning track next week and take the Portfolios with them.

Companies on the Radar

Amazon (NASD:AMZN) and Ferrari (NYSE:RACE) remain the only companies on my Radar. I like Amazon because it is a leader in several growth areas, and I see it going higher once this bear market ends. As for Ferrari, this is more of a heart over brain decision so I must think this one through in the event there is a red flag that would make me pass. In a sense I am doing what you should not do and waiting for the bear market to cause the share prices to drop further (trying to time the market). Hopefully, this will not blow up in my face. I hope to run them through my Multibagger Analysis this week.

- Amazon: scored a 6 out of 13 on my Radar test.

Figure : Radar Check of Amazon

- Ferrari: scored a 9 out of 13 on my Radar List test.

Figure : Radar Check of Ferrari

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended July 15, 2022: DOWN ![]()

- Thanks to the Rogers Communications (TSX:RCI.B) network outage on July 8, the merger with Shaw Communication (TSX:SJR.B) may be in jeopardy. The outage disrupted numerous services including banking services and 911 emergency calls. The Canadian government will likely take a much closer look at the deal that would reduce an already small number of national cellular providers in Canada. That was Rogers second nationwide outage in the last 15 months. So much for Rogers’ claim to be Canada’s most reliable network. 😊

- As part of the fallout of the Rogers network outage, the Canadian government has demanded three main national telecommunications providers – Rogers, BCE (TSX:BCEv), and Telus (TSX:T) – produce a plan to keep customers better informed in the event of future network outages.

- Rivian announced plans to let go up 5% of its workforce. I think the most likely areas to feel the brunt of the layoffs are in the non-manufacturing since Rivian cannot afford slippage in production of their electric vehicles.

- Unity Software (NYSE:U) announced it’s acquiring ironSource (NYSE: IS) in an all-stock deal, worth $4.4 billion. ironSource is a platform that allows mobile game developers to scale their games, and provide mobile app advertising to monetize their games, similar to Unity’s Operate solutions. At the same time, Unity’s board of directors approved a stock buyback program of $2.5 billion, which will likely help reduce the dilution from this new acquisition.

This sounds like they have given themselves a loan (use shares to acquire ironSource) that they can payback overtime (repurchase shares). Every investors’ piece of the pie is diluted when more shares are issued (not shareholder friendly), while share buybacks increase investors share of the pie (shareholder friendly). The market did not like this deal and punished them with a sharp 17% drop in share price on July 13. That being said, ironSource has recorded net income since 2019, which should improve Unity’s path to profitability. - Rivian is expected to unveil the Amazon custom electric delivery vehicle (EDV) on July 21. This is a significant milestone for both companies. For Rivian, it is the start of fulfilling an order for 100,000 EDV to Amazon. For Amazon, its a key step on the road (pardon the pun) to reach their carbon net-zero goal.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Automotive Properties Real Estate Investment Trust (TSX:APR.UN)

Andlauer Healthcare Group Inc (TSX:AND)

US $

BSR Real Estate Investment Trust (TSX:HOM.U)

Innovative Industrial Properties Inc (NYSE:IIPR)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended July 15, 2022: DOWN ![]()

- Disney (NYSE:DIS) announced plans to raise the monthly subscription fee for its ESPN+ streaming service by US$ 3 per month to US$ 9.99 per month. However, if you get ESPN+ as part of a bundle of Disney streaming service such as Disney+ and Hulu, there will be no price increase for the bundle. Sounds like a ploy to get ESPN+ subscribers to upgrade to a bigger Disney package. No doubt the Disney package will be more than the new ESPN+ price. 😊

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Summit Industrial Income REIT (TSX:SMU.UN)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended July 15, 2022: DOWN ![]()

- Microsoft (NASD:MSFT) announced they will partner with Netflix (NASD:NFLX) on Netflix’s upcoming ad-supported subscription offering. Microsoft will supply the technology and help grow sales of this new service.

- Brookfield Infrastructure Partners LP (TSX:BIP.UN) is partnering with U.S.-based investor DigitalBridge, to buy a majority interest in Deutsche Telekom’s cellphone-tower assets in Germany and Austria. This partnership will add another revenue producing asset to Brookfield.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Alvopetro Energy Ltd (TSXV:ALV)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.