What’s BRICS, and Why Is It Back in the Headlines?

I first heard the term BRIC – referring to Brazil, Russia, India, and China – back in the late 1990s when I was researching high-growth mutual funds. The pitch was that these were fast-growing economies, and investing in a BRIC-focused fund would add a boost to a long-term portfolio. I ended up passing on the fund… and promptly forgot about BRIC.

Fast forward to today, and the term is back in the spotlight – this time with an “S” on the end, as South Africa officially joined the group in 2010. With BRICS now grabbing headlines again, I thought it was a good time to revisit what the group is and why it’s suddenly become a target of President Trump’s latest trade threats.

The term BRICS refers to a group of five major emerging economies—Brazil, Russia, India, China, and South Africa—that have been working together since the late 2000s to increase their global economic and political influence. These countries share fast-growing markets, large populations, and a desire to reshape global institutions traditionally led by the US and its allies.

In 2023, the BRICS group announced plans to expand, inviting six new countries to join:

Egypt, Ethiopia, Iran, Saudi Arabia, the United Arab Emirates (UAE), and Argentina (though Argentina later declined after a change in government). The expansion signalled a push to build a broader coalition of countries exploring alternatives to the US-led global financial system – including reducing reliance on the US dollar and deepening trade ties within the group.

So why are BRICS back in the headlines?

President Trump recently threatened to impose an additional 10% tariff on goods from any country that aligns itself with BRICS. It’s part of his broader trade strategy aimed at reasserting US dominance and discouraging countries from joining or supporting global blocs seen as rivals to American influence. By using tariffs as a stick, Trump is trying to pressure potential BRICS partners and frame the group as a geopolitical threat.

For investors, this adds yet another layer of trade uncertainty, especially since BRICS includes major American trading partners like China and India, and fast-growing economies like Saudi Arabia and the UAE. As we’ve seen in past trade disputes, tariff threats can rattle markets, disrupt supply chains, and put pressure on everything from stock prices to commodity costs.

With that global backdrop in mind, let’s take a look at how the Canadian and American markets performed this past week and what drove the markets.

Items that may only interest or educate me ….

Nvidia #1, Liberation Day, 50% Tariff on Brazil, Canadian Economic news, US Economic news, .…

Nvidia Becomes World’s Most Valuable Public Company

This past week, artificial intelligence (AI) powerhouse Nvidia (NASD: NVDA) became the first publicly traded company to surpass a US$4 trillion market cap – making it the most valuable public company in the world. As of July 11, Nvidia’s share price is up around 22% year-to-date, and that’s even after a sharp drop in early April. Not bad for six months. 😊

To put that in perspective, Nvidia is now worth more than the entire Canadian economy.

What Is Liberation Day? A Key Moment in Trump’s Trade Agenda

“Liberation Day” refers to April 2, 2025, when President Trump announced sweeping new tariffs on all US trading partners – calling it a move to “liberate” American industry from what he described as unfair global trade practices. The name quickly stuck (at least in headlines), and the day became shorthand for a major escalation in US trade policy.

Just a week later, on April 9, following a sharp market sell-off, the US administration hit pause. It announced a 90-day delay on most of the new tariffs (while keeping a 10% baseline in place), saying the pause would allow time for countries to negotiate new bilateral deals with the US. The move calmed markets temporarily, but it also added a layer of uncertainty. Would the full tariffs still take effect? Would some countries get exemptions? Investors were left guessing.

Then, just before the pause was set to expire on July 9, Trump extended the deadline to August 1 and began rolling out country-specific tariffs—including 25% tariffs on Japan and South Korea. These were part of his “reciprocal” tariff approach, targeting countries the administration views as having unfair trade imbalances with the US. The higher rates likely serve as negotiating pressure, while the extension may have been designed to give a few pending deals more time to close.

For markets, this kind of unpredictability matters. Tariffs raise costs for businesses and disrupt global supply chains, while sudden shifts – like a sweeping announcement, followed by a pause, then a delay – rattle investor confidence and fuel volatility. It’s a reminder that policy risk is real, and when trade signals get murky, markets take notice.

Trump Slaps 50% Tariff on Brazil—But This One’s Personal

Trade tensions flared up again this past week as President Trump announced a 50% tariff on all Brazilian imports, set to begin on August 1. The hefty tariff was in response to Brazil’s ongoing trial of former president Jair Bolsonaro – who Trump called “a patriot.” He framed the move as retaliation against what he described as a political witch hunt, making this one of the most politically charged trade actions in recent history.

This isn’t just another tariff – it’s unprecedented. While past American tariffs have usually focused on trade deficits or national security concerns, this one is aimed directly at a foreign country’s legal system. It’s the steepest tariff Trump has announced so far in 2025, and it’s not tied to any specific industry – it covers all goods coming from Brazil.

For investors, this adds a new layer of unpredictability to global trade. Brazil is a major exporter of everything from coffee and orange juice to steel and aircraft, and a 50% tariff could mean higher prices on everyday items and more volatility in commodity and emerging markets. For those who rely on a morning cup of coffee to kickstart their day, that daily habit could soon cost a bit more. The Brazilian real dropped sharply on the news, and Brazilian exporters like Embraer and Petrobras took an immediate hit.

With tariffs now being used as tools of political pressure, the line between trade and diplomacy is getting blurry – and that could mean more market swings ahead.

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Labour Force Survey (LFS)

Canada’s economy added 83,100 jobs in June – its first net gain since January and a big upside surprise compared to expectations for a 3,000-job decline (and May’s modest 8,800 increase). That strength helped pull the unemployment rate down to 6.9%, better than the expected 7.1% and reversing a recent upward trend.

One yellow flag: most of the new jobs were part-time, accounting for about 84% of the total, which may temper some of the optimism.

Wage growth also cooled slightly. Average hourly wages for permanent employees rose 3.2% year-over-year, down from 3.4% in May, while the average hourly wage slipped to C$36.01 from C$36.14.

The strong hiring numbers, especially alongside slowing population growth, point to a more resilient economy than many had expected, raising the odds of stronger-than-expected second quarter economic growth. However, this labour market strength, combined with ongoing trade uncertainty, has dimmed hopes for a BoC rate cut in July. Analysts now see September as the earliest possibility, depending on the next inflation report.

Canadian Market Volatility

Canada’s volatility barometer, the S&P/TSX 60 Volatility Index (VIXC), opened the week at 10.31 and briefly spiked to 10.71 in early trading. But it quickly dropped below 9.0 after the US extended its tariff deadline to August 1, easing some market tension. The VIXC fell as low as 7.16 before bouncing back above 8.7 following President Trump’s threat of a 35% tariff on all Canadian goods not covered by the CUSMA trade agreement. It ended the week at 9.21 – suggesting that while investors remain cautious, many are taking Trump’s latest threat with a grain of salt.

Aside from the risk around potential 50% tariffs on copper, investors mostly remained optimistic that a Canada – US trade deal could come together in the coming weeks.

If you’re new to the VIXC, think of it as Canada’s version of a fear gauge. A reading below 10 suggests investors are feeling pretty calm. Between 10 and 20 signals a steady, business-as-usual market. But once it climbs above 20, that’s when nerves show up and volatility starts to pick up.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Federal Open Market Committee minutes

The Fed released minutes this past week from its June 17–18 Federal Open Market Committee (FOMC) meeting, offering a glimpse into how members were thinking about interest rates and the economy. As expected, they left the benchmark rate unchanged at 4.25%–4.50%, sticking with a wait-and-see approach as they navigate mixed economic signals.

Inflation is still heading in the right direction (down), but only gradually. Fed officials described it as “somewhat elevated,” especially with the risk that new tariffs could push prices higher. The labour market is still strong overall, though there are early signs of softening.

What stood out in the minutes was a clear divide: seven officials don’t expect any rate cuts this year, while a few are open to easing – possibly as soon as September. But that’s far from guaranteed. The Fed made it clear they want more convincing evidence that inflation is cooling sustainably and that tariff-driven price pressures aren’t making a comeback.

Investors had been hoping for a July rate cut, but a strong labour report the previous week, coupled with lower weekly jobless numbers, pushed those hopes back to September at the earliest. Even that will depend on how upcoming data – like inflation, jobs, and trade – shape up.

Bottom line: the Fed is in no rush. And with tariffs now in the mix, the path to lower rates just got a little more complicated.

American Market Volatility

Wall Street’s “fear gauge,” the CBOE Volatility Index (VIX), started the week on relatively calm footing, opening at 17.47 and continuing the downward drift from the previous week. It briefly climbed to 18.50 on Monday after the US announced 25% tariffs on key trading partners Japan and South Korea, but then eased steadily lower, falling as far as 15.7. Late in the week, President Trump’s threat of 35% tariffs on Canadian imports sent the VIX back above 17, before it ultimately settled at 16.40 – still within the “normal” range, but a clear reminder that markets are still on edge as Trump continues to shake up the global trade landscape.

If you’re new to the VIX, think of it as a real-time pulse check on investor nerves. It tends to rise when markets get jittery – whether it’s due to geopolitical tensions, inflation surprises, or uncertainty around interest rates. When investors start pulling back from higher-risk stocks like tech, price swings get bumpier, and that’s when the VIX starts to climb.

A VIX reading between 12 and 20 generally signals a steady, normal market. But once it climbs above 20, it means investors are starting to brace for more volatility. The higher it goes, the more market turbulence is being priced in.

Weekly Market and Portfolio Review

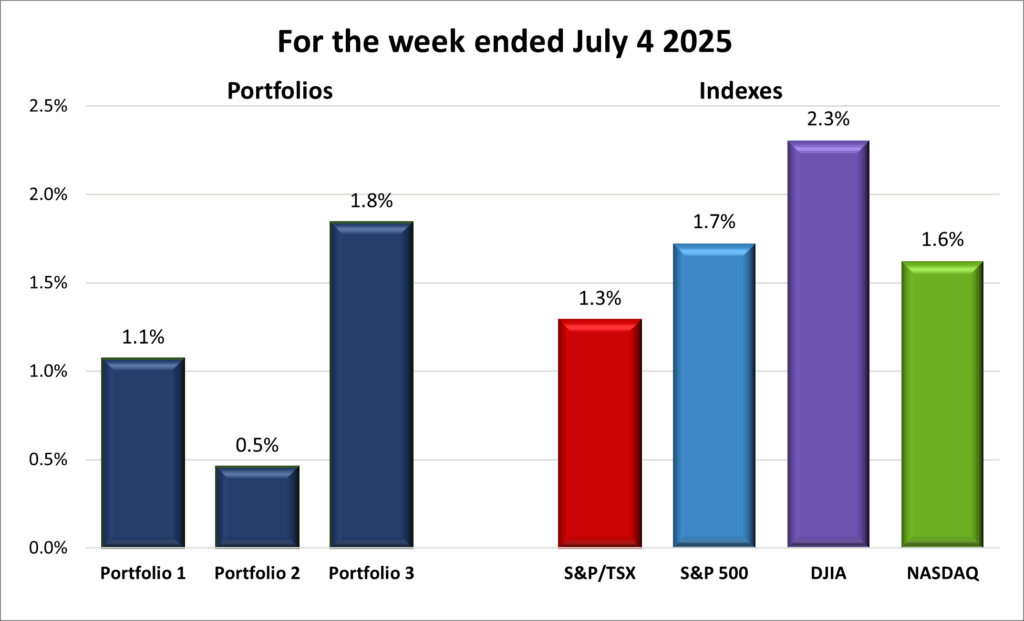

For the week, the TSX (SPTSX) was essentially flat, down 0.05%, the S&P 500 (SPX) lost 0.3%, the DJIA (INDU) fell 1.0% while the Nasdaq (CCMP) declined 0.1%.

| Index | Weekly Streak |

| TSX: | 1 – week losing streak |

| S&P: | 1 – week losing streak |

| DJIA: | 1 – week losing streak |

| Nasdaq: | 1 – week losing streak |

![]() The week began with the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), and the Nasdaq Composite Index (Nasdaq) all at record highs, with the Dow Jones Industrial Average (DJIA) not far behind. But markets stumbled early as President Trump reignited global trade tensions, injecting fresh uncertainty. Sentiment improved midweek, with the TSX, S&P and Nasdaq all hitting record highs, and all four indexes looked on track for another weekly gain – until a late-week barrage of new tariff threats halted the rally. By Friday’s close, all four had slipped into the red, as shown in the weekly progress chart above.

The week began with the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), and the Nasdaq Composite Index (Nasdaq) all at record highs, with the Dow Jones Industrial Average (DJIA) not far behind. But markets stumbled early as President Trump reignited global trade tensions, injecting fresh uncertainty. Sentiment improved midweek, with the TSX, S&P and Nasdaq all hitting record highs, and all four indexes looked on track for another weekly gain – until a late-week barrage of new tariff threats halted the rally. By Friday’s close, all four had slipped into the red, as shown in the weekly progress chart above.

Trade concerns dominated the early part of the week. Trump announced 25% tariffs on imports from Japan and South Korea, plus 25%–40% tariffs on several other trading partners. He also floated an extra 10% levy on countries aligning with BRICS (Brazil, Russia, India, China, and South Africa). While the original July 9 deadline was pushed to August 1, offering temporary relief, it still left investors on edge. At week’s end, Trump escalated things further, threatening a 35% tariff on Canadian goods not covered by the CUSMA trade agreement and suggesting 15%–20% tariffs on all other US trading partners, up from the current 10% baseline.

He also added a 50% tariff on copper to the growing list of sector-specific levies, which already includes steel, aluminum, and auto parts. Pharmaceuticals could face tariffs of up to 200%, with semiconductors and other sectors still under investigation by the US Department of Commerce.

In a highly unusual move, Trump slapped a sweeping 50% tariff on all Brazilian imports, citing the trial of former president Jair Bolsonaro. It marked the first time a politically motivated, broad-based tariff has been imposed on a major US trade partner.

This steady stream of shifting deadlines, surprise announcements, and walk-backs has left investors on edge. Still, after Trump extended the deadline “one last time” and insisted there would be no further delays, markets regained some footing midweek. Many investors appear increasingly skeptical of Trump’s threats, having seen similar rhetoric softened in the past.

On the upside, markets got a lift from the long-awaited passage of Trump’s tax and spending bill, which includes several business-friendly provisions. A key campaign promise, its approval helped clear a major cloud of policy uncertainty.

Stronger-than-expected labour data also helped steady nerves. A robust June jobs report, coupled with another drop in weekly jobless claims, pointed to a labour market holding up well despite trade tensions.

Meanwhile, the Fed’s June meeting minutes revealed a split among policymakers. Some are now open to at least one rate cut this year, with several officials calling the inflationary effects of tariffs “temporary or modest.” Still, after two strong labour reports, a July cut now looks unlikely – pushing expectations to September at the earliest.

In Canada, looming American tariffs on key exports – like steel, aluminum, autos, and copper – pushed Ottawa to accelerate trade talks with other countries. The federal government is working to finalize a deal with the 10-member Association of Southeast Asian Nations bloc to reduce reliance on US trade. That pivot to new markets is both a defensive strategy and a long-term opportunity. That proactive tone helped lift investor sentiment and sent the TSX to a record high, before it pulled back following Trump’s latest threat.

Underscoring the urgency, Trump warned of a 35% tariff on all Canadian goods not made in the US, adding that any retaliation would be met with even higher tariffs. A move like that would hurt Canadian jobs – and Ottawa has made clear it’s ready to respond if talks break down.

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week losing streak |

| Portfolio 2: | 1 – week losing streak |

| Portfolio 3: | 1 – week losing streak` |

![]() After three straight weeks of gains, my portfolios hit a speed bump, snapping their winning streaks, with all three ending the week lower – as shown in the chart below. Given how the major indexes performed, the pullback wasn’t all that surprising.

After three straight weeks of gains, my portfolios hit a speed bump, snapping their winning streaks, with all three ending the week lower – as shown in the chart below. Given how the major indexes performed, the pullback wasn’t all that surprising.

One notable move this week was transferring some Nvidia shares from Portfolio 1 to Portfolio 3. That helped rebalance Nvidia’s weight in Portfolio 1 – though it’s still the largest holding – and made it the new heavyweight in Portfolio 3, more than doubling the size of Shopify’s (TSE: SHOP) position, now the second-largest.

Portfolio 1 led the pack in a tough week, slipping 0.4%. That loss wasn’t too bad, considering only 39% of its holdings finished in the green. Nvidia’s all-time high, along with a 14% jump from Kraken Robotics (TSEV: PNG), helped cushion the drop. Another bright spot was Celestica (TSE: CLS), which hit a new record high. On the downside, Datadog (NASD: DDOG) fell 14%.

Portfolio 2 lost 0.6%, with just 29% of its holdings posting gains. A solid week for its oil stocks helped limit the damage, and Microsoft (NASD: MSFT) reaching a record high certainly didn’t hurt.

Portfolio 3 was the weakest of the three, down 0.8%. With only 22% of its holdings moving higher, the newly added Nvidia shares definitely softened the blow. Aside from Nvidia, Microsoft’s record high was the only other real standout.

It’s always a bit frustrating to see red across the indexes after a few solid weeks of green, but that’s investing—some weeks just don’t cooperate. Thankfully, a few bright spots (thank you, Nvidia!) helped limit the downside. The Nvidia transfer also gave Portfolio 3 a stronger growth engine and helped rebalance things overall. With earnings season approaching and President Trump still capable of rattling markets, I’m hopeful some great opportunities will appear. 😊

Companies on the Radar

With the start of a new week, three new companies made it onto my radar:

With the start of a new week, three new companies made it onto my radar:

Mainstreet Equity Corp. (TSE: MEQ) is a Calgary-based real estate company focused on mid-market apartment buildings – typically under 100 units – across Western Canada. It acquires underperforming properties at below-market prices, renovates them, and increases rental income through improved operations. With strong demand for rental housing, a repeatable value-add strategy, and a solid balance sheet, Mainstreet offers a compelling mix of income and growth. Shares currently trade below net asset value, giving investors a margin of safety alongside steady cash flow and long-term upside.

Amer Sports (NYSE: AS) is a Finland-based sporting goods company that went public in February 2024. It owns premium global brands like Wilson, Salomon, Arc’teryx, Atomic, and Louisville Slugger, selling in over 100 countries. Revenue comes from both retail partners and a growing direct-to-consumer (DTC) segment through branded stores and online sales. With strong revenue growth, expanding DTC margins, and a valuation below peers, Amer offers an attractive mix of growth and value. As a consumer-focused company riding the health and outdoor trend, it’s definitely caught my eye.

Copart (NASD: CPRT) runs one of the world’s largest online vehicle auction platforms, specializing in salvage cars from accidents and natural disasters. It sells on behalf of insurers, dealerships, rental companies, and individuals. Copart earns revenue through transaction fees, storage, transportation, and listing services. Its digital model, global buyer network, and asset-light approach support strong margins and steady growth. With no long-term debt and rising tailwinds from vehicle values and insurance claims, it’s a steady growth story that’s earned a spot on my radar.

These three names join the four companies already on my radar last week: Aritzia, TerraVest, Secure Energy, and Novo Nordisk. Together, they span everything from real estate and retail to industrials, healthcare, and consumer goods – but they all share a few key traits: strong fundamentals, long-term demand drivers, and business models with long-term appeal. Here’s a quick recap of the four from the previous week:

- Aritzia (TSE: ATZ): a fashion retailer and design house known for its upscale in-house brands of women’s clothing and accessories. It controls everything from design to distribution and sells through more than 130 boutiques across North America, along with a fast-growing online platform. Its main markets are Canada and the US, where it continues to expand.

- TerraVest Industries (TSE: TVK): an industrial manufacturer serving the energy, agriculture, and transportation sectors across North America. Its products include propane tanks, ammonia storage vessels used in farming, natural gas transport vehicles, and various energy processing systems. It’s a solid operator in essential industries.

- Secure Energy Services (TSE: SES): an industrial company that focuses on environmental and waste management services for energy and industrial clients. It offers recycling, disposal, and infrastructure support across North America. For anyone interested in sustainability and infrastructure, this one’s worth keeping an eye on.

- Nordisk A/S (NYSE: NVO) Novo Nordisk is a global leader in diabetes and obesity care, thanks to products such as: Ozempic (for type 2 diabetes), Wegovy (for obesity), and Rybelsus (an oral version for diabetes). These products have pushed the company into the forefront of diabetes and medical weight loss solutions.

It’s a diverse group overall, but each company brings something compelling to the table – whether it’s steady income, breakout growth potential, or a strategic niche worth following.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated July 11, 2025.

Portfolio Updates

Portfolio 1

Transferred Out: Some Nvidia shares. Nvidia had grown to nearly 40% of Portfolio 1, so trimming it back has been on my to-do list for a while. At the same time, I was looking to add Nvidia to Portfolio 3. Instead of selling in one account and buying in the other – racking up two sets of transaction fees – I opted for a direct transfer. One move, two problems solved. 😊

And since the shares were held in a Tax-Free Savings Account (TFSA), there were no tax consequences on the transfer out of Portfolio 1.

Portfolio 3

Transferred In: Some Nvidia shares from Portfolio 1. These shares were originally in Portfolio 1’s TFSA, where gains are tax-free (hence the name “Tax-Free Savings Account” 😊). But to move them into Portfolio 3’s TFSA, they first had to pass through the regular cash account so the value at the time of entry into the TFSA could be recorded. That one-day stopover caused a small hiccup—Nvidia’s share price jumped a few bucks during the transfer window, triggering a capital gain. Since that gain happened in a taxable account, it’ll come with a small tax hit. ☹

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!