When Good News Is Bad News (and Vice Versa)

This week brought a steady stream of US labour market data, and you might’ve noticed something that feels a little backwards: sometimes good news about jobs or the economy makes stocks fall, while disappointing news sends markets higher. At first, this can be hard to wrap your head around. After all, if more people are working and businesses are hiring, that should be a positive sign, right? But markets don’t just react to the data itself – they react to what that data means for interest rates and the US Federal Reserve’s (Fed) next move.

This week’s lineup included the Job Openings and Labor Turnover Survey (JOLTS), the ADP Employment Report, and the Employment Situation Summary (ESS). On the surface, stronger numbers might look like a win for both the economy and the markets. But for us investors, it’s not just about how the economy is doing. It’s about how that strength could affect inflation and whether the Fed will keep interest rates higher for longer.

When the economy shows signs of strength – like the solid job gains in June’s ESS or stronger-than-expected wage growth – investors start to worry that the Fed might delay cutting rates to keep inflation under control. Higher rates make borrowing more expensive for both businesses and consumers, which can slow spending, reduce profit margins, and weigh on company earnings. So even though strong hiring suggests a healthy economy, the market may see it as a reason to be cautious.

On the other hand, when labour market data comes in softer than expected – such as the job losses in the ADP report or signs of easing wage growth – markets can actually rally. That’s because weaker data may suggest inflation is cooling, which increases the odds of a Fed rate cut. Lower interest rates are typically good for stocks, especially in sectors like technology and consumer discretionary, where companies benefit from cheaper borrowing and investors are more willing to take on risk.

This constant back-and-forth between economic strength and interest rate expectations is why you’ll often hear the phrase “good news is bad news” in financial headlines. It’s not that investors want people to lose jobs or see growth stall. It’s that markets are always trying to anticipate what comes next. For long-term investors, it’s a reminder that markets are driven as much by expectations as by current conditions. Reacting emotionally to every data release is rarely a winning strategy.

When I first started paying attention to what moved the markets, this kind of upside-down reaction felt confusing. But over time, it started to make more sense. The key is recognizing that the market isn’t always looking for the strongest data – it’s looking for the right balance: steady growth, falling inflation, and the potential for lower interest rates. That’s why this week’s labour reports have been under the microscope – not just for what they say about jobs, but for what they might hint about the Fed’s next move and where markets could be headed next.

With that context in mind, let’s take a look at how the markets responded to the latest labour data this past week and what it meant for the major indexes and my portfolios.

Items that may only interest or educate me ….

Markets Primed for a Strong July, Canadian Economic News, US Economic News, ….

Markets Primed for a Strong July

As we kick off July, it’s worth noting that this month has historically been one of the stronger ones for both American and Canadian markets.

In the US, July has typically been a strong performer. Over the past few decades, the S&P 500 (S&P) has averaged solid gains during the month, making it one of the top three for returns. More recently, over the past ten years, it’s delivered average returns of over 3%, second only to November. The Nasdaq Composite Index (Nasdaq), with its heavy tech weighting, also tends to do well, often lifted by positive momentum and investor optimism heading into second-quarter earnings season.

In Canada, the Toronto Stock Exchange Composite Index (TSX) shows a similar, though slightly more muted, seasonal trend. July has typically brought average gains of around 2%, with no significant summer slowdown. While not as flashy as US performance, it’s still a steady month for Canadian stocks.

Of course, seasonality is just one factor. This July, investors are keeping a close eye on trade developments – especially the July 9 deadline to complete US trade deals – as well as the upcoming wave of earnings reports. If markets can navigate those events without too much turbulence, history suggests July could offer some helpful tailwinds.

Past performance is never guaranteed, but July has earned its reputation as a strong seasonal month. And this year, the setup looks cautiously optimistic.

Canadian Economic News

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Canadian Market Volatility

Canada’s volatility barometer, the S&P/TSX 60 Volatility Index (VIXC), opened the week at 10.37. It dipped below 9.5 and mostly stayed between 8.5 and 10.5 during what turned out to be a fairly calm stretch for Canadian markets. The shortened trading week – split by the Canada Day holiday on Tuesday – wrapped up with the VIXC closing at 9.53.

If you’re new to the VIXC, think of it as Canada’s version of a fear gauge. When it dips below 10, it’s a sign that investors are feeling relaxed. A range between 10 and 20 signals a steady, business-as-usual market. And once it climbs above 20, that’s when nerves start showing and volatility really starts to pick up.

US Economic news

This past week’s key data points that the Fed considers when deciding whether to raise or lower the interest rate.

Labour data

The latest updates from the JOLTS, the ADP Employment Report, and the ESS offer a snapshot of the US labour market. Together, they tell a story of a labour market that’s still holding up, but not without signs of softening beneath the surface.

JOLTS

The JOLTS report from the Bureau of Labor Statistics showed that job openings rose to 7.8 million in May, up from April’s revised 7.4 million and well above forecasts for a drop to 7.3 million. That’s the highest reading since November 2024, with most of the increase coming from the Leisure and Hospitality sector.

While that sounds great, the report also pointed to a slowdown in hiring, suggesting that companies are growing more cautious about bringing on new staff amid ongoing economic uncertainty – especially with the July 9 tariff deadline looming. In short, demand for workers is still there, but business confidence is looking shaky.

For investors, this kind of “Goldilocks” data – strong job openings but not overheating – can be just what the markets like. It supports the idea of a soft landing, where inflation cools and growth slows without tipping the economy into recession. That’s good news for equities, particularly rate-sensitive sectors like tech and growth.

ADP Employment Report

In contrast, the ADP Employment Report painted a weaker picture. Private-sector jobs fell by 33,000 in June, marking the first decline since March 2023 and far below expectations for a 99,000 gain. May’s figure was also revised down to just a 29,000 increase.

This wasn’t a wave of layoffs, but rather a sign that employers are hesitant to hire or replace departing workers. Concerns about slowing growth, sticky inflation, and global risks like trade tensions are making businesses cautious. While not alarming on its own, this report adds to the sense that the labour market is gradually losing momentum – and that could push the Fed closer to a rate cut if future data tells a similar story.

ESS

Finally, the US Bureau of Labor Statistics’ ESS report for June showed the US economy added 147,000 jobs, beating expectations and slightly ahead of May’s revised 144,000. That marks four straight months of solid gains, reinforcing the idea that the labour market remains surprisingly resilient.

The unemployment rate dipped to 4.1%, defying forecasts for a third straight month at 4.2%. Wage growth cooled slightly, with average hourly earnings up 3.7% year-over-year, below the expected 3.9%. On a monthly basis, wages rose 0.2%, down from May’s 0.4%.

This is something of a sweet spot for the Fed: strong job creation but easing wage pressures. It helps reduce inflation risks but probably isn’t soft enough yet to justify a rate cut in July. Unless upcoming inflation data comes in much lower than expected, even a September cut is starting to look less likely.

Summary

Taken together, these three reports show a resilient but cooling labour market. There’s no sign of a sharp downturn, but the momentum is clearly slowing. For now, it’s a mixed bag – positive for growth, but not quite the kind of softness that would prompt the Fed to cut rates soon. For us investors, that means markets may continue to grind higher, but expectations for summer rate relief just took another hit.

American Market Volatility

Wall Street’s “fear gauge,” the CBOE Volatility Index (VIX), started the week on relatively calm footing, opening at 17.19 – quieter than we’ve seen in recent weeks. Easing geopolitical tensions, optimism around trade negotiations, and the lead-up to the July 4th long weekend all contributed to the more relaxed tone. The VIX hovered mostly between 16.25 and 17.25 through the shortened week before closing at 16.38 on Thursday, as investors packed it in early for the holiday.

For those new to the VIX, it’s often referred to as Wall Street’s stress meter. When investors grow uneasy about global issues – like ongoing conflicts in the Middle East – or domestic concerns such as inflation or rate hikes, they tend to step back from riskier assets like technology and other growth stocks. That pullback can lead to sharper price swings in the market, which is when the VIX tends to climb.

Readings between 12 and 20 typically signal that markets are behaving normally. But once it rises above 20, it suggests that investors are starting to brace for more volatility. The higher the number, the more market turbulence is being priced in.

Weekly Market and Portfolio Review

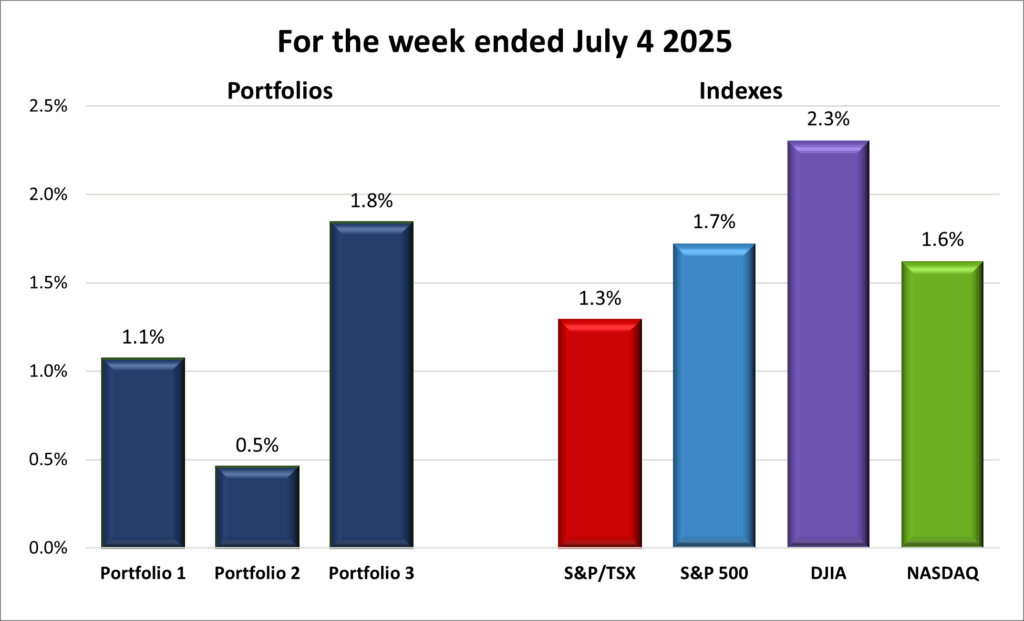

For the week, the TSX (SPTSX) rose 1.3%, the S&P 500 (SPX) advanced 1.7%, the DJIA (INDU) jumped 2.3% and the Nasdaq (CCMP) climbed 1.6%.

| Index | Weekly Streak |

| TSX: | 2 – week winning streak |

| S&P: | 2 – week winning streak |

| DJIA: | 3 – week winning streak |

| Nasdaq: | 3 – week winning streak |

![]() It may have been a holiday-shortened week, with Canada Day and Independence Day celebrations closing markets on both sides of the border, but that didn’t stop stocks from pushing higher. The S&P, the TSX, and the Nasdaq all set new record highs multiple times during the week. Even the Dow Jones Industrial Average (DJIA) came close, finishing just 0.6% below its all-time high.

It may have been a holiday-shortened week, with Canada Day and Independence Day celebrations closing markets on both sides of the border, but that didn’t stop stocks from pushing higher. The S&P, the TSX, and the Nasdaq all set new record highs multiple times during the week. Even the Dow Jones Industrial Average (DJIA) came close, finishing just 0.6% below its all-time high.

Once again, tariffs were front and centre – though this time with a more upbeat tone that helped fuel investor optimism. The week kicked off on solid footing after the US and China agreed to a trade framework, and Canada scrapped its planned digital services tax restarting Canada-US trade negotiations. Those two moves signalled progress in trade talks with two of America’s biggest partners and helped ease concerns about escalating tensions.

President Trump added to the optimism by confirming he wouldn’t extend the July 9 deadline for countries to strike trade deals with the US, removing a layer of uncertainty. Instead, the US is narrowing the scope of negotiations in hopes of wrapping up more agreements quickly. One such deal came through with Vietnam this week, lifting market sentiment and raising hopes that more countries could reach agreements before Tuesday’s deadline.

But in typical fashion, Trump later changed course. Toward the end of the week, he said he preferred applying simple tariff rates instead of pursuing complex individual negotiations. Starting as early as July 4, the US will begin notifying countries of standardized tariff levels – ranging from 10% to as high as 70% – marking a sharp departure from earlier deal-by-deal plans.

On the economic front, Trump’s massive tax and spending bill narrowly passed the Senate, needing a tiebreaker from Vice President Vance. The bill cleared Congress and was signed into law, and while markets didn’t react much, analysts warned that ballooning deficits could put pressure on the bond market and long-term borrowing costs.

Meanwhile, a flurry of US labour reports offered mixed signals. Job growth remains solid, wage growth is cooling, and there’s no sign of a sharp downturn. That’s good news for the economy, but not soft enough for a July rate cut. Elsewhere, in a speech overseas, Fed Chair Jerome Powell said the Fed remains cautious, pointing to trade uncertainty and the unknown effects of tariffs as reasons to hold off. With the benchmark rate still at 4.25% to 4.5%, the Fed wants to see whether inflation flares up again before making its next move.

In Canada, the economic outlook showed some challenges, with manufacturing output falling back to levels last seen in 2020, suggesting US tariffs are starting to take a toll. Still, the TSX managed to close at record highs each day during the shortened trading week. Investor optimism was lifted by the revival of US –Canada trade talks, sparked by Canada’s decision to cancel its digital services tax. This move, along with the US-Vietnam trade deal, raised hopes that more trade agreements could be completed before the July 9 deadline, easing uncertainty in the markets. Coupled with strong US labour data, investors felt more confident buying stocks and taking on a bit more risk, pushing the TSX to record highs.

So far, July is off to a strong start. Here’s hoping it keeps up for the rest of the month and beyond. 😊

| Portfolio | Weekly Streak |

| Portfolio 1: | 3 – week winning streak |

| Portfolio 2: | 3 – week winning streak |

| Portfolio 3: | 3 – week winning streak |

![]() To paraphrase The Kings’ classic “This Beat Goes On/Switchin’ to Glide,” the gains go on… and on… and on. 😊 It was another upbeat week for all three portfolios, each extending their weekly winning streak to three. While none managed to top the DJIA, the week’s top-performing index, Portfolio 3 did beat the other three major indexes, as shown in the performance chart below.

To paraphrase The Kings’ classic “This Beat Goes On/Switchin’ to Glide,” the gains go on… and on… and on. 😊 It was another upbeat week for all three portfolios, each extending their weekly winning streak to three. While none managed to top the DJIA, the week’s top-performing index, Portfolio 3 did beat the other three major indexes, as shown in the performance chart below.

Portfolio 1 climbed 1.1% for the week, with 79% of its holdings in the green. Standout performers included Pulse Seismic (TSE: PSD), which jumped 18%, Datadog (NASD: DDOG), on inclusion in the S&P index, and Magnite (NASD: MGNI), both up 17%, and Carnival Corp. (NYSE: CCL), which rose 13%. A few names also reached new all-time highs: Celestica (TSE: CLS), Magnite, and CrowdStrike (NASD: CRWD). And then there’s Nvidia (NASD: NVDA), which surged to a record high, pushing its market valuation to an eye-popping US$3.89 trillion – cementing its spot as the world’s most valuable company and the undisputed leader in AI chipmaking.

The only damper? Energy stocks – all of them finished lower, limiting the week’s gains.

Portfolio 2 was the slowest of the bunch but still nudged up 0.5%. There were no major moves in either direction, though iA Financial (TSE: IAG) did hit an all-time high. Like the other portfolios, energy holdings were a drag on the portfolio. However, this was the only portfolio where two energy stocks actually finished higher: South Bow Corp (TSE: SOBO) and Whitecap Resources (TSE: WCP) managed modest gains.

Portfolio 3 led the way with a 1.8% weekly gain, with 80% of its holdings ending in the green. Magnite 17% gain was partly offset by a 10% drop in Alvopetro Energy (TSEV: ALV). Still, the broad strength across the rest of the portfolio helped push it to the top spot among the three this week.

All in all, it was another solid week across the board. The portfolios seem to have found their groove, and with markets still moving to a positive beat, here’s hoping the gains go on… and on… and on as July rolls on. 😊

Companies on the Radar

With the holiday-shortened week, I didn’t have much time to scout for new investing ideas, so my radar list is holding steady. For now, my list is included of the same four companies from the previous week:

With the holiday-shortened week, I didn’t have much time to scout for new investing ideas, so my radar list is holding steady. For now, my list is included of the same four companies from the previous week:

- Aritzia (TSE: ATZ): a fashion retailer and design house known for its upscale in-house brands of women’s clothing and accessories. It controls everything from design to distribution and sells through more than 130 boutiques across North America, along with a fast-growing online platform. Its main markets are Canada and the US, where it continues to expand.

- TerraVest Industries (TSE: TVK): an industrial manufacturer serving the energy, agriculture, and transportation sectors across North America. Its products include propane tanks, ammonia storage vessels used in farming, natural gas transport vehicles, and various energy processing systems. It’s a solid operator in essential industries.

- Secure Energy Services (TSE: SES): an industrial company that focuses on environmental and waste management services for energy and industrial clients. It offers recycling, disposal, and infrastructure support across North America. For anyone interested in sustainability and infrastructure, this one’s worth keeping an eye on.

- Nordisk A/S (NYSE: NVO) Novo Nordisk is a global leader in diabetes and obesity care, thanks to products such as: Ozempic (for type 2 diabetes), Wegovy (for obesity), and Rybelsus (an oral version for diabetes). These products have pushed the company into the forefront of diabetes and medical weight loss solutions.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated July 4, 2025.

Portfolio Update

Portfolio 1

Sold: Nvidia After Nvidia’s incredible run over the past few years, I decided to trim a few shares this past week.

Nvidia has become one of the most valuable companies in the world, riding first the cloud computing/data centre wave and now the artificial intelligence (AI) boom. It’s been a huge winner in Portfolio 1. I still think it’s a great company with a long runway ahead, but its massive success has caused it to grow into an outsized position – at one point making up nearly 40% of the portfolio’s total value. As Nvidia went, so did the portfolio.

Trimming helps reduce my exposure to any one stock and brings my allocation back into balance. I also saw this as a good opportunity to lock in a bit of profit while the share price was at an all-time high. Even the strongest companies can face pullbacks, especially when expectations get ahead of earnings.

This wasn’t a big move – I’m still holding onto the majority of my shares. But after such a strong run, taking a few chips off the table felt like the right way to manage risk while staying invested in a company I still believe in.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!