Items that may only interest or educate me ….

Breaking banks, Deposit insurance, US economic news, European interest rate hike, dividends are a good thing …

The US Federal Reserve (Fed) raised interest rates at the fastest pace in years. Last week the financial system cracked with the sudden and unexpected failures of the Silicon Valley Bank (NASD: SIVB) and Signature Bank (NYSE: SBNY). Things are starting to break. For more on the fall of the SIVB, read the post “48 hours: The Demise of a Bank”.

Despite US regulators doing their best to calm and stabilize the markets at the start of the week, problems at European bank Credit Suisse (NYSE: CS) and First Republic Bank (NYSE: FRC) only served to bring jitters about the overall global financial system back to the surface. Famous investor Warren Buffet once said, “It’s only when the tide goes out that you learn who’s been swimming naked.” The tide is falling for the banking industry.

CS is a large Switzerland based bank that operates as a bank in Switzerland, while globally it provides wealth management, investment banking and asset management services. Its fall from grace was the result of several problems, exasperated by the current financial environment in the US. Scandals, huge losses, changes in leadership and an uninspiring recovery strategy all played a part in CS’s fall. A slow but steady withdrawal of 110 billion Swiss francs during the fourth quarter, combined with a loss of 7.29 billion Swiss francs didn’t help the bank’s liquidity issue or its reputation. When its largest lender was unable to help, Switzerland’s central bank stepped in to provide up to US$54 billion to improve CS’s liquidity and restore investor confidence. It remains to be seen if CS will pull through but a failure of one of the 30 ‘global systemically important banks’* would have a major impact on global financial system.

FRC’s problem had a similar liquidity problem but the trouble was caused by a run on its cash. The FRC is home to many high-net-worth clients who had deposits above the FDIC US$250,000 insurance limit. The wealthy clientele began shifting their money to larger, more stable banks. By midweek, their credit rating had been downgraded, accelerating the company’s share price drop off which had already lost 70% since the previous week, creating more panic. On Thursday, a group of big US banks deposited US$30 billion at FRC, where it will remain for at least 4 months.

Because banks are so interconnected, the failure of two major regional banks since March 10 threatens to erode investor and consumer confidence to a degree that could spiral in unexpected ways. The Fed now must consider the impact of further interest rate hikes on the stability of the American and global financial systems.

SIVB update: US Federal Deposit Insurance Corp (FDIC) is seeking Chapter 11 bankruptcy protection for SIVB while it looks sell off SIVB’s assets. In Canada, SIVB was taken over by the Office of the Superintendent of Financial Institutions and all of the Canadian assets will be transitioned to a temporary ‘bridge bank’ in the US, setup by the FDIC.

If you own shares in one of Canada’s big 5 banks, you should be fine other than a dip in share price (also known as a buying opportunity 😊). Same goes for investors in the big US banks. If you own shares in one or more of the smaller regional banks you are in for a wild ride until this banking crisis settles.

Status of banks in the news this past week:

- Silvergate Bank (NYSE: SI) – closed, voluntarily liquidated its assets.

- Silicon Valley Bank – closed, seeking Chapter 11 bankruptcy protection while it attempts to sell its assets.

- Signature Bank – closed, FDIC looking for a buyer.

- Credit Suisse – saved by a credit line of up to US$54 billion from Swiss National Bank, Switzerland’s central bank.

- First Republic Bank – saved by US$30 billion cash deposit by a group of large US banks.

- PacWest Bancorp Corp (NASD: PACW) – in talks with investment firms to improve its liquidity.

Is this the end of it or the tip of the iceberg?

* Globally systemic banks: banks that are considered to be critical to the global financial system due to their size, interconnectedness, complexity, and potential impact on the economy if they were to fail.

In the above section you may have noticed American depositors are insured up to US$250,000. Did you know bank accounts in Canada are insured by the Canada Deposit Insurance Corp (CDIC)? And were you aware those accounts are insured for up to C$100,000 per insured category of deposit (for example, savings, chequing, term deposits, TFSA, RRSP, etc.), at each CDIC member institution? Check out the CDIC to see if your financial institution is a member of the CDIC, and what is covered and what is not.

The latest US Labor Department report showed the US Consumer Price Index (CPI) rose 6.0% in February on a year over year basis, down from January’s 6.4%. February’s gain was the smallest on a yearly basis since September 2021. On a monthly basis, the CPI rose 0.4% last month, down from 0.5% in January. Analysts had been expecting 6% and 0.4%, respectively. The Core CPI (CPI without the food and energy components) increased 5.5% year over year, down from January’s 5.6%. That was the smallest core CPI increase on a yearly basis since December 2021. On a monthly basis, core CPI rose 0.5%, up slightly from January’s 0.4% increase. Analysts had been expecting 5.5% and 0.4%, respectively.

The US Commerce Department reported February retail sales fell 0.4% from January but were up 5.4% from February 2022. Analysts were expecting a decline of 0.3% from January.

The February Producer Price Index (PPI), what suppliers sell to businesses, unexpectedly fell 0.1% from January. On a yearly basis, the PPI rose 4.6%. Analysts had expected a monthly increase of 0.3% and a yearly increase of 5.4%. Core PPI (PPI less food, energy, and trade) grew 0.2% on a monthly basis and increased 4.4% on a yearly basis. Analysts had been expecting, 0.3% and 5.2%, respectively. On an annual basis, the PPI and core PPI were the lowest in over a year.

The Fed was going to hike interest rates by at least 0.25% at their meeting next week. Then Silicon Valley Bank and Signature Bank collapsed. Now the Fed must decide which is more important, getting inflation down to its 2% target or ensuring stability in the financial markets.

The European Central Bank (ECB) raised its benchmark rate by a surprising 0.5%, analysts and investors had a expected a 0.25% increase given the current banking situation. The larger than expected increase signalled getting inflation down was their top priority. However, they also stated they were keeping an eye on the situation and were prepared to act quickly to maintain price and financial stability in the European Union.

The Fed’s in a mandatory blackout period, which means the members are restricted from making public statements, speeches, comments to the media or to financial analysts regarding monetary policy (interest rates). The blackout begins two weeks prior to the Fed’s Federal Open Market Committee meeting and ends at the conclusion of the meeting. In other words, Fed officials aren’t talking so investors do not know what they are thinking. Despite the sudden bank failures of the last few days, the Fed is still expected to raise interest rates at its March 21-22 meeting.

Hopefully the Fed doesn’t follow the ECB’s lead with an aggressive 0.5% hike.

Previously I wrote about how share buybacks were investor friendly. This week let’s take a look at another shareholder friendly action – dividends.

A dividend is when a company pays out a percentage of their profits to shareholders. Typically, dividends are paid out quarterly, but they can also be paid monthly or other regular intervals. Some companies will even pay out special dividends when they have excess profits. In the last few years oil companies were generating windfall profits and they shared these profits with shareholders in the form of special one-time dividends, on top of their regular dividends.

Another nice thing about dividends is that they tend to increase as the company grows and generates increasing profits. On the flip side, if the company suffers a setback they may cut or eliminate their dividend altogether. This was the case with Chorus Aviation (TSX: CHR). When the Covid-19 pandemic struck in March 2020, they eliminated their quarterly dividend and have yet to restart it.

For me, the ideal dividend end company is a growing company with a rising share price and increasing dividend payments.

Now, let’s see what happened this past week….

Weekly Market Review

Monday: Ahead of this week’s US CPI report, investors are nervous following the collapse of two US regional banks. The four major North American indexes went for quite the ride Monday before ending the day largely where they started. A lot of the excitement was due to the sharp decline in bank stocks. Investors throughout the world unloaded bank shares on fears their banks could be in a similar situation or had exposure to the two American banks that collapsed.

In Canada, the Toronto Stock Exchange Composite Index (TSX) was caught in the global banking downdraft. Oil prices also fell on concerns a financial crash would cause people to cut back on spending, leading to lower energy demand. On the day, the best performing Canadian sectors were Basic Materials (mining companies and fertilizer manufacturers) and Utilities, while the Energy and Financials sector lost the most.

In the US, the indexes spent most of the day in the green before the S&P 500 Index (S&P) and the Dow Jones Industrial Average (DJIA) dropped into the red. The Nasdaq Composite Index (Nasdaq) was able to end in the green thanks to investor expectations the Fed will not make a larger rate hike next week in lieu of the SIVB collapse. In trading, the defensive Utilities sector led a group of four sectors higher. Unsurprisingly, the Financials and the Energy sectors dropped the most, both ending down more than 2%.

Tuesday: It was a bit of a bounce back day as all four indexes finished the day higher. Today’s US CPI data came in at 6% and core CPI increased 5.5%, both on a yearly basis. Both matched forecasts. Investors seem to have absorbed the banking events of the past few days and are now expecting the Fed to raise the US interest rate by 0.25%, with an optimistic few hoping for a pause considering the stress past hikes have put on the US financial system.

In Canada, the Financials sector rebounded from yesterday’s decline. The Technology and Basic Materials sectors led Canadian sectors, while the Energy and Telecommunications Services sectors were the only two sectors to end lower.

In the US, the smaller regional banks bounced back as fears of a banking crisis faded. As well, the CPI data indicated inflation continues to cool. Investors reacted to the good news by sending the three US indexes sharply higher. In trading, all American sectors ended higher, led by the Technology and Financials sectors, with Energy and Consumer Staples bringing up the rear.

Wednesday: All four indexes tumbled lower before trimming losses in a late afternoon rally. Only the Nasdaq was able to inch into positive territory. European bank Credit Suisse caused fresh banking concerns when it reported it had identified “material weaknesses” in its financial reporting controls. Investors pummeled the share price, sending its US listed shares to a record low. Separately, US economic data showed US inflation was slowly falling but not enough to avoid at least one more interest rate hike. Oil prices dropped sharply as banking concerns continue to rattle the market along with fears of what another interest rate increase would do to the global economy.

In Canada, the TSX has its worst day since October 2022, pulled lower by the ongoing weakness in the global financial sector. In trading, of the Canadian sectors, the defensive sectors Consumer Staples and Utilities gained the most, while Energy and Basic Materials lost the most.

In the US, the February retail sales fell 0.4% and the PPI dropped 0.1% since January. On a yearly basis, both were up 5.4% and 4.6%, respectively. With the monthly drops, investors are hoping the Fed would leave the interest rate unchanged. In trading, of the American sectors, only the defensive Utilities and Consumer Staples sectors ended in positive territory. Energy and Basic Materials dropped the most.

Thursday: The market got off on the wrong foot when the European Central Bank raised its benchmark rate by a surprising 0.5%. What looked like another decline took a turn for the better when a group of American banks joined together to deposit US$30 billion into First Republic which had been teetering on the edge of collapse. The influx of cash stabilized the bank and calmed depositors and investors, starting a strong rally in all four indexes.

In Canada, the TSX was lifted into positive territory on the news banking crisis in the US had been averted, in the short term anyway. In trading, Industrials and Consumer Cyclicals led the pack of Canadian sectors. Consumer Staples was the only sector to end the day in the red.

In the US, the American indexes rebounded strongly from yesterday’s losses when the larger US banks stepped up to stabilize Federal Bank, and by extension the US banking system. The technology sector had a big rally, leading the Nasdaq to its best single day in over a year. On Wall Street, Technology and Consumer Cyclicals shone the brightest of the American sectors. The only sector to lose ground was Telecommunications Services.

Friday: The wild ride of the banking industry continued today, with all four indexes ending the day solidly in the red. Losses in the North American banking industry and fears of a recession continued to drag the markets lower.

In Canada, the TSX is heavily exposed to Financials and Energy (both sectors tend to fall during a recession) so its not surprising with fears of a looming recession that the TSX experienced another losing session. In the Canadian market, Basic Materials, Utilities and Telecommunications Services were the only sectors to advance. Of those that declined, Financials and Industrials dropped the most.

In the US, the banking crisis continued, which increases the chance of a recession. Ahead of the Fed’s meeting next week, investors now are expecting a 0.25% rate hike but hoping for no rate change. In the American markets it was not a good day, with all sectors ending lower. The Technology and Telecommunications Services sector were the best of the bad lot, dropping the least, while Financials and Industrials dropped the most.

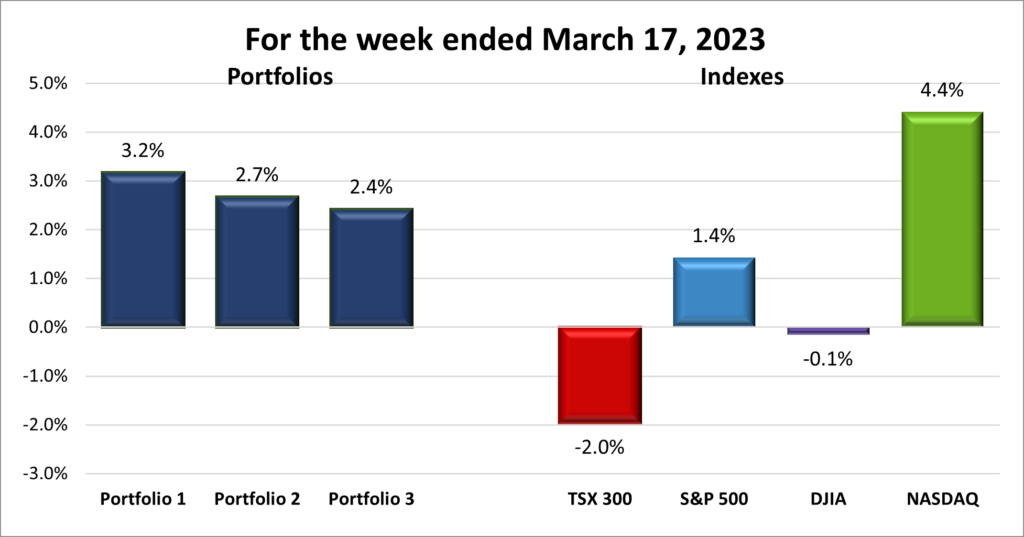

For the week, the TSX dropped 2.0%, the S&P 500 advanced 1.4%, the DJIA fell 0.1% and the Nasdaq grew 4.4%.

Weekly Portfolio Review

![]()

Given all the sky is falling chatter about the US banking system, and by extension, the global financial system, I was surprised to see the Nasdaq and S&P end the week higher (as shown in the chart above). I thought the Financials sector in both countries would drag all four indexes lower but the technology heavy Nasdaq and S&P received a nice little boost from investors who decided to park their cash in the big technology companies. As a result, the Nasdaq and S&P made it into positive territory for the week. How good was the week for big tech? Microsoft had its best week in almost eight years. 😊

The Financials sector did drag the DJIA and TSX lower. For the DJIA, four of the thirty companies are in the Financials sector. However, Microsoft (NASD: MSFT) is also a DJIA member and I suspect its banner week helped limit the fall. On the TSX, the Financials and Energy sectors combine to make up 49% of the index. Both sectors had a bad week, causing the TSX to end the week in the red.

The Portfolios benefitted from the Nasdaq’s strong week. Each portfolio has at least one big-tech company. Portfolio 1 contains four of them – Alphabet (NASD: GOOGL), Amazon (NASD: AMZN), Apple (NASD: AAPL), and Nvidia (NASD: NVDA) – which helped the portfolio gain 3%. Portfolios 2 and 3 both contain Microsoft, which helped them each outperform all of the indexes except the Nasdaq. Any week where all three Portfolios advance is a good week, but it would be better without the drama of a banking crisis. 😊

Companies on the Radar

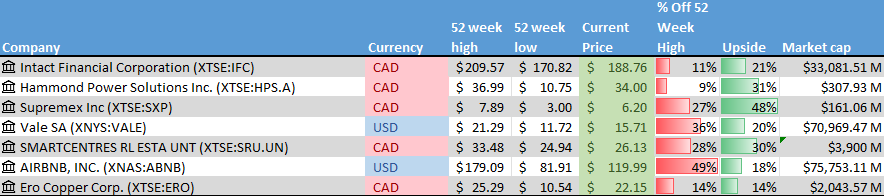

Only one new company came onto my radar this past week – Ero Copper Corp. (TSX: ERO). A small cap Canadian copper mining company with mines in Brazil. It also owns a smaller gold and silver mine in Brazil. I have been considering a mining company for a while now because there is a growing demand for these metals in electric vehicle (EV) manufacturing, the renewables sector and industry in general. Copper, in particular, is used extensively in EV motors, wind turbines, solar panels as well as electrical components, industrial machinery, medical equipment, wiring/cabling, and plumbing equipment.

- Intact Financial (TSX: IFC): A mid size insurance company supplying home, car and business insurance in Canada, the US, and the UK.

- Hammond Power Solutions (TSX: HPS.A): A Canadian company manufacturing transformers used throughout the world in a wide variety of industries.

- Supremex (TSX: SXP): A small cap company selling packing solutions throughout Canada and the USA.

- Vale (NYSE: VALE): A global mining company that extracts various metals and rare earth elements such as nickel, cobalt, gold, copper, that are used in electric vehicles.

- Smartcentres Real Estate Investment Trust (TSX: SRU.UN): Owns and manages a number of income producing malls and retails spaces throughout Canada.

- Airbnb (NASD: ABNB): An online platform allowing people to book private residences for short term stays.

The Radar Check was last updated March 17, 2022.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended March 17, 2023: UP ![]()

- Rivian (NASD: RIVN) and Amazon are in negotiations to end the exclusivity deal Amazon has with Rivian for the first 100,000 of Rivian’s electric vans. On the surface this sounds like a negative development for Rivian, but it could free Rivian to focus on their higher profit margins vehicles and execute on its plans to deliver 50,000 vehicles in 2023. Rivian no longer has a demand problem with 114,000 reservations for Rivian trucks and SUVs and its expected it will take until late 2024 to clear the backlog. How one views this depends on whether you think the glass is half full or half empty.

- ZIM Integrated Shipping Services Ltd. (NYSE: ZIM) announced a dividend of US$6.40 payable to shareholders as of April 4, 2023. Not a bad quarterly dividend. 😊

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSX: DIR.UN)

BSR Real Estate Investment Trust (TSX: HOM.U)

Yellow Pages Ltd (TSX: Y)

US $

General Motors Co (NYSE: GM)

Quarterly Reports

ZIM Integrated Shipping Services Ltd.

All currency listed in millions of US dollars.

Selected highlights from their fourth quarter 2022 financial results on March 13, 2023

- Revenue of $2,188.9 for the three months ended December 31, compared to $3,466.4 for the same period in 2021. A decrease of almost 36%.

- Net income of $416.5 for the three months ended December 31, compared to net income of $1,708.4 in the same period in 2021.

- Diluted earnings per ordinary share of $3.44 for the three months ended December 31, compared to $14.17 for the same period in 2021.

- Revenue of $12,561.6 for the year ended December 31, compared to $10,728.7 for the same period in 2021. An increase of over 17%.

- Net earnings of $4,629.0 for the year ended December 31, compared to net earnings of $4,649.1 in the same period in 2021.

- Diluted earnings per ordinary share of $38.35 for the year ended December 31, compared to $39.02 for the same period in 2021.

Algonquin Power & Utilities Corp.

All currency listed in millions of US dollars.

Selected highlights from their fourth quarter 2022 financial results on March 17, 2023

- Revenue of $748.0 for the three months ended December 31, compared to $592.0 for the same period in 2021. An increase of over 26%.

- Net loss of $74.4 for the three months ended December 31, compared to net income of $175.6 in the same period in 2021.

- Diluted loss per ordinary share of $0.11 for the three months ended December 31, compared to earnings of $0.27 per share for the same period in 2021.

- Revenue of $2,765.2 for the year ended December 31, compared to $2,274.1 for the same period in 2021. An increase of almost 22%.

- Net loss of $212.0 for the year ended December 31, compared to net earnings of $264.9 in the same period in 2021.

- Diluted loss per ordinary share of $0.33 for the year ended December 31, compared to earnings of $0.41 per share for the same period in 2021.

Portfolio 2

Portfolio 2 for the week ended March 17, 2023: UP ![]()

- The advertising technology partnership between Microsoft and Netflix (NASD: NFLX) may becoming to an end. The deal is for two years but Netflix is considering bringing its advertising technology in house, either buying the technology or building it themselves.

Microsoft signed another 10-year licensing agreement to provide Xbox and Activision games with another cloud-based gaming company. This time it was with Japan’s Ubitus. The deal goes in effect once the Microsoft acquisition of Activision Blizzard (NASD: ATVI) closes. Microsoft now has licensing agreements in place with Nvidia, Nintendo, Boosteroid and Valve Corp, owner of Steam, the world’s largest video game distribution platform.

Microsoft announced Artificial Intelligence (AI) will be rolled out to Office 365 users. The platform will be called ‘Microsoft 365’ and supposedly can pull data from other applications, help users with Excel formulas and features, summarize email chains and best of all, summarize virtual meetings on the Teams platform. - Alimentation Couche-Tard (TSX: ATD) bought a portion of France’s TotalEnergies (NYSE: TTE) gas stations. In return for US$3.3 billion, ATD will receive all of TotalEnergies’ gas stations in Germany and the Netherlands, plus 60% of it’s station in Belgium and Luxembourg. ADT plans to turn these gas stations into food and service hubs, similar to the fuel stations it operates in North America.

- Last December, Disney (NYSE: DIS) raised the price of its Disney+ ad free streaming service by 38% to US$10.99 per month. At the same time Disney launched the ad supported streaming service Disney+ Basic for US$7.99 per month. Despite the lower fee Disney+ Basic, Disney+ was able to maintain 94% of its subscribers. That is impressive pricing power!

- Guardant Health’s (NASD:GH) co-CEO AmirAli Talasaz bought 97,000 shares of his company for approximately US$2.5 million. He now directly owns over 1.9 million shares. Usually, the only notices I receive of insider buys and sells is when an insider sells shares. If anyone should know how the company is doing it’s the CEO. When I saw this large purchase, it gave me renewed confidence in the company and the share price should recover.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

iA Financial Corporation Inc (TSX: IAG)

US $

No US$ dividends this past week.

Quarterly Reports

Alimentation Couche-Tard Inc.

All currency listed in millions of US dollars.

Selected highlights from their third quarter 2023 financial results on March 15, 2023

- Revenue of $20,055.1 for the 16 weeks ended January 29, compared to $18,576.4 for the same period in 2022. An increase of almost 8%.

- Net income of $737.4 for the 16 weeks ended January 29, compared to net income of $746.4 in the same period in 2022.

- Diluted earnings per ordinary share of $0.73 for the 16 weeks ended January 29, compared to $0.70 for the same period in 2022.

- Revenue of $55,592.3 for the 40 weeks ended January 29, compared to $46,375.0 for the same period in 2021. An increase of almost 20%.

- Net earnings of $2,420.2 for the 40 weeks ended January 29, compared to net earnings of $2,205.6 in the same period in 2021.

- Diluted earnings per ordinary share of $2.38 for the 40 weeks ended January 29, compared to $2.06 for the same period in 2021.

Portfolio 3

Portfolio 3 for the week ended March 17, 2023: UP ![]()

- The Royal Bank (TSX: RY) is considered one of the favourites to pick up both SIVB’s current list of corporate customers, as well as future Canadian startup clients. With one of the most aggressive lenders to startups out of the picture (SIVB), the big five Canadian banks can afford to be more selective in who they help finance. Good for banks, not so good for startups.

- Shopify (TSX: SHOP) has integrated Moovly Media Inc. (TSXV: MVY) E-commerce video maker into their web offerings. Moovly’s video maker provides Shopify’s merchants with the tools to create their own product videos and ads based on the data on their Shopify site.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

Fortuna Silver Mines Inc.

All currency listed in thousands of US dollars.

Selected highlights from their fourth quarter 2022 financial results on March 16, 2023

- Revenue of $164.7 for the three months ended December 31, compared to $198.9 for the same period in 2021. A decrease of over 17%.

- Net loss of $160.4 for the three months ended December 31, compared to net income of $16.6 in the same period in 2021.

- Diluted loss per ordinary share of $0.52 for the three months ended December 31, compared to earning of $0.05 per share for the same period in 2021.

- Revenue of $681.5 for the year ended December 31, compared to $599.9 for the same period in 2021. An increase of almost 14%.

- Net loss of $135.9 for the year ended December 31, compared to net earnings of $59.4 in the same period in 2021.

- Diluted loss per ordinary share of $0.44 for the year ended December 31, compared to earning of $0.24 per share for the same period in 2021.