How Government Moves Can Drive Companies

Big moves don’t always come from companies themselves – sometimes, it’s governments that shake up markets. This week, the US government stepped more directly into the race for critical resources, with lithium the latest focus. With demand for electric vehicles (EV) and clean energy storage rising, Washington is making moves to secure supply chains and reduce reliance on imports.

That push was front and centre with the Canadian company Lithium Americas (TSE: LAC). Shares surged in after-hours trading after reports that the US government is looking to renegotiate a $2.26B loan tied to its Thacker Pass project in Nevada. As part of the talks, Washington may seek up to a 10% stake in the company – a strong signal of just how strategic this project has become.

We’ve seen this playbook before. Earlier this year, the US government secured a stake in Intel (NASD: INTC) as part of its broader effort to rebuild domestic chipmaking capacity. Lithium Americas could be the next example of Washington using ownership stakes to lock down critical supply chains and support industries essential to the country’s economic future.

For us investors, it’s a good reminder that markets aren’t just moved by earnings reports or product launches. Government policy, financing, and even ownership can dramatically reshape a company’s outlook. In this case, Washington is making it clear how serious it is about securing lithium – the building block of EV batteries and clean energy storage. And with Thacker Pass set to become the Western Hemisphere’s largest lithium source by 2028, it’s easy to see why the US wants a seat at the table.

As a shareholder, I see the potential government stake as a double-edged sword. On the upside, it can bring stability, easier access to funding, and political support for strategic projects. On the downside, it may dilute existing shareholders, add political strings and extra oversight, and expose the company to shifting government priorities. For now, though, I’ll happily sit back and enjoy nearly doubling my position’s value since the announcement. 😊

While the spotlight was on Lithium Americas this week, the rest of the market had plenty of action too. Let’s take a look at how the major indexes moved, what drove market sentiment, and how my three portfolios held up over the past week – there were some interesting developments to keep an eye on. 😊

Items that may only interest or educate me ….

Canadian economic news, US economic news, ….

Canadian Economic News

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Gross Domestic Product (GDP)

Statistics Canada reported that Canada’s GDP grew 0.2% in July, the first increase in four months following a slight 0.1% decline in June. Analysts had expected a 0.1% rise, so the economy slightly outperformed expectations. This growth was largely driven by a 0.6% rebound in goods-producing industries, with all sectors in that group posting gains. Services-producing industries edged up 0.1%, supported by wholesale trade and real estate, while retail trade saw a small pullback. Overall, 11 of the 20 industrial sectors expanded.

Month over month, goods-producing industries were led by mining and energy, which jumped 1.4%, while construction and agriculture grew more modestly. Services gains were driven by transportation and warehousing, though retail and arts and entertainment slipped. On a yearly basis, GDP rose 0.9%, with mining and finance seeing strong gains while the management of companies sector fell sharply.

Overall, July’s data points to a modest rebound, with some sectors bouncing back while others lag. Advance estimates suggest August GDP was essentially flat, highlighting the uneven pace of Canada’s economic recovery.

Canadian Market Volatility

Canada’s volatility gauge, the S&P/TSX 60 Volatility Index (VIXC), opened the week at 9.77 and steadily climbed, briefly spiking above 11.5 on news of a stronger-than-expected US economy. It then eased back below 11 after data showed the Canadian economy grew for the first time in four months and US inflation came in as expected, finishing the week at 10.77.

For those new to it, the VIXC is like a barometer of investor nerves in Canada. When it sits in the single digits to low teens, markets are usually calm. Once it climbs into the mid-teens or higher, it signals traders are getting more uneasy and bracing for turbulence. With the index closing near the lower end of its usual range, the mood on Bay Street looked more relaxed than rattled to end the week.

US Economic News

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Gross Domestic Product (GDP)

The US economy turned in a stronger showing than expected in the second quarter. The Commerce Department’s Bureau of Economic Analysis (BEA) reported that GDP grew at a 3.8% annualized pace in its final estimate – above the earlier 3.3% reading and far stronger than the 0.6% growth we saw in the first quarter.

The upgrade came mainly from consumers spending more than expected, alongside fewer imports and a narrower trade deficit. At the same time, some areas like business investment and exports were revised lower, showing the growth wasn’t entirely broad-based.

For us investors, the message is clear: the American economy is running hotter than many thought. That’s a double-edged sword. Stronger growth can fuel company earnings, but it also gives the Fed less incentive to keep cutting rates. Keep in mind, the Fed doesn’t want to add fuel to an already-strong economy. The biggest risk now is whether consumers, the backbone of the US economy, can keep spending at this pace as inflation, debt, and employment pressures build.

In short, investors may welcome the growth surprise, but they’ll also stay cautious. The Fed’s next moves could hinge less on GDP and more on whether inflation remains sticky and the labour market continues to cool.

Personal Consumption Expenditures Price Index (PCE)

The BEA’s August PCE report showed inflation moving largely in line with expectations. Headline PCE, or all items, rose 0.3% in August, a touch higher than July’s 0.2%, bringing the annual rate to 2.7% versus 2.6% last month. Core PCE, which strips out food and energy, gained 0.2% on the month after July’s 0.3% uptick, with the annual pace climbing to 2.9% from 2.6%. In short, the numbers matched what analysts were looking for – no major surprises for the markets.

The data signals that inflation isn’t cooling just yet – instead, it’s proving sticky, with both headline and core running above the Fed’s 2% target. At the same time, consumer spending is still growing, underlining the economy’s resilience. That combination keeps the Fed in a tricky spot: move too quickly on rate cuts and risk fuelling more inflation or hold back and risk slowing growth. For now, the central bank seems more likely to tread carefully before making big moves.

For investors, this means uncertainty remains the theme. Companies with strong pricing power, the ability to protect margins by passing on costs, may be better positioned. Diversification is also important, since inflation-hedging assets like commodities and real assets can help balance risk. Real assets are things you can physically touch or use, such as real estate, infrastructure, or farmland, and they often hold value better during inflation. On the flip side, rate-sensitive sectors – industries that rely heavily on borrowing, like utilities, real estate, or some consumer discretionary companies – could stay under pressure until the Fed signals more confidence that inflation is heading toward its target.

Consumer Sentiment Index (CSI)

The University of Michigan’s final Consumer Sentiment Index (CSI) for September came in at 55.1, a touch below expectations of 55.4 and down 5.3% from August’s 58.2. Compared to a year ago, sentiment has tumbled 21.6%, showing how cautious households have become.

Breaking it down, the Current Economic Conditions Index – which gauges how people feel about their present situation, from job security to personal finances – slipped to 60.4, down 2.1% month over month and 5.3% year over year. The Expectations Index, which looks six months ahead, saw a steeper drop, falling 7.5% to 51.7 and down a hefty 30.6% from last year.

On inflation, short-term expectations (one year ahead) eased slightly to about 4.7% from 4.8%, but longer-term expectations crept up to around 3.7%. Sentiment weakness was broad across age, income, and education groups, though investors with larger stock holdings were more resilient, while those with smaller or no portfolios felt the pinch more sharply.

For us investors, the key takeaway is that while consumer spending has remained strong according to the latest GDP report, households are clearly growing more cautious about the future, especially with prices still weighing on budgets. Since consumer activity drives the bulk of the US economy, this dip in confidence could eventually translate into slower spending, making it worth watching closely alongside hard data like GDP and retail sales.

American Market Volatility

The CBOE Volatility Index (VIX), often called the market’s “fear gauge,” was relatively calm this week, but there were bumps along the way. Starting at 16.14, it jumped above 17 after Fed Chair Powell warned the Fed would move cautiously on future rate cuts. It spiked above 17 several more times on anticipation of labour, GDP, and PCE inflation data before settling back down to 15.29 by week’s end.

Think of the VIX as a market mood ring. When it’s in the 12 to 20 range, investors are generally calm and steady. Once it pushes higher, it’s a sign traders are growing uneasy and bracing for bumpier days ahead. A rising VIX doesn’t always mean panic, but it does mean caution is creeping back into the market.

Weekly Market and Portfolio Review

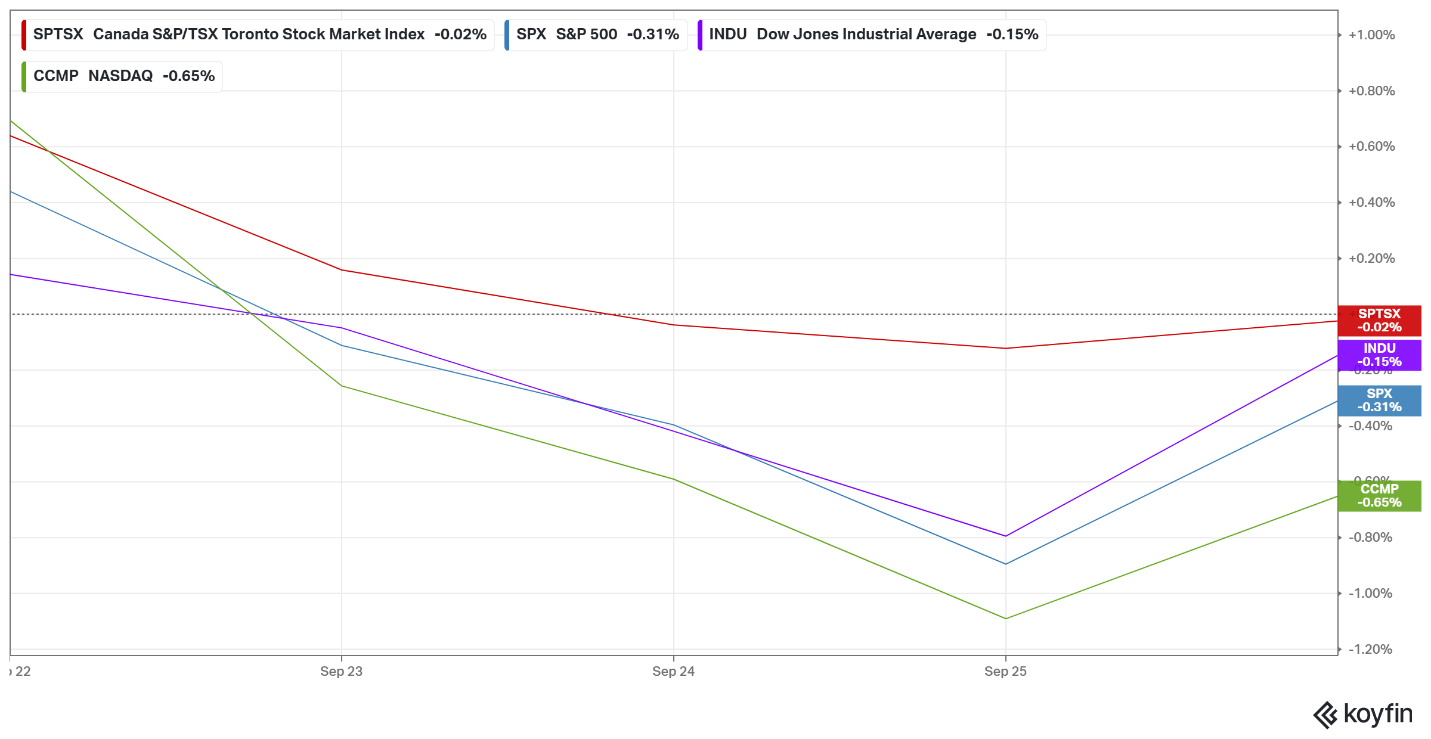

For the week, the TSX (SPTSX) ended slightly lower, dropping 0.02%, the S&P 500 (SPX) fell 0.3%, the DJIA (INDU) dipped 0.1% while the Nasdaq (CCMP) tumbled 0.7%.

| Index | Weekly Streak |

| TSX: | 1 – week losing streak |

| S&P: | 1 – week losing streak |

| DJIA: | 1 – week losing streak |

| Nasdaq: | 1 – week losing streak |

![]() The week started on a high note, with all four major North American indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite (Nasdaq) – extending their streak of record highs. But the celebration didn’t last long. Fed Chair Powell’s reminder that the central bank would move cautiously on future rate cuts cooled the rally, a quick reality check that September’s trademark volatility was still in play.

The week started on a high note, with all four major North American indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite (Nasdaq) – extending their streak of record highs. But the celebration didn’t last long. Fed Chair Powell’s reminder that the central bank would move cautiously on future rate cuts cooled the rally, a quick reality check that September’s trademark volatility was still in play.

By midweek, US markets slipped as stronger-than-expected GDP upended expectations for aggressive rate cuts. The economy grew faster than first thought in the second quarter, thanks to resilient consumer spending. Normally a positive sign, the strength raised concerns about how far the Fed can go with cuts without risking an overheated economy. Optimism faded and economic growth that might have been a tailwind turned into a policy headwind. PCE inflation, the Fed’s preferred gauge, came in largely as expected, though underlying price pressures remained sticky.

Trade tensions added more fuel to the fire. President Trump escalated tariff wars with US trading partners, rolling out sector-specific levies: a 100% tariff on branded pharmaceuticals not manufactured in the US; 25% on imported heavy-duty trucks; 50% on kitchen cabinets, bathroom vanities, and related products; and 30% on upholstered furniture. Set to take effect October 1, the measures clouded the global trade outlook just as negotiations with partners like South Korea showed glimmers of progress. Investors were left weighing solid economic growth against the risks of policy and trade setbacks.

North of the border, the TSX snapped its seven-week winning streak, though resource strength softened the blow. Gold and oil prices climbed, giving miners and energy stocks a lift. Lithium Americas surged on reports the US government may take up to a 10% stake in its Thacker Pass project as part of a loan renegotiation – a move tied to Washington’s drive to secure critical minerals for EV supply chains. On the flip side, tech heavyweight Constellation Software (TSE: CSU) slipped after longtime president Mark Leonard resigned for health reasons, dragging the sector lower. On the economic front, July GDP showed a modest rebound, but third-quarter growth is tracking flat, adding to the cautious tone.

In the end, a pair of strong trading sessions bookended a choppy week in both countries. With commodity prices holding firm, economic growth beating expectations on both sides of the border, and US inflation coming in as forecast, investors had reason to feel a bit more optimistic heading into next week. 😊

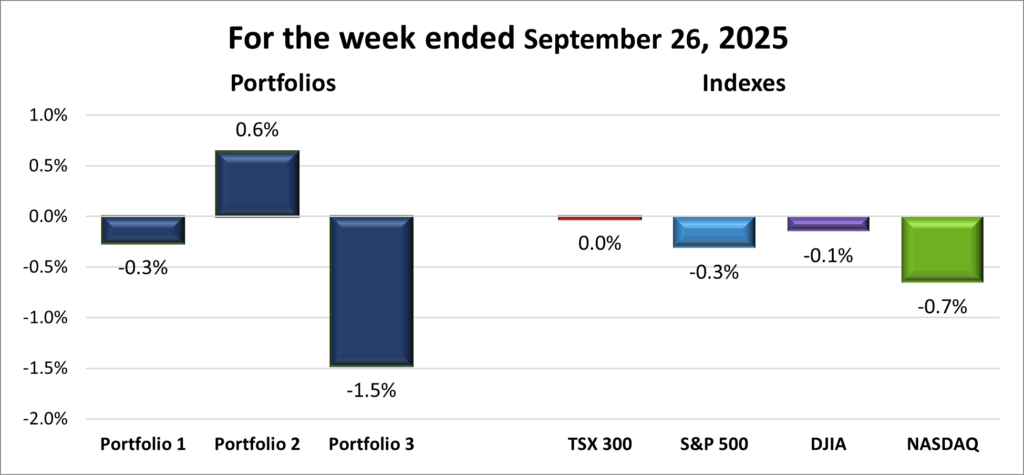

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week losing streak |

| Portfolio 2: | 8 – week winning streak |

| Portfolio 3: | 1 – week losing streak |

![]()

![]() Not the best week in the markets, but at least none of the major indexes fell more than 1%. My portfolios, however, had a tougher time – though there were still some bright spots to highlight.

Not the best week in the markets, but at least none of the major indexes fell more than 1%. My portfolios, however, had a tougher time – though there were still some bright spots to highlight.

Portfolio 1 slipped 0.3%, splitting evenly between winners and losers. The highlights included all-time highs from Nvidia (NASD: NVDA), Cameco (TSE: CCO), and Celestica (TSE: CLS), plus a 10% jump from indie Semiconductor (NASD: INDI). The drag came from Magnite (NASD: MGNI), which tumbled 14%.

Portfolio 2 was one of the bright spots, pulling off a 0.6% gain. It wasn’t flashy, but in a down week, a win is a win. 😊 Portfolio 2 also had the best percentage of weekly winners, with 59%. Take-Two Interactive (NASD: TTWO) and South Bow (TSE: SOBO) both hit all-time highs during a tough week.

Portfolio 3 had the roughest ride, falling 1.5%, with only a third of holdings finishing the week higher. The big story was Lithium Americas, which surged as much as 90% after reports that the US government may take up to a 10% stake in the company – and it had doubled by week’s end. On the flip side, Magnite’s 14% slide hurt, but thanks to Nvidia’s 1.7% gain (and heavy portfolio weighting), the damage was at least partly cushioned.

All told, it was a mixed week across the three portfolios, with some big wins and some setbacks. Even in a choppy market, a few standout performances reminded me that there are always opportunities to celebrate. 😊

Companies on the Radar

No new names landed on my radar this week, but I did some tidying up by trimming Copart (NASD: CPRT) from the list. Copart is a solid operator, running one of the world’s largest online vehicle auction platforms, but I felt my attention was better spent on other opportunities – either among the companies already in my three portfolios or those that are still on my radar list.

No new names landed on my radar this week, but I did some tidying up by trimming Copart (NASD: CPRT) from the list. Copart is a solid operator, running one of the world’s largest online vehicle auction platforms, but I felt my attention was better spent on other opportunities – either among the companies already in my three portfolios or those that are still on my radar list.

For now, my radar list consists of the four holdovers from last week:

- Mainstreet Equity Corp. (TSE: MEQ): a Calgary-based real estate company focused on mid-market apartment buildings – typically under 100 units – across Western Canada. It buys underperforming properties at below-market prices, renovates them, and increases rental income through improved operations. With strong demand for rental housing, a repeatable value-add strategy, and a solid balance sheet, Mainstreet offers a compelling mix of income and growth. Shares currently trade below net asset value, giving investors a margin of safety alongside steady cash flow and long-term upside.

- Tornado Infrastructure Equipment Ltd. (TSEV: TGH), a small Canadian industrial company that designs, builds, and sells hydrovac trucks across North America, while also generating recurring revenue through rentals, parts, and maintenance – making it more than just a pure equipment play.

- Arista Networks (NYSE: ANET): an American company that designs and sells advanced networking hardware and software, with a focus on high-speed, low-latency switches for its key markets: data centres, artificial intelligence (AI), cloud computing, and financial trading. The company has been riding the AI tailwind with solid demand from its core markets, especially in AI and cloud data centres. It also has a hefty share buyback program and increasing investments from some of the top institutional investment companies.

- Corning Incorporated (NYSE: GLW): a large cap American company that is a leader in specialty glass, optical fiber, environmental technology, life sciences, and other specialty glasses. They have been the supplier of the glass used in Apple’s iPhones since 2007, and they are riding the tailwind of an AI-driven fiber optic boom.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated September 26, 2025.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!