A Government Shutdown Doesn’t Mean a Market Meltdown

This past week, funding for the US government expired at midnight on September 30. With Republicans and Democrats dug in, no deal was reached to pass a temporary spending bill and avert a shutdown. As a result, the government was suspended for the 15th time since 1981, halting scientific research, financial oversight, environmental cleanup, and a wide range of other services. About 750,000 federal workers were ordered to stay home, while others – including the armed forces and Border Patrol agents – continued working without pay (they’ll be paid retroactively once operations resume). A shutdown usually doesn’t send markets into free fall, but it does tend to stir up volatility on both sides of the border. So, let’s take a look at what a US government shutdown actually is and what it means for us investors.

A shutdown happens when Congress can’t agree on a budget or stopgap funding measures, forcing many federal agencies to close or scale back operations. Essential services keep running, but hundreds of thousands of government workers are furloughed without pay, and many public services grind to a halt until funding is restored. That lack of paycheques can ripple into consumer spending and confidence if the shutdown drags on.

The biggest immediate impact for investors isn’t that markets stop functioning – it’s that critical economic data releases get delayed. Agencies like the Bureau of Labor Statistics (BLS), which produces jobs data, the unemployment rate, and inflation reports like Consumer Price Index, and the Bureau of Economic Analysis (BEA), which publishes Gross Domestic Product and Personal Consumption Expenditure inflation (a favourite of the Fed), would have to pause. With data blacked out, investors and policymakers alike lose important data about where the economy is headed. With official reports stalled, investors often turn to alternative data – things like private payroll surveys or credit card spending trends – and many take on more defensive positions as they brace for potential swings in asset prices.

For markets, shutdowns bring short-term uncertainty and nervous trading, but history shows the economic damage is usually limited. In 2013, a 16-day shutdown over healthcare funding triggered an initial dip in the S&P 500, only for stocks to rebound once a deal was struck. The 2018–19 shutdown – the longest in history at 35 days – weighed on sentiment but didn’t stop the market from climbing, as investors focused on earnings and Fed policy. In short, shutdowns rattle nerves more than they alter the long-term trajectory.

For investors, the bigger worry is what shutdowns signal: deepening political gridlock in Washington. Battles over spending and the debt ceiling can raise concerns about fiscal discipline and send investors toward safe havens like bonds or gold, often at the expense of stock prices.

And for us Canadian investors, the ripples travel north quickly. When Wall Street stumbles, Bay Street usually follows. A shutdown adds uncertainty for Canadian companies tied to US demand, pressures the US dollar, and delays data that Canadian policymakers and markets rely on. It’s one more reminder that while shutdowns may start in Washington, their effects are felt well beyond America’s borders.

At the end of the day, shutdowns make headlines, but history shows markets usually take them in stride once the dust settles. For us investors, what really matters is how companies are performing and where interest rates are headed. So, let’s move from Washington’s gridlock to the week in the markets – and see how my portfolios made out.

Items that may only interest or educate me ….

US Government Takes Stake in Another Public Company, Canadian Economic news, US Economic news, ….

US Government Takes Stake in Another Public Company

Last week I mentioned that the US government was weighing a stake in Lithium Americas (TSE: LAC) to shore up access to lithium, the critical metal behind electric vehicle (EV) batteries. This week, it became official: the Department of Energy (DOE) is taking a 5% equity stake in Lithium Americas, plus another 5% in its Thacker Pass mine joint venture with General Motors (NYSE: GM). The deal comes alongside a US$2.26 billion loan to help build out Thacker Pass, which is on track to become one of the largest lithium mines in North America.

Lithium is at the heart of EV batteries and renewable energy storage, yet the US still depends heavily on imports, especially from China, for refined supply. By taking a direct stake, Washington is signaling just how serious it is about securing domestic supply chains. For Lithium Americas, government backing not only boosts credibility but also provides the financial firepower to accelerate development.

For investors, the US government’s move is a major vote of confidence. It shows that Lithium Americas now has both the funding and political backing to get Thacker Pass off the ground. Of course, risks remain – mining is a tough business and lithium prices can swing wildly – but the odds of this project becoming reality just went up, along with the value of my investment in the company. 😊

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Bank of Canada minutes

On September 17, 2025, the BoC cut its overnight rate by 0.25% to 2.50%, the first cut in six months and the lowest level in three years. The minutes showed there was debate around holding at 2.75%, given inflation still near the top of the bank’s 1%–3% target range, resilient consumer spending, and uncertainty over whether earlier cuts had fully worked their way through the economy. But in the end, mounting headwinds tipped the balance toward a cut.

The decision was driven by four main concerns:

- Labour market strain – Canada lost over 100,000 jobs in two months, pushing unemployment to a nine-year high (excluding pandemic years).

- Economic contraction – GDP shrank 1.6% in the second quarter, weighed down by weaker exports and business investment, even as consumer spending and housing stayed firm.

- Easing inflation – Headline CPI cooled to 1.9%, while core inflation held between 2.5–3%.

- Trade pressures – US tariffs on steel, aluminum, autos, lumber, and copper added more stress to an already slowing economy.

For investors, the message is clear: borrowing costs are heading lower, a tailwind for consumers and housing. At the same time, the move highlights real worries about growth and trade, meaning financials may feel some pressure while more defensive sectors like consumer staples and utilities could be better positioned.

Looking ahead, the Bank’s next policy announcement comes on October 29, when it will also release its Monetary Policy Report. That report is basically the Bank’s playbook – it lays out how they see the economy performing, what risks they’re watching, and where interest rates might be headed next. Until then, the BoC has signaled it’s ready to cut again if conditions get worse.

Canadian Market Volatility

Canada’s volatility gauge, the S&P/TSX 60 Volatility Index (VIXC), had a calm week overall, opening at 11.23, hovering mostly between 11 and 11.5, and easing to close at 10.96. The only odd move came at the October 2 open, when it briefly plunged to 9.25 before bouncing back above 10 within minutes. That quick drop was just a quirk of how the market opens – when buy and sell orders are matched at the opening bell, volatility indexes can flicker before settling into their normal range.

For those new to it, the VIXC is like a barometer of investor nerves in Canada. When it sits in the single digits to low teens, markets are usually calm. Once it climbs into the mid-teens or higher, it signals traders are getting more uneasy and bracing for turbulence. With the index closing near the lower end of its usual range, the mood on Bay Street looked more relaxed than rattled to end the week.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Consumer Confidence Index (CCI)

According to The Conference Board, in September US consumer confidence fell more than expected, with the CCI dropping to 94.2, its lowest level since April. The Present Situation Index, reflecting views on current business and labour conditions, dropped 7 points to 125.4 – its largest drop in a year. The forward-looking Expectations Index fell to 73.4, staying below the 80 mark and signaling that consumers expect a challenging economic period ahead.

The report suggests Americans are growing more uneasy about the job market, with perceptions of job availability hitting a multi-year low. Rising costs for essentials and softer labour conditions are adding to the concerns.

For markets, this hints at a slowing economy and may boost expectations for Fed rate cuts. For us investors, it suggests that consumer-reliant sectors like retail and travel could face headwinds, while defensive sectors like groceries and healthcare often hold up better.

Labour data

This week’s labour data from three major reports – the Job Openings and Labor Turnover Survey (JOLTS), the ADP Employment Report, and the Employment Situation Summary (ESS) – gives a full snapshot of the US job market. Each report looks at a different angle: JOLTS tracks demand for workers through openings, hires, and quits; ADP previews private-sector payroll growth; and the ESS, also known as the monthly jobs report, delivers the big picture with unemployment, job gains, and wage growth. Together, they show whether the job market is heating up or starting to cool.

Labor Department’s Job Openings and Labor Turnover Survey

The August JOLTS report showed job openings ticking up slightly to 7.23 million, just 19,000 higher than July. The broader takeaway: the job market looks to be leveling off. Companies aren’t aggressively hiring anymore, but they’re also not cutting in big numbers – signalling cooling demand but still-stable employment. For the Fed, that softer trend adds to the case for more rate cuts, giving them room to support growth.

ADP Employment Report

ADP’s September data showed private employers shed 32,000 jobs, compared with expectations for a 50,000 gain. Adding to the surprise, August was revised from a reported 54,000 increase to a small 3,000 loss. The weakness was broad-based, with leisure and hospitality hit hardest. Since ADP only covers private-sector jobs, it excludes government workers, the takeaway is clear: hiring momentum is fading. With jobs long considered the backbone of the US economy, this slowdown makes another Fed rate cut more likely and nudges markets toward dovish expectations. And with the government shutdown delaying official data, private reports like ADP carry extra weight and can swing markets more than usual.

Bureau of Labor Statistics’ Employment Situation Report (ESR)

The US government shutdown has put key economic data on hold. September’s nonfarm payrolls report, a closely watched measure of job growth, won’t be released until the government reopens and agencies get back to normal operations.

Summary

The latest JOLTS and ADP reports show the US labour market is losing steam. Job openings are flattening, private payrolls are slipping, and confidence in the job market is fading. While companies aren’t cutting staff en masse, the pace of hiring is clearly slowing. For the Fed, that provides more cover to ease interest rates, but for investors it signals an economy that’s shifting down a gear. The US government shutdown won’t help the labour situation either – the shutdown temporarily slows the economy, and the longer it drags on, the harder it is for growth to fully bounce back.

American Market Volatility

The CBOE Volatility Index (VIX), often called the market’s “fear gauge,” showed some jitters this past week but stayed within a relatively calm range. It opened at 15.85, bounced between 16 and 17 over the following days, and closed the week at 16.65. The only real flare-up came the morning after the US government shutdown, when the VIX briefly jumped above 17.2 before quickly easing back below 17 once regular trading began.

Think of the VIX as a market mood ring. When it’s in the 12 to 20 range, investors are generally calm and steady. Once it pushes higher, it’s a sign traders are growing uneasy and bracing for bumpier days ahead. A rising VIX doesn’t always mean panic, but it does mean caution is creeping back into the market.

Weekly Market and Portfolio Review

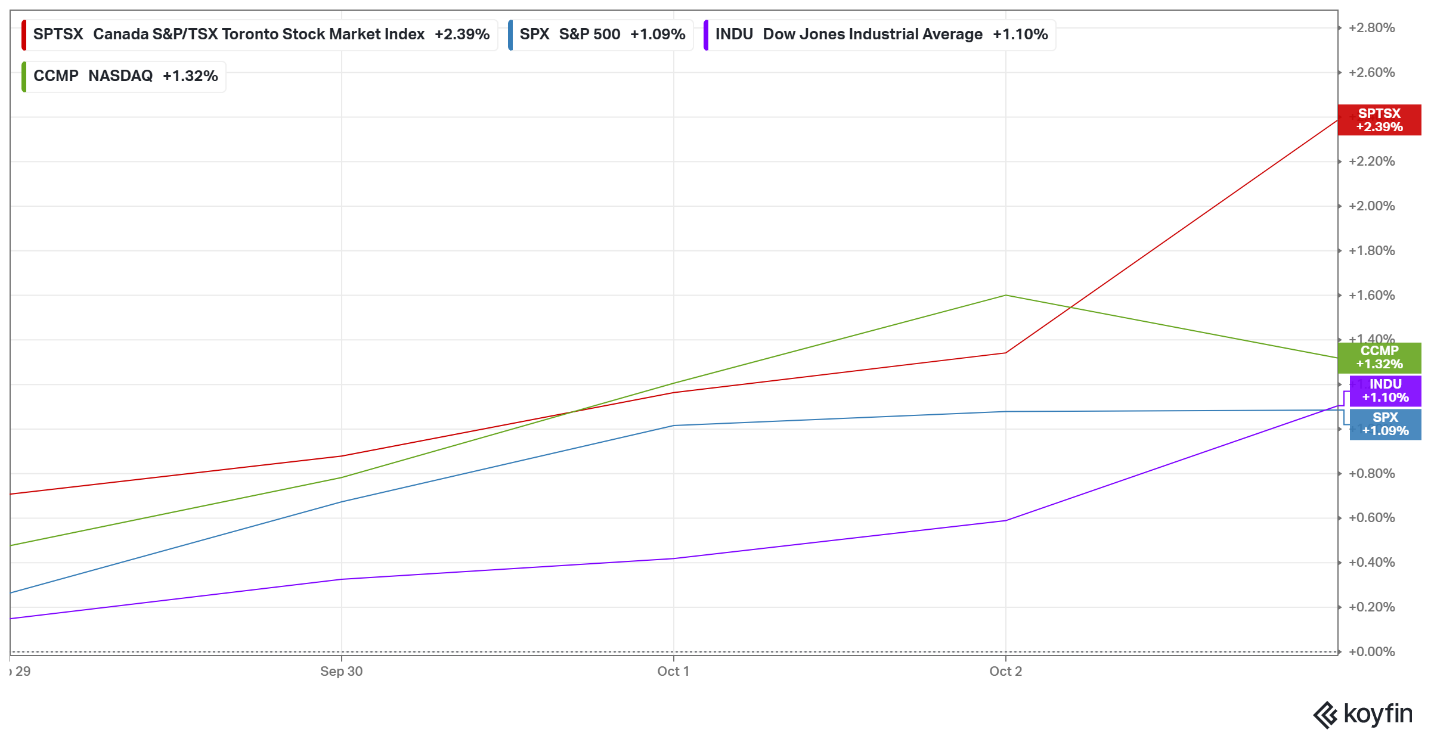

For the week, the TSX (SPTSX) surged 2.4%, the S&P 500 (SPX) rose 1.1%, the DJIA (INDU) grew 1.1% and the Nasdaq (CCMP) climbed 1.3%.

| Index | Weekly Streak |

| TSX: | 1 – week winning streak |

| S&P: | 1 – week winning streak |

| DJIA: | 1 – week winning streak |

| Nasdaq: | 1 – week winning streak |

![]() After stumbling the week before, the markets bounced back in a big way, with all major indexes kicking off new weekly winning streaks. The Toronto Stock Exchange Composite Index (TSX) stretched its win streak to six days, setting multiple record highs along the way. South of the border, the S&P 500 (S&P), Dow Jones Industrial Average (DJIA), and Nasdaq Composite Index (Nasdaq) all set record highs multiple times, with the S&P crossing the 6,700 mark for the first time and the DJIA briefly topping 47,000 for the first time ever before falling back.

After stumbling the week before, the markets bounced back in a big way, with all major indexes kicking off new weekly winning streaks. The Toronto Stock Exchange Composite Index (TSX) stretched its win streak to six days, setting multiple record highs along the way. South of the border, the S&P 500 (S&P), Dow Jones Industrial Average (DJIA), and Nasdaq Composite Index (Nasdaq) all set record highs multiple times, with the S&P crossing the 6,700 mark for the first time and the DJIA briefly topping 47,000 for the first time ever before falling back.

The US government shutdown that began on October 1 initially cast a shadow, with economists warning it could drain billions from the economy each week. One immediate casualty was the Bureau of Labor Statistics, which had to delay its closely watched September jobs report. With no nonfarm payrolls data, investors leaned on private reports like ADP’s, which showed a cooling labour market and strengthened expectations of another Fed rate cut.

Trade tensions resurfaced after President Trump announced new tariffs – a 10% duty on softwood lumber and a 25% levy on kitchen cabinets, vanities, and upholstered wood products. For Canadian exporters, the pain is acute: combined duties on lumber shipments now top 45%. Trump also reignited the threat of 100% tariffs on foreign-made movies, keeping markets on edge.

Balancing out the political noise was a rally in artificial intelligence (AI) stocks, which gave markets a powerful tailwind. Investors piled into chipmakers and AI infrastructure companies after news that the private company OpenAI was valued at roughly $500 billion. The eye-popping figure reignited excitement around AI’s growth potential, sending the tech-heavy Nasdaq higher and lifting the broader S&P.

In Canada, gold’s surge to record highs lifted resource and mining stocks, giving the TSX a boost. Resilient commodity prices and strong corporate earnings added support, even as manufacturing data painted a weaker picture with falling output, new orders, and exports. The latest Purchasing Managers’ Index (PMI) signaled a cooling labour market and the steepest drop in backlogs in five years. While that points to a slowing economy, it also strengthens the case for the BoC to cut rates at its next meeting later this month.

All told, booming AI enthusiasm and firm commodity prices kept Canadian markets moving higher, but trade risks, weak manufacturing, and political uncertainty from the US shutdown tempered the optimism.

Overall, it was an encouraging rebound for markets, even with Washington’s gridlock hanging over investors. For now, the shutdown clouds the near-term picture, but the longer-term story is still being driven by AI optimism and strong commodities.

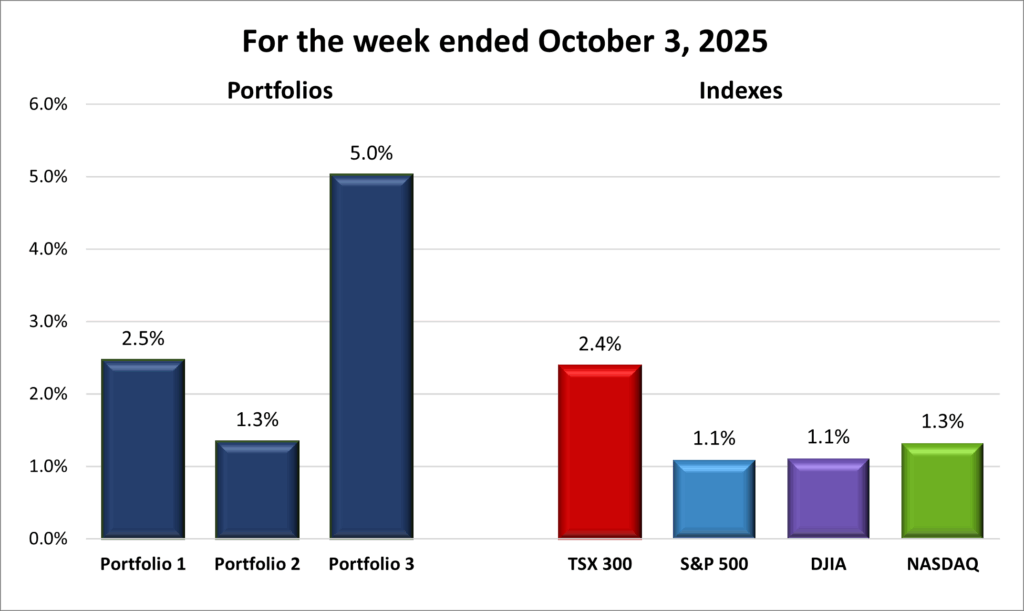

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week winning streak |

| Portfolio 2: | 9 – week winning streak |

| Portfolio 3: | 1 – week winning streak |

![]() After last week’s mixed results, when only Portfolio 2 managed a slim gain, it was great to see all three portfolios finish in the green. Even better, the gains came from across the board rather than one or two stocks carrying the load. And as a bonus, Portfolios 1 and 2 outperformed the strongest of the major indexes.

After last week’s mixed results, when only Portfolio 2 managed a slim gain, it was great to see all three portfolios finish in the green. Even better, the gains came from across the board rather than one or two stocks carrying the load. And as a bonus, Portfolios 1 and 2 outperformed the strongest of the major indexes.

Portfolio 1 got back on track with a 2.5% gain. About 64% of its holdings moved higher, led by a 12% jump in Navitas Semiconductor (NASD: NVTS) and a 13% surge in Shopify (TSE: SHOP), sending it to a new high. TD Bank (TSE: TD) and Nvidia (NASD: NVDA) also reached record levels. The main setback came from Carnival Corporation (NYSE: CCL), which slipped 11%.

Portfolio 2 didn’t post the biggest gain, rising 1.3%, but it outpaced both the S&P and the DJIA and boasted the broadest participation – with 70% of holdings moving higher. Take-Two Interactive (NASD: TTWO) set a fresh high, while lower oil prices held back the portfolio’s energy names, limiting the upside. ☹

Portfolio 3 led the way with a strong 5.0% gain – more than double the TSX, the week’s best-performing index. Like the others, breadth was solid, with 63% of holdings moving higher, but a couple of standouts stole the show. Lithium Americas followed last week’s 103% surge with another 43% jump, while Vertiv Holdings (NYSE: VRT) climbed 12% to a new high. To top it off, five of the six largest holdings ended the week higher, adding extra fuel to the advance. 😊

All in all, it was a week to smile about – strong gains, broad participation, and fresh highs across all three portfolios. With AI excitement and solid commodities backing the markets, here’s hoping this momentum carries into next week and beyond! 😊

Companies on the Radar

This past week, two small-cap (market value under US$2 billion), owner/operator companies – which tend to outperform over the long term – caught my attention: Napco Security Technologies, Inc. (NASD: NSSC) and XPEL, Inc. (NASD: XPEL).

This past week, two small-cap (market value under US$2 billion), owner/operator companies – which tend to outperform over the long term – caught my attention: Napco Security Technologies, Inc. (NASD: NSSC) and XPEL, Inc. (NASD: XPEL).

Napco provides electronic locks, intrusion and fire alarms, access control systems, and video surveillance solutions for homes, businesses, and institutions. With a broad network of distributors and installers, growing recurring service revenue, and smart home integrations, the company has several avenues for growth. Rising concerns around safety and security give Napco a strong tailwind.

Founder and CEO Richard L. Soloway has guided Napco since its inception. Aside from a 2023 accounting hiccup – where inventory and cost-accounting errors overstated profits and temporarily knocked the stock price down – the company has steadily grown revenues and maintained strong gross margins, supported by a solid balance sheet. Napco has since strengthened internal controls and addressed these issues.

Despite short-term uncertainty, Napco’s market position, recurring revenue focus, and broad product portfolio make it a company worth taking a closer look at. With demand for security continuing to rise, its long-term prospects remain compelling.

XPEL produces high-quality protective films, coatings, and related products, primarily for cars but increasingly for architectural and other applications – think paint protection film (PPF), window tint, and ceramic coatings. The company sells through multiple channels – authorized installers, dealers, direct online, company-owned centres, and franchisees – giving it both reach and control.

Demand for XPEL’s products is growing alongside EV adoption and the rising demand for car-detailing. Strong partnerships with automakers like Tesla, Rivian, Porsche, and Jaguar Land Rover highlight its market influence. In July, Tesla expanded its collaboration by offering XPEL PPF on the Model 3 and Y, underscoring the company’s growing role in EVs. Beyond automotive, XPEL is branching into architectural films and coatings, opening additional growth opportunities.

XPEL is led by co-founder and CEO Ryan Pape, who transformed the company from a $1 million market cap to over $2 billion, delivering an impressive return on investment. Under Pape’s leadership, XPEL has expanded its products and global presence, becoming a leader in the automotive protective film industry. With multiple levers for expansion, XPEL is definitely a company to I want to learn more about.

With these two additions joining the four holdovers from last week (listed below), my radar list now features six intriguing companies.

- Mainstreet Equity Corp. (TSE: MEQ): a Calgary-based real estate company focused on mid-market apartment buildings – typically under 100 units – across Western Canada. It buys underperforming properties at below-market prices, renovates them, and increases rental income through improved operations. With strong demand for rental housing, a repeatable value-add strategy, and a solid balance sheet, Mainstreet offers a compelling mix of income and growth. Shares currently trade below net asset value, giving investors a margin of safety alongside steady cash flow and long-term upside.

- Tornado Infrastructure Equipment Ltd. (TSEV: TGH): a small Canadian industrial company that designs, builds, and sells hydrovac trucks across North America, while also generating recurring revenue through rentals, parts, and maintenance – making it more than just a pure equipment play.

- Arista Networks (NYSE: ANET): an American company that designs and sells advanced networking hardware and software, with a focus on high-speed, low-latency switches for its key markets: data centres, AI, cloud computing, and financial trading. The company has been riding the AI tailwind with solid demand from its core markets, especially in AI and cloud data centres. It also has a hefty share buyback program and increasing investments from some of the top institutional investment companies.

- Corning Incorporated (NYSE: GLW): a large cap American company that is a leader in specialty glass, optical fiber, environmental technology, life sciences, and other specialty glasses. They have been the supplier of the glass used in Apple’s iPhones since 2007, and they are riding the tailwind of an AI-driven fiber optic boom.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated October 3, 2025.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!