Fractional shares….

The big news that impacted us investors came out of the USA this week, causing share prices to tumble.

As expected, the US Federal Reserve (Fed) raised the US benchmark interest rate by 0.75% this week. This was the third straight 0.75% increase. What was unexpected was the Fed’s vow to crush inflation, signaling further aggressive increases were coming. Analysts are speculating the US interest rates could rise to 4.4% by the end of this year (June projections were for 3.4%), with the potential to reach 4.6% in 2023. At this point, it seems clear the Fed is not going to ease off on rate hikes in the near term, and with rates at these levels, the US economy cannot help but slow down as businesses must slow their growth plans to pay off debt.

For us investors, that is not good news. After a summer rally that lifted the S&P 500 Index out of a bear market (down more than 20% from its recent highs), it has slid back into a bear market. The technology heavy Nasdaq Composite Index is well into bear territory, down over 30%, while the Dow Jones Industrial Average has fallen 18%, barely avoiding bear territory. But it could still get worse, with some analysts predicting the S&P could fall 40% by the end of 2023. If that projection is correct, we are only at the halfway point. For now, the market will likely be extremely sensitive to any comments from the Fed or upcoming data.

Statistics Canada revealed Canada’s inflation rate was down for the second month in a row in August, at an annualized rate of 7.0% compared to July’s 7.6%. The rate decelerated by even more than analysts’ predictions of 7.3%, mainly because of lower gasoline prices during August. If gasoline is removed from the mix, the August inflation rate was 6.3 % in the last year, compared to 6.6% in July. The Bank of Canada’s (BoC) Core CPI (excludes food and energy prices) declined to 5.8% from 6.1% in July. This too came in below analysts’ expectations of 6%, suggesting the interest rate increases by the BoC are having an impact.

However, the BoC stated “We will continue to take whatever actions are necessary to restore price stability for households and businesses and to maintain Canadians’ confidence that we can deliver on our mandate of bringing inflation back to 2%.”

Inflation rates in Canada and the US are going in the opposite direction. While the Fed has indicated they will continue to be aggressive in their interest rate hikes to battle increasing inflation in the US, the BoC might be able to back off their aggressive rate hikes since inflation appears to be slowing in Canada. Hopefully, with these lower-than-expected numbers, the BoC will ease off the pedal of interest rate hikes at their next planned increase in October.

Higher interest rates and faltering economies are not limited to North America. Around the world, fears are growing that the various central banks’ plans of raising interest rates to wrestle inflation down to their 2% target will drag major economies into recession. Below are a few of the latest interest rate hikes by national central banks:

In their fight to bring down Britain’s 9.9% inflation rate, the Bank of England raised their benchmark interest rate by 0.5%, bringing it to 2.25%.

Norges Bank, Norway’s central bank, raised its interest rate by 0.5% to 2.25%.

The Reserve Bank of Australia raised their interest rate by 0.5% for a fifth straight month, bringing it to 2.35%, a seven year high.

Sweden’s central bank, Riksbank, raised their interest rate by an unexpected 1%, bringing their national interest rate to 1.75% as it battles surging inflation.

The Swiss National Bank raised its rate by 0.75%, lifting it from negative 0.25% to 0.5%. And so ends the negative rates experiment.

In Europe, where inflation hit 9.1% in August, the European Central Bank delivered its largest-ever increase with a 0.75% hike, impacting all 19 countries that use the euro.

Brazil’s central bank, Banco Central do Brasil, voted not to make an any changes to their benchmark interest rate. Now, before you start asking why Brazil did not raise their interest rate like many of the other countries, be aware their interest currently sits at 13.75%. And we think our rates are high!

Ethereum is officially a proof-of-stake blockchain. One of the top achievements was the elimination of Ethereum’s dependence on power-intensive GPUs. Ethereum is down 64% year to date. If you invested in Ethereum, like I did, you are hoping that the “Merge” will renew enthusiasm for the cryptocurrency and send it up to set new highs.

While interest rates around the world were rising, unfortunately the same cannot be said about the North American stock markets this week. Let’s take a look at what happened in the markets and the Portfolios this past week….

Weekly Market Review

Monday: All four major North American Indexes ended the day higher as investors await the US Federal Reserve’s (Fed) upcoming US interest rate hike. In Canada, investors in Canadian equities are waiting for Canada’s Consumer Price Index (CPI) data, due Tuesday, to find clues on the Bank of Canada’s (BoC) next Canadian interest rate hike due October 26. In the marketplace, the Toronto Stock Exchange Composite Index (TSX) rose on the strength of higher shares prices for Energy and Basic Materials (natural resources and Fertilizers) companies.

South of the 49th in the US, the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) were up and down all day before ending the session in the black. Trading was light as investors have adopted a wait and see approach ahead of this week’s US interest rate hike. Analysts and investors expect a 0.75% hike, with an outside chance of a 1.0% hike, and are also looking for signs of how aggressive the Fed will likely be for future rate hikes. Given the fear of the upcoming rate hike, it was generally a good day in the US markets as ten of eleven S&P sectors ended in the black. Healthcare was the lone laggard as shares in vaccine makers slipped on President Bidens declaration “the pandemic is over.”

Tuesday: The Indexes drifted lower as investors continued to hold their breath ahead the Fed’s interest rate hike announcement. In Canada, the Canadian CPI indicated the inflation rate dropped from 7.6% in July to 7.0% for August, below analysts estimates of 7.3%. On the Toronto Stock Exchange, the TSX dipped over concerns aggressive interest rate hikes could send the global economy into downturn which would lower demand for drive commodities (oil, resources, etc.) causing their current prices to fall.

In the US, once again trading was lower in the US markets as investors await tomorrow’s announcement by the Fed. It is anticipated the Fed will raise the interest rate by 0.75%. Across the New York Stock Exchange and the Nasdaq Exchange, all S&P sectors ended the session lower.

Wednesday: The big story in investing today was the Fed raised US interest rates by 0.75% for a third consecutive time, bringing the US benchmark rate to 3.25%. They also signaled additional similar sized rate hikes were likely. When the news of the interest rate increase reached the markets, all four Indexes, which had been slightly higher throughout the day, plunged into negative territory.

In Canada, declines in the Energy sector and the Consumer Cyclical led the TSX lower. The Telecommunications sector was the only Canadian sector to end the day higher.

In the US, it was a broad-based sell off as all eleven S&P sectors reacted poorly to the news additional hawkish interest rate hikes were likely. At the end of the day, all three Indexes slumped, and the S&P slid back into a bear market (a drop of 20% or more from the all-time high value).

Thursday: Tremors continue to ripple through the markets after yesterday’s announcement by the Fed. Not so much the 0.75% increase, but the pace and aggressiveness of future interest rate hikes to get inflation under control in the US.

In Canada, the TSX ended lower as falling share prices in the Technology and Healthcare sectors overwhelmed gains made by the Energy and Basic Materials sectors . Meanwhile in the US, all three major American Indexes ended lower, drawn down by Technology sector companies and other high growth companies. Healthcare was the only sector of the eleven to squeak out a gain, ending 0.01% higher.

Friday: With thoughts of a global recession dancing in their heads, investors sold, sold, sold, and asked questions later. It was tough day in the markets as all four major North American Indexes dropped sharply, with all sectors in both countries losing ground. In Canada, the TSX dropped sharply thanks to a plunge in the price of oil, which led to a 6% drop in Canada’s Energy sector. A recession would lead to less demand for energy, which is why oil sold off.

In the US, the S&P Energy sector had a similar trajectory as the Canadian Energy sector, plunging 6.8%. The DJIA established a new low for 2022. Despite interest sensitive technology and other growth-oriented companies being scorned by investors, the S&P Technology sector was the second-best performing sector, ‘only’ falling 1.53%. I would not have guessed that.

Let us hope next week is significantly better.

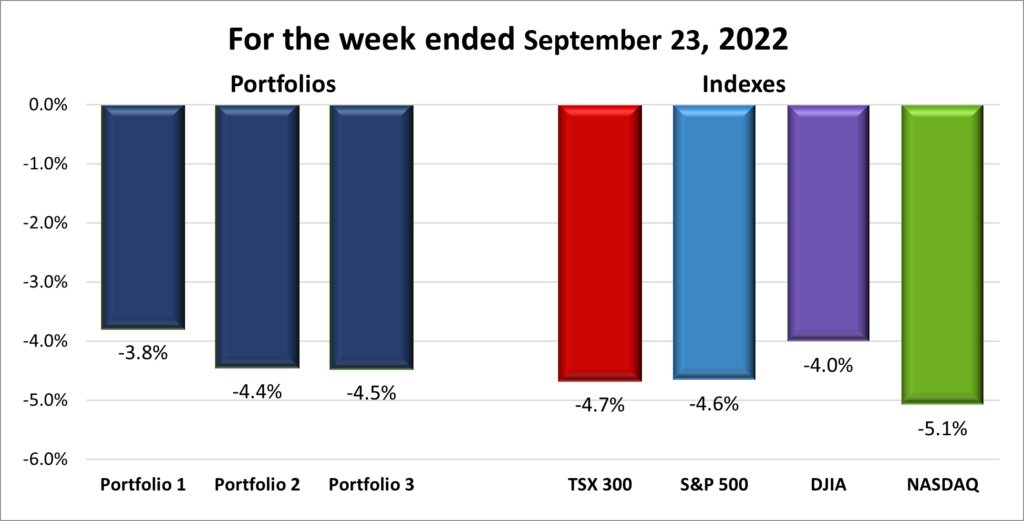

For the week, the TSX dropped 4.7%, the S&P 500 lost 4.6%, the Dow sank 4.0% and the Nasdaq plunged 5.1%.

Weekly Portfolio Review

All four major North American Indexes have dropped in five out of the last six weeks, with interest sensitive growth and technology stocks getting hit the hardest thanks to the Fed’s interest rate-hiking. If you are wondering why the Portfolios are doing so poorly in 2022, consider that the S&P and Nasdaq are both in bear markets (down more than 20% from their respective recent highs), the TSX and DJIA are both in market corrections (down more than 10% from its recent highs), and most importantly for the three Portfolios, the S&P tech sector has fallen 28% since the start of the year. Ouch! ☹ And there are no signs of relief around the corner.

Since it was a bad week for the Indexes, and therefore the Portfolios, the only silver lining is other than the DJIA, all three Portfolios did better than the Indexes. Barely, I admit, but I am trying to take a positive out of this week. 😊

Companies on the Radar

With the markets falling this week, I’m giving myself a pat on the back for not falling for the summer rally, also known as a bear market rally, or a bear trap, and jumping in to buy Amazon (NASD:AMZN) or Ferrari (NYSE:RACE) when the prices were moving upward during July and August. With prices dropping these two companies move to the front of the radar. The challenge now is how much lower will the share prices fall? WESCO International (NYSE:WCC), XPEL, Inc. (NASD:XPEL) and Brookfield Select Opportunities (TSX:BSO.UN) are on the next level.

As for copper companies, I had thought with the huge demand for copper in the production of batteries for electric vehicles that the earnings and share prices of copper miners would be drifting higher. Unfortunately, copper prices, and by extension, copper mining companies are not doing as well as I had thought.

After doing a bit of due diligence on copper, I discovered the price of copper is considered to provide a consistent barometer of economic health, since changes to the price of copper can suggest global growth or an upcoming recession. Given the price of the metal has fallen considerably since March highs, and the deteriorating state of the economy, that relationship appears intact in this instance. Given the current downward trend of the global economy and copper prices, I am putting copper companies on the outer rings of my radar.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended September 23, 2022: DOWN ![]()

- General Motors’ (NYSE:GM) electric vehicle unit Cruise is currently the only fully licensed, fully autonomous electric vehicle ride service. The service operates only during nighttime hours, in limited areas of San Francisco. Cruise operates up to 70 autonomous vehicles nightly and has been charging for rides since June 2022. Management recently announced plans to expand Cruise’s robotaxi service to Austin, Texas and Phoenix, Arizona by the end of the year.

GM also announced Hertz Rent a Car plans to purchase 175,000 GM electric vehicles over the next five years as part of Hertz’s efforts to green.

- Tesla (NASD:TSLA) announced the completion of their capacity expansion at their Shanghai Gigafactory. The expansion should enable Tesla to produce up to 22,000 units per week at their Chinese factory.

In a different type of recall, Tesla is recalling over 1 million vehicles in the US thanks to a faulty window reversal system that does not reverse when it encounters an object while being raised. Whereas in the past recalls involved bringing your vehicle into a dealer to make the repair, Tesla has said they will perform an over the air software update to resolve the problem. Assuming this works as planned, owners will not have to spend time taking their vehicles in for the maintenance and Tesla will save considerable labour expenses with a software update rather than mechanical repairs. If all goes well, I see this as a win-win for both consumers and the company. - Apple (NASD:AAPL) announced they will be raising prices in Europe and Asia for apps and in-app purchases. The changes are to adjust for currency fluctuations. Nothing to see here.

Apple won a bidding war to take over sponsorship of the NFL Super Bowl Halftime Show, starting in February 2023. Apple will use this promote their products, naturally, to one of the largest single show audiences, and as an opportunity to highlight their capabilities as Apple attempts to become the host for the NFL Sunday Ticket that allows fans to view every Sunday game.

- Nvidia (NASD:NVDA) announced a new chip optimized for gaming that will use Artificial Intelligence to enhance graphics capabilities. The new chips will be named after one of the first women in what would become computer science. Ada Lovelace was a British mathematician in the 19th century.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended September 23, 2022: DOWN ![]()

- Take-Two Interactive (NASD:TTWO) acknowledged they had been hacked. Initially it was only some early footage of their upcoming Grand Theft Auto VI game that was leaked. However, it turns out Take-Two’s Help Desk platform was also hacked. The company said the hack will have no impact on the development of Grand Theft Auto VI. We shall see.

- Canadian energy company Pieridae Energy (TSX:PEA) is proposing to build a natural gas terminal on Canada’s Atlantic coast to ship the gas to Europe. The catch, they have asked the Canadian government to ensure pipeline builder/operator TC Energy (TSX:TRP) will be able to acquire the necessary permits in a timely fashion, and not get disrupted by legal challenges or protesters. They are waiting for a response from the federal government. I guess they did not hear the government say there was no business case to ship natural gas to Europe. 😊

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Alimentation Couche-Tard Inc (TSX:ATD)

Dream Industrial Real Estate Investment Trust (TSX:DIR.UN) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended September 23, 2022: DOWN ![]()

- Last week I noted Shopify’s (TSX:SHOP) new employee compensation system. This week Royal Bank analysts suggested once Shopify fine tunes their compensation system, they could roll it out to their merchants (also known as their customers). The theory is this would make it easier for merchants to attract employees and grow their business. This would not be the first time Shopify built an in-house system and rolled it out to the public. Afterall, that is how Shopify went from a snowboard company to an e-commerce powerhouse. 😊

- TD Bank (TSX:TD) announced a contract extension with US retailer Target Corporation (NYSE:TGT) to remain the sole issuer of Target’s consumer credit cards.

TD is also investing C$ 10 million with the Boreal Wildlands Carbon Project in northern Ontario to protect 1,500 square kilometres of boreal forest. In return, TD will receive carbon offsets generated from the project. - Brookfield Asset Management (TSX:BAM.A) controlled NTS, a Brazilian natural gas pipeline operator, announced plans to invest $2.4 billion over the next eight years to build out its pipeline network and natural gas storage facilities. It appears NTS sees the business case for building out their natural gas capabilities. 😊

In other Brookfield news, the company’s board of Directors approved plans to divide into two publicly traded companies. Brookfield Asset Management will be renamed Brookfield Corp following the split, and will own 75% of the asset management business, called the Manager, with shareholders owning the remaining 25% distributed by the board.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

No quarterly reports this past week.