Items that may only interest or educate me ….

Canadian economic news, US economic news, Better to be lucky …

Canadian economic news

Statistics Canada showed that the nation’s economy continued to grow in the first quarter, rising by 3.1%, which is well above the anticipated 2.5% increase. On a monthly basis, the economy remained flat at 0% in March, surpassing estimates of a 0.1% decline. Early projections for April indicate a 0.2% growth in the economy. Canadian consumers have continued their spending habits in the first part of 2023, particularly on new vehicles, dining, and vacations.

Consumer spending plays a crucial role in the Canadian economy, but it also contributes to upward pressure on inflation. To address inflation, the Bank of Canada (BoC) raises the benchmark interest rate, thereby increasing the cost of borrowing. Consequently, consumers allocate more of their funds toward debt obligations, leaving less money available for other expenses. The underlying theory is that if there is less money for spending, demand will moderate, leading to a decrease in inflation.

Given the better-than-projected economic growth and the persistent high inflation, there is an increased likelihood that the BoC will raise the benchmark interest rate. However, that does not mean another increase will occur at their next meeting. If there is an increase, it may occur as early as next week or sometime this summer.

US economic news

The non-farm payrolls data for May indicated a robust increase in job numbers, surpassing expectations and pointing to a strong labor market. The gain of 339,000 jobs exceeded the forecast of 195,000 and outperformed the previous month’s increase. However, it is important to note that the unemployment rate also rose slightly from the previous month.

Despite the strong job numbers, wage growth did not accelerate at the same pace, which suggests a potential “soft landing” scenario where the economy can sustain growth without triggering excessive inflation. This dynamic has led investors to believe that the Federal Reserve (Fed) may pause their rate hike cycle and maintain the current benchmark interest rate, as they seek to balance economic growth with inflation concerns.

On the consumer front, the decline in the Consumer Confidence Index to a six-month low of 102.3 from 103.7 (out of 200) indicates lingering uncertainty among Americans about the economy. Factors such as the recently concluded debt ceiling negotiations and the upcoming interest rate announcement by the Fed are likely contributing to this uncertainty. However, it is noteworthy that consumer confidence remains slightly higher than the 99.1 anticipated by analysts, suggesting a moderate level of consumer optimism.

Better to be lucky

Back in 2017-2018, “blockchain technology” companies were the darlings of the North American stock markets, but they were soon replaced by “metaverse” companies in 2020-2021. Currently, artificial intelligence (AI) is the latest trend in the stock markets. Although I missed out on the blockchain surge, I managed to invest in Nvidia (NASD: NVDA) because reports indicated that their graphic processor units (GPUs) were well-suited for the computing power demands of blockchain technologies, cloud computing, and the emerging metaverse. However, I regretfully chased after Unity Software (NYSE: U) to capitalize on the metaverse. ☹

Fortunately, with the emergence of AI, I have investments in the right companies at the right time. Both Nvidia and Microsoft (NASD: MSFT) were purchased in 2020, before the AI craze, and are currently market leaders in AI technology. In 2022, during a bear market for technology companies (a decline of 20+% over an extended period), I acquired Alphabet (NASD: GOOGL) and Amazon (NASD: AMZN). Alphabet’s Google, with their Bard AI product, is likely positioned as the third major player in the race to capture AI market share. While Amazon may not currently lead in AI, according to their annual letter to shareholders, AI is core to every area of their business. They are leveraging AI internally and developing AI tools for their Amazon Web Services (AWS) customers to integrate into their own offerings.

As Microsoft and Google compete for AI leadership, Nvidia is content to be at the forefront of significant technological mega-trends. Amazon’s position in the AI race is not as clear, but I anticipate they will be among the top five AI companies within a year. Having four of the top five AI-related companies is largely luck, especially since these investments were made prior to AI becoming the “hot thing.” Sometimes its better to be lucky rather than good. 😊

A new oil benchmark

The world’s oil benchmark, Brent crude, is about to acquire a touch of Texas flavor. Brent crude, formally known as Dated Brent, is the most widely traded oil benchmark worldwide. Initially, it was based solely on oil from the Brent oilfield off the coast of Scotland. However, in the 1980s, due to falling supplies, four other North Sea oilfields were included in the formula that determined the price for Brent crude.

Previously, Brent crude consisted of five North Sea oil fields’ grades: Brent, Forties, Oseberg, Ekofisk, and Troll. However, in early May, West Texas Intermediate (WTI) Midland crude, produced in the oil fields of Texas, became part of the Brent benchmark. This change is considered the most significant overhaul of the measure since the 1980s.

There are two primary reasons for including WTI Midland in the Brent basket. Firstly, the United States has emerged as one of the top oil producers globally, and the addition of WTI Midland to the Brent index acknowledges the growing influence of the US in the global energy market. Secondly, the supply from the North Sea oil fields has been declining for a few years, and incorporating WTI Midland enhances the liquidity of the Brent benchmark.

Now, let’s see what happened this past week….

Weekly Market Review

Monday: The American markets were closed for Memorial Day. Over the weekend, US negotiators struck a deal to prevent the US defaulting on its debt.

In Canada, the Toronto Stock Exchange Composite Index (TSX) ended higher on rising oil prices that were a result of news a deal had been struck that would prevent the US from defaulting on its debt. Technology and Consumer Cyclicals led the Canadian sectors higher, while Healthcare was the only sector to decline.

Tuesday: Concerns about the viability of the US debt ceiling deal cooled the major North American indexes. The TSX and the Dow Jones Industrial Average (DJIA) both ended lower, the S&P 500 Index (S&P) was flat, while the Nasdaq Composite Index (Nasdaq) was the only index to advance. The price of oil plunged on uncertainty over the US debt deal and mixed signals from major oil producers regarding the supply outlook for the summer.

In Canada, the resource heavy TSX closed at a two-month low thanks to the fall in oil prices. In trading, all Canadian sectors were down. The Industrials and Utilities dropped the least, while Energy and Technology had the biggest drops.

In the US, the Nasdaq extended last week’s Nvidia and AI fuelled rally. Today’s surge in Nvidia pushed the company into the US$ 1 trillion market cap club. Lost in the debt negotiations drama and looming on the horizon, is the upcoming Federal Reserve (Fed) meeting where the Fed members will decide whether to raise the US benchmark interest rate or leave it at its current 5.25%. In trading, Consumer Cyclicals, Technology and Financials were the only sectors to end higher, while Energy and Consumer Staples suffered the biggest drops.

Wednesday: All four indexes ended lower as investors worried about the US debt ceiling deal ahead of an evening vote in the US House of Representatives. Also weighing on the markets, concerns about interest rate hikes in Canada and the US, and bumps in China’s economy.

In Canada, falling oil prices caused by expectations of lower demand from China added another layer of downward pressure on the TSX, sending it to its lowest level in two months. In trading on Bay Street, Technology and Basic Materials (miners and fertilizer manufacturers) ended higher, while Consumer Cyclicals and Energy had the biggest falls.

In the US, an unexpected increase in job openings, coupled with hawkish comments from Fed officials has investors concerned there will be another interest rate hike. In trading on Wall Street, Utilities, Healthcare and Telecommunications Services were the only American sectors to advance. Leading the remaining sectors lower were Energy and Industrials.

Thursday: Two bits of good news sent all four indexes surging higher today. First, the deal to raise the US debt ceiling was approved by the House of Representatives last night. The other bit was indications from Fed officials suggested a potential pause in interest-rate hikes. Oil prices also rose on news of the passage of the debt ceiling bill.

In Canada, the TSX responded positively to the news out of US about the progress of the debt ceiling deal. Basic Materials and Energy were the top gainers of the Canadian sectors, while Consumer Staples and Utilities dropped the most.

In the US, in addition to the debt deal moving through Congress, signs of slowing inflation led investors to believe the Fed would pass on an interest rate hike at their next meeting. Basic Materials and Energy led a broad-based advance of the American sectors, while Utilities was the only sector not to advance.

Friday: All four indexes soared after the US debt deal was passed by the US Senate, putting it a presidential signature away from being a done deal. Progress of the debt ceiling bill and the latest jobs report showing a strong US economy gave a much-needed boost to the price of oil.

In Canada, the TSX had its best day since November 2022 thanks to the rise in the price of oil and a rally in financial stocks. It was a broad-based rally in the Canadian sectors that saw all of them end higher. Leading the way were Energy and Consumer Cyclicals, while Telecommunications Services and Basic Materials brought up the rear.

In the US, diminished fears of a debt default and a strong jobs report sent the three American indexes soaring, with the S&P closing at its highest point since August 2022. The jobs report indicated slowing wage growth and higher unemployment, had investors hoping that would provide the Fed a reason to pause their rate hike. In trading in the American sectors, Basic Materials and Energy had the biggest gains while Telecommunications Services was the only sector to drop.

Weekly Market and Portfolio Review

For the week, the TSX (SPTSX) added 0.5%, the S&P 500 (SPX) added 1.8%, the DJIA (INDU) jumped 2.0% and the surged (CCMP) rose 2.0%.

![]()

As you can see from the chart above, an end of the week surge lifted all four indexes into the money this past week. Driving the market this past week was the progress of the US debt ceiling negotiations. Once the deal passed through the House of Representatives on Wednesday the indexes surged, followed by another surge Friday when it passed through the Senate. Even the rising tide of optimism created by the US debt ceiling deal lifted the TSX into positive territory for the week. That was the first weekly gain for the TSX in five weeks.

![]()

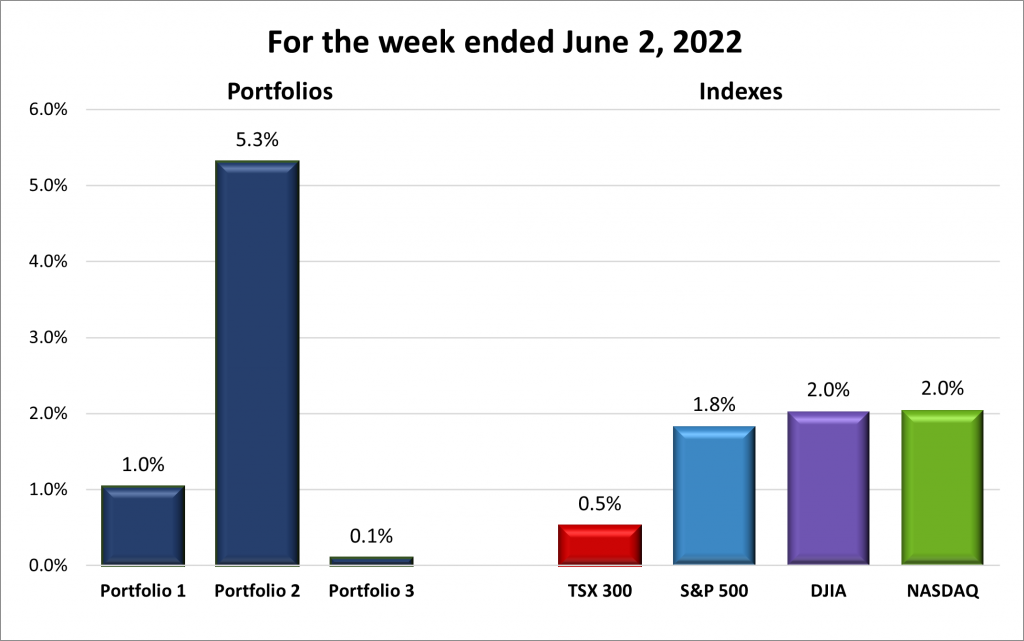

The end-of-week rally propelled all three portfolios into positive territory. As depicted in the chart below, Portfolio 2 emerged as the clear winner, primarily due to a substantial 28% gain from MongoDB (NASD: MDB). Portfolio 1 benefited from its significant technology holdings, as well as the growth companies like Celsius Holdings (NASD: CELH). On the other hand, Portfolio 3 was somewhat disappointing, despite the overall upward movement in the indexes. The gains in technology companies were offset by declines in a few other stocks, particularly a pullback in Shopify (TSX: SHOP) as investors, including myself, took profits following its recent surge.

However, considering the portfolios’ consistent decline last year, any week where all three portfolios experience growth is considered a positive outcome. 😊

Monthly Portfolio Review

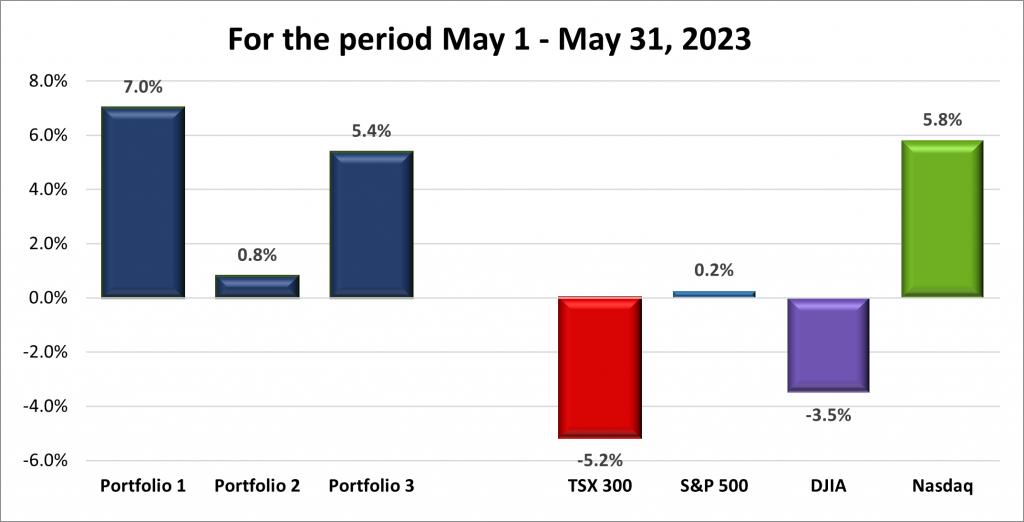

For the month, the TSX (SPTSX) fell 5.2%%, the S&P 500 (SPX) nudged up 0.2%, the DJIA (INDU) dropped 3.5% and the Nasdaq (CCMP) surged 5.8%.

![]()

Aside from the Nasdaq, May was not a favorable month for the four major North American indexes. The Nasdaq outperformed the others, as indicated in the chart above. This was primarily driven by the strong performance of technology stocks, particularly semiconductor companies, which surged on the excitement surrounding artificial intelligence. The positive momentum in big technology stocks on the Nasdaq also had a positive impact on the S&P index. However, the industrial-focused companies that make up the 30-company DJIA dragged it into negative territory for May and the year.

In Canada, the TSX experienced its worst monthly performance in 2023, largely due to declining commodity prices, such as oil and copper, as well as disappointing earnings from banks.

![]()

In terms of the portfolios, May proved to be a positive month, with all three portfolios experiencing growth. Portfolio 1 saw significant growth, primarily driven by a surge in its mega-cap companies. Portfolio 2 managed to achieve positive returns, as its American technology companies were able to overcome the drag of Canadian bank stocks in the portfolio. Portfolio 3 benefited from the performance of Shopify and its other American technology companies, contributing to its overall growth.

Companies on the Radar

Given the uncertainty in the markets, including the US debt ceiling and interest rates in both Canada and the US, I have decided to remain on the sidelines unless an exceptional opportunity presents itself. I recall the costly lesson from late 2021 when I ignored signs of a slowing economy and watched the value of the portfolios drop significantly in 2022. Having learned from that experience, I plan to wait for the resolution of the US debt ceiling issue before making any new investment decisions. As of now, my radar list of potential investment opportunities remains unchanged:

- Intact Financial (TSX: IFC): A Canadian mid-size insurance company that offers home, car, and business insurance in Canada, the US, and the UK.

- Cameco (TSX: CCO): A large Canadian company involved in uranium mining, sales, and the construction of reactor components.

- Amphenol: (NYSE: APH) A large cap producer of high-tech interconnect, sensor, and antenna solutions for industries such as automotive, aerospace, industrial, and technology.

- BWX Technologies (NYSE: BWXT): A mid cap size American company specializing in the construction and sale of nuclear components to customers worldwide, including the US Navy.

- Smartcentres Real Estate Investment Trust (TSX: SRU.UN): A mid size fully integrated REIT that owns and manages a number of income producing shopping centres and retails spaces throughout Canada.

The Radar Check was last updated June 2, 2023.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended June 2, 2023: UP ![]()

- At the start of the week, Nvidia joined the US$ trillion-dollar club, as investors climbed aboard Nvidia’s AI bandwagon. Nvidia is the dominant semiconductor company with over 80% of the high-end semiconductor market. As a result of the growing interest in AI, Nvidia has gained roughly 240% since October 2022. I am very glad to have invested in the company well before investors started piling into the stock. 😊

- Amazon has been talking with telecom firms about being able to offer Amazon Prime members low-cost wireless services. I suspect this is only in the US, for now, but would be great if it came to Canada since Canadians already pay some of the highest fees for mobile services.

- General Motors (NYSE: GM) is predicting its Cruise unit of self driving vehicles could bring in US$ 50 billion a year by 2030. That assumes Cruise vehicles will be deployed internationally.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

TMX Group Ltd (TSX: X)

US $

Visa Inc. (NYSE: V)

Quarterly Reports

CrowdStrike Holdings, Inc.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their first quarter 2024 financial results on May 31, 2023

- Revenue of $692,580 for the three months ended April 30, compared to $487,834 for the same period in 2022. An increase of almost 42%.

- Net income of $499 for the three months ended April 30, compared to a net loss of $31,523 in the same period in 2022.

- Diluted earnings per ordinary share of $0.00 for the three months ended April 30, compared to a loss of $0.14 per share for the same period in 2022.

Portfolio 2

Portfolio 2 for the week ended June 2, 2023: UP ![]()

- TC Energy Corp’s (TSX: TRP) received permission from US energy regulators to put their North Baja natural gas pipeline expansion in Arizona and California into service. The pipeline expansion will supply additional natural gas from the southwestern USA to Mexico.

- Guardant Health (NASD: GH) obtained regulatory approval for its Guardant360 CDx blood test by the Singapore Health Sciences Authority. The liquid biopsy test provides comprehensive genomic profiling for patients with advanced solid cancers.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Fortis Inc. (TSX: FTS)

US $

No US$ dividends this past week.

Quarterly Reports

MongoDB, Inc.

All currency listed in thousands of US dollars, except for per share data.

Selected highlights from their first quarter 2024 financial results on June 1, 2023

- Revenue of $368,280 for the three months ended April 30, compared to $285,447 for the same period in 2022. An increase of over 29%.

- Net loss of $54,246 for the three months ended April 30, compared to a net loss of $77,294 in the same period in 2022.

- Diluted loss per ordinary share of $0.77 for the three months ended April 30, compared to a loss of $1.14 per share for the same period in 2022.

Portfolio 3

Portfolio 3 for the week ended June 2, 2023: UP ![]()

- Shopify is facing a class-action lawsuit by recently laid off employees who allege Shopify reneged on a deal it offered when they were laid off recently.

- Microsoft signed a deal with Nvidia-backed CoreWeave to ensure their OpenAI integrated applications would have sufficient computing power going forward. CoreWeave provides GPU-accelerated solutions to the machine learning industries.

- Brookfield Asset Management (TSX: BAM) announced it had purchased a controlling stake in CleanMax Enviro Energy Solutions, an Indian solar-panel maker. CleanMax operates solar and wind farms, as well as rooftop panels for corporate clients throughout India.

Activity

Sold: Shopify has grown significantly and represented nearly 30% of the value of Portfolio 3. In light of this concentration, I decided to sell some Shopify shares after the recent surge to over C$ 80 per share. This was done to reduce the concentration of Shopify in the portfolio and mitigate potential risks associated with a single stock holding. By selling some Shopify shares, I have freed up cash that can be used to further diversify the portfolio to reduce risk and increase the potential for overall returns.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Enghouse Systems Ltd (TSX: ENGH)

Royal Bank of Canada (TSX: RY)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.