Items that may only interest or educate me ….

Canadian Economic news, US Economic news, A new investing resource, AI at work …

Apparently, mid October is when the stock markets historically start to rally until the end of the year. After 18 months of rate hikes by the Canadian and US central banks, both economies have avoided a recession. In Canada, the growth in the labour market easily surpassed expectations for the last three months. It is a similar story in the US, only a stronger labour market and more robust economy. Inflation that refuses to go away is the speed bump preventing the markets from rallying. But let us not get ahead of ourselves. Here is a quick look at items that caught my attention this past week.

Canadian Economic news

This week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

There were no key economic reports released this past week.

Canadian market volatility

Last week I obtained a reading of 11.27 based on the S&P/TSX 60 VIX. I checked it this week and it had not moved from last week’s reading of 11.27. I found that highly unlikely given the events in the middle east and the latest US inflation numbers. I did a bit of research and discovered the TSX 60 VIX index (TSX: VIXI), a volatility index that measures the implied volatility of S&P/TSX 60 index options over the next 30 days. It is calculated using a similar methodology to the US VIX index. Going forward, I will use this reading to get a sense of the volatility in the Canadian markets.

This week the TSX 60 VIX index ended at 15.52, down slightly from last week’s 15.59 reading. The index remains low and suggests that investors are becoming more confident in the Canadian stock market. Generally, a Canadian VIX reading above 20 is considered to be high, while a Canadian VIX reading below 20 is considered to be low.

US Economic news

This week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Producer Price Index

The Producer Price Index (PPI) for September came in higher than expected, up 2.2% from a year ago, the fastest pace since April. On a monthly basis, PPI prices rose 0.5%, down from August’s 0.7% increase. Analysts had forecast a pace of 1.6%. Core PPI, the PPI excluding energy and food prices, rose 2.7% on an annual basis and 0.3% since August.

Whereas the Consumer Price Index (CPI) measures price changes at the end consumer level, the PPI measures price changes at the wholesale level before the final prices reach consumers. PPI is often considered a leading indicator of the CPI, as changes in wholesale prices typically precede changes in consumer prices. The latest data suggest inflationary pressures remain high, despite the high interest rates. However, looking at the monthly numbers, the rate is slowing.

FOMC minutes

The latest minutes from the Federal Open Market Committee’s (FOMC) September 19-20 meeting showed that while the committee did not raise the benchmark interest rate, the majority felt an additional increase sometime this year would be appropriate. It was felt the rate had to remain high enough to drive inflation to their target inflation rate of 2%. Officials were concerned about inflation, higher energy prices, slower economic growth and higher unemployment and that decisions should be made based on the data rather than a predetermined path.

The FOMC minutes are important documents because they provide insights into the discussions and decisions made during meetings that impact America’s economic and monetary policy. They provide a view into the Fed’s thinking and reasoning, allowing us investors to understand what factors influence their decisions and help us make more informed choices about our investments. Finally, the minutes hold the Fed accountable for its actions, ensuring transparency and helping investors anticipate potential changes in the economy and financial markets.

Consumer Price Index

The Labor Department’s CPI report for September showed overall, or headline, inflation rose 0.4% in September after a 0.6% rise in August. Excluding the volatile food and energy components, the core CPI grew by 0.3% in September, matching August’s increase. Analysts were expecting 0.3% for both headline CPI and core CPI.

On an annual basis, the rate of CPI growth was 3.7%, matching August’s rate, and core CPI was up 4.1%. The annual increase in the core number was the smallest in two years. Analysts were expecting 3.6% for headline CPI and 4.1% for core CPI. Analysts prefer the core CPI numbers as a better indicator of underlying inflation than the overall CPI.

For overall CPI, fuel and shelter were the biggest contributors to higher prices in September, while Shelter and Transportation Services were the biggest contributors on a year over year basis. For core CPI, Shelter and Transportation Services saw the biggest gains both monthly and annually.

In September, both the PPI and the CPI were higher than expected. Combine that with a stronger than expected job market, the chances of another interest rate hike by the Fed have only increased.

Consumer Sentiment Index

The University of Michigan’s initial measure of consumer sentiment came in at 63.0 for October, down from September’s 68.1. October’s reading is the lowest reading since May and lower than analysts’ expectations of 67.2. The reading is down 7.5% since September but up 5.2% year over year. The biggest reason for the short-term drop was concerns about inflation, higher interest rates and declining economic conditions. As for the long term, consumers believe the economic situation has improved since the same period in 2022.

Analysts and the Fed closely watch the Consumer Sentiment Index because it is seen as a leading indicator of economic growth. A decline in the CSI can be a sign of a recession on the horizon.

American market volatility

During the week, the CBOE Volatility Index (VIX) reached 19.32, up from 17.45 last week. This suggests an increase in the volatility in the American markets.

A new investing resource

Recently, I stumbled upon Stratosphere.io, a great website for diving into corporate financial data and ratios, ideal for researching companies you are interested in investing in. Its user-friendly interface presents information through intuitive tables and charts, making it easy to spot key insights and trends. I am currently using the free version since it offers everything I need. If you are searching for a reliable resource to analyze companies you are interested in, check it out.

AI at work

How many times have you been stuck in traffic or stopped at a traffic light wondering why anyone cannot figure out a way to keep traffic moving. Well, Google (NASD: GOOGL) is attempting to use artificial intelligence (AI) to fix that, or at least help traffic flow better.

Google’s Project Green Light is a relatively new AI-powered initiative to help cities improve traffic flow at intersections and reduce stop-and-go emissions. It uses Google Maps driving trends to model traffic patterns and make recommendations for optimizing the existing traffic light plans. City engineers can implement these in as little as five minutes, using existing infrastructure to keep costs down. It is both scalable and flexible since it can be applied to any city with existing traffic lights and adapted to different traffic conditions and city needs.

While it is still in the early stages, project Green Light has been shown to reduce stops by up to 30% and emissions at intersections by up to 10%. The project is currently being tested at 70 intersections in 12 cities across four continents, ranging from Abu Dhabi in the United Arab Emirates to Seattle, Washington. Unfortunately, it is not being tested in Canada.

In Seattle, Google is working with the city engineers to optimize traffic lights for buses. This will help reduce bus travel times and make public transportation more attractive to riders. Another example is in Rio de Janeiro where Google is developing a new AI-powered traffic signal system that will give priority to pedestrians and cyclists at intersections.

The purpose of Project Green Light is to make cities more sustainable and livable by reducing traffic congestion and air pollution. This is a great example of AI being used to make people’s lives better and big companies using technology for the better. Hopefully, it will come to Canada sooner rather than later to ease traffic congestion and thereby reduce pollution caused by vehicles idling in traffic and at traffic lights.

The week got off to a good start, before falling at the end of the week. Let’s see what caused the market movements this past week ….

Weekly Market Review

Monday: All three indexes – the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – ended the day on a high note after spending the morning largely below the breakeven bar. The Hamas attack on Israel prompted many investors to move into safer assets, causing the early morning decline. However, the markets moved higher after two Fed members suggested they may not need to increase the US benchmark interest rate. Oil prices moved higher as investors worried about the conflict spreading across the Middle East and the potential disruption to global oil supplies.

In Canada, the Canadian markets were closed for the Canadian Thanksgiving Day holiday.

In the US, it was a quiet day of trading on Columbus Day/Indigenous Day, which saw all sectors end in the green. The Energy and Telecommunications Services sectors posted the biggest gains, while Consumer Staples and Basic Materials (miners & fertilizer manufacturers) brought up the rear.

Tuesday: New measures in China to boost their economy, and dovish comments from Fed officials boosted all four indexes into positive territory. After recent comments from Fed officials, investors now believe the Fed will maintain the current 5.5% interest rate.

In Canada, the Toronto Stock Exchange Composite Index (TSX) ran its winning streak to four and posted its biggest single day gain in almost a month. The TSX benefitted from higher commodity prices and the comments from various Fed officials. In trading, the Energy and Basic Materials sectors were the big beneficiaries of higher commodity prices, outperforming all other Canadian sectors. Healthcare and Consumer Staples were the only sectors to decline.

In the US, the markets rose after a Fed official said they it was unlikely they would have to increase the interest rate to get inflation back to their 2% target. He also said a recession was unlikely given the latest data. These dovish comments caused the yields on US government bonds to fall, leading investors back into the stock markets. In trading, all American sectors ended higher, led by Utilities and Consumer Cyclicals, with Energy and Technology bringing up the rear.

Wednesday: The indexes continued their respective winning streaks as they all ended in positive territory. Oil prices dropped when Saudi Arabia said it would help stabilise oil supplies, quelling investors fears of supply disruption. Lower energy prices decrease inflationary pressures. The other market driver was the release of the minutes from the Fed’s last meeting. The minutes revealed the Fed will proceed cautiously, suggesting that the Fed is not leaning towards a rate hike.

In Canada, The TSX posted its fifth consecutive day of gains as the yields on bonds (long term borrowing) continues to drop, leading investors to move back into stocks. It was a good day for the TSX, with nine of ten sectors moving upward, led by Utilities and Consumer Cyclicals. The only sector to drop was Healthcare.

In the US, the three American indexes briefly dipped into the red on news the PPI came in higher than expected, suggesting inflationary pressures persist despite the cumulative effect of all the interest rate hikes. With the higher PPI, investors now turn to tomorrow’s CPI report to gather clues as to what the Fed is likely to do at their next meeting. In trading, Utilities and Basic Materials posted the biggest gains, while Energy, Consumer Staples and Healthcare were the only sectors to sink.

Thursday: The winning streaks ended with a thud! today as all four indexes ended lower. The big news for the day was the latest US inflation report that showed inflation cooled since August but remains high at 3.7%, well above the Fed’s 2% target. Stocks fell on the news and its implications for interest rates, possibly higher but definitely longer. Oil prices inched higher as the Organization of Petroleum Exporting Countries (OPEC) repeated their predictions for demand.

In Canada, the US sneezed on their inflation number and the TSX’s winning streak ended. 😊 In trading, it was a day of broad-based losses in the Canadian sectors with only the Energy sector ending in positive territory. The biggest losses on the day were suffered by the Utilities and Consumer Cyclicals sectors.

In the US, consumer prices increased at a faster pace than expected. This led to concerns about how the Fed would react to prices growing faster than projected, bringing an end to the respective four day winning streaks of the three American indexes. In trading, the Energy sector was the only American sector to end in the green. The Basic Materials and Utilities sectors posted the biggest losses for the day.

Friday: The indexes started in the green before ending the day with mixed results. The DJIA was the only index to end higher, the TSX and S&P were down, while the Nasdaq was sharply lower. The higher-than-expected US inflation data has investors worried about ‘higher for longer’ interest rates. The conflict in the middle east also weighs on investors. Oil prices rose after the US increased sanctions on Russian oil exports, reports that global oil stockpiles declined, and fears the conflict could expand into other oil producing countries in the region.

In Canada, the TSX ended lower despite higher commodity prices, largely due to concerns about the ongoing conflict in the middle east. On Bay Street, the commodity sectors Basic Materials and Energy (Oil) were the only two Canadian sectors to advance. The biggest losers of the day were Technology and Consumer Staples.

In the USA, the DJIA was lifted by solid third quarter results by a few of the big banks. Neither the S&P nor Nasdaq contain big US banks to offset the drop caused by declining consumer confidence brought on by lingering inflation. On Wall Street, the Energy and Utilities sectors posted the largest gains, while the interest sensitive Technology and Consumer Cyclicals sectors suffered the biggest drops.

Weekly Market and Portfolio Review

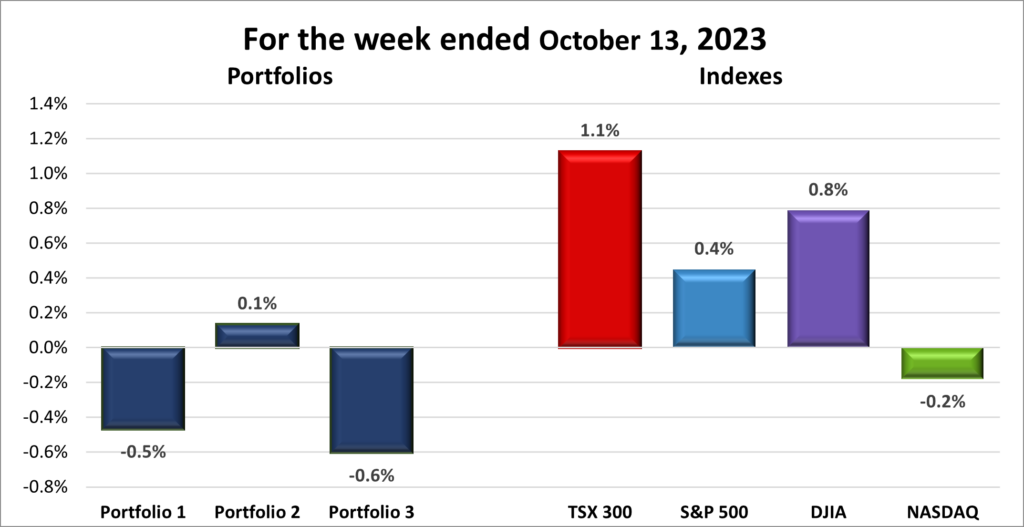

For the week, the TSX (SPTSX) gained 1.1%, the S&P 500 (SPX) was up 0.4%, the DJIA (INDU) advanced 0.8% and the Nasdaq (CCMP) slipped 0.2%.

![]() Despite inflation staying high, three of the four indexes posted weekly gains, as you can see in the chart above. If it were not for a Friday selloff, all four indexes would have posted weekly gains. Sigh!

Despite inflation staying high, three of the four indexes posted weekly gains, as you can see in the chart above. If it were not for a Friday selloff, all four indexes would have posted weekly gains. Sigh!

The American indexes were initially boosted by the good news that inflation is cooling but then fell on the realization inflation is still much higher than the Fed’s 2% target. While the latest inflation news may not be enough for the Fed to warrant raising the US interest rate again, it did increase the chances of a rate hike. Whether there is an increase or not, it did reinforce the Fed’s higher-for-longer mantra about interest rates, causing the markets to slide towards the end of the week.

The selloff brought the S&P lower and sent the Nasdaq into the red. The DJIA was the only index to rally on Friday thanks to decent third quarter earnings from a few major US banks that reported this past week.

In Canada, the TSX snapped a streak of three straight weekly declines. This past week, the TSX was driven higher by surging energy and commodity prices, particularly a surge in energy prices. However, Canada has a similar problem to the US when It comes to sticky inflation. Unfortunately, inflation is not falling as fast as the BoC would like which could lead to another hike to Canada’s benchmark key interest rate.

![]() At the close of trading on Thursday, all three portfolios were performing well, suggesting it was going to be a good week for the portfolios. However, a sudden and sharp decline in the Nasdaq on Friday reversed a lot of the gains. This decline impacted all three portfolios, causing two of them to end the week in negative territory, as you can see below. Portfolios 1 and 3, which lean heavily towards growth-oriented companies, were particularly affected, slipping into negative figures. Portfolio 2, being more balanced and less reliant on technology companies, managed to stay in positive territory, albeit barely.

At the close of trading on Thursday, all three portfolios were performing well, suggesting it was going to be a good week for the portfolios. However, a sudden and sharp decline in the Nasdaq on Friday reversed a lot of the gains. This decline impacted all three portfolios, causing two of them to end the week in negative territory, as you can see below. Portfolios 1 and 3, which lean heavily towards growth-oriented companies, were particularly affected, slipping into negative figures. Portfolio 2, being more balanced and less reliant on technology companies, managed to stay in positive territory, albeit barely.

As we approach mid-October, historically a period marked by market rallies that can extend through to the year-end, I am hopeful that proves true again this year. 😊

Companies on the Radar

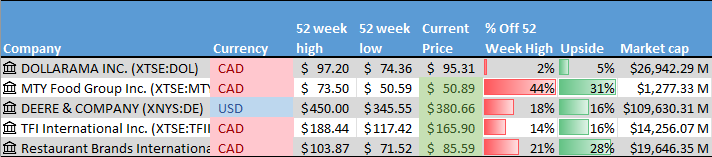

Another week with no new potential companies on my radar. The five companies on my radar remain:

Another week with no new potential companies on my radar. The five companies on my radar remain:

- Dollarama (TSX: DOL), a large Canadian company that operates dollar stores across Canada.

- MTY Food Group Inc. (TSE: MTY), A small cap Canadian consumer cyclical company that operates and franchises quick service and casual dining restaurants throughout North America and internationally.

- Deere & Company (NYSE: DE), a large American company that manufactures and sells agricultural equipment worldwide.

- TFI International Inc. (TSX: TFII), a mid-sized Canadian transportation and logistics company operating across North America.

- Restaurant Brands International Inc. (TSE: QSR), a large cap Canadian consumer cyclical company that operates in the North American quick serve restaurant industry. The company owns Tim Horton’s, Burger King, and Popeye’s Louisiana Kitchen, among others.

The Radar Check was last updated October 13, 2023.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended October 13, 2023: DOWN ![]()

- Cloudflare (NYSE: NET) helped disclose a new vulnerability that would have given hackers the ability to launch attacks larger than anything previously seen on the internet.

- General Motors (NYSE: GM) announced GM Canada has reached a tentative labour agreement with the Canadian union Unifor. The 4,000 workers will receive up to a 25% raise, plus other benefits the union had been demanding. In the US, the strike by the United Auto Workers union against GM, Ford (NYSE: F) and Stellantis (NYSE: STLA) continues.

- Lattice Semiconductor (NASD: LSCC) won a 2023 Cybersecurity Breakthrough Award in the “Overall Network Solution of the Year” category for its Open Radio Access Network (ORAN) solution stack. The ORAN stack help customers deliver data securely and efficiently to the intended destination.

- In the first quarter of 2023, Tesla (NASD: TSLA) owned 62% of the North American electric vehicle (EV) market. By the end of the third quarter Tesla had slipped to 50% of the EV market, losing share to other North American EV manufacturers despite the price war initiated by Tesla.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSX: DIR.UN)

Algonquin Power & Utilities Corp (TSX: AQN)

US $

Innovative Industrial Properties Inc (NYSE: IIPR)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended October 13, 2023: UP ![]()

- TC Energy (TSX: TRP) named its former chief executive officer as the chair of its pipeline business. Earlier this year, the company said it would split into a pipeline business and natural gas transportation company. We now know who will lead the oil pipeline spin off.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Brookfield Renewable Partners LP (TSX: BEP.UN)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week, except for per share data.

Portfolio 3

Portfolio 3 for the week ended October 13, 2023: DOWN ![]()

- Microsoft (NASD: MSFT) received a Notices of Proposed Adjustment from the Internal Revenue Service (IRS) requesting an additional US$28.9 billion for the tax year 2001 through 2013. Ouch! If that is not enough, the IRS is also seeking interest and late penalties. Of course, Microsoft disagrees with this ruling and will appeal.

In other Microsoft news, Britain’s Competition and Markets Authority (CMA) has given Microsoft the go ahead to proceed with their acquisition of Activision Blizzard (NASD: ATVI). Activision Blizzard had to sell the streaming rights to their games, including the popular ‘Call of Duty’ franchise, to obtain CMA approval. The deal now has been signed off by US, European Union, and British anti trust regulators. - TD (TSX: TD) could face a C$500 million lawsuit over claims it did not properly pay vacation and statutory holiday pay to its more than 1,000 mobile mortgage specialists.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

TD U.S. Equity Index ETF (TSX: TPU)

Brookfield Renewable Partners LP (TSX: BEP.UN)

Alvopetro Energy Ltd (TSX: ALV)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.