Items that may only interest or educate me ….

Canadian Economic news, US Economic news, Another potential US government shutdown, Canadian banks to set aside more capital, A pivotal week coming up …..

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Consumer Price Index

Canada’s annual inflation rate, measured by the Consumer Price Index (CPI), grew 3.8% in September, after gaining 4.0% in August. Monthly, the cost of living actually dropped in September by 0.1%, after a gain of 0.4% in August. Analysts had expected gains of 4.0% and 0.1%, respectively.

The annual decline was due to a slowdown in economic growth, with prices rising more slowly in five of the eight major components. The biggest increases were in ‘gasoline’ (up 7.5%) and ‘shelter’ (up 6.0%). The only component to see a decline was ‘household operations, furnishings, and equipment’ (down 1.1%).

The month-over-month decline was the first monthly decline since November 2022 and was primarily the result of lower gas prices. The biggest increases were in ‘clothing and footwear’ (up 0.9%) and ‘shelter’ (up 0.5%), while the biggest declines were in ‘gasoline’ (down 1.3%) and ‘household operations, furnishings, and equipment’ (down 0.7%).

Core CPI, which strips out the volatile food and energy components from the overall CPI, fell 0.1% in September, but rose 3.2% on a year-over-year basis. Core CPI is a more accurate measure of underlying inflation trends.

The slowdown in the pace of price growth suggests that the Bank of Canada’s (BoC) rate hikes are making progress in reducing inflation. As a result, the pressure on the BoC to raise the benchmark interest rate at its October 25 meeting has eased. Analysts believe the chances of the BoC leaving the rate at 5.0% have increased with this latest data.

Retail Sales

In August, Statistics Canada reported a 0.1% decline in retail sales, in contrast to the 0.3% increase in July. Analysts had predicted a 0.3% drop for August, following July’s 0.3% growth. Yearly sales saw a 1.6% increase. Core retail sales, which excludes ‘gas, vehicles, and parts’, fell by 0.3% from July to August but showed a 2.1% increase compared to the previous year.

Breaking down the monthly data, the largest increase occurred in the ‘Gasoline stations and fuel vendors’ subsector, marking a 2.8% increase, while the ‘Food and beverage retailers’ subsector experienced the steepest decline, dropping by 1.2%. Annually, the ‘Health and personal care retailers’ subsector jumped 8.4%, whereas the ‘Gasoline stations and fuel vendors’ subsector faced a 9.3% decline compared to the previous year.

High inflation continues to impact Canadian consumers’ spending habits. Many are delaying significant purchases that require borrowing from financial institutions. Additionally, many retailers cited product availability issues due to the port strike in Vancouver, which hampered sales throughout August.

Canadian market volatility

The Canadian Volatility Index (VIXC), as measured by the TSX 60 VIXI, ended the week at 17.09, up from last week’s 17.04 reading. Investors expectation of market volatility in the Canadian stock market has increased slightly but remains low. Generally speaking, a Canadian VIX reading above 20 is considered to be high, while a Canadian VIX reading below 20 is considered to be low.

Canadian economy projections

The recent report from the independent Parliamentary Budget Officer (PBO) paints a bleak picture of Canada’s economic future, especially in the short term. So much for ‘sunny ways’. Projections suggest economic stagnation well into 2024, driven partly by falling consumer spending due to rising interest rates. Unemployment rates are expected to rise from 5.1% in 2022 to 6.0%, and while current inflation hovers around 4%, it is projected to gradually decrease to 2.8% later in 2024. The report also suggest that the BoC will start reducing the benchmark interest rate by the end of the first quarter in 2024, with rates likely to remain between 2% – 3% until 2028.

For consumers and businesses with a mortgage, line of credit or any type of loan, you will be paying more in interest expenses for the next few years, at least.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

American market volatility

During the week, the CBOE Volatility Index (VIX) reached 21.71, up from 19.32 last week. Once again, the there was an increase in the perceived volatility of the American markets.

Retail sales

The Commerce Department reported a 0.7% increase in retail sales for September, following a 0.6% rise in the previous month, surpassing analysts’ expectations of a 0.3% growth. Year over year, retail sales showed a robust increase of 3.8%. When retail sales rise, it signals that consumers are confident in their financial situations and are willing to spend on goods and services, indicating their positive outlook on job stability and the overall economy. While this reflects a strong economy, the Fed will view it cautiously as they continue their battle against inflation.

Another potential US government shutdown

Remember the narrow escape from a government shutdown in the US at the end of September? If not, here is a quick reminder: they pushed the deadline to November 17. Now, with less than a month left, the House of Representatives has not yet passed a budget to avoid a shutdown. Before they can even propose a budget, the majority party, the Republicans, needs to elect a leader. They have not, and do not appear to being able to elect a leader.

A shutdown would halt non-essential government operations, leading to unpaid leave for many federal employees and disruptions in government contracts and payments.

For us investors, the major concern is the likely delay in economic data and reports released by government agencies. The Fed relies on this data when determining the appropriate US interest rates. Such a delay would not only impact US stock markets but would also reverberate globally since the US has the largest economy in the world. Moreover, as we know, markets do not respond well to uncertainty. The absence of crucial economic information and the government’s inability to function properly would introduce uncertainty into financial markets, amplifying market volatility.

Let us hope the House can get their affairs in order and propose a reasonable budget sooner rather than later. American citizens who work for or depend on the US government certainly do not need a third round of brinkmanship in 2023. For us investors, we can do without the uncertainty a shutdown would bring.

Canadian banks to set aside more capital

The BoC recently issued a directive to Canadian banks and lending institutions, requiring them to maintain a higher amount of capital as a buffer against financial risks. This directive aims to enhance the stability of the banking system, making it more stable and safer during economic downturns and financial uncertainties. For investors, this directive signifies increased stability in the banking sector, translating to reduced investment risks. However, as banks need to retain more of their earnings to meet these requirements, it will likely impact their ability to engage in shareholder-friendly activities in the short term, such as raise dividends, pay one-time special dividends or buyback their own shares.

A pivotal week coming up

The next few weeks could be quite interesting for the US markets as the “Magnificent 7” – Apple (NASD: AAPL), Microsoft (NASD: MSFT), Alphabet (NASD: GOOGL), Amazon (NASD: AMZN), Nvidia (NASD: NVDA), Tesla (NASD: TSLA) and Meta Platforms (NASD: META) report third quarter earnings. The oversized influence that the Magnificent 7 has over the Nasdaq and S&P is one of the reasons that I and other investors will closely be watching their earnings reports. These seven companies have led the market all year so its important that they deliver strong earnings results. Their performance is likely to set the tone for the fourth quarter. Hopefully Tesla’s dismal results are not a harbinger of things to come in the next few weeks.

While the economic landscape seemed fairly quiet last week, beneath the surface, several significant events were in motion. Let’s take a look at the highlights and see what happened this past week…

Weekly Market Review

Monday: all four major North American indexes ended higher, getting the week off to a good start. Investors appeared to have digested last week’s higher US inflation numbers and are optimistic about upcoming third quarter earnings later this week. Oil prices sank on news the US and Venezuela could reach a deal to ease sanctions on Venezuela in exchange for more oil.

In Canada, wholesale trade data came in slightly below expectations but still increased a solid 2.3% in August. The Toronto Stock Exchange Composite Index (TSX) mirrored its American cousins with a surge in growth-oriented technology companies. All Canadian sectors ended in the green, led by the Technology and Telecommunications Services sectors. Consumer Cyclicals and Energy brought up the rear.

In the US, investors anticipate a strong third quarter earnings season, pushing all three indexes solidly into the green. Strong performances in all sectors lifted the Nasdaq Composite Index (Nasdaq), S&P 500 Index (S&P), and the Dow Jones Industrial Average (DJIA) higher.

Tuesday: it was a day of mixed results. The TSX ended higher, the DJIA and S&P were essentially flat with the DJIA barely in the green and the S&P just under the line, and the Nasdaq ending lower. Oil prices rose as investors wait to see how the situation in the Middle East plays out.

In Canada, the TSX hit a three-week high as the CPI came in lower-than-expected raising hopes the BoC will leave the interest rate unchanged at there meeting next week. Surging share prices of gold mining companies gave the TSX a boost as investors return to gold as a safe heaven in times of uncertainty. In trading, the Basic Materials sector (miners, including gold, and fertilizer manufacturers) led all Canadian sectors.

In the US, retail sales for September came in twice as high as forecast, indicating the American consumer remains resilient in the face of higher interest rates. Third quarter earnings season continues with many of the companies that have reported beating expectations. A good sign for the economy.

Wednesday: fears of escalation in the Middle East sent oil prices higher, stoking concerns of inflation and higher interest rates. As a result, all four indexes ended the day firmly lower. Recent US economic data showed the American consumers spending remained strong causing investors to worry about interest rates staying high for longer. Oil prices jumped on lower US stockpiles and the conflict in the Middle East.

In Canada, concerns about higher for longer interest rates weighed on interest sensitive companies sending the TSX into the red. It was a day of broad-based losses as the Energy sector was the only sector to make it into the green. Consumer Cyclicals and Industrials fell the farthest.

In the US, the yields on low-risk Treasury bonds rose, making them more attractive than higher risk stocks. Disappointing quarterly results from some larger US companies also weighed on the markets. In trading, Energy was the only American sector to finish higher. The biggest declines were recorded by the Industrials and Basic Materials sectors.

Thursday: the indexes were up and down like a yoyo for most to the trading session. After the Fed Chair Jerome Powell said inflation is still too high, the indexes plunged into negative territory where they stayed for the rest of the day. Also weighing on the markets was the Middle East conflict. If the conflict spreads to oil producing parts of the region, it could lead to higher oil prices which in turn could cause inflation to rise.

In Canada, comments from the Fed Chair about higher for longer interest rates caused already shaky investor sentiment to wobble, sending the TSX to a two-week low. In Canada, Telecommunications Services and Energy were the only Canadian sectors to end higher, while Healthcare and Consumer Staples had the biggest drops.

In the US, Treasury yields surged after the Fed Chair said an additional rate hike may be necessary to get inflation back on track towards the 2% goal. This caused investors to flock to less risky government bonds, increasing overall market volatility. In trading, the Telecommunications Services sector was the only sector to advance. Consumer Cyclicals and Financials suffered the biggest losses.

Friday: all four indexes ended the day lower as oil prices and US Treasury yields continued to rise. Hawkish comments from the Fed Chair about the possibility of higher interest rates pushed government bonds higher. Investors responded by moving their money from riskier investments like stocks to safer government bonds. The higher yields make borrowing more expensive for companies, slowing the economy and putting downward pressure on stocks. As well, despite a drop in oil prices today, the recent run up of oil prices threatens to add more upward pressure on inflation.

In Canada, the TSX dropped to a two-week low as long-term borrowing costs continue to rise (the interest on bonds) driving down the share price of economically sensitive sectors such as Energy (lower demand when interest rates are high) and Financials (less lending due to higher rates and having to hold more capital in the event of default loans and mortgages). It was not a good day in trading on Bay Street as all sectors ended lower. Consumer Cyclicals and Industrials posted the smallest losses, while Financials and Telecommunications had the biggest losses.

In the US, ten-year government bonds are barely under 5%, causing investors to sell riskier stocks in favour of almost no risk government bonds, putting downward pressure on the American stock markets. Investors believe the Fed will not raise the interest rate at their end of the month meeting, but higher energy prices could force the Fed’s hand at the mid December meeting. It was a day of broad-based losses on Wall Street, as all sectors ended in the red. Telecommunications Services and Healthcare dropped the least while Technology and Financials went the deepest into the red.

Weekly Market and Portfolio Review

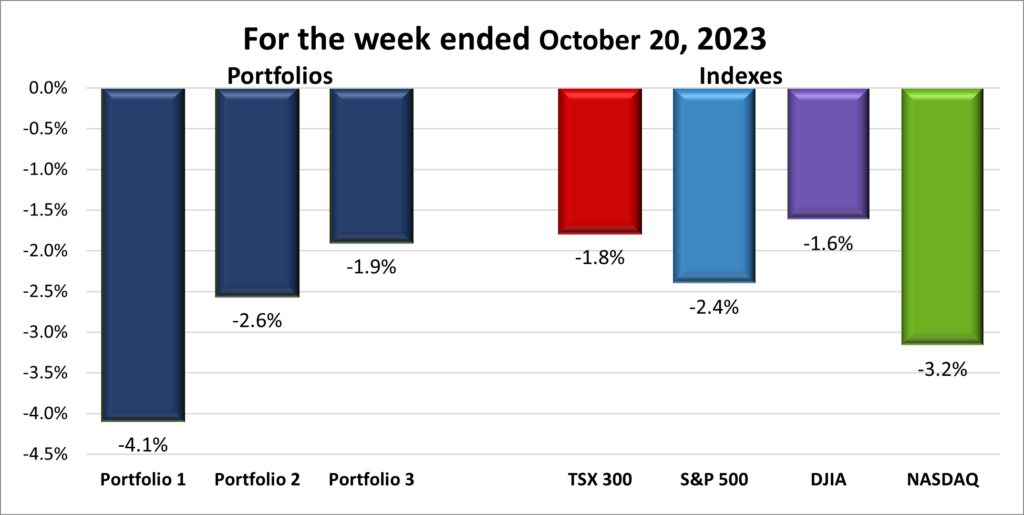

For the week, the TSX (SPTSX) sank 1.8%, the S&P 500 (SPX) dropped 2.4%, the DJIA (INDU) fell 1.6% and the Nasdaq (CCMP) plunged 3.2%.

![]() Once again, the market started the week strong, but by midweek, a downward trend began, as depicted in the graph above. The decline was triggered by concerns that the ongoing conflict in the Middle East might spread to neighbouring oil-producing nations, leading to surging oil prices. This, in turn, could push up inflation rates, prompting central banks to consider raising interest rates. Comments from Fed Chair Powell about a potential rate hike only added to existing worries.

Once again, the market started the week strong, but by midweek, a downward trend began, as depicted in the graph above. The decline was triggered by concerns that the ongoing conflict in the Middle East might spread to neighbouring oil-producing nations, leading to surging oil prices. This, in turn, could push up inflation rates, prompting central banks to consider raising interest rates. Comments from Fed Chair Powell about a potential rate hike only added to existing worries.

Learning point: When there’s substantial government spending, as seen in both Canada and the US, it results in a flood of new government bonds. As the economy’s benchmark interest rate rises, newly issued bonds must offer higher coupon rates to attract investors. Consequently, previously issued bonds with lower coupon (interest) rates become less attractive. To match the appeal of new bonds, the prices of existing bonds decrease in the secondary market. As bond prices fall, their yields, calculated by dividing the annual interest payment by the bond price, rise.

The escalating risk-free yields on government bonds have made them increasingly appealing compared to riskier stocks. Towards the week’s end, when yields neared 5%, many investors chose to sell off their more volatile stocks and invest in risk-free government bonds to secure a guaranteed return. As government bond yields increase, more investors are shifting from risky stocks to bonds, leading to the volatility observed in the stock markets.

This pattern was evident in both the Canadian and US markets, resulting in weekly declines across all four indexes.

![]() The portfolios faced another challenging week, as seen in the chart below. As discussed earlier, a shift from high-risk stocks, particularly technology companies prominent in the portfolios, to safer bonds has increased market volatility, especially in the Nasdaq. Unfortunately, this volatility took its toll on the portfolios, resulting in widespread losses. ☹

The portfolios faced another challenging week, as seen in the chart below. As discussed earlier, a shift from high-risk stocks, particularly technology companies prominent in the portfolios, to safer bonds has increased market volatility, especially in the Nasdaq. Unfortunately, this volatility took its toll on the portfolios, resulting in widespread losses. ☹

Seeing a significant downturn across all four indexes, I anticipated it would not be a great week for the portfolios. Although the value of oil companies increased during the week, it did not come close to compensating for losses in other sectors. The presence of oil companies in each portfolio proved vital to mitigating the losses. This highlights the importance of a diversified portfolio. Interestingly, a few years back, I would not have considered owning any oil companies, but now I am glad that I heeded two pieces of advice: its important to be diversified and the world needs oil. 😊

The technology sector had a challenging week, affecting all three portfolios. Portfolio 1, containing both major and lesser-known tech names, experienced widespread declines, making it the worst performer among the portfolios and indexes. Portfolio 2, being more balanced, also faced losses across almost every company in the portfolio, positioning it as the second-worst performer. While Portfolio 1’s drop led me to expect a similar fate for Portfolio 3, it surprisingly experienced less of a decline, primarily due to its lower exposure to the technology sector. However, being the best among a bad lot is not a cause for celebration.

I definitely hope for a market rebound next week, and a return to the winning ways of the first half of the year. I am staying optimistic and look forward to brighter days ahead!

Companies on the Radar

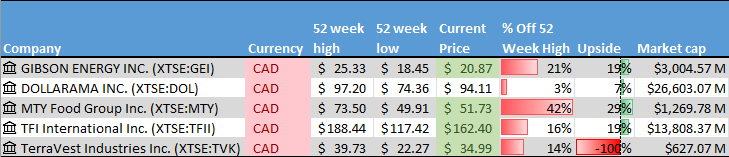

During the past week, I removed Deere & Company (NYSE: DE) and Restaurant Brands International Inc. (TSE: QSR) from my radar list. Although both are good companies, I believed I could find better options, so I decided to explore elsewhere. Two new companies caught my attention: TerraVest Industries (TSE: TVK) and Gibson Energy (TSE: GEI).

During the past week, I removed Deere & Company (NYSE: DE) and Restaurant Brands International Inc. (TSE: QSR) from my radar list. Although both are good companies, I believed I could find better options, so I decided to explore elsewhere. Two new companies caught my attention: TerraVest Industries (TSE: TVK) and Gibson Energy (TSE: GEI).

TerraVest is a diverse small-cap Canadian company that manufactures and sells goods and services to energy, agriculture, mining, and transportation sectors in Canada and the US. While Gibson is a small-cap Canadian company specializing in providing liquid infrastructure products and services to the North American energy sector.

Small-cap companies, typically valued between $300 million and $2 billion (market capitalization is calculated by multiplying share price with the number of outstanding shares), offer the potential for higher returns. However, they come with higher volatility and increased risk. Due to their smaller size and lower trading volumes, these stocks tend to be more sensitive to market fluctuations, economic events, and company-specific news. The upside is they have lots of room to grow, which I would count on.

Interestingly, with the departure of Deere & Company and the inclusion of these two new companies, I noticed my radar list is unintentionally comprised solely of Canadian companies. Normally, I prefer a mix of Canadian and American companies for diversification purposes and to be invested in the world’s largest economy. I will need to keep an eye out for potential American additions in the future.

- Dollarama (TSE: DOL), a large Canadian company that operates dollar stores across Canada.

- MTY Food Group Inc. (TSE: MTY), a small cap Canadian consumer cyclical company that operates and franchises quick service and casual dining restaurants throughout North America and internationally.

- TFI International Inc. (TSE: TFII), a mid-sized Canadian transportation and logistics company operating across North America.

The Radar Check was last updated October 20, 2023.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended October 20, 2023: DOWN ![]()

- The US government is tightening the restrictions on the sale to China of semiconductors used in artificial intelligence (AI) by chip designers such as Nvidia. Nvidia’s top chips were already barred from sale to Chinese companies, but these new regulations will prohibit the sales of a broader range of advanced semiconductors. Nvidia says it will not have much impact on its financial results in the short term.

- Tesla announced they are recalling over 54,000 of their Model X electric vehicles (EV) built between 2021 and 2023. The problem is the vehicle controller module is unable to detect low brake fluid.

Tesla’s third quarter report was downright dismal as the company missed expectations on third quarter revenue, gross margin, and net profit. Ouch! The company said higher interest rates are hurting sales. They did not mention that their price cuts were likely the cause of lower gross margins and profits. - General Motors (NYSE: GM) raised its offer to United Auto Workers unions. The latest offer includes a wage hike of 23%, plus other benefits. The wage hike matches those made by fellow car makers Ford (NYSE: F) and Stellantis (NYSE: STLA).

Activity

Bought: Rivian Automotive (NASD: RIVN) I do not expect to recover my initial investment in Rivian, but I do believe the company will do well going forward and the share price will rise. While Tesla is the undisputed #1 in EVs, I think Rivian could become the #1 maker of electric trucks and electric SUVs. I am seeing more and more Rivian electric trucks and electric SUVs on the road, whereas Tesla’s Cyber truck is not in production, and I have seen very, very few electric trucks and SUVs from other manufacturers.

The risk is Rivian runs out of money or loses market share to other competitors. At this time, Rivian is practically the only EV maker in the truck and SUV market so it could obtain a dominant share of the market before competitors enter the market, much like Tesla has done in the electric car market.

On the positive side, management at Rivian has shown strong execution, surpassing delivery expectations in the second quarter. Additionally, they are constructing a new facility and developing more affordable EV versions. These strategic moves are expected to enhance production efficiency, lower vehicle costs, and boost revenues. A positive sign is the insider trading activity, where more shares have been bought than sold in the last six months. Finally, analysts’ insights further support Rivian’s potential. TD Direct Investing has a twelve-month target in the range of US$29, while Morningstar currently shows a fair value price of US$29.

Overall, I wish I had sold my initial purchase of shares when it was in the US$160 range but there is nothing, I can do about that. I think Rivian will do well from here as they are a first mover in the electric truck and SUV market. The share price had been trending higher, but this recent drop offered an opportunity to pick up shares at a reasonable price. If the company keeps performing well, I will be quite happy if it reaches the US$29 range for a 50% gain. I would be ecstatic if it reached US$160. 😊

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Andlauer Healthcare Group Inc (TSE: AND)

US $

BSR Real Estate Investment Trust (TSE: HOM.U)

Quarterly Reports

Tesla, Inc.

All currency listed in millions of US dollars, except for per share data.

Selected highlights from their third quarter 2023 financial results on October 18, 2023

- Revenue of $23,350 for the three months ended September 30, compared to $21,454 for the same period in 2022. An increase of almost 9%.

- Net income of $1,853 for the three months ended September 30, compared to net income of $3,292 in the same period in 2022.

- Diluted earnings per ordinary share of $0.95 for the three months ended September 30, compared to earnings of $0.53 per share for the same period in 2022.

Portfolio 2

Portfolio 2 for the week ended October 20, 2023: DOWN ![]()

- The Bank of Nova Scotia (TSE: BNS) announced it will reduce its workforce by approximately 2,700, or 3% in the coming months. Do not be surprised if similar announcements come from other Canadian banks and money lenders.

- TC Energy (TSX: TRP) received sign off from the US Federal Energy Regulatory Commission (FERC) to add an additional 150,000 dekatherms per day of firm transportation service to its Gas Transmission Northwest (GTN) system. In case you were wondering, as I was, a dekatherm is a unit of energy used to measure natural gas consumption. It is equivalent to 1 million British thermal units (BTUs). It is a standard unit used in the energy industry to simplify large-scale energy measurements, particularly when dealing with substantial quantities of natural gas.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

SmartCentres Real Estate Investment Trust (TSE: SRU.UN)

Dream Industrial Real Estate Investment Trust (TSE: DIR.UN)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week, except for per share data.

Portfolio 3

Portfolio 3 for the week ended October 20, 2023: DOWN ![]()

- Microsoft announced they would layoff an additional 3% of their 20,000 LinkedIn staff to cut costs amid slowing revenue growth.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

SmartCentres Real Estate Investment Trust (TSE: SRU.UN) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.