The markets kicked off 2024 with a stumble the previous week but recovered nicely this past week. While December often sees a surge due to year-end bonuses and holiday spirit (the “Santa Claus rally”), January can bring a return to normalcy with potential pullbacks. This week’s rebound shows the market’s inherent fluctuations, emphasizing the importance of a long-term perspective for investors.

Investing can be like planting an acorn – through careful selection, nurturing, and patience our portfolios will grow big and resilient. Remember, investing is a long-term game, and focusing on quality companies can help you reach your financial goals, even with the occasional dip along the way.

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, AI gets its own button, 2024 TFSA contributions, A new #1, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Canadian market volatility

Canada’s stock markets’ ‘fear gauge,’ represented by the TSX 60 VIXI, ended the week at 10.57, almost a full point lower than last week’s reading of 11.55. This decrease suggests investors anticipate smaller price swings in the near future. investors are more confident and prepared to risk more in Canadian stocks. Investors are also anticipating interest rate cuts by the central banks of Canada and the US.

The VIXC’s “high” and “low” volatility thresholds are defined as readings above 20 and below 20, respectively. Therefore, the current level of 10.57 indicates a calm market environment.

Canadian trade balance

Statistics Canada’s latest update on Canada’s trade balance revealed the trade surplus shrank to a C$1.6 billion surplus in November, following a revised surplus of C$3.2 billion in October. Analysts had expected the surplus to shrink to C$1 billion. The surplus marked the fourth consecutive monthly surplus.

On a monthly basis, imports increased by 1.9% over October, driven by an 11.6% surge in ‘Energy products.’ The most significant decline was observed in ‘Consumer goods,’ down 2.2%. Regarding exports, there was a 0.6% decrease, primarily due to a 6.5% decline in ‘Metal and non-metallic mineral products.’

On an annual basis, exports were up 3.0%, while imports dipped 0.1%. The biggest gain in exports was by the ‘Motor vehicles and parts’ sector, rising 43.2% while the biggest decrease was in ‘Farm, fishing and intermediate food products,’ down 19.4%. On the import side, ‘Aircraft and other transportation equipment and parts,’ saw the largest increase, up 13.8%, while Energy products’ suffered the biggest decline, down 16.0%.

While Canada still maintained a surplus, the reduction indicates a potential moderation in economic activity, consistent with the slowing Gross Domestic Product. As well, the decrease in imports of ‘consumer goods’ confirms a slowdown in domestic consumption, as consumers tend to reduce spending on goods when interest payments are higher.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Consumer Product Index

The Labor Department’s December inflation report, measured by the Consumer Price Index (CPI), shows a 0.3% increase compared to November’s 0.1% rise. Year-over-year, CPI grew by 3.4%, exceeding analysts’ expectations of 3.2%. This indicates that inflation has increased slightly after a period of decline, potentially due to the holiday season.

‘Medical Care services’ led the monthly increases, rising by 0.7%, while ‘Shelter’ saw a 0.5% bump. Conversely, the price of ‘Fuel oil’ experienced the steepest monthly decline, down 5.5%. On an annual basis, ‘Motor vehicle insurance’ saw the biggest rate increase, up 20.3%, while ‘Fuel oil’ dropped the most, by 14.7%.

The core CPI, which excludes the volatile food and energy price components, also saw a 0.3% increase in prices in December, mirroring November’s growth. Annually, it grew by 3.9%, higher than expectations of a projected 3.8% increase. ‘Medical Care services’ led monthly price increases, while ‘Motor vehicle maintenance’ saw the largest dip, down 0.3%. On an annual basis, ‘Motor vehicle insurance’ saw the largest price increases, while ‘Used cars and trucks’ saw the steepest price decline, down 1.3%.

The Labor Department’s Producer Price Index (PPI), which tracks the prices producers get for their goods and services before they reach consumers, came in lower than expected. The data suggests inflation is still falling despite the higher CPI, which tracks the average change in prices paid by consumers for goods and services over time. The data from these reports suggests that a soft landing for the economy might still be possible. If inflation continues to fall in the coming months and the robust labour market holds steady, the Fed may be able to lower the benchmark interest rate at their March meeting without triggering a recession. This would be a positive development for businesses and consumers alike.

American market volatility

By the end of the week, the ‘fear gauge,’ formally known as the CBOE Volatility Index (VIX), had dipped to 12.70 at the end of the week, after registering 13.35 the previous week. The decrease suggests increased investor confidence that the markets will continue their upward trend that they resumed this past week. Investors are less anxious about potential risks and more willing to invest in stocks.

The VIX is a measure of the market’s expectation of short-term volatility based on S&P 500 options prices.

AI gets its own button

Microsoft (NASD: MSFT) introduced a dedicated keyboard button for its Windows keyboard, specifically for its artificial intelligence (AI) Copilot service. The button will be a standard feature on all new Windows 11 PCs. When users press the AI key, it will activate the Copilot chatbot, designed to assist with various computer tasks like summarizing articles or emails, creating images, and adjusting system settings. Copilot is already seamlessly integrated into Bing, Microsoft’s search engine, and users of the Edge browser will find the Copilot button in the top right corner.

This marks the first alteration to the keyboard layout since 1994 when Microsoft introduced the special ‘Windows’ key, positioned to the left of the spacebar. The new Copilot key will be located to the right of the spacebar. The introduction of a dedicated key for AI signifies Microsoft’s recognition of the importance and impact it anticipates AI will have on computing in the future.

If there were any doubts about Microsoft’s commitment to AI, their significant investment and effort in this emerging technology should dispel them.

2024 TFSA contributions

As of January 1, 2024, Canadians can contribute an additional C$ $7,000 to their Tax-Free Savings Accounts (TFSAs). Contributions can be made in the form of cash or securities to your TFSA. If you are moving stocks into your TFSA, remember to match their currency with the relevant currency account (Canadian stocks for Canadian dollar accounts, US stocks for US dollar accounts).

A quick reminder, with a TFSA you do not get a tax deduction when you contribute to a TFSA. However, your investments grow tax free and are withdrawn tax-free from your TFSA. If used properly, TFSAs are a terrific way to grow your wealth. 😊 You can make regular monthly contributions, one lump sum deposit up to your limit or whenever you have extra cash but do contribute. TFSAs are a terrific way to save for retirement, a down payment, or any other goal you have in mind.

If you do not already have a TFSA and are interested in starting one, check with a financial planner or tax specialist before depositing cash or other investments into a TFSA.

A new #1

The market landscape underwent a significant shift this week as Microsoft surpassed Apple (NASD: AAPL) to claim the title of the world’s most valuable company. Microsoft’s valuation at the week’s close stood at US$2.887 trillion, edging past Apple’s US$2.874 trillion by US$13 billion. While Apple has long been a dominant force in consumer electronics with its iPhones and Macs, a slight dip in its market capitalization opened the door for Microsoft’s rise. This transformation underscores the increasing influence of AI, an area where Microsoft has firmly established itself as a leader.

Despite Apple retaining its formidable status and enjoying substantial brand loyalty, recent sales figures for iPhones and Mac computers have shown a slowdown. In contrast, Microsoft’s stock has experienced a consistent ascent, driven by its achievements in implementing AI technology. This technological edge played a crucial role in propelling Microsoft to the top spot.

Such market shifts are relatively common and should be kept in perspective. Both Microsoft and Apple are industry giants with impressive portfolios and dedicated followings. Between the two, one or the other has held the title of world’s most valuable company since February 4, 2019, with Apple holding the title since November 2021. Together, their combined market capitalization represents approximately 14% of the S&P.

The question now is: Can Apple regain its title as the world’s most valuable company, or is Microsoft poised for an extended reign? Only time will tell.

The indexes and the portfolios all got back on the winning track this past week even after US inflation came in higher than expected. Let’s look into the market’s ups and downs of the past week and see how it impacted the portfolios ….

Weekly Market Review

Monday: investors returned to the technology sector after last week’s pullback, boosting all four indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – solidly into positive territory. Oil prices fell after Saudi Arabia lowered the price of crude oil and the Organization of Petroleum Exporting Countries (OPEC) nations decided to boost output.

In Canada, gains in Canada’s technology sector overcame the declines in the Energy sector. For the Canadian technology sector to overcome the much bigger Energy sector it must have been a good day for technology companies. And it was, with the Technology sector advancing almost 2.5 times as high as the next best performer – Consumer Cyclicals. Energy and Basic Materials (miners and fertilizer manufacturers) were the only Canadian sectors to end lower.

In the US, the yields on US government bonds fell, causing investors to move back into stocks, pushing the S&P and Nasdaq to their best single day in almost 2 months. The DJIA’s gains were held back by a drop in Boeing (NYSE: BA) following the inflight blow out of a panel on one of its planes. In the American sectors, it was a day of broad-based gains, led by Technology and Consumer Cyclicals. Energy was the only sector to end the day lower.

Tuesday: the markets gave back much of yesterdays gains as only the Nasdaq was able to inch up into positive territory. Two members of the Fed said its likely that if the US interest rate remains at its current level, inflation could fall to their target of 2%. Oil rebounded from yesterday’s losses after Libya closed one of its largest oilfields and the ongoing conflict in the Middle East.

In Canada, investors continue to take profits from the late 2023 rally as they look toward the BoC and the Fed for clues as to when rates might start to decline. In trading, the Technology was the only Canadian sector to post a gain, followed by the Telecommunications Services sector that ended the day flat. On the losing side, Healthcare and Financials fell the hardest.

In the US, investors are now doubting interest rates will start to fall in the first quarter, causing US government bond yields to creep higher and the markets to wobble. In trading, the Technology sector was the only sector to post a gain, while the Basic Materials and Telecommunications sectors fell the farthest into negative territory.

Wednesday: the markets moved modestly higher as investors await tomorrow’s US inflation report hoping they will show inflation continuing to drop, opening the door for the Fed to lower the interest rate. In anticipation, investors moved back into the riskier, growthier sectors like Technology and Consumer Cyclicals. Oil prices fell on higher US oil inventories, suggesting a slowdown in demand.

In Canada, analysts are forecasting that the BoC will not start lowering the Canadian benchmark rate until the second half of 2024. In trading, the Technology and Consumer Staples sectors led the TSX higher. The biggest declines were in Healthcare and Financials.

In the USA, a Fed official said it was too soon to consider rate cuts causing investors to lower expectations of a rate cut in March. In trading, Technology and Consumer Cyclicals were the big winners, while Energy, Basic Materials and Utilities were the only sectors to end lower.

Thursday: All four indexes fell in morning trading after US inflation data came in higher than expected. However, an afternoon rally enabled the DJIA and the Nasdaq to rise above the breakeven point, although barely. Investors had been expecting the US inflation data to be lower so today’s report raises doubts the Fed will lower rates as early as expected. Oil prices rose when tensions in the Middle East escalated after Iran seized an oil tanker.

In Canada, the TSX ended the day lower as investors reacted to the likelihood that interest rates will not be coming down as previously expected. In trading on Bay Street, the Consumer Cyclicals and Consumer Staples sectors posted the biggest gains for the day, while Utilities and Financials recorded the biggest daily losses.

In the US, the S&P was the only American index to end the day in the red. Investors got skittish after higher inflation data and a strong weekly employment report combined to decrease the odds the Fed will lower rates in March. In trading on Wall Street, Technology, Energy and Consumer Staples were the only sectors to end in the green, while Utilities and Telecommunications Services had the biggest declines.

Friday: it was a mostly positive day with the DJIA the only index to end lower. Investors who were concerned about Thursday’s higher then expected inflation for December received some upbeat news when the US Producer Price Index (PPI), came in lower than expected. Oil prices rose after the US and Britain struck Houthi militant targets in Yemen to protect the vital Red Sea shipping channel.

In Canada, rising oil and commodity prices helped the TSX get back into positive territory for the week as it closed at its highest level in almost 21 months. In trading, the top performing sectors were Basic Materials and Healthcare, while Consumer Cyclicals and Financials incurred the biggest decline.

In the US, the three American indexes started the day with a small rally before falling into negative territory and then climbing back to the flatline to end the day relatively unchanged. In trading, the Energy and Telecommunications Services sectors were the biggest winners on the day, while Consumer Cyclicals and Financials suffered the biggest losses.

Weekly Market and Portfolio Review

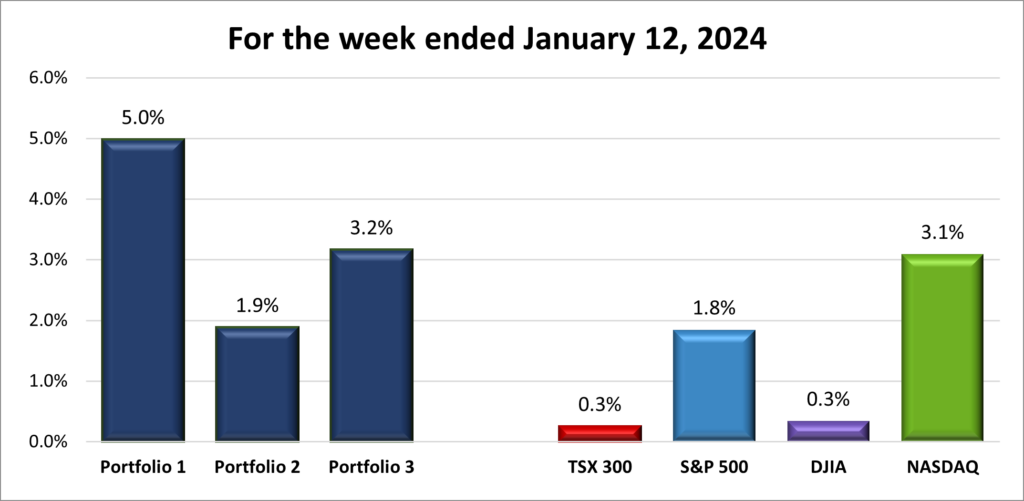

For the week, the TSX (SPTSX) inched higher 0.3%, the S&P 500 (SPX) gained 1.8%, the DJIA (INDU) added 0.3% and the Nasdaq (CCMP) advanced 3.1%.

| Index | Weekly Streak |

| TSX: | 1-week winning streak |

| S&P: | 1-week winning streak |

| DJIA: | 1-week winning streak |

| Nasdaq: | 1-week winning streak |

![]() After a shaky start, the North American returned to their winning ways this week, as seen on the chart above. Despite a sluggish start to 2024 for the indexes last week, the three American indexes are approaching their respective highs. The S&P is almost at its record highs set in January 2022, the Nasdaq is approaching a two-year high, while the DJIA is close to its all-time high set on January 2 of this year. As in 2023, the vanguard of these gains has been the bigger technology companies, especially the Magnificent 7 companies. All seven companies reside on the Nasdaq so its no coincidence that that index posted the largest weekly gain.

After a shaky start, the North American returned to their winning ways this week, as seen on the chart above. Despite a sluggish start to 2024 for the indexes last week, the three American indexes are approaching their respective highs. The S&P is almost at its record highs set in January 2022, the Nasdaq is approaching a two-year high, while the DJIA is close to its all-time high set on January 2 of this year. As in 2023, the vanguard of these gains has been the bigger technology companies, especially the Magnificent 7 companies. All seven companies reside on the Nasdaq so its no coincidence that that index posted the largest weekly gain.

As for the TSX, it does not have as robust of a technology sector component as its American cousins, so it has not experienced the same success. The commodity-heavy TSX got off to a slow start last week as optimism of early rate cuts started to fade. However, the TSX has quietly gained over 12% since a late October swoon.

The main drivers of the markets this past week were inflation data, with the worrying news of the CPI offset by the good news of the PPI. The mixed inflation news led investors once again contemplate rate cuts sooner rather than later. Also impacting the markets was the ongoing conflict in the Middle East where concerns about the supply of oil helped the energy sector recover some of the losses from the previous week.

Overall, the positive factors held sway during this week, leading to gains for the four major North American indexes.

| Portfolio | Weekly Streak |

| Portfolio 1: | 1-week winning streak |

| Portfolio 2: | 1-week winning streak |

| Portfolio 3: | 1-week winning streak |

![]() With each of the indexes posting a weekly gain it was no surprise to see the three portfolios all get back into the win column, outperforming the S&P and the TSX, both are considered common benchmarks. As shown in the chart below, Portfolio 1 had the best week of the portfolios and the indexes. It was lead by significant (more than 10% up or down) gains in uranium producer Cameco (TSE: CCO), up 18% to reach an all time high as uranium prices surged. Crowdstrike (NASD: CRWD) also posted an impressive 12% gain for the week.

With each of the indexes posting a weekly gain it was no surprise to see the three portfolios all get back into the win column, outperforming the S&P and the TSX, both are considered common benchmarks. As shown in the chart below, Portfolio 1 had the best week of the portfolios and the indexes. It was lead by significant (more than 10% up or down) gains in uranium producer Cameco (TSE: CCO), up 18% to reach an all time high as uranium prices surged. Crowdstrike (NASD: CRWD) also posted an impressive 12% gain for the week.

Portfolio 2 lagged the other two portfolios as it had no significant movers up or down. It was lifted by the rising tide of the overall market. Portfolio 3 also benefitted from the overall market rise but got an extra boost from e-commerce giant Shopify which gained 8% over the week. Shopify has grown to represent almost 23% of the portfolio so when it moves, the portfolio moves.

After last week’s stumble, it was good to see all three portfolios increase in value.

Companies on the Radar

This week the radar list says good bye to Jacobs Solutions (NYSE: J) and MP Materials (NYSE: MP), and welcomes Equitable Bank (TSE: EQB), a Canadian mid sized company based on market capitalization (number of shares outstanding X market price that falls between $1 billion – $4 billion). As the name implies, this is a bank that provides financial services to consumers and businesses. Unlike the big 6 Canadian banks that saw their share prices remain flat for most of 2023, Equitable’s share price increased 50%. That got my attention. 😊 It joins the four companies listed below.

This week the radar list says good bye to Jacobs Solutions (NYSE: J) and MP Materials (NYSE: MP), and welcomes Equitable Bank (TSE: EQB), a Canadian mid sized company based on market capitalization (number of shares outstanding X market price that falls between $1 billion – $4 billion). As the name implies, this is a bank that provides financial services to consumers and businesses. Unlike the big 6 Canadian banks that saw their share prices remain flat for most of 2023, Equitable’s share price increased 50%. That got my attention. 😊 It joins the four companies listed below.

- McDonald’s (NYSE: MCD), the large sized American fast-food chain.

- Celestica Inc. (TSE: CLS), a medium sized Canadian company that manufactures electronic products and provides supply chain services to companies around the world.

- Kinaxis (TSE: KXS), a Canadian mid sized company that provides cloud based supply chain solutions to customers around the world.

- Lumine Group (TSE: LMN), a young Canadian mid sized company that acquires and strengthens communications and media software companies.

The Radar Check was last updated January 12, 2024.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended January 12, 2024: UP ![]()

- Nvidia (NASD: NVDA) is putting the finishing touches on a semiconductor specifically designed for the Chinese AI market. The H20 chip, and two other chips destined for the Chinese market, were designed to adhere to US export restrictions. The company says the chip should be ready to ship in the second quarter of 2024.

- Apple announced its Vision Pro mixed-reality headset will be available in the US starting February 2. The headset is considered the company’s biggest product launch since the iPhone back in 2007. Prices start at US$ 3,499.

- After new US government vehicle regulations were implemented, Tesla (NASD: TSLA) has started to lower their driving range estimates. Its good to see the government taking a harder line with inflated ranges estimates by electric vehicle (EV) manufacturers.

Separately, Tesla has launched a revamped Model 3 EV for North America. - In a blow to EV manufacturers, Hertz Rent a Car (NASD: HTZ) is selling the bulk of its EV fleet, citing higher repair costs for damaged EVs. Hertz plans to sell approximately 20,000 EVs and replace them with conventional vehicles. Hertz EVs for sale include vehicles from Tesla and General Motors (NYSE: GM).

- Amazon (NASD: AMZN) laid off a few hundred employees from their Prime Video and Amazon MGM Studios as the company continues to reduce expenses.

- Alphabet’s (NASD: GOOGL) Google is back in court, this time arguing they did not infringe on patents belonging to computer scientist Joseph Bates during the development of their internal usage AI chips. At stake is US$ 1.67 billion in damages. The complainant said Google copied his code after collaborating with him to solve a problem Google had with AI. Google argues its developers never met with Mr. Bates and the chips were designed independently.

In other Google news, the company is laying off hundreds of employees across multiple business units as it continues to cut costs. - Crowdstrike was named a Leader in Gartner’s Magic Quadrant for Endpoint Protection. That was the fourth straight time Crowdstrike has been selected as a Leader in this category.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Yellow Pages Ltd (TSE: Y)

Pulse Seismic Inc (TSE: PSD)

US $

Costco Wholesale Corp (NASD: COST)

Innovative Industrial Properties Inc (NYSE: IIPR)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended January 12, 2024: UP ![]()

- Guardant Health (NASD: GH) announced they have partnered with multinational pharmaceutical company Hikma Pharmaceuticals to market Guardant’s collection of liquid and tissue biopsy tests for cancer screening throughout the Middle East and North Africa.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Telus (TSE: T) DRIP

US $

Walt Disney Co (NYSE: DIS)

Quarterly Reports

No quarterly reports this past week, except for per share data.

Portfolio 3

Portfolio 3 for the week ended January 12, 2024: UP ![]()

- The European Union’s antitrust regulator, the European Commission (EC) is considering opening an investigation into the relationship between Microsoft and OpenAI, a leader in AI. The EC is considering whether Microsoft’s US$10 billion investment in OpenAI is the same as a merger.

- Shopify (TSE: SHOP) announced they are partnering with Manhattan Associates (NASD: MANH), a global supply chain commerce company. Together they will create omnichannel order management solutions to help their merchants deliver a top-notch experience to their customers.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

No quarterly reports this past week.