I have often been asked what is gambling? Is not investing the same as gambling? Or similar variations of these questions. As an amateur investor myself, I remember feeling similar confusion when I first started. This week, I will attempt to answer this question for those who are considering investing in public companies or have just started investing in companies. I will also review the broader economic landscape, gauge the pulse of the markets, and, of course, peek into the performance updates of our portfolios.

Let’s begin.

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, Another US budget extension, What is Investing? …

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Consumer Price Index

Statistics Canada’s December inflation report, as measured by the Consumer Price Index (CPI), revealed that annual headline inflation in Canada rose by 3.4%, a slight increase from November’s 3.1%. On a monthly basis, inflation decreased by 0.3% in December, following a 0.1% increase in November – both in line with analysts’ expectations.

In December, the most significant monthly price increases were observed in the ‘Air transportation’ and ‘Mortgage interest cost’ categories, rising by 31.1% and 1.8%, respectively. The largest downward pressures came from ‘Travel tours,’ down 18.2%, and ‘Gasoline,’ which saw a 4.4% drop – marking the fourth consecutive month of falling gas prices. Year over year, key contributors to inflation were ‘Mortgage interest cost,’ up 28.6%, ‘Rent,’ up 7.7%, and ‘Food from restaurants,’ up 5.6%. Conversely, downward pressure came from ‘Telephone Services’ and ‘Natural gas,’ down 20.6% and 14.5%, respectively.

Excluding the more volatile food and energy components, more commonly referred to as core CPI, prices increased by 3.4% annually, slightly down from the 3.5% rise in November. On a monthly basis, core prices fell by 0.3%, following a 0.2% increase in November.

In the ‘CPI: Annual review for 2023’, data revealed that inflation averaged 3.9%, significantly lower than 2022’s 6.8% average which was a 20-year high. The primary factor contributing to this decrease was the drop in gas prices, down 4.2% in 2023 after a 22% increase in 2022.

While December headline inflation, the overall inflation picture, edged slightly higher than expected, making an interest rate cut unlikely, the report hints at potential easing on the horizon. On a monthly basis, inflation dipped, and even core inflation, while still elevated, showed signs of slowing. Overall, this appears to be a temporary deviation from the Bank of Canada’s path to their 2% target, suggesting that interest rate adjustments might still be on the table for later in the year, hopefully sooner rather than later. 😊

Retail Sales

Canadian retail sales data for November came in lower than expected, falling 0.2% after a gain of 0.6% in October. Analysts had expected a drop of 0.1%. On an annual basis, retail sales were up 1.8%.

The biggest monthly and annual increases were in ‘Motor vehicle and parts dealers,’ up 0.5%, and 7.0%, respectively. The biggest monthly decline was in ‘General merchandise retailers,’ down 1.8%, while the biggest annual decline was in ‘Gasoline stations and fuel vendors,’ down 11.1%.

Core retail sales, retail sales less sales from gasoline stations and motor-vehicle and parts dealers, dropped 0.6% from October, but were up 2.1% year over year.

The weak sales data suggests a period of slower growth for the economy, however, initial estimates for December show an increase of 0.8%. This latest report open’s the door for the BoC’s to signal the end of rate hikes at their January 24 meeting.

Canadian market volatility

Canada’s stock markets’ ‘fear gauge,’ represented by the TSX 60 VIXI, ended the week at 12.26, 16% higher than last week’s reading of 10.57. That is a significant jump and signals growing concern among investors about the Canadian market. Geopolitical tensions, a struggling Canadian economy and the upcoming fourth quarter earning could all factor into the increased anxiety. However, keep in mind that this latest volatility reading is still considered low, and investors remain cautiously optimistic about the Canadian markets.

The VIXC’s “high” and “low” volatility thresholds are defined as readings above 20 and below 20, respectively. Therefore, the current level of 12.26 indicates a calm market environment.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

American market volatility

By the end of the week, the ‘fear gauge,’ formally known as the CBOE Volatility Index (VIX), had risen to 13.30 at the end of the week, after registering 12.70 the previous week. The higher VIX reading suggests investors are expecting more volatility in the weeks ahead. Tensions in the Middel East, upcoming fourth quarter earnings and the likelihood the interest rate will remain at 5.5% past March are likely contributors to the higher VIX reading. The fear gauge remains in a historically low range and investors continue to be optimistic about the markets.

The VIX is a measure of the US investors’ expectation of short-term volatility based on S&P 500 options prices.

Consumer Sentiment Index

The preliminary measure of consumer sentiment for January, as indicated by the University of Michigan’s Consumer Sentiment Index (CSI), surged by 13% to 78.8, surpassing December’s reading of 69.7. Analysts had expected a reading of 70. On an annual basis, the CSI recorded a significant increase of 21.4%.

This marks the highest point for the CSI since July 2021. Following a significant upturn in December, the index has now risen by 29% since November, representing the largest two month increase since 1991. However, the CSI remains 20% lower than before the COVID-19 pandemic in 2020. The improved sentiment was seen in all five components of the CSI and spanned all age and income groups, as well as across the USA.

Consumer sentiment was buoyed by falling inflation, a strong labour market, and expectations of declining interest rates. That translates to cheaper groceries, more job security, and the possibility of lower interest rates – all things that could mean more spending and a stronger economy. The rising sentiment since November could provide some upward momentum for the American economy, which is good news for us investors. 😊

Retail Sales

The Commerce Department’s early numbers for December retail and food services sales surpassed expectations, showing a 0.6% increase compared to November’s 0.3% rise. Analysts had anticipated a 0.4% increase. On an annual basis, sales experienced a 5.6% boost compared to December 2022.

For the month, the biggest increase was in motor vehicle and parts dealers, up 1.1%, while the largest decrease was in gasoline, down 1.3%. Year over year, motor vehicle and parts dealers saw the biggest increase, up 10.3%, while gasoline sales dropped the most, down by 6.6%.

Excluding automobile sales, retail and food services sales grew by 0.4% in December, following a 0.2% increase the previous month.

In 2023, retail and food services sales were 3.2% higher than 2022, indicating robust growth despite economic challenges, such as rising interest rates. This growth was primarily driven by ‘non-store retailers’ and ‘Food services and drinking places,’ which increased by 9.7% and 11.1%, respectively.

The strong December retail sales data suggests that consumers remain resilient and are still spending money despite rising prices and higher interest rates. This could signal positive momentum for the economy in the near term.

In summary, the December retail and food services data provides mixed signals. While continued consumer spending is encouraging, the long-term impact of inflation remains a concern. Higher retail sales are beneficial for the US economy, boosting Gross Domestic Product, but they also exert upward pressure on inflation, reducing the likelihood of a rate cut. Higher interest rates not only pose challenges for consumers but also for us investors as they can limit growth opportunities for companies. ☹

Another US budget extension

Without all the drama of previous budget showdowns, the American Congress was able to pass a temporary budget. The bill was passed by the Senate, quickly followed by passage in the House of Representatives, before being sent to President Biden for approval. This is the third extension and simply pushes the deadline to approve a full fiscal 2024 budget out to early March.

The bill provides temporary funding at current levels for most agencies, with funding for some others (such as the Pentagon) extending slightly longer. Congress now has more time to negotiate and finalize the twelve individual appropriations bills that make up the full federal budget for the fiscal year.

If a budget had not been approved by the US House of Representatives and the US Senate, parts of the US government would have shut down. The Transportation agency, which covers air traffic controllers, the Food and Drug Administration are among the agency that would have been affected.

A month from now Congress will likely face another round of brinkmanship to produce a budget acceptable to both the Republican controlled House and the Democrat controlled Senate.

What is Investing?

Let me start by saying investing is not gambling. Gambling is a form of instant gratification. It is like playing a game of chance, with the house often having an advantage. Investing is about growing your money over time, like planting seeds and nurturing them to grow into a bountiful harvest. You can do this by putting your money to work in various assets, such as shares of companies (stocks), bonds, or even funds that hold a mix of these. While the hope is to see your investments grow in value, it is important to remember that there is also a chance they could lose some value. Different investments have different levels of risk, so finding the right ones for you depends on your goals and how comfortable you are with potential losses.

Remember, investing should be a long-term strategy, not a get-rich-quick scheme. By investing in well run companies, with strong financials, good track records, promising prospects and staying patient, you can increase your chances of achieving your financial goals over time. By spreading your investments across companies in different sectors, with a mix of growth, dividend paying and defensive companies (those that provide essential products or services, such as utility companies) can help mitigate the impact of losses in any one area.

Now that we know the economic news for the past week, let’s see what impact it had on the stock markets this past week….

Weekly Market Review

Monday: in the US, American exchanges were closed for Martin Luther King Jr. Day.

In Canada, trading was light as investors waited for tomorrow’s CPI report to hopefully reveal clues on the BoC’s interest rate outlook. In trading, the Toronto Stock Exchange Composite Index (TSX) edged higher, led by Basic Materials (miners and fertilizer manufacturers) and Healthcare. Consumer Cyclicals and Financials suffered the biggest losses.

Tuesday: Investor optimism took a hit after a Fed official said, “I see no reason to move as quickly or cut as rapidly as in the past,” causing all four major North American indexes to end lower.

In Canada, shaken investor optimism, lower oil and commodity prices, and the latest inflation report showing inflation rose in December all weighed on the TSX. In trading, Consumer Cyclicals and Telecommunications Services posted the biggest daily gain, with Basic Materials and Energy dropping the most.

In the US, the shortened week began with a thud. All three American indexes ended the day in the red – the Nasdaq Composite Index (Nasdaq), the S&P 500 Index (S&P) and the Dow Jones Industrial Average (DJIA). The Nasdaq was the only index to even break into the green, even if it was only temporary. In trading, Telecommunications Services was the only sector to end in the green, while Energy and Basic Materials suffered the biggest declines.

Wednesday: the markets fell as investors unwound bets that the Fed would lower interest rates starting in March. Oil prices reversed course at mid day to end higher as Middle East supply concerns outweighed weak economic data out of China could lead to lower demand.

In Canada, the TSX suffered its biggest one day fall since mid October as investor confidence in early rate cuts continues to wane. In trading, it was day of sector wide declines. Consumer Cyclicals and Consumer Staples dropped the least while Basic Materials and Utilities incurred the biggest declines.

In America, US retail sales came in higher than expected, further dampening the possibility of an early rate cut by the Fed. It was a day of broad-based declines as all sectors ended lower. Healthcare and Consumer Staples dropped the least while Utilities and Basic Materials dropped the most.

Thursday: an artificial intelligence (AI) led rally in technology companies helped the markets rebound into positive territory. The rally came after two straight days of losses as investors are coming to the conclusion there is unlikely to be a rate cut in March. Oil prices rose on forecasts of higher demand by the International Energy Agency (IEA). The freezing weather gripping North America also helped to draw down oil reserves in the US.

In Canada, the TSX advanced on gains led by Consumer Staples and Industrials. The only sectors to end lower were Healthcare, Technology and Utilities.

In the US, despite losing ground the previous two days, the S&P approached a record high today on the strength of a rally in semiconductor companies. It likely would have set a record if not for one Fed member who said he did not think the Fed would lower the interest rates until the second half of the year. In trading, Technology and Industrials were the top performers, while Utilities and Healthcare were the only two American sectors to decline.

Friday: optimism that the US economy would have a soft landing, which is lowering inflation without sending the economy into a recession, propelled all four indexes into positive territory.

In Canada, November retail sales came in below expectations, suggesting the Canadian economy is slowing. Otherwise, it was a case of a rising tide lifts all boats as the TSX was lifted by investor optimism from the US. In trading on Bay Street, Technology and Financials posted the biggest gains, while Consumer Staples and Energy were the only two sectors to lose ground.

In the US, the ongoing rally in technology companies, especially those associated with AI, combined with strong economic news, and rising consumer sentiment sent the S&P and DJIA to record closing highs. In trading on Wall Street, Technology and Financials were the big winners, while Consumer Staples and Utilities were the only sectors to end lower.

Weekly Market and Portfolio Review

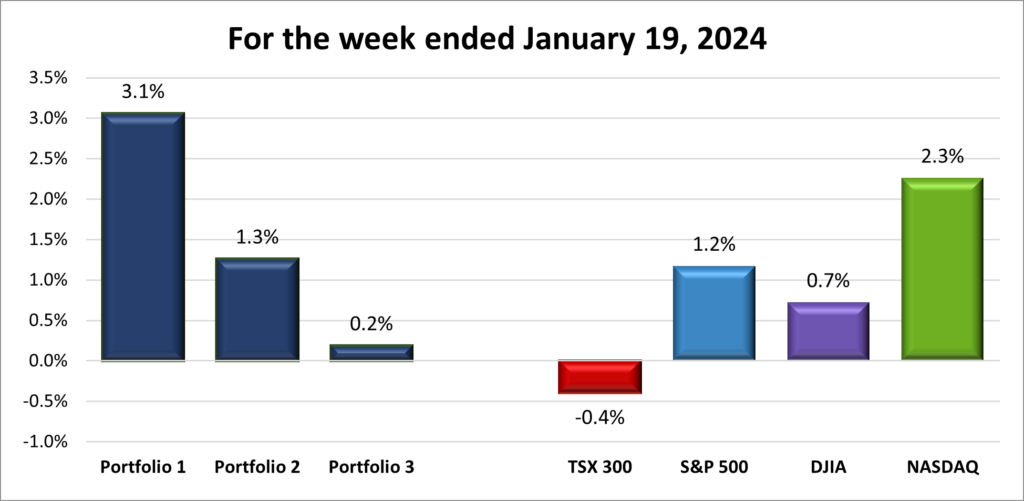

For the week, the TSX (SPTSX) slipped 0.4%, the S&P 500 (SPX) rose 1.2%, the DJIA (INDU) gained 0.7% and the Nasdaq (CCMP) advanced 2.3%.

| Index | Weekly Streak |

| TSX: | 1-week losing streak |

| S&P: | 2-week winning streak |

| DJIA: | 2-week winning streak |

| Nasdaq: | 2-week winning streak |

![]() As shown in the chart above, a slow start to the week saw a rebound that sent the American indexes higher and the TSX falling just short of the breakeven line.

As shown in the chart above, a slow start to the week saw a rebound that sent the American indexes higher and the TSX falling just short of the breakeven line.

Buoyed by lower jobless claims, resilient retail sales and soaring consumer sentiment (its biggest two month jump since 1991), the American indexes extended their winning streaks to two weeks. A rally in technology companies, especially the Magnificent 7 group of companies (Alphabet (NASD: GOOGL), Amazon (NASD: AMZN), Apple (NASD: AAPL), Meta (NASD: META), Microsoft (NASD: MSFT), Nvidia (NASD: NVDA) and Tesla (NASD: TSLA)), propelled the indexes higher. The S&P and DJIA each set record highs at the end of the week, while the Nasdaq closed at a two year high. Interestingly, Apple and Microsoft are members of all three indexes, indicating their sizable roles in the US economy and their appeal to a wide range of investors. When the the Magnificent 7, especially Apple and Microsoft, are moving, the indexes tend to follow along. This week the direction was upward. 😊

Speaking of being dragged along, the TSX was influenced by the overall market sentiment in the US. However, it was hampered by its smaller technology component (8.7% as of December 29, 2023) so it did not receive the same boost from the rally in technology companies. The TSX has a large resource sector, including energy and basic materials companies which account for 28% of the TSX, which acted as a drag on the index.

Hopefully the momentum generated at the end of this past week will carry over and all four indexes will end in positive territory.

| Portfolio | Weekly Streak |

| Portfolio 1: | 2-week winning streak |

| Portfolio 2: | 2-week winning streak |

| Portfolio 3: | 2-week winning streak |

![]() As shown in the chart below, it was another week of gains for each of the three portfolios, extending their respective weekly winning streaks to two.

As shown in the chart below, it was another week of gains for each of the three portfolios, extending their respective weekly winning streaks to two.

Portfolio 1 had the best week of the three portfolios and outperformed the Nasdaq, the best of the indexes. The portfolio was primarily lifted by its Magnificent 7 companies. None of the companies in the portfolio saw significant (share price changes greater than 10%) upward movement. However, there were significant drops by Rivian (NASD: RIVN) down 17%, and Celsius Holdings (NASD: CELH) down 12.8%.

Portfolio 2 generally had a positive week outperfoming the S&P. It was led by its tehcnology companies. However, it was held down by a near 10% decline in the share price of energy company Crew Energy (TSE: CR).

Finally, Portfolio 3 had no significant ups or downs, however, a big rebound on Friday boosted the portfolio into the win column for the week. A surge in the share prices of the technology companies overcame declines in resource companies Alvoptero Energy (TSXV: ALV), Lithiium Americas (TSE: LAC) and Lithium America Argentina (TSE: LAAC). The gain was not as big as the increase of the other two portfolios but a win is still a win. 😊

Companies on the Radar

No new companies came on my radar this past week. For now, my Radar List consists of the five companies listed below:

No new companies came on my radar this past week. For now, my Radar List consists of the five companies listed below:

- Equitable Bank (TSE: EQB), a mid sized Canadian bank that provides financial services to consumers and businesses.

- McDonald’s (NYSE: MCD), the large sized American fast-food chain.

- Celestica Inc. (TSE: CLS), a medium sized Canadian company that manufactures electronic products and provides supply chain services to companies around the world.

- Kinaxis (TSE: KXS), a Canadian mid sized company that provides cloud based supply chain solutions to customers around the world.

- Lumine Group (TSE: LMN), a young Canadian mid sized company that acquires and strengthens communications and media software companies.

The Radar Check was last updated January 19, 2024.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended January 19, 2024: UP ![]()

- Apple did what was once unthinkable and offered a discount on its newest iPhones. Before you go rushing out to buy a new iPhone 15, you should know the lower price is only available in China, and only for a limited time. China is Apple’s second largest smartphone market and sales fell 30% in 2023 as China’s Huawei introduced its latest smartphones.

More bad news for Apple, their latest Apple Watch models have been banned from sale in the US while the company fights a legal battle over technology used in their Series 9 and Ultra 2 watches. The dispute is over patents for the blood oxygen measurement feature. Apple is expected to disable any feature related to the disputed technology until the dispute is resolved. - Afte lowering prices on their Model Y electric vehicles (EV) in China, Tesla announced price reductions in the European market.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSE: DIR.UN)

Decisive Dividend (TSE: DE)

Andlauer Healthcare Group Inc (TSE: AND)

US $

BSR Real Estate Investment Trust (TSE: HOM.UN)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended January 19, 2024: UP ![]()

- A fight for control of Walt Disney’s (NYSE: DIS) board of directors is shaping up as a battle of the incumbents against activist investors led by Trian Fund Management. Trian claims it will bring brand expertise to the company, restore “the magic” to the company and focus on building shareholder value. Disney’s current earnings per share remain below where they were ten years ago. A rise in share price would make this shareholder happy. 😊

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSE: DIR.UN) DRIP

SmartCentres Real Estate Investment Trust (TSE: SRU.UN)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week, except for per share data.

Portfolio 3

Portfolio 3 for the week ended January 19, 2024: UP ![]()

- Cloudflare (NYSE: NET) made the news this past week, but for the wrong reason. An employee filmed her firing by two Cloudflare representatives. She was fired via a video call and the two company representatives failed to explain why she was being let go and why her manager was not present. The video of the firing went viral and will probably go down as one of the best examples of how not to let people go.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Alvopetro Energy Ltd (TSE: ALV)

SmartCentres Real Estate Investment Trust (TSE: SRU.UN)

TD U.S. Equity Index ETF (TSX: TPU)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.