Riding Out the Emotional Rollercoaster of Market Meltdowns

The sell-off at the start of the week wiped out the past 12 months of gains, with stocks edging closer to bear market territory. Since the previous Thursday, US markets saw their steepest three-day decline since 1987 – and before that, not since World War II. Meanwhile, Canada’s TSX Composite Index (TSX) experienced its sharpest drop since the early days of the COVID-19 pandemic. This time, though, the damage was self-inflicted—and, frankly, far from fun. ☹

Investing isn’t just about numbers – it’s also about managing your emotions, especially during turbulent times like these. Over the past few days, we’ve seen another sharp market drop that’s stirred up everything from fear and frustration to cautious optimism. So how should we respond? And how does this moment compare to past market meltdowns?

Looking back, history gives us some helpful perspective. In March 2020, as the COVID-19 crisis hit, markets plunged 34% in just a few weeks. Headlines were full of panic. But even amid all the fear, some investors saw opportunities – buying into sectors like tech and healthcare, which would later lead the recovery.

That wasn’t the first time panic gripped the markets. Go back to 2008, and the story is even more dramatic. The financial system itself was at risk, and investor confidence was shattered. Many sold off everything and locked in their losses. Others who held on – or even bought during the depths – ended up doing very well as the recovery unfolded.

And this time we faced another sharp decline, fuelled by what The New York Times called “the dumbest trade war ever,” that have led to growing geopolitical tensions. Emotions are running high. Some investors were rushing to sell. Others were cautiously looking for chances to “buy the dip.”

I’ve been through moments like this before. During the 2008 crisis, I saw Canadian bank stocks getting hammered – even though there was nothing fundamentally wrong with them. They were simply caught up in the broader market panic. I bought them at steep discounts, and it turned out to be a smart move. Fast forward to the COVID crash, and I’ll admit – my first reaction was panic. I had more money invested by then, so the losses felt bigger. But I reminded myself that selling would only lock in the damage. Within a week, markets started bouncing back, and I began picking up some of the hardest-hit names. Over the next 18 months, the markets soared, and all three portfolios recovered – and then some. If I’d sold during the panic, I would’ve missed all of it.

Getting back to the present: Just as feelings of doom and gloom were settling in—at least for those not buying the dip—President Trump hit pause on the US tariffs. Saying markets responded positively would be an understatement. The Nasdaq Composite Index (Nasdaq) surged over 12%, logging one of its biggest single-day gains since 2008. The S&P 500 Index (S&P) jumped 9.5%, the Dow Jones Industrial Average (DJIA) climbed 7.8%, and the TSX rose more than 5%.

This sharp reversal reflects a wave of investor relief, as the pause eased fears of escalating trade tensions and their economic fallout. That said, tariffs on Chinese imports were still hiked to 145%, which could complicate things down the road. But the key takeaway? If you had panicked and sold during the downturn, you would’ve missed this rebound—and it may now cost you more to buy back the same stocks.

So what’s the takeaway here? Emotional decisions rarely lead to long-term success. Selling in fear usually means locking in losses. Instead, use market meltdowns as a chance to reassess your strategy. If you believe in the fundamentals of the companies you own, staying the course might be the best move. And if you’ve got dry powder (also known as extra cash available), corrections like these can offer a shot at picking up great companies at lower prices.

At the end of the day, investing is a long game. Markets rise, fall, and rise again. Staying patient, sticking to your plan, and not letting fear take the wheel – that’s what builds wealth over time.

So, with that perspective in mind, let’s take a look at what actually unfolded in the markets this past week – and how it all played out across the portfolios.

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Canadian market volatility

The S&P/TSX 60 VIX (VIXC), which tracks expected volatility in the Canadian market, opened the week at 18.32 before quickly climbing above 20. It kept rising throughout the week – spiking above 30 after the 90-day tariff pause was announced, and then surging past 40 the next day as the US-China trade war escalated. By Friday, it had eased slightly but still closed at a high 32.78.

For those unfamiliar with the VIXC, think of it as the Canadian market’s stress meter. A reading below 10 signals strong investor confidence, 10 to 20 is business as usual, and anything above 20 suggests uncertainty is starting to take hold. With the latest reading, it’s safe to say uncertainty has definitely settled into the Canadian market.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Federal Open market Committee minutes

This week, the Federal Reserve released minutes from its Federal Open Market Committee (FOMC) meeting on March 18–19, offering a look at what policymakers were thinking and giving us a better sense of where interest rates might be headed – and how they’re viewing the economy.

The minutes revealed the reasoning behind the Fed’s decision to keep its target interest rate range steady at 4.25% to 4.50%. That move was driven by a mix of solid economic activity, low unemployment, and still-elevated inflation. But the minutes also flagged a key source of new uncertainty: US tariffs and their potential ripple effects on inflation and growth.

The Fed now expects GDP growth to slow to 1.7% in 2025, down from its 2.1% estimate back in December. Unemployment is expected to stay around 4.4%, and inflation is still projected to gradually move toward the 2% target – though tariffs could muddy that path by raising prices and slowing trade.

In short, the Fed is walking a tightrope. They’re trying to cool inflation without slamming the brakes on growth or triggering a surge in unemployment. That’s why they’re holding rates steady and taking a cautious, wait-and-see approach. They want time to assess the impact of tariffs and other risks before making any moves.

Bottom line: No rate cuts just yet, but no surprises either. The Fed’s keeping its options open, waiting to see how things play out. If inflation continues to ease and the economy stays on steady footing, cuts could still be in the cards later this year. In the meantime, growing concerns about a tariff-fuelled slowdown have many betting the Fed will need to step in before too long.

Consumer price Index (CPI)

Inflation finally gave us a bit of breathing room. The March CPI report showed that prices cooled more than expected, offering some welcome relief to both consumers and investors. Headline inflation – which includes all components – fell 0.1% for the month, following a 0.2% increase in February. Analysts had been expecting a modest 0.1% rise. On a yearly basis, inflation slowed to 2.4%, down from 2.8% and below the forecasted 2.6%. That’s the lowest annual rate since September 2024.

Some of the biggest monthly shifts came at the gas pump and in home energy. Gasoline prices plunged 6.3%, helping to ease overall inflation. Compared to last year, gas is now down 9.8%. Meanwhile, ‘Utility gas services’ – used to heat homes – rose 3.6% in March and are up 9.4% year-over-year.

Housing costs, one of the stickier components of inflation, also continued to cool. Shelter rose 0.2% for the month, down from 0.3% in February. On a yearly basis, shelter inflation eased to 4.0%, from 4.2% the month before.

Core CPI – which strips out the more volatile food and energy categories and is often seen as a better gauge of underlying inflation – also came in softer than expected. It rose just 0.1% in March, half the pace analysts had predicted, and eased to 2.8% year-over-year, down from 3.1% in February. It’s another encouraging sign for the Fed as it tries to bring inflation closer to its 2% target without slowing the economy too much.

Still, the road ahead isn’t without bumps. While this report shows clear progress, it reflects price trends before the latest tariffs were introduced – so it’s looking backward, not forward. The 10% tariffs already in place could add upward pressure in the months ahead, especially once the current 90-day pause on higher tariffs expires. For now, though, this is a win in the inflation fight.

Consumer Sentiment Index (CSI)

The University of Michigan’s preliminary CSI for April 2025 dropped sharply to 50.8 – its lowest level since June 2022 – down from 57.0 in March and well below economists’ expectations of 54.5. That’s a 10.9% decline from last month and a massive 34.2% drop from April 2024, when the index stood at 77.2.

The Current Economic Conditions index slid 11.4% to 56.5, down from 63.8 in March and 28.5% lower than April 2024’s reading of 79.0, reflecting rising concerns about personal finances and the broader economic outlook. Meanwhile, the Index of Consumer Expectations fell 10.3% to 47.2, down from 52.6 last month and nearly 38% lower year-over-year – highlighting deepening pessimism about the future.

Inflation expectations are also back in the spotlight. Consumers now expect prices to rise 6.7% over the next year, up from 4.9% in March – the highest level since 1981. The five-year inflation outlook also ticked up to 4.4% from 4.1%.

The report pointed to rising trade tensions – especially the surge in tariffs between the US and China – as a major driver of the souring mood. With consumers increasingly worried about business conditions, personal finances, and the job market, talk of a potential recession is gaining momentum. It seems consumers are now on the same page as investors – tariffs are expected to leave lasting damage on the economy.

American market volatility

The CBOE Volatility Index (VIX), often called the market’s “fear gauge,” opened the week at a sky-high 60.13, reflecting extreme investor anxiety as the second week of President Trump’s global tariff war kicked off. The VIX gradually eased into the 40s, but spiked back into the mid-50s on Wednesday when the US raised tariffs on China to 104%. However, after the announcement of a 90-day suspension of reciprocal tariffs on most US trading partners, the index dropped back below 40. It stayed near the 40-point mark for the rest of the week, with a few temporary jumps above 50, before dipping into the 30s and closing the week at 37.56.

For those new to the VIX, think of it as the stock market’s stress meter. A reading below 12 signals calm waters, 12 to 20 reflects normal market swings, and anything above 20 suggests rising uncertainty. With the VIX staying above 30 for another week, it’s clear the markets remain on edge.

Weekly Market and Portfolio Review

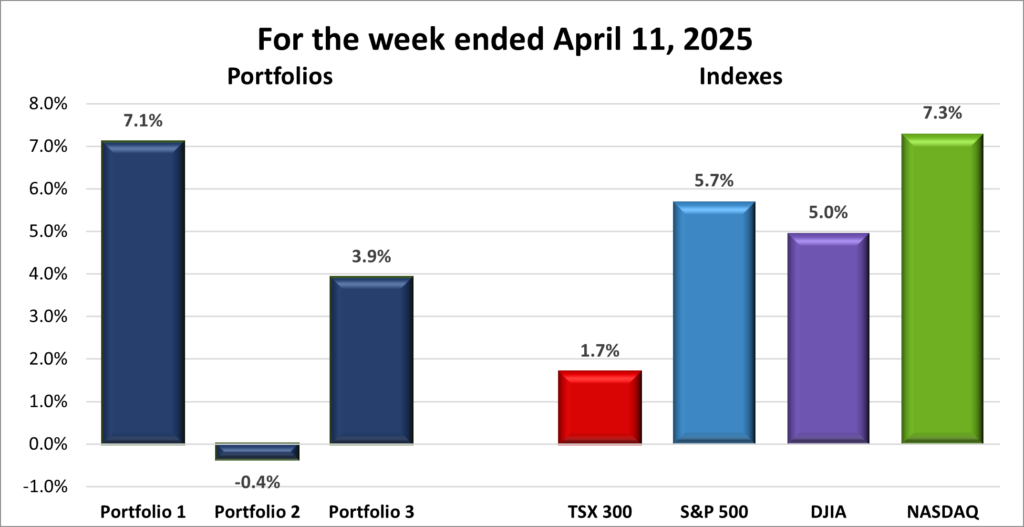

For the week, the TSX (SPTSX) added 1.7%, the S&P 500 (SPX) jumped 5.7%, the DJIA (INDU) gained 5.0% and the Nasdaq (CCMP) surged 7.3%.

| Index | Weekly Streak |

| TSX: | 1 – week winning streak |

| S&P: | 1 – week winning streak |

| DJIA: | 1 – week winning streak |

| Nasdaq: | 1 – week winning streak |

![]() The markets took a wild ride this past week, as seen in the weekly progress chart above, as escalating trade tensions sent shockwaves through global markets and whipsawed the four indexes. Despite a brutal start, the S&P and DJIA logged their best weeks since 2023, while the Nasdaq notched its strongest since 2022.

The markets took a wild ride this past week, as seen in the weekly progress chart above, as escalating trade tensions sent shockwaves through global markets and whipsawed the four indexes. Despite a brutal start, the S&P and DJIA logged their best weeks since 2023, while the Nasdaq notched its strongest since 2022.

The S&P stumbled out of the gate, dropping below 5,000 for the first time in nearly a year. It was the steepest four-day slide since the index’s inception in the 1950s, pushing it into bear market territory – down more than 20% from its record high. All three major US indexes fell to their lowest levels in over a year, rattled by growing fears of an economic slowdown and inflation creeping into North America, fuelled by an intensifying tariff battle.

Wednesday morning brought a glimmer of hope with rumours of a possible delay in US tariffs. But that optimism quickly vanished after the US raised tariffs on Chinese imports to 125%, and China fired back with its own hikes. Then, a surprise twist: the US paused most reciprocal tariffs for 90 days and replaced them with a flat 10% rate. Markets surged on the news, delivering one of the strongest one-day rallies in decades. The S&P jumped 9.5% – its best day since the 2006 financial crisis. The Nasdaq soared 12.2%, its second-best day ever, while the more conservative DJIA climbed 7.8%.

But the rally didn’t last. The very next day, the US hiked tariffs on China again – this time to 145% – turning up the heat in what’s starting to look like a full-blown trade war between the world’s two largest economies.

Even a better-than-expected inflation report on Thursday wasn’t enough to calm investor nerves. With most tariffs still in place and the 90-day pause looking more like a breather than a breakthrough, uncertainty only increased.

On Friday, markets flipped once more – boosted by strong first-quarter earnings from a few major US banks – and ended higher to cap off a chaotic week. This came despite China hiking tariffs on US imports to 125% and consumer sentiment falling to its lowest level since June 2022, when markets were last in correction territory. The late-week rally nudged the indexes into the green – a bit of a surprise, given how the week began.

Back in January, analysts were expecting the American economy to grow 2%. Now, many are warning a recession could be looming. With corporate earnings likely to take a hit from prolonged trade disruptions, the risk of a broader economic pullback is rising. And when selloffs like this start to snowball, they can tip economies into recessions that take years to recover from.

In Canada, markets mirrored their American counterparts. The TSX surged 5.4% on Wednesday during the global rally, dropped 3.0% the next day, then bounced back 2.5% on Friday – ending the week slightly higher.

Economically, cracks are beginning to show. After two months of tariff threats, Canada shed 33,000 jobs in March – the worst jobs report in over three years – and that’s before the full impact of US tariffs kicked in. With prices set to rise as the trade war escalates, the BoC is now in a tough spot: trying to tame inflation while also supporting an economy starting to take hits.

While billionaires will likely emerge unscathed, everyday consumers – like us – might not be so lucky. A prolonged slowdown could bring job losses, stagnant wages, and shrinking purchasing power. With the road ahead still murky, this kind of market volatility is bound to ripple through the broader economy for some time. And after the week we’ve just had, it might only take a single tweet to flip the script all over again. 😊

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week winning streak |

| Portfolio 2: | 3 – week losing streak |

| Portfolio 3: | 1 – week winning streak |

![]() I’ve got to admit – at the start of the week, I was fully expecting to be seeing red across all three portfolios. By the end of Thursday, it could’ve gone either way, with the markets getting whipsawed around by trade tensions and volatility. But thanks to the big rally on Friday, two of the three portfolios ended the week with gains, while the third fell just short of positive territory, as you can see in the chart below. A surge in tech stocks – especially the heavyweight technology companies – gave things a serious boost.

I’ve got to admit – at the start of the week, I was fully expecting to be seeing red across all three portfolios. By the end of Thursday, it could’ve gone either way, with the markets getting whipsawed around by trade tensions and volatility. But thanks to the big rally on Friday, two of the three portfolios ended the week with gains, while the third fell just short of positive territory, as you can see in the chart below. A surge in tech stocks – especially the heavyweight technology companies – gave things a serious boost.

Portfolio 1 came out on top with a 7.1% gain for the week. It was a huge turnaround: last week, only 6% of the holdings managed to post a gain, while this week, 79% finished in the green. Big winners included CrowdStrike (NASD: CRWD) and Nvidia (NASD: NVDA), both up 25%, Celestica (TSE: CLS) up 24%, Sea Limited (NYSE: SE) and Lattice Semiconductor (NASD: LSCC) both up 17%, Cloudflare (NYSE: NET) up 16%, and Walmart (NYSE: WMT) up 15%. Grab Holdings (NASD: GRAB) and Shopify (TSE: SHOP) each climbed 14%, while Amazon (NASD: AMZN) and Magnite (NASD: MGNI) added 13%, Apple (NASD: AAPL) rose 11%, and Alphabet (NASD: GOOGL) rounded things out with a 10% gain.

Portfolio 2 fell just short, slipping 0.4%. Honestly, with 82% of the holdings posting gains, I expected it to end in the green. It felt odd, so I double-checked – but unfortunately, a few of those gainers only edged up by a penny or two or were very small positions. The drops in the oil stocks ended up outweighing the gains in tech. Top performers included Guardant Health (NASD: GH) up 13%, Birkenstock (NYSE: BIRK) up 12%, and Take-Two Interactive (NASD: TTWO), Airbnb (NASD: ABNB), and MongoDB (NASD: MDB) each up 11%. Microsoft (NASD: MSFT) also pitched in with a 10% gain.

Portfolio 3 was the Goldilocks pick this week – right in the middle of the pack with a 3.9% weekly gain. It also saw the highest percentage of winners, with 91% of holdings ending the week in the green. Standouts included Vertiv Holdings (NYSE: VRT) up 27%, Adyen NV (OTCM: ADYEY) up 17%, Cloudflare up 16%, Evolution AB (OTCM: EVVTY) up 15%, Shopify up 14%, Magnite up 13%, and both goeasy (TSE: GSY) and Microsoft up 10%.

After the past few rocky weeks, it’s nice to see the portfolios back on the winning side. Not a bad week at all! 😊

Companies on the Radar

With the implementation of tariffs on all of America’s trading partners – even some penguins on an island off Antarctica – and counter-tariffs flying back in return, markets have been cratering, and I haven’t exactly had the time (or appetite) to scout for new companies to invest in. I’ve mostly been in a holding pattern, watching to see if any of the stocks I already own have dropped far enough to start looking like a deal.

With the implementation of tariffs on all of America’s trading partners – even some penguins on an island off Antarctica – and counter-tariffs flying back in return, markets have been cratering, and I haven’t exactly had the time (or appetite) to scout for new companies to invest in. I’ve mostly been in a holding pattern, watching to see if any of the stocks I already own have dropped far enough to start looking like a deal.

When that happens, my first move is to figure out whether the selloff is tied to the actual business or just overall market sentiment. If it’s the latter – if the company has limited tariff exposure and is just caught up in the broader panic – it goes straight to the top of my watchlist. Think of it as the market throwing the baby out with the bathwater.

From there, I do one last check: does the stock offer a solid dividend (ideally 3%+)? If it does, that income stream helps cushion the ride and takes some of the sting out of short-term volatility. Dividend stocks can also reduce overall portfolio risk and add a bit of stability – especially when markets are in one of their moods.

For now, my radar list still includes these six companies:

- Barrick Gold Corporation (TSE: ABX): A large-cap Canadian company that is one of the world’s largest gold and copper miners, with operations across the globe. A go-to for gold exposure.

- Brookfield Corporation (TSE: BN): A large-cap Canadian heavyweight in alternative asset management and real estate investing. Big, diversified, and built for the long haul.

- Dollarama (TSE: DOL): A growing large-cap Canadian discount retailer that’s also expanding into South America. With a recession expected in Canada, discount retailers are seeing an increase in business.

- goeasy Ltd.: A mid-cap Canadian company offering non-prime leasing and lending services. Higher risk, but high potential if they manage credit cycles well.

- iA Financial Corporation (TSE: IAG): A large-cap Canadian financial services firm with a solid insurance business in both Canada and the US. Steady and reliable.

- LPL Financial Holdings Inc. (NASD: LPLA): A large-cap US firm providing a brokerage and advisory platform for independent financial advisors. Benefiting from long-term trends in wealth management.

As always, these are not buy recommendations – be sure to do your own research and make decisions that align with your personal financial goals!

The Radar Check was last updated April 11, 2025.

That’s a wrap for this week—see you next time! Happy investing!