How Jobs and Prices Drive Rate Cuts

Recently the US labour market has been flashing signs of weakness, and this week’s revisions pushed job numbers even lower. That matters because the strength of the labour market often sets the tone for the economy – more jobs usually mean more spending, while slower job growth suggests things may be cooling. Against that backdrop, attention this past week turned to two key inflation reports: the Producer Price Index (PPI) and the Consumer Price Index (CPI).

The PPI measures price changes at the wholesale level – what businesses are paying for things like raw materials and supplies. If those costs rise, companies may try to pass them on to consumers. CPI, on the other hand, tracks what households actually pay for everyday goods and services like groceries, rent, and gas. For example, PPI is like the cost of flour for a bakery, while CPI is the price of the bread you buy at the store. If the cost of flour (PPI) goes up, bakeries may eventually raise the price of bread (CPI) to cover their higher expenses. Together, these two reports show us how inflation is moving through the system – from businesses to consumers.

This week’s results painted a mixed picture. PPI came in softer than expected, signalling cooling wholesale inflation and giving the Fed some breathing room to ease, especially as the labour market softens. CPI, however, told a different story: headline, or all items, inflation ran hotter than forecast in August, even as core CPI held steady.

That tug-of-war leaves the Fed with a tricky balancing act. Its “dual mandate” calls for both stable prices (keeping inflation in check) and maximum employment. For the past few years, the Fed has focused on bringing inflation down to its 2% target, but with the labour market showing signs of weakening, the emphasis is now shifting toward jobs. Cutting interest rates makes borrowing cheaper, encouraging spending and investment, which can help businesses hire more. As employment reports continue trending lower through revisions, many expect a rate cut next week. The question is how big – a 0.25% move looks more likely than the 0.5% cut some were hoping for. Either way, it should give markets a welcome boost.

Now that we understand the tug-of-war between jobs and inflation, and with the Fed’s next moves on most investor’s mind, let’s see how the markets reacted this past week and how my three portfolios held up.

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Canadian Market Volatility

Canada’s volatility gauge, the S&P/TSX 60 Volatility Index (VIXC), opened the week at 10.3 and spent most of the time drifting between 10 and 11. The only drama came midweek, when it briefly spiked above 15 after Ottawa announced five major projects would be eligible for fast-track approval. The jump was short-lived, and the index quickly slid back down, finishing at 10.72.

Think of the VIXC as Canada’s version of a “fear gauge.” It rises when investors get jittery over uncertainty or surprise news and falls when markets settle down. With the index ending near its lows, sentiment leaned more toward calm than caution.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Consumer Price Index (CPI)

The Bureau of Labor Statistics’ August CPI report showed inflation running a little hotter than expected. Headline, or all items, CPI rose 0.4% on the month, above the 0.3% forecast and up from July’s 0.2%. On a yearly basis, prices are 2.9% higher, compared with 2.7% in July.

Gasoline led the monthly increases with a 1.9% jump, while utility gas service dropped 1.6%. Looking at the past year, utility gas has surged 13.8%, while gasoline has actually fallen 6.6%. Shelter costs – covering mortgages, rent, and homeowner expenses – climbed another 0.4% in August, continuing to put steady pressure on households, though the annual pace edged slightly lower to 3.6%.

Core CPI, which strips out food and energy, rose 0.3% for the month and held at 3.1% year-over-year, right in line with forecasts.

For the Fed, this report makes the balancing act even trickier. The labour market is showing cracks, arguing for cuts, but inflation’s persistence may slow down how quickly or how much they ease. Rate cuts are still likely, but the timing just got more complicated.

Consumer Sentiment Index (CSI)

The latest University of Michigan consumer sentiment report showed confidence slipping again, with the index dropping to 55.4 in September from 58.2 in August, its lowest level since May and well below the expected 58.0. That marks a 4.8% decline month over month and a steep 21% drop from a year ago. Looking closer, the Current Economic Conditions Index, which gauges how people feel about their finances and job security right now, edged down 0.8% to 61.2, a 3.3% decline from last year. The bigger hit came in the Expectations Index, which looks ahead six months. It sank to 51.8 from 55.9, a 7.3% monthly slide and down more than 30% year over year.

The drop in sentiment was sharper than analysts expected and was prevalent in lower- and middle-income households. Many cited worries about weakening business conditions, a weakening job market, and inflation pressures. Trade policy is also weighing heavily – about 60% of respondents mentioned tariffs without being asked. Sentiment has only partly recovered since April, when President Trump’s announcement of sweeping tariffs on imported goods sent confidence tumbling.

American Market Volatility

The CBOE Volatility Index (VIX), often called the “fear gauge” for US stocks, opened the week at 15.21 and drifted steadily lower, closing at 14.76. With no major economic surprises to shake things up, markets stayed calm and played out much as investors expected. For anyone new to the VIX, think of it as a quick snapshot of market nerves – readings between 12 and 20 usually signal calm waters, while anything above 20 suggests traders are bracing for turbulence. The higher it climbs, the more uncertainty is being priced in.

Weekly Market and Portfolio Review

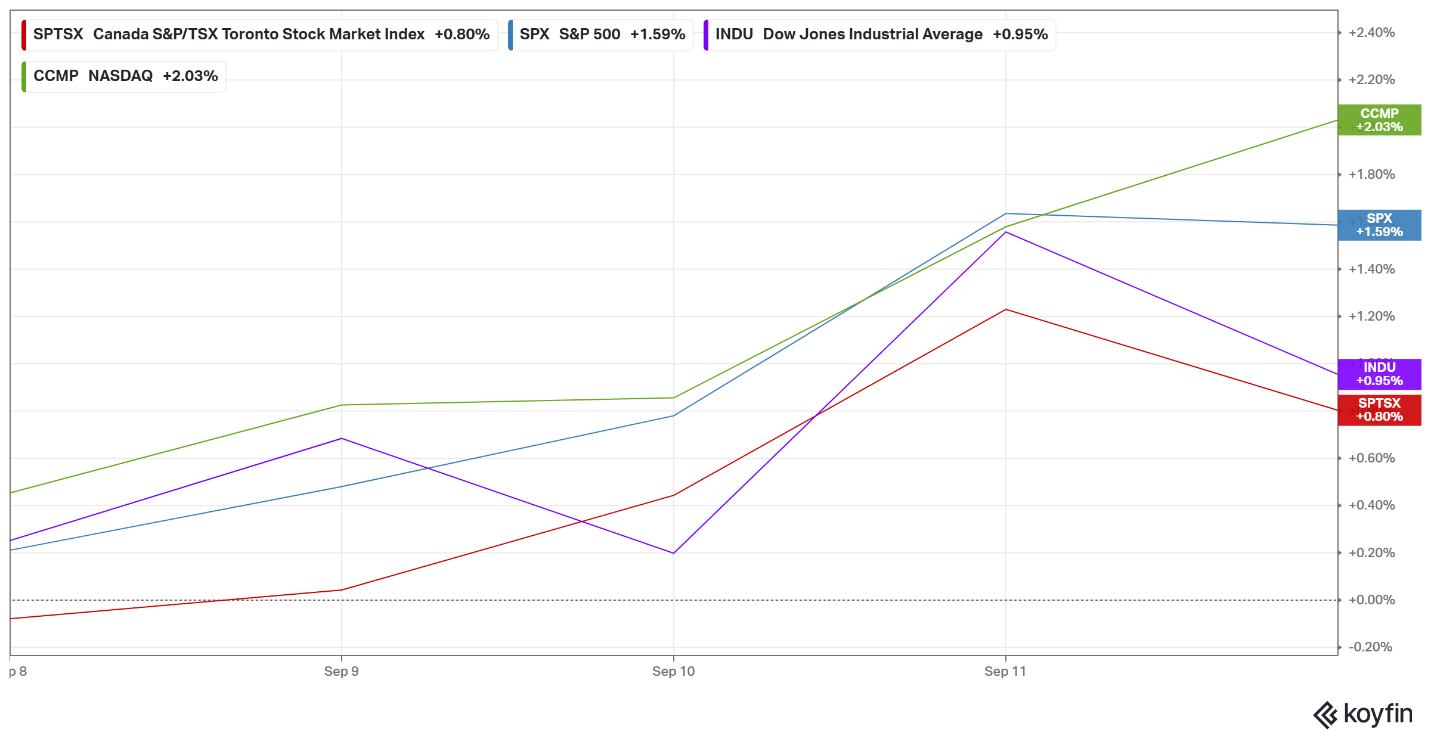

For the week, the TSX (SPTSX) rose 0.8%, the S&P 500 (SPX) advanced 1.6%, the DJIA (INDU) grew 1.0% and the Nasdaq (CCMP) surged 2.0%.

| Index | Weekly Streak |

| TSX: | 6 – week winning streak |

| S&P: | 2 – week winning streak |

| DJIA: | 1 – week winning streak |

| Nasdaq: | 2 – week winning streak |

![]() It was a record-setting week for the markets, with all four major indexes hitting fresh all-time highs. The Toronto Stock Exchange Composite Index (TSX) snapped its eight-day winning streak on Monday but quickly bounced back, posting three straight record closes before easing on Friday. In the US, the S&P 500 (S&P) and Nasdaq Composite Index (Nasdaq) each set multiple new highs, with the Nasdaq crossing 22,000 for the first time during a four-day run to end the week. The Dow Jones Industrial Average (DJIA) also joined in the record breaking fun, breaking above 46,000 for the first time to set its own record high and help snap its two-week losing streak.

It was a record-setting week for the markets, with all four major indexes hitting fresh all-time highs. The Toronto Stock Exchange Composite Index (TSX) snapped its eight-day winning streak on Monday but quickly bounced back, posting three straight record closes before easing on Friday. In the US, the S&P 500 (S&P) and Nasdaq Composite Index (Nasdaq) each set multiple new highs, with the Nasdaq crossing 22,000 for the first time during a four-day run to end the week. The Dow Jones Industrial Average (DJIA) also joined in the record breaking fun, breaking above 46,000 for the first time to set its own record high and help snap its two-week losing streak.

The week was driven by a mix of economic, geopolitical, and corporate news. Treasury Secretary Scott Bessent warned that the US might have to return some tariff revenues if the Supreme Court strikes them down, following an appeals court ruling that found most of them illegal. Meanwhile, oil prices ticked higher as tensions rose in the Middle East and Europe, with Israel targeting Hamas leadership in Qatar and Russia intensifying drone strikes in Ukraine.

On the economic front, investors grew more confident about a Fed rate cut next week. A downward revision to US labour data confirmed the job market is weaker than expected, with weekly jobless claims climbing to their highest since October 2021. Inflation was mixed: consumer prices came in slightly hotter than expected, while wholesale prices cooled, suggesting tariffs may be trickling down to consumers. With jobs softening and inflation steady, many now see a rate cut as all but certain.

Adding fuel to the rally was Oracle (NYSE: ORCL). Despite lacklustre earnings, the company forecast a massive revenue boost tied to surging demand for its cloud services from big-name artificial intelligence (AI) clients. The stock soared more than 35%, its best single-day gain in over 30 years, reigniting excitement around the AI build-out.

Back in Canada, the TSX kept momentum going, supported by growing expectations that both the BoC and the Fed will ease rates in response to weaker labour data in both countries. The big news came from the mining sector, where Canada’s Teck Resources (TSE: TECK) announced a merger with British based Anglo American (LSE: AAL), creating a global copper powerhouse in the second-largest mining deal ever. Energy stocks found support in steady oil prices, while record-high gold prices gave miners an extra lift, leaving Canadian investors cautiously optimistic heading into next week.

All told, it was a week where good news outweighed the bad, with rate cut hopes, a revived AI rally, and surging commodities powering indexes to new records. Still, the backdrop of softening labour data, tariff uncertainty, and rising geopolitical risks means markets aren’t without hurdles. For now though, momentum remains on the bulls’ side – and investors are heading into next week with optimism riding high.

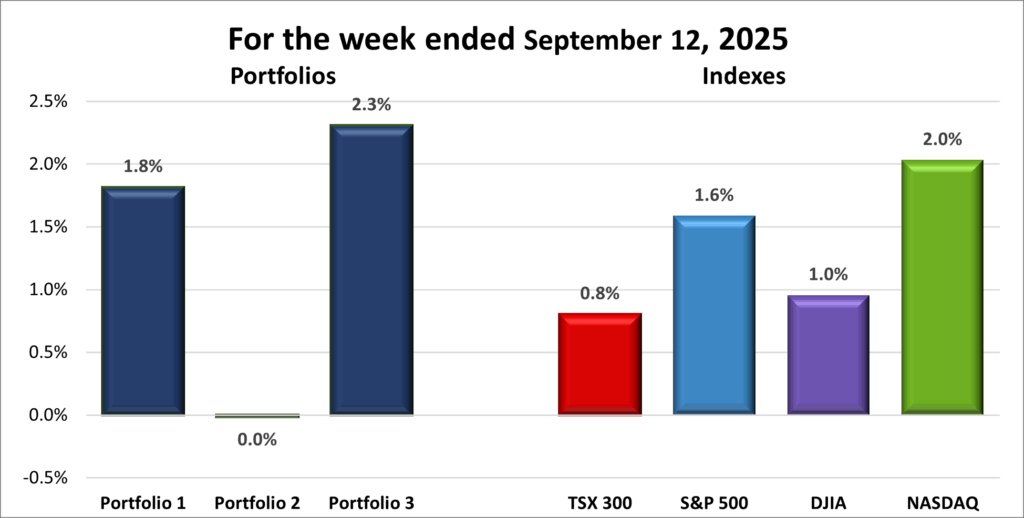

| Portfolio | Weekly Streak |

| Portfolio 1: | 2 – week winning streak |

| Portfolio 2: | 6 – week winning streak |

| Portfolio 3: | 1 – week winning streak |

![]() All three portfolios finally turned green this week, a welcome shift after some choppier stretches.

All three portfolios finally turned green this week, a welcome shift after some choppier stretches.

Portfolio 1 surprised with a solid 1.8% gain, even though less than half its holdings finished higher. Nvidia (NASD: NVDA) was one of the winners, giving the portfolio a big lift. 😊 Kraken Robotics (TSEV: PNG) jumped 20%, Grab Holdings (NASD: GRAB) climbed 15%, and both Cloudflare (NYSE: NET) and Alphabet (NASD: GOOGL) hit all-time highs. The main drag was Trade Desk (NASD: TTD), which tumbled 14% after Morgan Stanley (NYSE: MS) downgraded the stock over concerns about slowing growth in connected TV and the open web (any website or app that isn’t controlled by one big company) advertising .

Portfolio 2 lost momentum ending the week flat, despite nearly 60% of its holdings rose, including new highs from Take-Two Interactive (NASD: TTWO) and iAG Financial (TSE: IAG). Supremex (TSE: SXP) fell 10% and pulled the portfolio onto the brink of the red, but Microsoft’s (NASD: MSFT) late-week rally prevented the portfolio from sinking into the red. Microsoft shares jumped after the company dodged a hefty European Union fine by agreeing to offer lower-priced Office packages without Teams.

Portfolio 3 ended its four-week skid with a bang, surging 2.3%. Like Portfolio 2, over 59% of its holdings advanced, including Nvidia, the largest holding. While no single stock made an outsized move, the steady gains across the board were enough to put the portfolio firmly back in the win column.

It was great to see all three portfolios finish the week in the green, especially Portfolio 3 after a tough stretch. With rate cuts expected from both central banks, next week could bring more tailwinds, though markets always have a way of surprising us. For now, I’m cautiously optimistic that the momentum will carry through and I’ll be looking for another round of green across the board.

Companies on the Radar

No new companies made it onto my radar this past week, so the list still sits at five names for now:

No new companies made it onto my radar this past week, so the list still sits at five names for now:

- Mainstreet Equity Corp. (TSE: MEQ): a Calgary-based real estate company focused on mid-market apartment buildings – typically under 100 units – across Western Canada. It buys underperforming properties at below-market prices, renovates them, and increases rental income through improved operations. With strong demand for rental housing, a repeatable value-add strategy, and a solid balance sheet, Mainstreet offers a compelling mix of income and growth. Shares currently trade below net asset value, giving investors a margin of safety alongside steady cash flow and long-term upside.

- Arista Networks (NYSE: ANET): an American company that designs and sells advanced networking hardware and software, with a focus on high-speed, low-latency switches for its key markets: data centres, AI, cloud computing, and financial trading. The company has been riding the AI tailwind with solid demand from its core markets, especially in AI and cloud data centres. It also has a hefty share buyback program and increasing investments from some of the top institutional investment companies.

- Palo Alto Networks (NASD: PANW) is an American cybersecurity company, providing firewalls, cloud security, and AI-driven tools to companies around the world. It’s seen as a key play on AI-powered cybersecurity and is also benefitting from rising federal spending in this area. The stock can be volatile, but it’s been riding strong AI and cybersecurity tailwinds.

- Corning Incorporated (NYSE: GLW): a large cap American company that is a leader in specialty glass, optical fiber, environmental technology, life sciences, and other specialty glasses. They have been the supplier of the glass used in Apple’s iPhones since 2007, and they are riding the tailwind of an AI-driven fiber optic boom.

- Copart (NASD: CPRT): this American company runs one of the world’s largest online vehicle auction platforms, specializing in salvaging cars from accidents and natural disasters. It sells on behalf of insurers, dealerships, rental companies, and individuals. Copart earns revenue through transaction fees, storage, transportation, and listing services. Its digital model, global buyer network, and asset-light approach support strong margins and steady growth. With no long-term debt and rising tailwinds from vehicle values and insurance claims, it’s a steady growth story that’s earned a spot on my radar.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated September 12, 2025.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!