The Budget Is Here – Now What for Long-Term Investors?

This week, the Canadian government released its latest federal budget – essentially Ottawa’s financial game plan for the year ahead. Budgets can feel like giant spreadsheets, but at their core they show what the government wants to prioritize and where the money is going. This one focuses on boosting affordability (especially housing), supporting economic growth, and continuing to invest in clean energy and infrastructure. In the words of Daenerys Targaryen, “Let’s begin.” 😊

The budget lays out how much the government plans to spend, how much revenue it expects to bring in, and what it’s prioritizing. In this case, the goals are to “build the strongest economy in the G7,” improve long-term productivity and infrastructure, and reduce Canada’s reliance on the US as its main trading partner.

A few highlights stand out:

- A projected deficit of about $78.3 billion, meaning spending is well above revenue – adding roughly that same amount to the national debt.

- Major funding for housing, transportation, health care, defence, and clean-economy programs.

- A new trade diversification strategy aimed at strengthening economic ties beyond the US.

The size of the deficit is the big story. Last year’s shortfall was around $43 billion, so this is a noticeable jump. Higher deficits mean more borrowing, which lifts the national debt and increases the amount the government must spend on interest. That’s not necessarily negative if the money helps boost productivity – for example, improving infrastructure and energy systems can support growth over time. But more borrowing can also keep interest rates higher for longer, since governments, households, and businesses are all competing for the same pool of capital. And as debt servicing costs rise, there’s less room for future tax cuts or new programs. For us long-term investors, this is mostly background context — but it does mean that the level of interest rates is still an important force in company performance.

Budgets don’t usually move markets overnight like central bank decisions, but the themes can shape momentum. More homebuilding support could gradually help construction and materials companies. Continued clean-energy funding may provide stability for firms already leaning into the renewables space. Meanwhile, a higher deficit could translate into higher borrowing costs across the economy.

For us as investors, the core approach doesn’t change. The emphasis on housing, infrastructure, and clean energy could benefit companies tied to those areas over time, while a slower path to lowering debt means debt-heavy businesses may feel more pressure. But the long-term strategy stays the same: own strong, resilient companies that can grow earnings across different economic environments. Governments shift priorities year to year – well-run businesses keep building through every cycle

Now that we’ve covered the basics of Ottawa’s budget, let’s check out what else moved the markets this week – and how my three portfolios fared along the way.

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, ….

Canadian Economic News

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Labour Force Survey

Statistics Canada’s October Labour Force Survey came in much stronger than expected. The economy added 67,000 jobs in October, following a gain of 60,400 in September. Analysts had been expecting a slight decline, so this marks a second straight month of strength after a two-month stretch where job growth had been flat or negative. The increase in hiring also helped push the unemployment rate down from 7.1% to 6.9%, instead of holding steady as forecasters expected.

Most of the gains came from service-related industries – especially wholesale and retail trade, transportation and warehousing, and information, culture and recreation. Construction, however, saw job losses, which shows the momentum isn’t evenly spread across the economy. Wage growth came in around 3.5% year-over-year, up a touch from September’s 3.3%.

For the BoC, this data is a mixed but generally encouraging signal. A resilient job market supports consumer spending, but only modest wage growth means the report isn’t likely to reignite inflation pressures. That makes a rate cut at December’s meeting unlikely – the Bank is more likely to hold steady at 2.25% and allow the earlier cuts to continue working their way through the economy. Hopefully, these are the early signs of economic recovery.

Canadian Market Volatility

Canada’s volatility gauge, the S&P/TSX 60 Volatility Index (VIXC), ended last week around 15.5 – a fairly calm reading. But when markets reopened on Monday, it briefly jumped to 21.2 before quickly settling back into the 16–17 range and eventually closing the week at 15.96. That sharp move wasn’t about a sudden surge of fear – it was mostly a “calendar reset” effect as the index rolled into pricing a new month of options, which naturally builds in a bit more uncertainty. Once trading adjusted to the new expiry cycle, the fear gauge returned to where it started, slightly below 16.0.

For anyone new to it, the VIXC acts like a barometer of investor nerves in Canada. Lower readings (usually in the low teens) suggest calmer markets, while higher levels mean investors are bracing for more volatility. Finishing the week back near 16 suggests a cautious tone, but nothing close to panic.

US Economic News

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Labour Data

Because of the ongoing US government shutdown, a lot of the usual economic data that the Fed and investors rely on hasn’t been released. Reports like job openings and nonfarm payrolls were supposed to come out this week, but they’ve been paused – which means we’re missing some important clues about how the American economy is doing. For now, the ADP Employment Report is the main piece of labour data we have to work with.

ADP Employment Report

The latest ADP report, which looks at private sector hiring only, showed that the US added about 42,000 jobs in October. That’s a solid improvement after September’s decline and slightly better than what analysts were expecting. Wage growth also held at around 4.5% year-over-year, which suggests people are still getting raises, though the pace has been gradually slowing.

Most of the hiring happened in sectors like trade, transportation, utilities, education, and healthcare. Larger companies also added more workers, which helped lift the overall numbers. Meanwhile, areas such as professional and business services, technology and information, and leisure and hospitality lost jobs – a reminder that the labour market isn’t moving in one clear direction right now.

It’s also important to keep in mind that the ADP report is just one slice of the full picture. Normally, we’d compare it against several other government reports to get a sharper read on where the economy and job market are heading. With those missing for now, things are a bit less clear – and the longer the shutdown continues, the harder it becomes to know how strong (or weak) the labour market really is.

Consumer Sentiment Index (CSI)

The University of Michigan released its preliminary consumer sentiment reading for November, and it came in lower than expected at 50.3. That’s down from 53.6 in October and well below the 53.2 analysts were looking for. Sentiment has now fallen about 6% month over month and is sitting nearly 30% below where it was a year ago. We’re now back near the levels seen during the high-inflation stretch of 2022 – some of the weakest readings in the index’s history.

Breaking it down a bit, the Current Conditions Index (how people feel about their finances and job situation today) dropped sharply to a record low of 52.3, while the Expectations Index (which looks six months ahead) slipped to 49.0. Both declines were broad based, across all income groups, age groups, and political leanings. The ongoing US government shutdown seems to be the main driver, raising concerns about paycheques, benefits, and the broader economy.

Why does consumer sentiment matter? When consumers feel uncertain, they tend to spend less. Since consumer spending is the engine of the US economy, weaker sentiment can put pressure on corporate earnings, especially in retail and consumer-focused sectors. It also complicates things for the Fed: falling confidence paired with still-elevated inflation expectations makes deciding on interest rates even trickier. And when consumers get cautious, investors often do too.

For us as long-term investors, the message is straightforward: consumers are uneasy right now, and that may weigh on spending – but the investing approach doesn’t change. We stay focused on quality, resilience, and companies that can keep growing through different economic environments.

American Market Volatility

The CBOE Volatility Index (VIX) – often called the market’s “fear gauge” – started the week around 17. As the days went on, worries about stretched valuations in artificial intelligence (AI) stocks began to creep in, pushing the VIX higher. Then a private-sector labour report showed the highest number of layoffs since 2003, which added to the unease. The VIX briefly jumped above 20 before settling at 19.08 by the end of the week.

Think of the VIX as the market’s mood ring – it reflects how anxious or confident investors are feeling. Even with that mid-week spike, a close under 20 suggests investors aren’t panicking, but they’re not relaxed either. It’s a cautious, wait-and-see mood rather than full-on optimism or fear.

Weekly Market and Portfolio Review

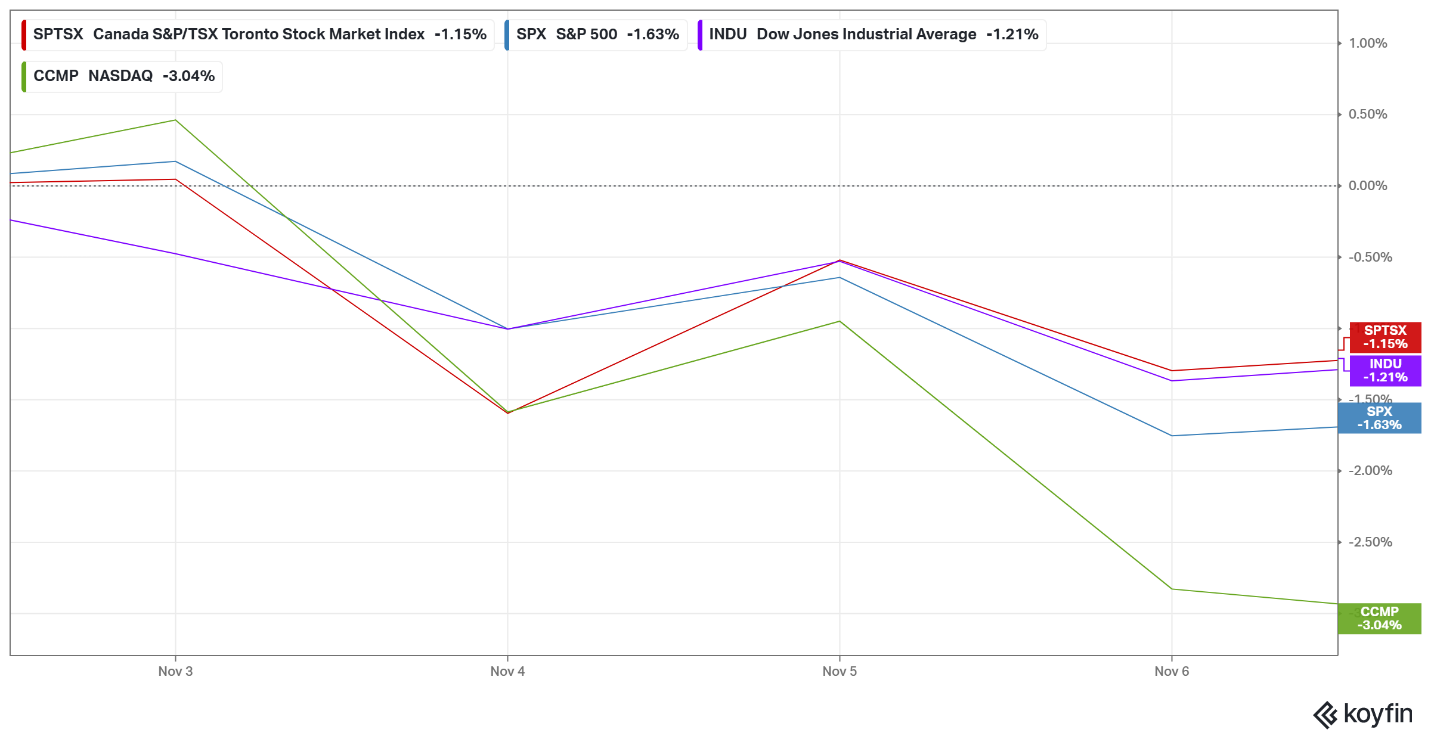

For the week, the TSX (SPTSX) dipped 1.2%, the S&P 500 (SPX) dropped 1.6%, the DJIA (INDU) declined 1.2% and the Nasdaq (CCMP) plunged 3.0%.

| Index | Weekly Streak |

| TSX: | 2 – week losing streak |

| S&P: | 1 – week losing streak |

| DJIA: | 1 – week losing streak |

| Nasdaq: | 1 – week losing streak |

![]() The markets took a breather this week as worries over pricey stocks, a potential AI bubble, weaker-than-expected US labour data, and the ongoing government shutdown cooled investor enthusiasm. All four major indexes finished lower. The Toronto Stock Exchange Composite Index (TSX) notched its second straight weekly decline, while the S&P 500 (S&P), Dow Jones Industrial Average (DJIA), and Nasdaq Composite (Nasdaq) all saw their recent winning streaks come to a halt. It was the biggest weekly drop for US markets since April, when trade tensions last grabbed the spotlight.

The markets took a breather this week as worries over pricey stocks, a potential AI bubble, weaker-than-expected US labour data, and the ongoing government shutdown cooled investor enthusiasm. All four major indexes finished lower. The Toronto Stock Exchange Composite Index (TSX) notched its second straight weekly decline, while the S&P 500 (S&P), Dow Jones Industrial Average (DJIA), and Nasdaq Composite (Nasdaq) all saw their recent winning streaks come to a halt. It was the biggest weekly drop for US markets since April, when trade tensions last grabbed the spotlight.

The week started on a hopeful note. News of Amazon.com’s (NASD: AMZN) US$38 billion partnership with OpenAI helped calm fears that the company was losing ground in the AI arms race. But that optimism faded quickly. Several large American banks warned that stock prices for leading AI players had raced far ahead of their earnings, prompting many investors to take profits. Earnings themselves weren’t bad – just not strong enough to support some of the bigger expectations that had built up.

At the same time, the ongoing US government shutdown continued to delay key economic reports, leaving investors to rely on private-sector data that painted a mixed picture. One firm pointed to stronger hiring, another flagged layoffs at a two-decade high, and a third suggested job losses in October. The longer the shutdown drags on, the thicker the fog of economic uncertainty becomes. That uncertainty is weighing on consumer sentiment, as Americans face rising inflation, higher unemployment, an ongoing government shutdown, and tensions from a global trade dispute. Sentiment has slipped back to levels last seen during the 2022 inflation spike, adding even more caution to the market mood.

Trade policy returned to centre court as the US Supreme Court (see what I did there 😊) heard arguments about whether the administration has the authority to impose broad tariffs without Congress approval. Several justices questioned those powers. A ruling against the administration could force changes in existing tariffs, with ripple effects on global supply chains, including Canadian companies with US exposure.

In Canada, the TSX eased lower as investors became more cautious, especially in interest-sensitive and higher-growth sectors. A pullback in major US technology names spilled over into Canadian technology stocks, while softer oil prices weighed on the energy sector. Since technology and energy have been two of the TSX’s main engines this year, both cooling at the same time pulled the index down. Corporate earnings were generally steady but didn’t offer enough momentum to offset the caution. The Canadian labour report added another layer as both the number of new jobs and unemployment came in better than expected. That’s normally a clear positive, but in the current environment it also raises questions about what the BoC may do at their December meeting, the last of the 2025.

Overall, the mood wasn’t gloomy, just cautious. There was optimism from big technology partnerships and steady earnings, balanced by signs that the broader economy may be showing a few cracks in jobs and trade. After several strong months, investors mostly stepped back to reassess and wait for clearer signals before making their next moves. It felt more like a pause to catch our breath than any major shift in direction. At least I hope that’s the case. 😊

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week losing streak |

| Portfolio 2: | 1 – week losing streak |

| Portfolio 3: | 1 – week losing streak |

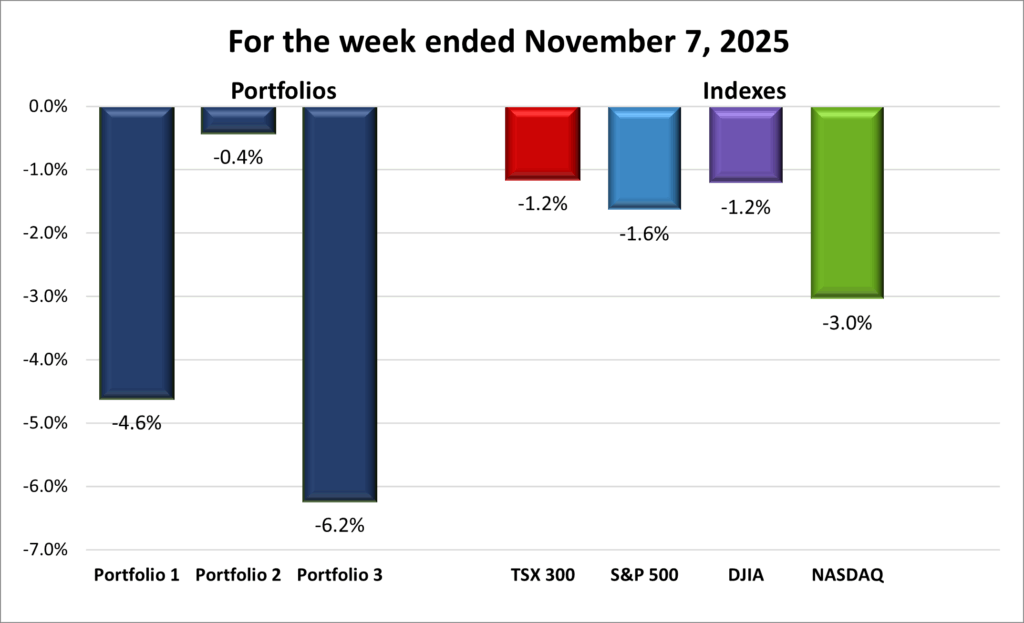

![]() After three weeks of gains, the markets hit the pause button, and all three portfolios felt the sting. Two of them ended deep in the red, and the week ended up like a “bad, worse, worst” scenario. It was the kind of week where even strong performers couldn’t fully offset the heavier losses.

After three weeks of gains, the markets hit the pause button, and all three portfolios felt the sting. Two of them ended deep in the red, and the week ended up like a “bad, worse, worst” scenario. It was the kind of week where even strong performers couldn’t fully offset the heavier losses.

Portfolio 1 had a bad week, falling 4.6%. Only 30% of its holdings gained ground, including bright spots like Datadog (NASD: DDOG) up 16% and International Petroleum (TSE: IPCO) up 12%. Cloudflare (NYSE: NET) and Amazon.com also hit new highs before slipping back at the end of the week. Unfortunately, the losses were deeper and more widespread, with Celsius Holdings (NASD: CELH) plunging 29%, Navitas Semiconductor (NASD: NVTS) down 23%, Kraken Robotics (TSE: PNG) down 18%, and several others including Magnite (NASD: MGNI), Arista Networks (NYSE: ANET), Hammond Power Solutions (TSE: HPS.A), Shopify (TSE: SHOP), The Trade Desk (NASD: TTD), Lattice Semiconductor (NASD: LSCC), and Cameco (TSE: CCO) dropping between 10% and 16%.

Portfolio 2 was the “best” of the three, because it was the least bad, declining only 0.4%. Interestingly, it outperformed all four major indexes. It also had a portfolio best 42% of the holdings post weekly gains, including iA Financial (TSE: IAG) hitting a record high. The main drags were Zoetis (NYSE: ZTS), down 16%, and Hammond Power Solutions dropping 14%.

Portfolio 3 was the worst performer, losing 6.2% in value and falling more than any of the indexes. Only 15% of its holdings finished the week up. ☹ Highlights were scarce, but the lowlights were dramatic: goeasy (TSE: GSY) tumbled 30%, including a 17% drop the day it missed revenue and earnings estimates. Magnite lost 16%, and Shopify fell 14%.

Overall, it was a tough week across the board. A reminder that markets don’t move in a straight line and short-term volatility is part of the game. Despite the setbacks, this week is just a small bump in the longer journey of wealth through investing. 😊

Companies on the Radar

There was a bit of movement on my radar list this week, but only in one direction – off. After a busy stretch of new names being added, things stayed quiet on the incoming side. The change this week was the removal of Canada Packers (TSE: CPKR), the small-cap Canadian pork producer focused on premium, value-added products. It’s graduating from the radar list and finding a home in Portfolio 3. We also say goodbye to Aritzia (TSE: ATZ), the Canadian women’s fashion retailer, which is now part of Portfolio 2.

There was a bit of movement on my radar list this week, but only in one direction – off. After a busy stretch of new names being added, things stayed quiet on the incoming side. The change this week was the removal of Canada Packers (TSE: CPKR), the small-cap Canadian pork producer focused on premium, value-added products. It’s graduating from the radar list and finding a home in Portfolio 3. We also say goodbye to Aritzia (TSE: ATZ), the Canadian women’s fashion retailer, which is now part of Portfolio 2.

With those moves, the radar list now sits at these six names from last week:

- GE Aerospace (NYSE: GE): This is the large American aviation and defence business that remained after General Electric split into three separate companies in 2024. It has been on a strong run thanks to high demand for commercial jet engines as global air travel continues to recover. The company focuses on aircraft propulsion systems and services for both commercial and military customers, and it’s also moving into drones. As a global leader in jet engines and aircraft systems, GE Aerospace offers exposure to long-term trends in travel, defence spending, and emerging aviation technology.

- Corning Incorporated (NYSE: GLW): A large US company known for specialty glass and optical technologies. Corning is the longstanding supplier of the glass used in iPhones and is also benefiting from the surge in demand for high quality fiber optics as data centres expand to support AI and cloud computing. The company is riding several tailwinds with long-term growth potential.

- Mainstreet Equity Corp. (TSE: MEQ): A Calgary-based real estate company focused on mid-market apartment buildings across Western Canada. Their business model is straightforward: buy underperforming buildings, renovate them, improve operations, and increase rental income. With strong demand for rentals, a disciplined approach, and shares that trade below the estimated value of the properties, Mainstreet offers a combination of income, stability, and long-term upside.

- Napco Security Technologies, Inc. (NASD: NSSC): A small US company that provides security hardware and systems like smart locks, intrusion alarms, fire alarms, and access control solutions. It sells through a network of distributors and installers, and has been increasing its recurring service revenue – something investors usually like to see. As demand for security and smart home products grows, Napco has multiple avenues for expansion.

- XPEL, Inc. (NASD: XPEL): A growing, founder-led maker of protective films, coatings, and related products – best known for automotive paint protection film. XPEL has been expanding into window films and architectural applications, and sells through multiple channels, giving it both reach and control. It’s a company with a focused niche and strong brand recognition in that niche.

- Dutch Bros Inc. (NYSE: BROS): A rapidly expanding drive-thru coffee chain in the US, known for its energetic customer service and customizable drinks. The company is aiming to open at least 160 new locations by the end of 2025 and has long-term goals of surpassing 2,000 stores. Strong brand loyalty, especially in the Western US, makes this an interesting high-growth story – though still in an aggressive build-out phase.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated November 7, 2025.

Portfolio Update

Portfolio 2

Bought: Aritzia (TSE: ATZ) This Canadian women’s fashion retailer is known for its in-house brands and curated, upscale shopping experience. The company started in Vancouver and has steadily expanded across North America, with a growing presence in major American cities. Instead of carrying a wide mix of third-party labels, Aritzia designs and controls most of the apparel it sells. That gives the company more control over branding, pricing, and margins – and when the product resonates, it really resonates.

The business model is straightforward: design women’s clothing → manufacture it (with partners) → sell directly to customers through boutiques and online. Because the clothing is sold under Aritzia’s own labels (like Wilfred, TNA, and Babaton), the company keeps more of the value it creates compared to retailers that resell other brands. The focus is on “everyday luxury” – high-quality, stylish basics and seasonal pieces that sit between fast fashion and designer pricing.

What I like about Aritzia is the combination of brand strength and long runway for US growth. The company already has a loyal Canadian customer base, and its US expansion is still in early innings. Stores in New York, Chicago, and Los Angeles have been performing well, and management plans to continue opening new locations while improving e-commerce. When a retailer has a brand that clicks with its audience, scaling it across markets can be powerful – especially when the company controls the product from design to sale.

Another appealing factor is Aritzia’s focus on improving profitability after several years of heavy growth investment. This includes optimizing store operations, strengthening inventory management, and refining its supply chain. If executed well, these efforts could drive margin recovery as revenue grows – a combination that can significantly lift earnings over time.

Of course, there are risks. Retail is competitive, fashion trends shift quickly, and misjudging demand or inventory can hurt profitability. The US rollout isn’t guaranteed – some brands expand smoothly across borders, others stumble. Efficiency improvements also need to translate into real margin gains.

For me, it comes down to brand strength and growth potential. Aritzia has proven it can attract and maintain loyal women customers, and early traction in the US suggests there’s plenty of room for continued expansion. I’m confident that management will keep executing well, growing revenue and expanding margins – and when a business performs like that, the share price usually follows. 😊

I’m adding it to Portfolio 2 as a long-term growth play, to boost the growth potential of the entire portfolio while adding a bit of diversity for stability. I only wish I had bought it earlier, back when it first came on my radar in late June – since then, it’s gone up 42%! Hopefully there’s more share price growth like that to come. 😊

Portfolio 3

Bought: Canada Packers (TSE: CPKR). The small-cap, newly independent Canadian company spun out from Maple Leaf Foods’ (TSE: MFI) pork operations. As an independent business, it’s positioned as a vertically integrated pork producer focused on premium, value-added products, selling both domestically and internationally.

As part of the spin-out, Canada Packers has a long-term supply agreement with Maple Leaf to supply pork to maple Leaf’s prepared-meats division. This gives the company a stable “anchor customer,” reducing reliance on volatile spot markets and providing a base of predictable demand. That stability is one of the reasons I found this investment particularly appealing.

In simple terms, Canada Packers raises or sources hogs, processes them into pork products – including cuts and value-added items – and sells them to customers. As mentioned, Maple Leaf is one major customer, while the rest of its sales come from domestic and export markets. Being vertically integrated means the company controls multiple steps of the process, which can help capture more of the profit margin. By focusing on premium products rather than commodity pork, Canada Packers has the potential for higher margins and less price competition.

What I like about this investment is that it combines stability and growth potential. The supply deal with Maple Leaf reduces uncertainty, vertical integration allows the company to capture more of the value chain, and premium-focused products help protect margins from commodity swings. On top of that, the company has signaled it plans to pay a dividend once cash flows stabilize, adding an income component to the investment.

As with all investments, there are risks. Hog and pork production is sensitive to feed costs, labour, energy, disease, regulation, and export rules – all of which can squeeze margins. Meat businesses are cyclical, so demand and prices can fluctuate. As well, being a spin-out, Canada Packers has a limited independent track record, though most senior executives came from Maple Leaf and bring valuable experience. Global competition is another factor, and dividends aren’t guaranteed until declared and sustained.

For me, I’m looking to add diversity and stability to the technology-heavy Portfolio 3. By investing just a few weeks after the spin-out and before the dividend announcement, I’m taking a bit of a risk but positioning myself at the start of the company’s journey. The business model is easy to grasp – raise hogs → process pork → sell to customers – making it a clear, easy-to-understand story. If the company executes well, there’s potential for both income from a future dividend and growth from global expansion and margin improvements. But execution is key – if they deliver, it could be a double win. 😊

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!