While preparing the Weekly Updates, I was increasingly writing about the Bank of Canada and the US Federal Reserve, the central banks for Canada and the USA, respectively. I knew they were central banks and they set the interest rates for their respective nations but that was about it. I soon discovered their actions had a significant impact on my investments, especially the Federal Reserve’s policies, so I decided I would like to know more about these two organizations.

Before looking at these two entities, its good to be clear on what is a central bank.

What is a central bank?

Throughout the world, each country has its own central bank. Most of the central banks are separate from their national governments, however, they are overseen by their respective national governments. For this article, let us focus on Canada’s Bank of Canada (BoC), and the USA’s Federal Reserve System (Fed).

Unlike the banks that individuals and businesses deal with in Canada and the US, the BoC and the Fed are not commercial banks that offers services to the public. Their role is to set and maintain the monetary policies of their respective countries, as well as ensure their respective financial system remains safe and secure. These two central banks are independent of each other and do not work together or coordinate their activities. However, I suspect they are aware of what each other is doing.

In 2022, the BoC found itself in the news more than it would like thanks to inflation hitting heights not seen for 40 years. To try and control inflation, the BoC raised the overnight interest rates to cool the Canadian economy and slow inflation. The overnight rate is the interest rate that the BoC expects to be used in Canadian financial markets for one-day (or “overnight”) loans between Canadian financial institutions (banks, credit unions, etc.). This rate becomes the prime rate which establishes how much it will cost to borrow money from the banks, whether it is a mortgage, a line of credit, personal or business loan or any other type of loan or debt. When the BoC raises its rate, it will cost more for commercial banks to borrow. These higher costs are in turn passed on to consumers and businesses. On the other hand, if the BoC lowers the benchmark rate, the lower rates will trickle down to borrowers.

The same applies to the Fed in the US. The Fed will set the benchmark rate for American financial institutions who in turn base their lending rates on this benchmark.

One other concept to be aware of is monetary policy. Monetary policy is a set of measures used by central banks to encourage or discourage the growth of demand for goods and services. These measures include adjusting the interest rate of overnight borrowing by commercials banks and increasing or decreasing the amount of cash available in the economy. Through these tools, monetary policy can be used to attempt to control inflation, unemployment, price and wages stability, and confidence in a nation’s currency. If you’d like a more detailed explanation, do an online search for ‘Canadian monetary policy’ or ‘US monetary policy’

With that out of the way, let us look at the BoC and the Fed.

Bank of Canada

The BOC is located in Ottawa, Ontario. It came into existence in 1935 with the mission to “regulate credit and currency in the best interests of the economic life of the nation.”

The BOC is located in Ottawa, Ontario. It came into existence in 1935 with the mission to “regulate credit and currency in the best interests of the economic life of the nation.”

The BoC is independent from the federal government to ensure the power to spend money remains separate from the power to create money. This independence allows the BoC to focus on medium- and long-term perspectives for the good of Canada rather than what is good for the governing party. One can only imagine the mess Canadian monetary policy would be in if politicians had direct input into the decisions. The BoC’s main duty is to promote financial stability by focusing on the following areas:

- Monetary Policy: Establishes policies (interest rates and cash supply) that are designed to preserve the value and stability of the Canadian dollar by keeping inflation in the target range of 1% – 3%. One way it does this is by raising or lowering Canada’s overnight, or benchmark, interest rate.

- Financial systems: Encourages a secure financial system for all members of the Canadian banking community. One of the ways it accomplishes this by being the lender of last resort for the Canadian banking industry.

- Currency: The sole authority for issuing and managing Canada’s national currency. The BoC is responsible for the design, distribution, security, and supply of new Canadian currency.

- Funds Management: Manages Canada’s public debt programs and foreign exchange reserves. They also provide Canadian denominated operating accounts for holding securities and gold for other foreign countries’ central banks.

How is the Bank of Canada structured?

At the end of 2021, the BoC employed over 2,000 people. It is overseen by a Board of Directors, led by the Governing Council, and managed by the Executive Council, as outlined below:

- Board of Directors: Provides general oversight of the management and administration of the Bank with respect to strategic planning, financial and accounting matters, risk management, human resources, and other internal policies.

The Board is composed of the BoC Governor and Senior Deputy Governor, plus 12 independent directors appointed to three-year, renewable terms by the federal Cabinet. The Deputy Minister of Finance is a non-voting Board member. - Governing Council: Responsible for the day-to-day conduct of Canada’s monetary policy and maintaining a dependable and efficient financial system. It includes the Governor, Senior Deputy Governor and the three Deputy Governors (4 Deputy Governors as of March 2023).

- Executive Council: Responsible for the strategic direction of the BoC. It includes all the members of the Governing Council, plus the Chief Operating Officer and the Executive Director – Retail Payments Supervision.

The key positions at the BoC are:

- Governor: The Governor is appointed by Canada’s Minister of Finance for a 7-year term, with approval of the federal Cabinet. The Governor is also Chair of the Board of Directors and leads the Governing Council. The Governor has full control over the business of the BoC.

- Senior Deputy Governor: This position is appointed by the independent members of the Board, with approval of the federal Cabinet, for a 7-year term. It is a member of the Board of Directors and the Governing Council and oversees the BoC’s strategic planning and operations.

- Deputy Governors: There are currently three Deputies who are responsible for:

- Supervising the BoC’s financial system activities.

- The BoC’s analysis of international economic developments in support of monetary policy decisions. They consult with the central banks of the Group of 7 countries and the Group of 20 countries.

- Overseeing the Financial Markets Department.

- Monitoring the Canadian economy and monetary policy.

The BoC meets eight times a year to make any announcements about changes to interest rates. At these meetings, the members decide whether to raise, lower or maintain Canada’s benchmark interest rate which is then used by banks and other financial institutions to establish their respective prime lending rate. Decisions are made by a consensus vote by the Governing Council.

Each quarter the bank provides an updated monetary policy report and its outlook for the Canadian economy. In the past, minutes from their meetings and discussions were not made public, however that changed following their January 25, 2023, meeting.

Finally, the BoC typically earns income from its assets (primarily Government of Canada bonds but includes provincial and corporate bonds, as well as other types of assets). Once all its expenses are paid, the net income is then transferred to the federal government. In 2021, it remitted C$2.7 billion.

Now that I have covered Canada’s central bank, lets look at America’s central bank, commonly referred to as the Fed.

US Federal Reserve System

![]() The Fed was created in 1913 as an independent agency of the federal government, reporting to Congress twice a year. Located in Washington, D.C., the Fed is a not-for-profit agency and, after paying all expenses and setting aside a limited amount in a surplus fund, must transfer all earnings to the US Treasury.

The Fed was created in 1913 as an independent agency of the federal government, reporting to Congress twice a year. Located in Washington, D.C., the Fed is a not-for-profit agency and, after paying all expenses and setting aside a limited amount in a surplus fund, must transfer all earnings to the US Treasury.

The purpose of the Fed is to act in the best interest of the American public by supporting the health of the US economy while maintaining a stable financial system. It is also the most influential central bank in the world because the vast majority of currency transactions involve the US dollar. Changes implemented by the Fed can impact the currency and economies of many other countries. For example, Canada cannot let US benchmark interest rate get too much higher than the Canadian benchmark interest rate to avoid weakening the Canadian dollar which in turn makes all products from the US more expensive for Canadians.

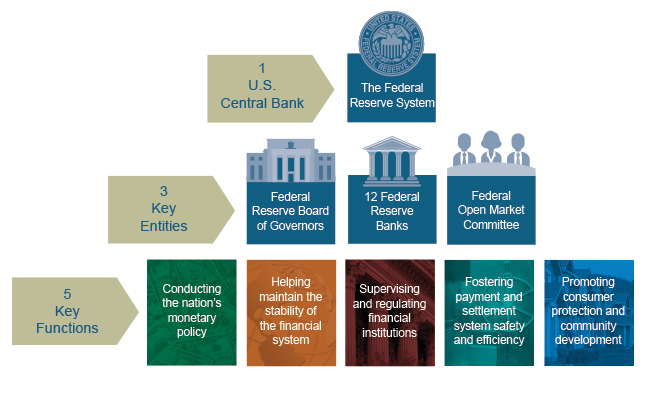

How is the Fed structured?

The Federal Reserve Act purposely designed a decentralized system of a central bank rather than a single central bank. As the second tier in the graphic above illustrates, the central banking “system” has three main entities:

- The Federal Reserve Board of Governors (BoG): Located in Washington, D.C, the BoG is the central governing body of the Fed. It is comprised of seven members (Governors), each nominated by the President and approved by the Senate. Each Governor serves a single 14-year term. The Chair and Vice Chair are selected from among the seven Governors by the President and approved by the Senate. The Chair and Vice Chair positions are 4-year terms and may be re-appointed to additional four-year terms until their 14-year term expires.

The BoG manages the operations of the Fed by providing guidance, and oversight to the 12 regional Reserve Banks. They make public the minutes from the Federal Open Market Committee meetings, as well as the Fed’s independently audited financial statements. - The Federal Reserve Banks (Reserve Banks): Located throughout the continental 48 states, the Reserve Banks are a decentralized operating structure of 12 geographic Reserve Banks. Each of the Reserve Banks collects economic information from their region and relay it to the Federal Open Market Committee, where monetary policy is decided. Essentially, the Reserve Banks are the banks used by commercial financial institutions (banks, credit unions, etc.) in their region. Each Reserve Bank has its own Chair, Deputy Chair (both appointed by the Fed’s BoG) and a Board of Directors, consisting of 5 – 7 members. These Boards are primarily appointed by the Reserve Bank itself, with the remaining positions appointed by the Fed’s BoG. Each Reserve Bank has a president.

- Federal Open Market Committee (FOMC): The FOMC is the committee within the Fed that establishes and manages the American monetary policy. They adjust the benchmark interest rate to keep the economy on the path to fulfill the Fed’s twin goals of maximum employment and price stability. When you hear the US benchmark interest rate has moved up, down or remained unchanged, this committee made the decision. As well as establishing the interest rate, they can purchase and sell securities on the open market to manage the monetary policy.

The FOMC is comprised of 12 voting members which includes all 7 members of the Fed’s BoG; the president of the Federal Reserve Bank of New York; and 4 of the remaining 11 Reserve Bank presidents, who serve one-year terms on a rotating basis. The remaining 7 Reserve Bank presidents not on the FOMC attend and participate in the meetings but do not vote on policy decisions. The Chair of the FOMC is the Chair of the Fed’s BoG, while the Vice Chair is the president of the Federal Reserve Bank of New York. All 12 members of the FOMC meet eight times per year in Washington DC, with additional meetings if necessary. After each meeting, they provide forward guidance for the interest rate that is consistent with their economic outlook, and they must explain any deviations from their projected path.

As the bottom tier in the graphic above illustrates, the Fed performs the five following functions to promote the American economy:

- Implements the monetary policy to maximize and stabilize the US economy.

- Ensures the stability of the American financial system by minimizing risk.

- Ensures the safety and soundness of individual financial systems.

- Strengthens the safety of payment and settlement systems that involve US dollar transactions.

- Promotes consumer protection by analysing emerging consumer issues and trends, administers consumer laws and regulations, among other responsibilities.

Key Differences

The BoC and the Fed have plenty in common. Both are responsible for implementing their respective monetary policy through interest rate decisions, issuing currency, regulating banks, and as the lender of last resort to commercial banks to ensure the stability of their respective financial systems. However, there are some significant differences, including:

- The BoC focuses primarily on achieving price stability, while the Fed has a dual mandate of promoting both price stability and maximum employment.

- The BoC operates as a crown corporation owned by the Canadian government, while the Fed is an independent entity within the US government.

- The BoC’s Governor is appointed by Canada’s Minister of Finance with Cabinet approval, while each member of the Fed’s Board of Governors is appointed by the US President with Senate approval. The Chair and Vice Chair are chosen from the seven governors and appointed by the President and confirmed by the Senate. Being approved to the Fed appears to be much more difficult because a majority of Senators from across both political parties is required. In Canada, Cabinet members, which includes the Minister of Finance, are all from the same party.

- According to the Bank of Canada Act, the BoC Governor makes Canada’s monetary policy. As shown in the recently published minutes from their January 25, 2023 meeting, the Governor heavily consults with the deputy governors and others to come to a consensus. In the US, decision making is shared across members of the FOMC.

- The BoC is responsible for managing the Canadian dollar exchange rate against other major currencies. The Fed does not directly manage the exchange rates, relying on supply and demand to set the rate.

- The BoC is responsible for the design of all Canadian currency, in conjunctions with the Royal Canadian Mint and major Canadian law enforcement agencies to prevent counterfeiting. The US Department of the Treasury’s Bureau of Engraving and Printing is responsible for the design of US currency. They work with the Fed, the US Secret Service and major American law enforcement agencies to protect the currency from counterfeiting.

Central Banks’ Influence on Investing

The most obvious influence on investors is through raising and lowering the interest rate. With the rise of inflation in Canada to a 40 year high in 2022, the BoC has fought to get inflation down to their 2% target, each increase of the interest rate was felt by every Canadian. When the BoC raises its lending rate to Canadian commercial banks, the banks immediately pass it on to consumers and businesses in the form of higher interest rates.

For investors, the higher interest rate means companies must spend more of their revenues servicing their debt rather than growing the business. Slower growth generally means slower share price appreciation, or in the case of high growth companies (like technology companies), share prices can plummet. Lower share prices can make them vulnerable to being bought by larger, financially healthier companies. If their debt payments become too large it can threaten their survival, pushing the company into bankruptcy. It is not fun watching your investments decline drastically. I realize its more than higher interest rates that make share prices drop significantly but they do not help.

It may be obvious that the biggest influence on Canadians is the BoC, but the Fed also has an impact on Canadians. One area that affects all Canadians is the gap between the Canadian and American benchmark rates. Generally, the difference is small. However, there are consequences when the gap gets too narrow or to far apart. Since the US economy is significantly larger than the Canadian economy (according to the World Bank, US$ 22.99 trillion compared to US$ 2 trillion), it is BoC that must adjust its interest rate, giving rise to the adage “when the U.S. sneezes Canada catches a cold.” If the Canadian interest rate gets too high (or too close to the US rate) it will push up the currency exchange rate, making Canadian exports more expensive. If the Canadian interest rate gets too low compared to the US rate, the Canadian currency exchange rate will drop, making US imports more expensive, which can lead to inflation.

Many Canadian investors are invested in American companies that trade on one of the American stock exchanges. Not only do we have to keep in mind currency exchange rates that can be impacted by interest rates, as outlined above, but the share prices of the American companies can rise and fall on changes to the US lending rate, just as Canadian companies on the Canadian exchanges respond to changes in the Canadian borrowing rate.

As well as interest rates, there are other ways the BoC and the Fed impact investing, including:

- Economic Growth: Their actions to stimulate their respective economies through monetary policy (interest rates) can influence the overall level of the nation’s economic growth. A strong economy usually leads to growing markets (rising share prices), while a slowing economy is usually accompanied by falling markets (sinking share prices).

- Inflation: Their ability to manage inflation expectations can affect the purchasing power of investments and their long-term value. As we saw in 2022, when inflation gets too high, the markets fall as interest rates rise to bring down inflation.

- Market Sentiment: Their policy decisions can influence investor sentiment, which can affect the performance of different sectors and types of investments. Their announcements are dissected by analysts to get a sense of what moves they may make at upcoming meetings.

As you can see, the BoC and the Fed can have a significant impact on the stock markets, but there are other factors outside their control that can influence the performance of investments. Global economic conditions like those brought on by the Covid-19 pandemic, or geopolitical events such as Russia’s invasion of Ukraine will also impact investments (increase the price of oil and natural gas, for example). And do not forget company-specific actions are the biggest mover of share prices.

Summary

Although they are structured differently, both central banks are similar in that they are responsible for their respective nation’s monetary policy (setting the benchmark borrowing rate). Ideally, they would be happy if inflation stayed at 2% and they never had to move the interest rate one way or the other. However, stuff happens, causing economies to overheat or shrink. When it does, central banks will react accordingly, either adjusting the interest rate as necessary, or in the case of inflation, threatening to increase the rate to cool investor sentiment.

To wrap up, lets end with a good example of the impact the BoC and the Fed can exert is the last few years. The start of the Covid-19 pandemic threatened to shut down economies. In response, the BoC and the Fed lowered their respective benchmark interest rates to 0.25%. With the ‘cheap’ supply of money the economies quickly rebounded and ran too hot through 2021, as pent-up demand sent prices soaring as suppliers were unable to match demand. Inflation started creeping higher until finally both central banks hit the brakes on the economy. Both quickly increased the lending rate, making money borrowing money more expensive. Companies had to put more money towards servicing their debt at the expense of growing their business. Corporate earnings slowed or even declined, leading to a drop in share prices.

After researching and writing this article I had a much better understanding of these two central banks. I hope this piece provided you with a high-level view of the BoC and the Fed – their structure, their similarities and differences, and how they impact the companies we invest in. There is plenty more about the BoC and the Fed, but this site is about investing, not central banks. 😊. If you wish to know more, check out the Bank of Canada site and the Federal Reserve System, otherwise, thank you for reading.