Items that may only interest or educate me ….

Central banks, Bank of Canada minutes, Canadian interest rate predictions, ignore the noise, Canadian jobs, Bing challenging Google? …

If it seems like the Bank of Canada (BoC) and the US Federal Reserve (Fed) are common topics in this section of the Weekly Updates, you would be correct. This was not by design. Rather, the two were noteworthy because the markets responded to their actions and words, especially the Federal Reserve’s policies. To get a better understanding of them, I did a little research on the two organizations. If you would like a high-level overview of these two government organizations, check out the article on Central Banks.

The BoC made public the minutes from their January 25 rate decision. The BoC was one of the few central banks that did not provide notes from their meetings. However, following a recommendation from the International Monetary Fund (IMF), the BoC will publish the discussions amongst the BoC members that went into their interest rate decision.

The minutes showed that the central bank was inclined to pause interest rate hikes, but the strong Canadian labour market and stronger than expected economic growth caused them to increase the rates by 0.25%. Other factors the BoC took into consideration include declining energy prices, global supply chains improving, and that China ended their Covid-19 lockdowns. At the end of the day, the BoC members concluded global inflation was drifting downward and “the perceived risk of a deep recession had decreased” but a 0.25% increase was required to ensure inflation kept heading downward.

During a speech to analysts, Bank of Canada (BoC) Governor Mr. Tiff Macklem said no additional interest rate hikes will be required if inflation continues to fall. If the data continues to confirm the BoC’s inflation forecast, Canadians can expect the benchmark interest rate to have peaked at 4.5%. However, he did not say when Canadians can expect to see interest rates to decline, saying it was too early to think about lowering the interest rate.

The day prior to Mr. Macklem’s speech, a BoC survey of the 28 major Canadian market participants revealed they believe:

- The Canadian benchmark interest rate will drop to 4%, if not lower, by the end of 2023.

- The rate will continue to fall into 2024.

- None of the participants believe the rate will go higher.

- Inflation will drop to 2.9% by the end of the 2023. This would put inflation within the BoC’s target range of 1% – 3%.

Let us hope they are clairvoyant.

The BoC made its latest adjustment to Canada’s benchmark interest rate on January 5, raising the rate to 4.5% and saying they would pause interest rate increases unless the data dictated otherwise. Their next meeting is March 8. The US Federal Reserve (Fed) announced a 0.25% increasing bring the US interest rate to 4.75%, however, they indicated there would be future increases rather than a pause. Their next meeting is March 21 -22.

Between now and the next announcements from the two central banks a lot may happen. One thing you can count on is there will be no shortage of ‘experts’ telling us what the two central banks will do. Many will say the BoC will pause, many will say they will raise the rate. The same goes for the ‘experts’ following the Fed. They will probably change their positions based on data as it becomes available. Take their predictions with a grain of salt, its mostly noise. No one knows what is going to happen (see the next section item the Canadian jobs report). If you are investing for the long term (5+ years), don’t worry about these short term events.

If you want to get an idea of which way the BoC or the Fed is leaning, follow the data. The Canadian Consumer Price Index (CPI) and Producer Price Index (PPI) are published by Statistics Canada. In the US, the CPI and PPI reports are published by the Bureau of Labor Statistics. There are other reports published monthly but the CPI and PPI are good places to start if you want to know if inflation is going up or down.

Statistics Canada’s latest jobs report showed the Canadian economy added 150,000 jobs in January, well above analysts’ prediction of 15,000 new jobs, while the unemployment rate remained at 5.0%, barely above the record low. The data suggests the labour market remains strong, leading to concerns the BoC may reconsider pausing interest rate hikes.

This follows the stronger than expected jobs report out of the US last. Investors in Canada and the USA are now waiting for next week’s January CPI data for clues on the next moves from the BoC and the Fed. If the February data is similar to the January data, both central banks may be inclined to raise the interest rate another 0.25%.

Could Microsoft (NASD:MSFT) be disrupting Google’s dominance of online search? Alphabet’s (NASD:GOOGL) Google has been the dominant search engine for years, with over 90% of the market. However, Microsoft has recently upped its search engine game with the addition of OpenAI’s ChatGPT artificial intelligence (AI) chatbot (a computer program designed to simulate conversation with human users.)

It’s estimated that for every percentage point in market share that Microsoft can gain from Google in the battle for search supremacy, they will bring in US$2 billion in search advertising revenues. As well as incorporating ChatGPT into their Bing search engine and Edge browser, Microsoft plans to integrate it into many of their productivity applications. They’ve already launched a premium version of Teams featuring ChatGPT.

Google has announced their own chatbot – Bard – which will provide similar services for Google’s Search and Maps applications. Unfortunately for Google, Bard did a face plant in a promotional video at a company event when it responded to a query with inaccurate information. Thanks to this misfire, Alphabet lost US$ 100 billion in market value over concerns the company was falling behind Microsoft.

As well as being used in their respective search engines and productivity tools, similar AI tools could be used in numerous industries for tasks such as for online content creation, answering customer queries and other applications. The possibilities are endless and there is a lot at stake as Microsoft, Google and other AI developers rush to stake their claims in this emerging market.

For now, Microsoft and ChatGPT are winning the race, but this is marathon, not a sprint. Google has the resources and deep pockets to get back in the race. Perhaps there is another company no one has heard of that will dominate the AI market.

With the recent drop in Alphabet’s share price thanks to Bard’s pratfall, if you believe in the long-term success of the company now could be a good time to invest in Alphabet. 😊

With the interesting items out of the way, let’s see what happened this past week….

Weekly Market Review

Monday: It seems the part where the Federal Reserve’s (Fed) chairperson said there would be ongoing hikes to the US interest rate has made investors skittish as all four major North American indexes ended lower. Last week’s strong US jobs report caused investors to worry the US interest rate could go higher and last longer.

In Canada, the Toronto Stock Exchange Composite Index (TSX) fell on lower commodity prices and concerns of higher US interest rates. In trading, the defensive sectors Consumer Staples, Utilities, and Telecommunications Services were the only Canadian sectors to end higher. Falling the farthest were Consumer Cyclical and Basic Materials (miners and fertilizer manufacturers).

In the US, it was a tough day for the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) as they gave back some of last week’s gains. The only US Sector to advance was the Utilities sector, while the Technology and Basic Materials sank the farthest.

Tuesday: The markets rebounded from Monday’s setback, with all four indexes solidly higher. The main catalyst was comments from both the BoC and Fed that eased concerns about higher interest rates. Oil prices rebounded on increasing demand from China.

In Canada, a statement from the BoC Governor stating no further interest rate hikes would be required if the data continues to show inflation is falling, good news out of the US and higher oil prices propelled the TSX higher. That is almost the perfect storm for the TSX. 😊 On the Toronto Stock Exchange (TSE), the Energy and Basic Materials gained the most of the Canadian sectors, with the defensive sectors Consumer Staples and Utilities had the biggest drop.

In the US, the markets were up and down like a yo-yo for most of the day before a strong surge pushed all three indexes solidly into the green for the day. The Fed chair said there should be “significant declines in inflation” during the year, easing investor worries. In trading, the American Energy and Technology sectors advanced the most, while Telecommunications Services, Consumer Staples and Utilities were the only sectors to end lower.

Wednesday: Tuesday’s late afternoon rally failed to stick as all four indexes gave back yesterday’s gains as investors considered recent data and comments from the BoC and the Fed. Oil prices rose for third consecutive day on increased demand from US refineries.

In Canada, the BoC released the minutes from their January session, showing what went into their decision to raise the rate by 0.25% and pause future increases. The defensive sectors Consumer Staples and Telecommunications Services ended higher and were the best of the Canadian sectors, while the Basic Materials and Technology sectors weighed down the TSX with their declines.

In the US, the Telecommunications Services sector was the only American sector to advance, while Technology and Utilities fell the farthest.

Thursday: Despite a strong start to the day, all four indexes posted their second day of losses as investors worried about recent comments from the Fed that interest rate hikes would continue and remain elevated longer. As well, US Treasury yields rose, becoming a viable and safer alternative to stocks. Share prices fell as investors moved away from volatile stocks into safer US Treasury bonds.

In Canada, lower commodity prices and the falling tide of the American markets dragged the TSX lower. In the Canadian sectors, only the Consumer Staples and Financials sector ended the day in the green, while the Healthcare and Telecommunications Services sectors were the deepest in the red.

South of the border, it was a broad-based retreat in the American S&P sectors with all sectors ending lower. Consumer Staples and Consumer Cyclicals dropped the least while Utilities and Telecommunications Services fell the most.

Friday: A late afternoon rally pushed three of the four indexes into the green, with the Nasdaq the lone index to end the day in the red. The price of oil got a boost when Russia announced plans to reduce their production of oil next month by 5%, sending the share prices of energy companies higher.

In Canada, a strong Canadian jobs report gave investors concerns the BoC would reconsider its decision to pause interest rate hikes. However, investors overcame their fears to nudge the TSX into the green. On the TSE, it was the Canadian Energy and Utilities sectors that posted the biggest gains, while Consumer Cyclicals and Technology sectors fell the most.

In the US, the Nasdaq suffered its first weekly decline of the year as the yield on 10-year US Treasury notes rose, approaching 4%. Higher yields have a more adverse effect on the riskier, high growth technology companies. A risk-free investment paying 4% annually is a good place to park money. In trading, the Energy and Utilities climbed the most while the interest sensitive Consumer Cyclicals and Technology sectors had the biggest drops.

Weekly Portfolio Review

For the week, the TSX dropped 0.7%, the S&P 500 fell 1.1%, the Dow sank 0.2% and the Nasdaq declined 2.4%.

![]()

For the first time in 2023 all four indexes ended the week lower. It had to happen sooner or latter but with the TSX and the Nasdaq posting their first weekly losses, all four major North American indexes have now had at least one week where they lost ground. This was also the first time all indexes ended the week lower. The main driver of the markets was concerns the US benchmark interest rate increases would continue and remain longer than investors originally thought.

With the four indexes all lower for the week, it was no surprise the three portfolios were also down, as you can see blow. I’ve said previously that the portfolios roughly align with an index and that appears to have happened again. Portfolio 1, with the most companies compared to the other two seems to mirror the S&P. Portfolio 2 with its less risky approach and preponderance of larger Canadian companies aligns with the TSX. Finally, Portfolio 3 with its growth-oriented approach tends to follow the Nasdaq. This week the losses in the indexes were reflected in the losses in the portfolios. I much prefer it when the indexes rise and floats all the portfolios. 😊

Companies on the Radar

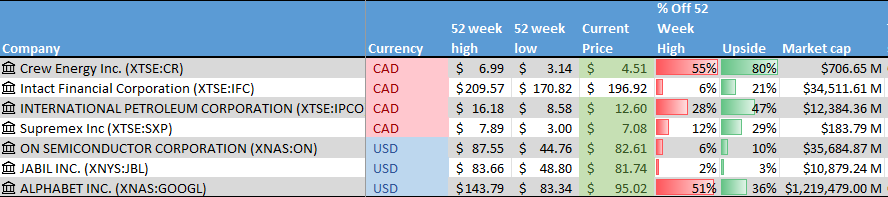

Two new technology companies crossed my radar this past week. The first is ON Semiconductor (NASD:ON) an American company that makes intelligent sensing and power solutions that enable the electrification of the automotive industry. The other is Jabil Inc. (NYSE:JBL), an American global company that specializes in providing manufacturing services and solutions. They make products for other companies, including “300 of the biggest brands in the world in every market from healthcare, packaging, smartphones and cloud equipment to automotive and home appliances.”

I had never heard of either company but from a quick check on Yahoo Finance they appear to provide semiconductors for a wide variety of companies and uses. With the growth of electronic and ‘smart’ products, I think the semiconductor industry has a long runway. I need to dig deeper on both companies but for now I’ll add them to the existing five companies on my Radar List, below.

- Crew Energy (TSX:CR): A Canadian oil and gas company with interests in British Columbia.

- Intact Financial (TSX:IFC): a mid size insurance company supplying home, car and business insurance in Canada, the US, and the UK.

- International Petroleum (TSX:IPCO): A Canadian company with oil and gas assets in Canada, Malaysia, and France.

- Supremex: (TSX:SXP) a small cap company selling packing solutions throughout Canada and the USA.

- Alphabet: The leading online search engine and advertising company, dominant mobile operating system.

The Radar Check was last updated February 10, 2022.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended February 10, 2023: DOWN ![]()

- Alphabet’s share price took a dive after their artificial intelligence chatbot Bard failed a test in its first public appearance. During the presentation Google did not provide a timeline for when Bard would be integrated into its search engine.

- Magnite (NASD:MGNI) announced their new Magnite Streaming service. Magnite Streaming will allow media owners to maximize the value of their assets holistically across live and Video On Demand inventory, CTV (Connected TV) and OTT (Over The Top) environments, while gaining insights to how their ads are working.

- Docebo (TSX:DCBO) was named a Core leader for Learning Systems by the Fosway Group, Europe’s top HR Industry analyst. It was the sixth straight year for Docebo to win this title. Fosway’s Core Leaders are companies with excellent record of enterprise win rates, customer delivery and support.

- General Motors (NYSE:GM) announced a deal with semiconductor manufacturer Globalfoundries (NASD:GFS) to secure chip production to avoid shortages which have plagued the automotive industries for the last few years.

- Ford (NYSE:F) has lowered its stake in Rivian (NASD:RIVN) to a minimal 1%. When Rivian went public in late 2021, Ford had a 11% stake in the new electric vehicle company.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Bank of Nova Scotia (TSX:BNS) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

TMX Group Limited

All currency listed in millions of Canadian dollars, except earnings per share.

Selected highlights from their fourth quarter 2022 financial results on February 6, 2023

- Revenue of $274.1 for the three months ended December 31, compared to $252.4 for the same period in 2021. An increase of almost 22%.

- Net income of $102.2 for the three months ended December 31, compared to net income of $87.9 in the same period in 2021.

- Diluted earnings per ordinary share of $1.83 for the three months ended December 31, compared to $1.56 for the same period in 2021.

- Revenue of $1,116.6 for the year ended December 31, compared to $980.7 for the same period in 2021. An increase of over 14%.

- Net earnings of $542.7 for the year ended December 31, compared to net earnings of $338.5 in the same period in 2021.

- Diluted earnings per ordinary share of $9.69 for the year ended December 31, compared to $5.99 for the same period in 2021.

Pinterest, Inc.

All currency listed in thousands of US dollars, except earnings per share.

Selected highlights from their fourth quarter 2022 financial results on February 6, 2023

- Revenue of $877,209 for the three months ended December 31, compared to $846,655 for the same period in 2021. An increase of 4%.

- Net income of $17,491 for the three months ended December 31, compared to net income of $174,699 in the same period in 2021.

- Diluted earnings per ordinary share of $0.03 for the three months ended December 31, compared to $0.25 for the same period in 2021.

- Revenue of $2,802,574 for the year ended December 31, compared to $2,578,027 the same period in 2021. An increase of 9%.

- Net loss of $96,047 for the year ended December 31, compared to net earnings of $316,438 in the same period in 2021.

- Diluted loss per ordinary share of $0.14 for the year ended December 31, compared to earnings of $0.46 for the same period in 2021.

Skyworks Solutions, Inc.

All currency listed in millions of US dollars, except earnings per share.

Selected highlights from their first quarter 2023 financial results on February 6, 2023

- Revenue of $1,329.3 for the three months ended December 31, compared to $1,510.4 for the same period in 2021. A decrease of almost 12%.

- Net income of $309.4 for the three months ended December 31, compared to net income of $399.9 in the same period in 2021.

- Diluted earnings per ordinary share of $1.93 for the three months ended December 31, compared to $2.40 for the same period in 2021.

PayPal Holdings, Inc.

All currency listed in millions of US dollars, except earnings per share.

Selected highlights from their fourth quarter 2022 financial results on February 9, 2023

- Revenue of $7,383 for the three months ended December 31, compared to $6,918 for the same period in 2021. An increase of almost 7%.

- Net income of $921 for the three months ended December 31, compared to net income of $801 in the same period in 2021.

- Diluted earnings per ordinary share of $0.81 for the three months ended December 31, compared to $0.68 for the same period in 2021.

- Revenue of $27,518 for the year ended December 31, compared to $25,371 for the same period in 2021. An increase of over 8%.

- Net earnings of $2,419 for the year ended December 31, compared to net earnings of $4,169 in the same period in 2021.

- Diluted earnings per ordinary share of $2.09 for the year ended December 31, compared to $3.52 for the same period in 2021.

Telus Corporation

All currency listed in millions of Canadian dollars, except earnings per share.

Selected highlights from their fourth quarter 2022 financial results on February 9, 2023

- Revenue of $5,023 for the three months ended December 31, compared to $4,872 for the same period in 2021. An increase of over 3%.

- Net income of $265 for the three months ended December 31, compared to net income of $663 in the same period in 2021.

- Basics earnings per ordinary share of $0.17 for the three months ended December 31, compared to $0.47 for the same period in 2021.

Cloudflare, Inc.

All currency listed in thousands of US dollars, except earnings per share.

Selected highlights from their fourth quarter 2022 financial results on February 9, 2023

- Revenue of $274,700 for the three months ended December 31, compared to $193,596 for the same period in 2021. An increase of almost 42%.

- Net loss of $45,917 for the three months ended December 31, compared to a net loss of $77,501 in the same period in 2021.

- Diluted loss per ordinary share of $0.14 for the three months ended December 31, compared to a loss per share of $0.24 for the same period in 2021.

- Revenue of $975,241 for the year ended December 31, compared to $656,426 for the same period in 2021. An increase of over 48%.

- Net loss of $193,381 for the year ended December 31, compared to a net loss of $260,309 in the same period in 2021.

- Diluted loss per ordinary share of $0.59 for the year ended December 31, compared to loss per share of $0.83 for the same period in 2021.

Portfolio 2

Portfolio 2 for the week ended February 10, 2023: DOWN ![]()

- Telus (TSX:T) partnered with virtual reality (VR) developer Paperplane Therapeutics to deliver VR headsets to the Fondation de l’Hotel-Dieu d’Alma (the Alma Hospital Foundation) to lower the anxiety level of patients in the Hospital’s psychiatry ward. A study has shown that 80% of patients that used the VR headsets felt less stress while undergoing treatment.

- Guardant Health’s (NASD:GH) Guardant360 CDx liquid biopsy test will now be covered by UnitedHealthcare as a companion diagnostic in advanced lung and breast cancer tests.

- MongoDB (NASD:MDB) received the US government’s Federal Risk and Authorization Management Program (FEDRAMP) Moderate Authorization security clearance. FedRAMP is a standardized approach to security authorization to provide cloud services to US government agencies. The Moderate level is when a loss of confidentiality would seriously impact an agency’s operations, such as damage to assets, financial loss or individual harm (but not death).

- In an attempt to save $5.5 billion in expenses, Disney (NYSE:DIS) announced they would let go 7,000 people from its global workforce. They have also restructured into three divisions: Disney Entertainment (all of their TV, film and streaming units); ESPN; and Disney Parks, Experiences and Products.

The state of Florida passed a bill authorizing the governor to appoint five supervisors to run what is now known as the Reedy Creek Improvement District. This effectively gives the state control of the board that oversees development in and around Disney’s Florida parks. The board will not be involved in day to day operations of the numerous Disney theme parks but it will have the authority to collect revenue, pay off debt and provide a range of government services. - TC Energy (TSX:TRP) reported a combination of things led to the failure of their Keystone pipeline back in December. The report identified a welding flaw and bending stress as possible causes.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Bank of Nova Scotia (TSX:BNS) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

Take-Two Interactive Software, Inc.

All currency listed in millions of US dollars, except earnings per share.

Selected highlights from their third quarter 2022 financial results on February 6, 2023

- Revenue of $1,407.8 for the three months ended December 31, compared to $903.3 for the same period in 2021. An increase of almost 56%.

- Net loss of $153.4 for the three months ended December 31, compared to net income of $144.6 in the same period in 2021.

- Diluted loss per ordinary share of $0.91 for the three months ended December 31, compared to earnings of $1.24 for the same period in 2021.

- Revenue of $3,903.7 for the nine months ended December 31, compared to $2,574.8 the same period in 2021. An increase of almost 52%.

- Net loss of $514.4 for the nine months ended December 31, compared to net earnings of $307.1 in the same period in 2021.

- Diluted loss per ordinary share of $3.27 for the nine months ended December 31, compared to earnings of $2.63 for the same period in 2021.

The Walt Disney Company

All currency listed in millions of US dollars, except earnings per share.

Selected highlights from their first quarter 2023 financial results on February 8, 2023

- Revenue of $23,512 for the three months ended December 31, compared to $21,819 for the same period in 2021. An increase of almost 8%.

- Net income of $1,361 for the three months ended December 31, compared to net income of $1,200 in the same period in 2021.

- Diluted earnings per ordinary share of $0.70 for the three months ended December 31, compared to earnings of $0.60 for the same period in 2021.

Telus Corporation

All currency listed in millions of Canadian dollars, except earnings per share.

Selected highlights from their fourth quarter 2022 financial results on February 9, 2023

- Revenue of $5,023 for the three months ended December 31, compared to $4,872 for the same period in 2021. An increase of over 3%.

- Net income of $265 for the three months ended December 31, compared to net income of $663 in the same period in 2021.

- Basics earnings per ordinary share of $0.17 for the three months ended December 31, compared to $0.47 for the same period in 2021.

Fortis Inc.

All currency listed in millions of Canadian dollars.

Selected highlights from their fourth quarter 2022 financial results on February 10, 2023

- Revenue of $3,168 for the three months ended December 31, compared to $2,583 for the same period in 2021. An increase of over 22%.

- Net income of $370 for the three months ended December 31, compared to net income of $328 in the same period in 2021.

- Diluted earnings per ordinary share of $0.77 for the three months ended December 31, compared to $0.69 for the same period in 2021.

- Revenue of $11,043 for the year ended December 31, compared to $9,448 for the same period in 2021. An increase of almost 17%.

- Net earnings of $1,514 for the year ended December 31, compared to net earnings of $1,405 in the same period in 2021.

- Diluted earnings per ordinary share of $2.78 for the year ended December 31, compared to $2.61 for the same period in 2021.

Portfolio 3

Portfolio 3 for the week ended February 10, 2023: DOWN ![]()

- Microsoft (NASD:MSFT) is incorporating artificial intelligence into its Bing search engine and Edge browser. Using a chatbot based on ChatGPT, it will be able to summarize web pages and integrate different sources, among other capabilities.

- Brookfield Asset Management (TSX:BAM) increased its property and casualty insurance footprint in the US with the acquisition of Argo Group International (NYSE:ARGO). The deal is worth $1.1 billon and is expected to close later in 2023.

- Enghouse Systems (TSX:ENGH) announced they acquired Mobi All Tecnologia S.A. (Navita), a Brazilian Software as a Service provider of Enterprise Mobility Management Solutions. Navita specializes in mobility and telecom expense management. Through this acquisition Enghouse hopes to expand their business in Brazil and upsell Navita’s solutions to their other clients.

- Shopify (TSX:SHOP) is launching a shopping channel. Actually, it is a live video shopping feature, one of many new innovative products Shopify plans to roll out to attract new audiences for their merchants.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

Telus International Inc.

All currency listed in millions of US dollars, except earnings per share.

Selected highlights from their fourth quarter 2022 financial results on February 9, 2023

- Revenue of $630 for the three months ended December 31, compared to $600 for the same period in 2021. An increase of almost 5%.

- Net income of $34 for the three months ended December 31, compared to net income of $36 in the same period in 2021.

- Diluted earnings per ordinary share of $0.13 for the three months ended December 31, compared to $0.13 for the same period in 2021.

- Revenue of $2,468 for the year ended December 31, compared to $2,194 for the same period in 2021. An increase of over 12%.

- Net earnings of $183 for the year ended December 31, compared to net earnings of $78 in the same period in 2021.

- Diluted earnings per ordinary share of $0.68 for the year ended December 31, compared to $0.29 for the same period in 2021.

Cloudflare, Inc.

All currency listed in thousands of US dollars, except earnings per share.

Selected highlights from their fourth quarter 2022 financial results on February 9, 2023

- Revenue of $274,700 for the three months ended December 31, compared to $193,596 for the same period in 2021. An increase of almost 42%.

- Net loss of $45,917 for the three months ended December 31, compared to a net loss of $77,501 in the same period in 2021.

- Diluted loss per ordinary share of $0.14 for the three months ended December 31, compared to a loss per share of $0.24 for the same period in 2021.

- Revenue of $975,241 for the year ended December 31, compared to $656,426 for the same period in 2021. An increase of over 48%.

- Net loss of $193,381 for the year ended December 31, compared to a net loss of $260,309 in the same period in 2021.

- Diluted loss per ordinary share of $0.59 for the year ended December 31, compared to loss per share of $0.83 for the same period in 2021.

Brookfield Corporation

All currency listed in millions of US dollars, except earnings per share.

Selected highlights from their fourth quarter 2022 financial results on February 6, 2023

- Revenue of $24,213 for the three months ended December 31, compared to $21,787 for the same period in 2021. An increase of over 11%.

- Net income of $44 for the three months ended December 31, compared to net income of $3,461 in the same period in 2021.

- Diluted earnings per ordinary share of $0.23 for the three months ended December 31, compared to $0.66 for the same period in 2021.

- Revenue of $92,769 for the year ended December 31, compared to $75,731 for the same period in 2021. An increase of over 22%.

- Net earnings of $5,195 for the year ended December 31, compared to net earnings of $12,388 in the same period in 2021.

- Diluted earnings per ordinary share of $1.19 for the year ended December 31, compared to $2.39 for the same period in 2021.