Risky Business

One phrase I keep running into early on my investing journey is “risk on, risk off.” At first, I thought it just meant investors were either piling into riskier assets (like technology stocks) or playing it safe with something more stable (like utility stocks). And while that’s partly true, there’s a bit more nuance behind it.

At its core, “risk on, risk off” is about investor mood – or more technically, risk tolerance. It’s a strategy that reflects how confident (or nervous) people feel about the market at any given moment.

- Risk-on means optimism is in the air. Investors are more comfortable taking on risk for higher potential returns, so money flows into stocks, high-yield bonds, cryptocurrencies, and other growth-focused assets. In my case, this would be investing in high growth stocks such as technology companies.

- Risk-off kicks in when fear or uncertainty takes over – maybe because of weak economic data, rising inflation, or geopolitical tensions. In those moments, investors move into safer territory like US Treasuries, gold, cash, or defensive sectors. For me, this would be stocks in the utility or consumer staple sectors.

These shifts can happen fast. Markets might flip between risk-on and risk-off within a single trading session depending on headlines or economic releases. Big catalysts include central bank decisions, inflation numbers, job reports, global events, and more recently, social media posts from President Trump.

A perfect recent example of this dynamic? President Trump. His actions have been major drivers of both market rallies and sell-offs due to his unpredictable policy shifts and fiery rhetoric.

During his second term, Trump’s aggressive tariff rollouts triggered serious volatility. Sweeping duties on imports from China, Mexico, and Canada rattled global markets, prompting a sharp move into risk-off territory. Stocks fell, and investors piled into safer, more stable assets like bonds and gold.

But when he signaled a pause or softened his tone, sentiment often reversed. Stocks bounced back, risk appetite returned, and investors poured back into growth stocks.

Trump’s presidency has been a masterclass in how fragile market sentiment can be – with sudden policy reversals keeping everyone on edge. It’s a real-world example of just how quickly markets can swing depending on the tone from the top.

So, when you hear someone say “risk-on” or “risk-off,” think of it as the market’s mood ring: green means go, red means retreat. 😊

This week, that market mood ring kept flashing green and red as investors tried to make sense of the latest inflation data, earnings results, and the ongoing fallout from Trump’s tariff moves. With sentiment swinging almost daily, it was a classic example of how quickly we can shift between fear and optimism. Let’s take a look at what moved the markets this week, how the major indexes performed, and what it all means for us investors. 👇

Items that may only interest or educate me ….

Canadian Economic news, American Economic news, First 100 days, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Bank of Canada meeting minutes

The Bank of Canada’s minutes from its April 16 meeting showed policymakers opted to hold the benchmark interest rate steady at 2.75%, pausing after seven straight cuts since June 2024. The decision reflected growing uncertainty, especially around US trade policy and the sweeping tariffs introduced earlier in the month.

Council members noted mixed economic signals: consumer sentiment and business confidence had softened, but the labour market remained relatively stable. Worries about a potential US recession and broader global slowdown weighed heavily on the discussion.

The Governing Council considered two scenarios – one where the tariffs are temporary, and another where they linger and potentially drive inflation above 3% by 2026. While some members pushed for another rate cut to support a slowing economy, others favoured caution, pointing to the inflation risks tied to higher import costs.

In the end, the Bank chose to hold the rate at the current level and wait for more clarity, stressing the need to balance support for growth with maintaining price stability. The minutes reiterated that the Bank remains ready to act if signs of stronger disinflation or a sharper downturn emerge.

Gross Domestic Product (GDP)

Canada’s economy contracted by 0.2% in February 2025, following a 0.4% gain in January, as severe winter storms weighed on economic activity. The drop was led by a 0.6% decline in goods-producing industries, with ‘Mining, quarrying, and oil and gas extraction’ plunging 2.5%. Service-producing industries also slipped 0.1%, dragged down by a sharp 4.2% decline in the ‘Management of companies and enterprises’ category.

Still, there were a few bright spots. The ‘Manufacturing’ sector posted a 0.6% gain – its fourth straight monthly increase – thanks to strength in durable goods like machinery. ‘Finance and insurance’ also grew 0.7%, offering a bit of a cushion amid broader weakness.

On a year-over-year basis, GDP was up 1.6%, slowing from 2.4% in January but still showing some resilience. Notably, the ‘Utilities’ sector remained up 8.5% from a year earlier. The overall February dip was largely blamed on extreme weather, which disrupted transportation services across Central and Eastern Canada as well as parts of B.C.

Looking ahead, Statistics Canada’s advance estimate for March points to a modest 0.1% uptick, bringing estimated first quarter growth to 0.4%.

Canadian market volatility

Canada’s market stress meter – the S&P/TSX 60 VIX (VIXC) – started the week on edge at 22.68 before easing down to 18.35 by market close on Friday. That’s just inside the range of “business as usual,” suggesting that investor anxiety is easing, at least temporarily. A declining volatility index typically signals greater market confidence, meaning traders may be adjusting to the recent turbulence rather than reacting with panic.

For anyone just getting familiar, the VIXC is Canada’s version of a fear gauge. Readings below 10 reflect strong investor confidence, 10–20 signals normal volatility, and anything above 20 points to growing uncertainty.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Consumer Confidence Index (CCI)

Consumer confidence took another hit in April, with the Conference Board’s Consumer Confidence Index falling to 86.0 – its lowest level since May 2020 – down from 92.9 in March. That marks five straight months of decline and came in below expectations of 87.9.

The Present Situation Index, which reflects how Americans view current business and job conditions, dipped slightly to 133.5 from 134.4. But the real red flag was the Expectations Index, which plunged 12.5 points to 54.4 – well below the 80 mark that often signals a recession, and the lowest reading since October 2011.

This sharp drop in expectations likely reflects growing concerns about rising prices due to tariffs, a cooling labour market, and broader fears of an economic slowdown. When future confidence falls this low, consumer spending often follows – putting more pressure on retail and the wider economy. Combine that with the market volatility earlier this month, and it’s no surprise that confidence continues to slide.

Gross Domestic Product (GDP)

According to the Department of Commerce’s Bureau of Economic Analysis (BEA), the US economy contracted by 0.3% in the first quarter of 2025, marking the first decline since early 2022 and falling well short of expectations for 0.4% growth. It’s a sharp reversal from the 2.4% expansion seen in the previous quarter and adds to growing concerns about the economy’s trajectory.

The biggest drag came from a 41% surge in imports, as businesses rushed to stockpile goods ahead of new tariffs. Since imports are subtracted from GDP, the spike delivered a heavy blow – shaving about 5% off growth. Government spending also declined, likely reflecting mass layoffs of federal employees, compounding the slowdown.

There were still a few bright spots: consumer spending rose 1.8%, and private investment remained stable – though both cooled noticeably from the fourth quarter of 2024, when consumer spending grew by 4%.

With tariffs rising, inflation lingering, and policy uncertainty in the mix, recession worries are back in focus. While President Trump has tried to shift blame for the weak performance onto his predecessor, the economy was under his leadership for most of the quarter. It was his administration that imposed the sweeping new tariffs – raising rates on nearly all major US trading partners. That move typically leads to higher prices, especially for imported products and materials. If these early returns are any indication, the new policies aren’t exactly confidence inspiring.

Personal Consumption Expenditures (PCE)

The latest PCE inflation data from the BEA came in with a bit of a twist. Headline prices rose 0.7% in March – hotter than expected – after a 0.4% gain in February. Analysts had been bracing for a flat reading, so the increase definitely turned a few heads. On a year-over-year basis, inflation eased to 2.3% from 2.7%, still a touch above the 2.2% forecast.

Core PCE, which excludes food and energy, the Fed’s preferred measure of inflation, was flat in March after rising 0.4% the month prior. That helped bring the year-over-year rate down to 2.6% from 3.0% – a welcome sign that underlying inflation pressures are starting to cool.

Overall, the data shows the US economy is holding up where it counts: consumer spending. People are earning more and were still spending, which is good news for businesses and growth. Better yet, prices aren’t rising as quickly, offering a rare combination that should keep both consumers and the Fed happy. 😊

The only catch? This data came in before the chaos unleashed by President Trump’s global trade war. The April inflation reports – both the PCE and Consumer Price Index – will offer the first real look at how tariffs ripple through the economy and whether inflation is about to heat back up.

Labour data

The latest updates from the Job Openings and Labor Turnover Survey (JOLTS), the ADP Employment Report, and the Employment Situation Summary (ESS) offer a snapshot of the US labour market – showing continued resilience, but also some signs of stress on the horizon.

JOLTS

The latest JOLTS report from the US Bureau of Labor Statistics showed job openings slipped to 7.19 million in March, down from a revised 7.48 million in February – and just below expectations. The ratio of job openings to unemployed workers dipped to 1.02, signalling that the labour market continued to cool heading into April’s tariff tensions.

This ongoing drop in job openings – well off the peak of 12 million in March 2022 – points to a broader hiring slowdown. It likely reflects growing caution from businesses amid rising economic uncertainty and the looming threat of new import tariffs. Still, while the labour market is softening, demand hasn’t fallen off a cliff – it’s holding steady, at least for now.

(Quick reminder: JOLTS tracks job openings as of the last business day of the month—in this case, March.)

ADP

The April ADP Employment Report showed US private sector job growth slowing to just 62,000 – the smallest monthly gain since July 2024 and well below the 120,000 jobs economists had expected. It’s also a sharp drop from March’s 155,000 new jobs, adding to signs that the labour market is losing steam.

Annual pay growth for job-stayers came in at 4.5%, a slight dip from last month, pointing to a broader trend of slowing wage momentum. The weaker job gains and easing pay growth suggest businesses are becoming more cautious, likely in response to growing economic uncertainty.

ESS

The US labour market added 177,000 jobs in April, beating expectations of a 120,000 gain – but still down from March’s 228,000 increase. While that’s a solid showing, it hints at a gradual cooling in job creation.

The unemployment rate held steady at 4.2%, keeping it within the narrow range of 4.0% to 4.2% where it’s been since last May. Wage growth also showed signs of moderation. Average hourly earnings rose 0.2% in April, following a 0.3% increase in March. Over the past year, wages are up 3.8% – still respectable, but slower than earlier in the cycle.

Overall, the labour market is holding up well, but there are cracks starting to show. Slower wage growth and the dip in job gains suggest businesses are becoming more cautious – likely due to the uncertainty sparked by the latest round of US tariffs. With higher costs and disrupted supply chains, many companies are taking a wait-and-see approach before expanding headcount.

Overall labour market summary

The latest data from JOLTS, ADP, and the Employment Situation Summary points to a cooling US job market. Slower hiring and wage growth could ease inflation pressures, but they also raise concerns about the broader economy if the slowdown continues.

Tariff uncertainty is adding to the drag on business sentiment. Higher import costs from tariffs are squeezing margins, leading many companies to delay hiring or scale back expansion plans.

While the labour market is still growing, the pace has clearly slowed – shaped by economic uncertainty, trade tensions, and fading momentum in both job creation and pay. Most of the recent data doesn’t yet reflect the full impact of President Trump’s new tariffs, as many were delayed by three months. However, tariffs on Chinese imports did take effect in April, and their impact could weigh more heavily on the job market in the months ahead.

American market volatility

The CBOE Volatility Index (VIX), often called the market’s “fear gauge,” opened the week at 25.75 and hovered between 27 and 23 before closing at 22.68 on Friday. The ride wasn’t exactly smooth – it was a rollercoaster ride with a sharp spike above 28 midweek followed the latest GDP report that showed the economy had unexpectedly contracted, reminding investors just how jittery the market remains.

Despite the bumps, the VIX continues to drift lower week by week, as investors gradually adjust to the uncertainty stirred up by President Trump’s aggressive trade policies.

For anyone new to the VIX: it’s basically Wall Street’s stress meter. Readings below 12 suggest markets are calm, 12–20 is the “business as usual” zone, and anything above 20 signals heightened anxiety.

First 100 days

This past week marked the first 100 days of President Trump’s return to office – and it’s been a rocky ride for markets. Despite lofty expectations from some investors following his re-election, the reality has been far more turbulent. US stocks suffered their worst start to a presidential term in over half a century, with trillions in asset value erased.

The S&P 500 Index (S&P) fell 7.9%, the Dow Jones Industrial Average (DJIA) dropped 6.8%, and the Nasdaq Composite Index (Nasdaq) plunged 11%, marking the roughest opening stretch since President Nixon’s second term in 1973. Trump’s aggressive trade policies were the main trigger, as new tariffs targeting Canada, Mexico, and China disrupted supply chains and rattled investor confidence. The early April announcement of a blanket 10% tariff on all imports sparked a sharp sell-off, leading to the S&P 500’s steepest four-day decline since March 2020.

With recession fears and global tensions adding to the mix, market volatility has become the new normal – to the point where many investors seem almost numb to the whiplash. There were brief rebounds when the administration hinted at walking back some tariffs, but for now, uncertainty is the defining theme. For those who were greedy while others were fearful, there were plenty of chances to “buy the dip.” 😊

Another major casualty of Trump’s first 100 days was oil. Benchmark US crude prices dropped over 20%, falling to around US$60 per barrel – levels not seen since the depths of the COVID-19 pandemic, and well below the US$65 breakeven point for many American producers.

The slide was largely driven by growing fears of a global slowdown tied to Trump’s trade actions. New tariffs raised concerns about weaker demand for oil, while OPEC+ ramped up production during the same stretch, adding further pressure. Sanctions on Iranian oil offered some support, but it wasn’t enough to outweigh the broader bearish sentiment fueled by economic uncertainty.

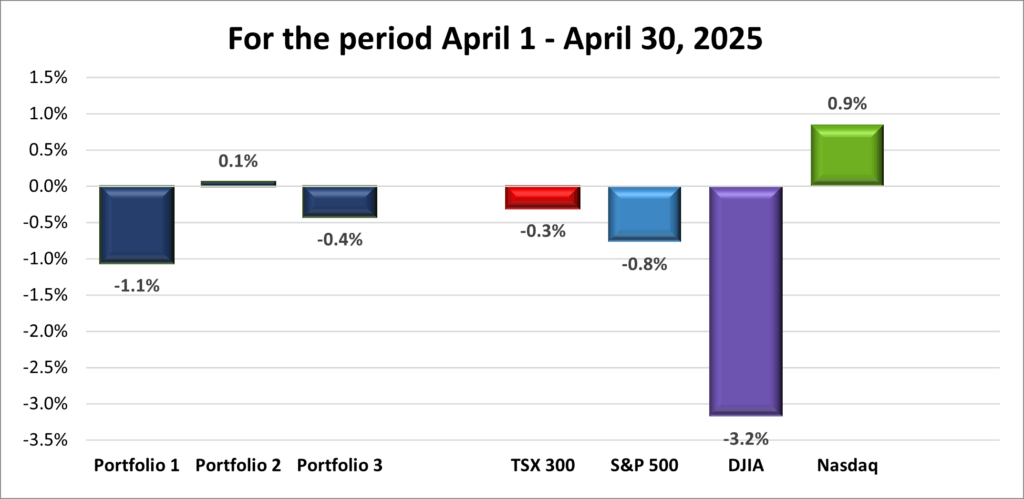

Weekly Market and Portfolio Review

For the week, the TSX (SPTSX) grew 1.3%, the S&P 500 (SPX) gained 2.9%, the DJIA (INDU) rose 3.0% and the Nasdaq (CCMP) climbed 3.4%.

| Index | Weekly Streak |

| TSX: | 4 – week winning streak |

| S&P: | 2 – week winning streak |

| DJIA: | 2 – week winning streak |

| Nasdaq: | 2 – week winning streak |

![]() It’s been a while, but markets finally delivered back-to-back weekly gains – something we hadn’t seen since January. All four major North American indexes – the Toronto Stock Exchange Composite Index (TSX), S&P, DJIA, and Nasdaq – ended the week in the green, keeping the positive momentum going.

It’s been a while, but markets finally delivered back-to-back weekly gains – something we hadn’t seen since January. All four major North American indexes – the Toronto Stock Exchange Composite Index (TSX), S&P, DJIA, and Nasdaq – ended the week in the green, keeping the positive momentum going.

It wasn’t the smoothest start, with the Nasdaq dipping slightly on Monday, but the rest of the week held firm. The DJIA and S&P quietly strung together nine consecutive daily gains – the longest winning streak for the S&P since November 2004 and for the DJIA since December 2023. For the S&P, the streak also helped erase the losses that followed President Trump’s sweeping tariff announcement on April 2. After a few unpredictable and volatile weeks, the mood felt cautiously optimistic.

What moved the markets?

Three main forces drove the markets this past week: economic data, earnings reports, and (as usual) tariffs.

The latest economic numbers gave investors a better look at how the US economy is absorbing the impact of new tariffs. Consumer confidence fell to its lowest level since the early days of the pandemic, and first quarter GDP contracted – raising doubts about whether the administration’s policies are boosting growth or holding it back. The labour market also showed signs of cooling, with fewer job openings, slower private sector hiring, and softer wage growth.

On the earnings front, big tech helped ease investor nerves. Microsoft (NASD: MSFT) and Meta (NASD: META) both posted strong results, easing concerns that their heavy artificial intelligence (AI) investments wouldn’t deliver returns. Their performance not only reassured investors but also suggested that, at least for now, tariffs haven’t slowed corporate spending – particularly in AI.

Still, many companies refrained from offering forward guidance, pointing to continued uncertainty from the trade war. With shifting policies and rising input costs, it’s getting harder for executives to confidently forecast the quarters ahead.

Tariffs remained in focus. This past week President Trump announced new exemptions for some foreign auto and parts imports to avoid “stacked” tariffs. Under the changes, companies like automakers will now pay only the highest applicable tariff, rather than multiple layers. Meanwhile, Commerce Secretary Howard Lutnick said a deal had been reached with one trading partner, and Treasury Secretary Scott Bessent reported progress on talks with India, South Korea, and Japan.

North of the border

In Canada, the TSX finally returned to positive territory for the first time since April 2, 2025. Investors welcomed the clarity brought by the newly elected federal government, seen as more business-friendly than the previous. That said, many businesses are taking a wait-and-see approach, as the new Prime Minister has so far left much of the previous government’s economic policies in place. Also weighing on the TSX was a sharp drop in oil prices – the biggest monthly decline in over three years.

For now, the markets stared into the jaws of a bear market and managed to avoid a mauling. But it’s too early to say whether the worst is behind us. Hopefully, the extreme volatility that’s rocked markets in recent weeks is fading – but we’re still just one social media post away from another wild ride. Still, after a stretch of uncertainty, it’s encouraging to see signs of stability – and maybe even a return to more traditional growth.

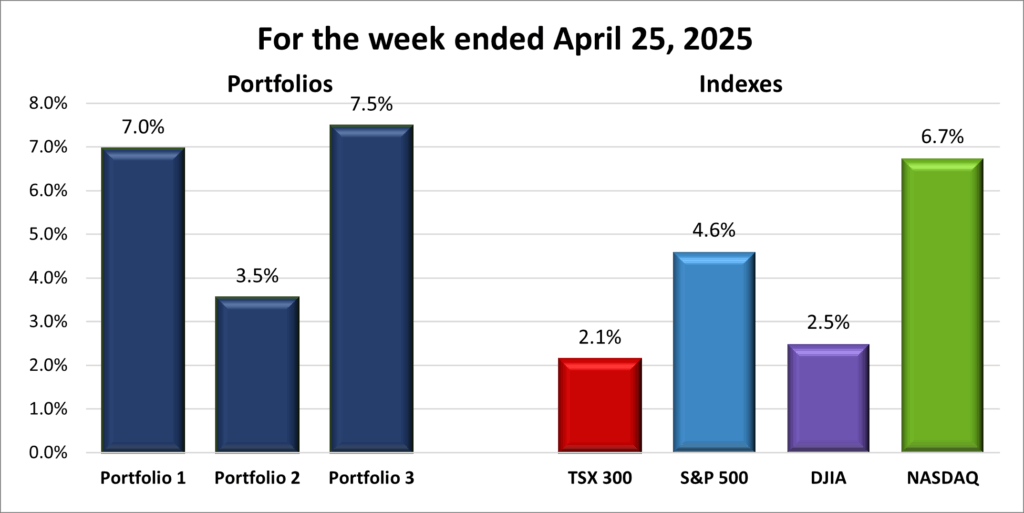

| Portfolio | Weekly Streak |

| Portfolio 1: | 2 – week winning streak |

| Portfolio 2: | 3 – week winning streak |

| Portfolio 3: | 4 – week winning streak |

![]() A strong week in the markets meant the rising tide lifted all boats – or in this case, all three of my portfolios, as shown in the chart below. It was great to see each one extend its win streak another week. 😊

A strong week in the markets meant the rising tide lifted all boats – or in this case, all three of my portfolios, as shown in the chart below. It was great to see each one extend its win streak another week. 😊

Portfolio 1 posted a modest 2.3% gain. I was hoping for more, especially since 75% of the holdings ended the week in the green – including my largest position, Nvidia (NASD: NVDA). That said, there weren’t any standout gains over 10%, which likely kept the overall growth in check. One bright spot: TMX Group (TSE: X) hit an all-time high, which is always nice to see.

Portfolio 2 also advanced 2.3%, with 55% of its holdings finishing positive. The big movers? Take-Two Interactive (NASD: TTWO) and Fortis (TSE: FTS) both hit record highs, while Microsoft surged 11% following a strong earnings report. Solid across the board.

Portfolio 3 had the best weekly performance – up 2.7% – with a strong 76% of its companies gaining on the week. Microsoft’s rally gave the portfolio a boost, helping offset a steep 19.3% drop in Evolution Gaming Group AB (OTCM: EVVTY). That one stung. 😬

The sharp drop came after news broke that the UK Gambling Commission had launched a review of Evolution Malta Holding Limited, a subsidiary of Sweden’s Evolution Gaming Group AB. The investigation rattled investors, raising concerns not just about the subsidiary but about Evolution’s broader compliance practices. With the potential for fines – or even a licence revocation – the uncertainty sent shares tumbling to a three-year low. Ouch! ☹

With all three portfolios now on winning streaks, it’s nice to see some consistency after weeks of volatility and uncertainty. Hopefully, the markets can keep clawing back the ground lost since the start of President Trump’s tariff wars and start riding the tailwinds many investors had been hoping for since November – lower taxes, fewer regulations, and a more stable policy environment. If that happens, there’s a good chance this streak still has room to run. 😊

Companies on the Radar

It was a quiet week on my investing radar. No new companies popped up, but I did make one change: I decided to drop iA Financial Corporation (TSE: IAG) from the list. After taking a closer look, it felt a little too similar to some of the other financial names already on my radar — like goeasy Ltd. (TSE: GSY), LPL Financial Holdings Inc. (NASD: LPLA), and Main Street Capital Corp. (NYSE: MAIN). Between them, GSY and LPLA seem like stronger opportunities, and MAIN still has me curious. With IAG off the board, my radar list is now down to these five companies:

It was a quiet week on my investing radar. No new companies popped up, but I did make one change: I decided to drop iA Financial Corporation (TSE: IAG) from the list. After taking a closer look, it felt a little too similar to some of the other financial names already on my radar — like goeasy Ltd. (TSE: GSY), LPL Financial Holdings Inc. (NASD: LPLA), and Main Street Capital Corp. (NYSE: MAIN). Between them, GSY and LPLA seem like stronger opportunities, and MAIN still has me curious. With IAG off the board, my radar list is now down to these five companies:

- goeasy Ltd.: A mid-cap Canadian company offering non-prime leasing and lending services. Higher risk, but high potential if they manage credit cycles well.

- Dollarama (TSE: DOL): A growing large-cap Canadian discount retailer that’s also expanding into South America. With a recession expected in Canada, discount retailers are seeing an increase in business.

- Brookfield Corporation (TSE: BN): A large-cap Canadian heavyweight in alternative asset management and real estate investing.

- LPL Financial Holdings Inc.: A large-cap US firm providing a brokerage and advisory platform for independent financial advisors. Benefiting from long-term trends in wealth management.

- Main Street Capital Corp.: A mid-sized American company that invests in or lends money to smaller private companies to help them grow.

As always, these are not buy recommendations – be sure to do your own research and make decisions that align with your personal financial goals!

The Radar Check was last updated May 2, 2025.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!