How Tariff Wars Are Impacting the Canadian Dollar—And What It Means for Us

With all the talk about tariffs and their effect on the Canadian and US economies, I started wondering – what do these trade battles mean for the already weak Canadian dollar? My first thought? It can’t be good. But that made me realize I wasn’t entirely sure how tariffs influence our currency or what that means for us as consumers, businesses, and investors. As Daenerys Targaryen would say, “Let’s begin!”

Why Tariffs Matter for the Canadian Dollar

The ongoing tariff war – sparked by President Trump’s levies on Canada and met with retaliatory tariffs from the Canadian government – has added uncertainty to global trade. As a country that depends on exports, Canada isn’t immune to the fallout. Here’s how these tariffs are putting pressure on the Canadian dollar:

- Tariffs Make Goods More Expensive Tariffs are basically taxes on imports and exports. When the US imposes tariffs on Canadian goods, it makes them more expensive for American buyers. That can lead to fewer Canadian products being sold internationally, which brings us to the next point….

- Fewer Exports Mean Less Demand for Canadian Dollars Here’s where the Canadian dollar (CAD) comes into play: When other countries buy Canadian goods, they need CAD to pay for them. But if tariffs make Canadian exports less competitive, fewer international buyers will be purchasing them – meaning less demand for our currency. This can weaken the CAD compared to other major currencies, like the US dollar (USD).

- Investors and Risk Sentiment Trade wars create uncertainty, and investors hate uncertainty. When global trade tensions rise, investors tend to move their money into “safe haven” currencies like the US dollar. This can weaken the CAD even further since it’s seen as more vulnerable to trade disruptions.

- Commodities and the CAD Canada’s economy is heavily tied to commodities like oil, gas, and metals. Tariff wars can hurt global trade, lowering demand for these resources. Since the CAD often moves in sync with commodity prices, a drop in demand for oil or minerals can put even more downward pressure on our currency.

In Summary

Tariffs disrupt trade by making goods more expensive, which can hurt Canadian exports. Fewer exports mean less demand for the Canadian dollar, and trade uncertainties can scare off investors, further weakening the CAD. For Canadian consumers, businesses, and investors, these pressures are felt in day-to-day expenses, operational costs, and market movements.

What This Means for Consumers, Businesses, and Investors

For consumers, tariffs often translate to higher prices on imported goods, from electronics to clothing and even groceries. Companies facing increased costs due to tariffs tend to pass those expenses on to shoppers. On top of that, a weaker Canadian dollar makes everything more expensive, including gas, travel, and online purchases from the US. With imports becoming pricier, some Canadians may start shifting their spending habits toward locally made products as a way to manage costs.

For businesses, the impact can be even more direct. Canadian exporters may struggle to compete in global markets if tariffs make their products too expensive. That could mean lower sales and, in some cases, job losses. Meanwhile, companies that rely on imported raw materials are also feeling the pinch, as tariffs drive up supply costs and squeeze profit margins. The uncertainty surrounding trade disputes can make things worse, leading some businesses to put expansion plans on hold or rethink their supply chains.

For investors, tariff wars add another layer of risk to the markets. A weaker Canadian dollar can affect returns on both domestic and international investments, making currency fluctuations something to watch closely. Trade uncertainty also fuels market volatility, which can create opportunities for experienced investors but may be nerve-wracking for beginners. Certain industries – particularly those reliant on exports – could face challenges, while companies focused on domestic markets might gain a competitive edge.

Final Thoughts

Tariff wars have thrown another wrench into an already uncertain global economy, and the Canadian dollar is feeling the pressure. The ripple effects are wide-reaching – higher prices for consumers, costlier operations for businesses, and increased market volatility for investors.

With tariffs continuing to put pressure on the Canadian dollar and adding uncertainty for businesses and consumers, markets have been reacting in their own way. This past week brought fresh economic information in both Canada and the US, and just as importantly, the latest rate decision and economic outlook from the US Federal Reserve. Let’s see how that information affected the markets and the three portfolios….

Items that may only interest or educate me ….

The Fed’s latest rate decision, Canadian Economic news, US Economic news, ….

The Fed’s latest rate decision

As expected, the Fed’s Federal Open Market Committee (FOMC) kept interest rates unchanged at 4.25% – 4.5%. But the bigger news was they still plan to cut rates twice in 2025, in line with their December forecast, which would bring the benchmark rate down to 3.75% – 4.0% by year-end.

Along with the rate decision, the Fed updated its economic projections. Inflation, measured by the Fed’s preferred PCE index, is now expected to end the year at 2.7%, up from the previous 2.5% forecast, before gradually reaching the 2% target by 2027. The unemployment rate is projected to tick up to 4.4% this year, compared to the earlier estimate of 4.3%, before stabilizing at 4.3% in 2026. Meanwhile, GDP growth for 2025 was revised down to 1.7% from the previous 2.1% estimate, with 1.8% growth expected in 2026. The Fed noted that “uncertainty around the economic outlook has increased,” a key factor in its downward revision. At the same time, it acknowledged that trade policy could complicate economic forecasts.

While the Fed didn’t explicitly mention tariffs, analysts warn that global trade tensions could fuel inflation while also dragging down growth – a classic recipe for stagflation. With so many moving parts, the Fed is taking a cautious approach, balancing inflation concerns with the risk of slowing the economy too much.

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Consumer Price Index (CPI)

Statistics Canada reported that annual inflation jumped to 2.6% in February, up from 1.9% in January – the highest reading in eight months. This also marks the first time since last summer that inflation has climbed above 2%, the midpoint of the BoC’s target range. Monthly inflation also surged, rising 1.1% in February compared to just 0.1% in January, much higher than the 0.6% analysts had expected.

Looking at the numbers, some categories saw sharper price increases than others. Compared to January, ‘Recreation, education, and reading’ prices saw the biggest jump at 3.4%, while ‘Transportation’ costs crept up just 0.3%. On a yearly basis, ‘Gasoline’ prices surged 5.1%, making it the biggest driver of inflation, while ‘Alcohol, tobacco, and cannabis’ products had the smallest increase at 0.6%. Meanwhile, the all-important ‘Shelter’ category – covering mortgage costs and rent – rose 4.2% year-over-year and 0.2% month-over-month.

Core inflation, which strips out volatile food and energy prices, also moved higher for the first time in three months. It rose 0.9% in February, pushing the annual core CPI rate up to 2.9% from 2.2% in January.

The end of the GST/HST tax break in mid-February was one of the factors behind the inflation spike. Since sales taxes are included in CPI calculations, the return of the GST directly pushed prices higher (who said higher taxes don’t make things more expensive? 😊). Now, the BoC is shifting its focus to tariffs, watching closely to see if US tariffs and Canada’s countermeasures drive costs even higher.

With inflation picking up speed – both in headline and core measures – the BoC may rethink its plans for rate cuts. Keeping rates steady for now could help prevent further weakening of the Canadian dollar and maintain a more stable economic environment.

Retail sales

According to Statistics Canada, retail sales in Canada fell more than expected in January, declining 0.6% after an upwardly revised 2.6% jump in December. Analysts had expected a smaller drop of 0.4%. On an annual basis, however, sales grew 4.2%, slightly above December’s 3.9% pace.

Core retail sales – which exclude gasoline, fuel vendors, and auto sales – also came in weaker than forecast, slipping 0.2% after a 2.7% gain in December. Analysts had anticipated a smaller 0.1% decline. Year-over-year growth, however, remained steady at 3.0%, matching expectations.

To make matters worse, an early estimate for February points to another 0.4% decline. If confirmed, this would mark the first back-to-back drop in retail sales since mid-2023 – a potential sign that Canadian consumers are tightening their wallets amid economic uncertainty. While some analysts see January’s decline as a return to normal after December’s GST holiday boost, the bigger question is whether consumer spending is losing momentum. Since household spending is a key driver of Gross Domestic Product, a prolonged slowdown could weigh on economic growth in the months ahead.

Canadian market volatility

Canada’s Volatility Index (VIXC) started the week at 16.84, briefly spiking to 18.90 before settling back below 17 and drifting lower as the week went on. By Friday, it closed at 14.33 – indicating that market volatility remained within a typical range. With little new tariff-related news, there wasn’t much to rattle investors.

For those unfamiliar with the VIXC (traded as VIXI on the TSX), think of it as a barometer for market anxiety. A reading below 10 signals strong investor confidence, while 10 to 20 suggests normal market fluctuations. When it rises above 20, uncertainty starts to dominate. This week’s brief jump suggests investors were reacting to shifting economic signals but weren’t bracing for major turbulence.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Retail Sales

Retail sales in February came in weaker than expected, and to make matters worse, January’s numbers were revised even lower. According to the Commerce Department, retail sales rose just 0.2% last month, missing the forecasted 0.6% increase. Meanwhile, January’s sales were revised down to a sharp 1.2% decline – the biggest monthly decline since July 2021.

On a year-over-year basis, retail sales were up 3.1%, but that’s a step down from January’s revised 3.9% gain. Core retail sales, which strip out autos, vehicle parts, and gas stations, fared a bit better with a 0.5% increase in February after falling 0.8% the previous month. Still, the year-over-year growth in core sales slowed slightly to 3.5% from 3.6% in January.

The data suggests consumers are holding back on spending, likely due to inflation concerns and uncertainty stemming from President Trump’s tariffs on America’s biggest trading partners. Some analysts warn that weaker consumer activity could weigh on first-quarter GDP growth, with a potential contraction now in the conversation.

American market volatility

The CBOE Volatility Index (VIX), often called the market’s “fear gauge,” kicked off the week at a volatile 22.9 before steadily trending lower, eventually dipping just below 20. By Friday, it closed at 19.28 – signaling that market tensions eased, and volatility returned to a more typical range.

A few factors likely contributed to this decline: no major tariff-related developments, the Fed maintaining its pause on rate cuts while hinting at two possible cuts later this year, and a lack of any alarming economic data. With no fresh catalysts to shake investor confidence, fear in the market subsided.

For those unfamiliar with the VIX, think of it as a stress meter for stocks. A reading below 12 signals calm conditions, while 12 to 20 reflects typical market fluctuations. Above 20, uncertainty is creeping in, and anything over 30 suggests markets are in turmoil. With the VIX settling under 20, investor sentiment suggests worries are cooling – for now – though cautious optimism remains the dominant theme.

Weekly Market and Portfolio Review

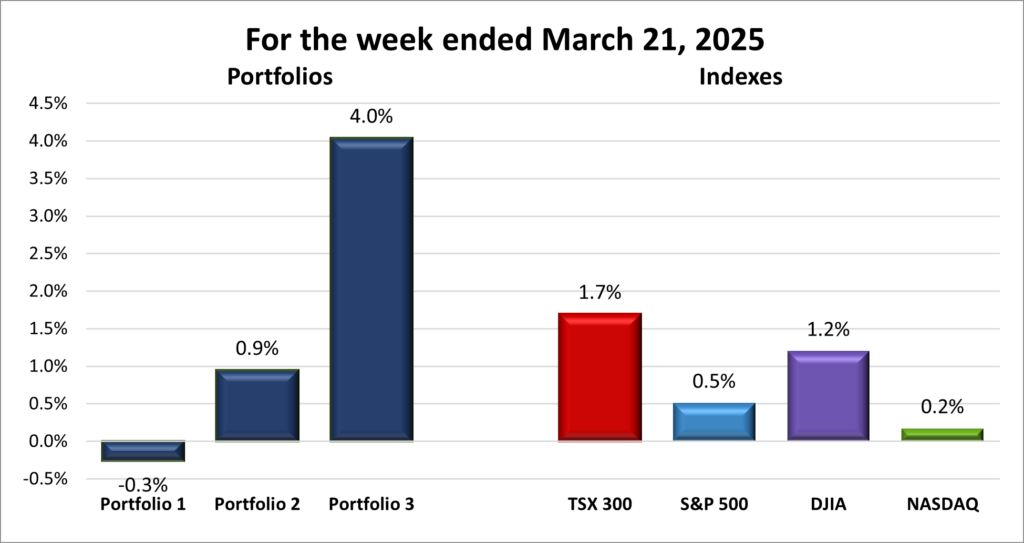

For the week, the TSX (SPTSX) rose 1.7%, the S&P 500 (SPX) increased 0.5%, the DJIA (INDU) advanced 1.2% and the Nasdaq (CCMP) edged higher by 0.2%.

| Index | Weekly Streak |

| TSX: | 1 – week winning streak |

| S&P: | 1 – week winning streak |

| DJIA: | 1 – week winning streak |

| Nasdaq: | 1 – week winning streak |

![]() After a choppy week of ups and downs, all four major indexes finally snapped their losing streaks, as you can see in the chart above. The Toronto Stock Exchange Composite Index (TSX) and Dow Jones Industrial Average (DJIA) ended two-week slides, while the S&P 500 Index (S&P) and Nasdaq Composite Index (Nasdaq) broke four-week streaks.

After a choppy week of ups and downs, all four major indexes finally snapped their losing streaks, as you can see in the chart above. The Toronto Stock Exchange Composite Index (TSX) and Dow Jones Industrial Average (DJIA) ended two-week slides, while the S&P 500 Index (S&P) and Nasdaq Composite Index (Nasdaq) broke four-week streaks.

The week kicked off with the US retail sales report, which, along with the previous week’s inflation data, pointed to a slight cooling in inflation. That reassured investors that the Fed might not need to take aggressive action on interest rates. However, the real market mover was the Fed’s latest rate decision.

The Fed faced a tough balancing act – juggling sticky inflation, slowing growth, and uncertainty over Trump’s trade policies. Despite the challenge, Fed Chair Jerome Powell struck an optimistic tone in his post meeting press conference, stating the Fed was holding the US benchmark rate at 4.5% and reaffirming expectations for two rate cuts later this year.

Markets initially rallied after Powell reassured investors that tariff-driven inflation would be ‘transitory’ and that recession risks remained low. Hopes for rates to drop to 4.0% by year-end fueled optimism. However, the relief rally was short-lived as concerns over stagflation risks quickly took centre stage, causing gains to fade.

Trade uncertainty added another layer of volatility, with concerns over looming reciprocal tariffs weighing on sentiment. US indexes seemed poised to extend their losing streaks, only to be saved by a last-minute comment from Trump, suggesting he had some ‘flexibility’ on the upcoming tariffs. This comment pushed the American indexes into the green for the day. What does ‘flexibility’ mean? We’ll find out soon enough.

In Canada, the TSX was boosted by rising oil prices, driven by new US sanctions on Iran, heightened tensions in the Middle East, and the ongoing Russia-Ukraine war. The positive sentiment from the Fed’s outlook also supported the market, though gains were capped by uncertainty over the tariffs set to take effect on April 2.

Going forward, the fate of the markets this year may depend on whether tariff-fueled inflation truly is transitory, as Powell suggests. If not, the US could find itself grappling with stagflation fears. In the meantime, the recent sell-off has pulled some high-flying stocks back down to fair value, or even into bargain territory, providing opportunities to become an owner of some of the world’s best companies.

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week losing streak |

| Portfolio 2: | 1 – week winning streak |

| Portfolio 3: | 1 – week winning streak |

![]() This week turned out better than expected, with two of the three portfolios finishing in the green, as you can see in the chart below, despite markets swinging up and down throughout the week. There weren’t any major standout gains or losses, just steady, solid performance across the board.

This week turned out better than expected, with two of the three portfolios finishing in the green, as you can see in the chart below, despite markets swinging up and down throughout the week. There weren’t any major standout gains or losses, just steady, solid performance across the board.

Portfolio 1 came close to breaking even, missing out by just 0.3%. On the bright side, 60% of the companies in the portfolio gained value over the week. However, Nvidia (NASD: NVDA), which makes up over 36% of the portfolio, slipped 4% for the week, ultimately dragging the portfolio into the red.

Portfolio 2 had a solid week, rising 0.8% as 77% of its holdings posted gains. The energy sector stocks in particular had a strong showing, lifting the portfolio higher.

Portfolio 3 stole the spotlight with a 4.0% gain – almost double the TSX’s weekly return, the top performing index. An impressive 95% of its holdings finished in the green, with Evolution AB (OTCM: EVVTY) being the only stock to drop.

Given how choppy the markets were, I was pleasantly surprised to see all three portfolios finish higher – even if one barely moved. 😊 But the real surprise? Portfolio 3’s near-perfect performance! That’ll be a tough act to beat, but I’d love to see one of them pull it off. 😊

Companies on the Radar

With market volatility still running high, I’ve been hesitant to jump into new investments. Instead, I’ve focused on adding to companies I already own—businesses I know well that have delivered strong performance or growing dividends since I first invested (even if my stake is microscopic! 😊). Many of these stocks have dipped due to market uncertainty surrounding tariffs, making now a good time to add to existing positions. Case in point: my recent addition to Canadian Natural Resources (TSE: CNQ) (see Portfolio Updates below).

With market volatility still running high, I’ve been hesitant to jump into new investments. Instead, I’ve focused on adding to companies I already own—businesses I know well that have delivered strong performance or growing dividends since I first invested (even if my stake is microscopic! 😊). Many of these stocks have dipped due to market uncertainty surrounding tariffs, making now a good time to add to existing positions. Case in point: my recent addition to Canadian Natural Resources (TSE: CNQ) (see Portfolio Updates below).

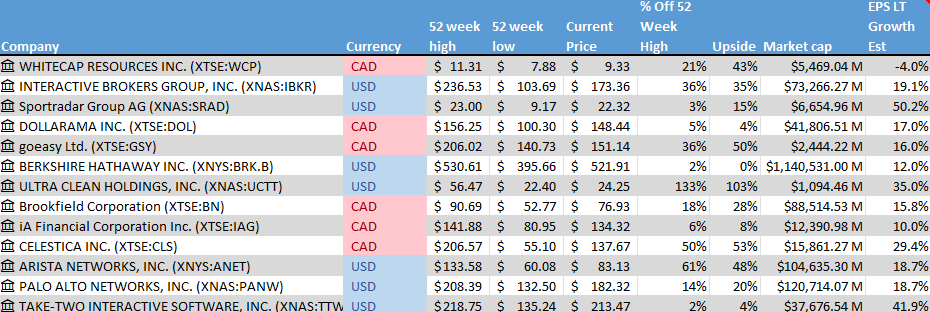

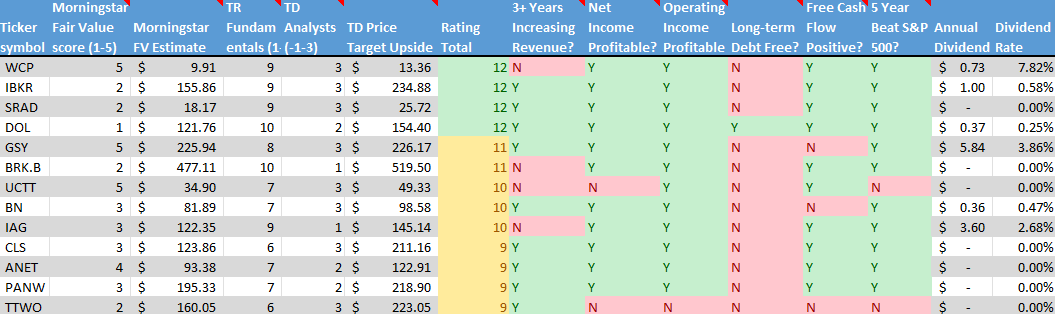

For this week’s ‘Companies on the Radar,’ I’ve added stocks from my existing portfolios that I’m considering increasing my stake in. That brings the list to 13 names: three holdovers from last week (with Axon Enterprise, Inc. (NASD: AXON) dropped), two new companies that recently caught my attention, and eight current holdings I’m eyeing for potential top-ups.

- Whitecap Resources (TSE: WCP): A medium-cap Canadian oil and gas company. The company offers an impressive monthly dividend yield of over 7% per month, which has grown steadily.

- Interactive Brokers (NASD: IBKR): A large-cap American online brokerage firm known for its advanced trading platform used by professionals and retail investors like us at all levels.

- Sportradar Group AG (NASD: SRAD): A mid-cap Swiss company specializing in sports data, content, and integrity services that support businesses in sports, media, and betting industries.

- Dollarama (TSE: DOL): A large cap Canadian company that operates a growing chain of discount stores across Canada and is expanding into South America.

- goeasy Ltd. (TSE: GSY): a mid cap Canadian company that provides non-prime leasing and lending services to consumers in Canada.

- Berkshire Hathaway (NYSE: BRK.B): The mega cap American conglomerate managed by Warren Buffet.

- Ultra Clean Holdings (NASD: UCTT): A small-cap American company specializing in critical components and ultra-high purity cleaning and analytical services in the semiconductor industry.

- Brookfield Corporation (TSE: BN): A large cap Canadian alternative asset manager and REIT/Real Estate Investment Manager.

- iA Financial Corporation (TSE: IAG): A large cap Canadian company that provides insurance products in Canada and the US.

- Celestica Inc. (TSE: CLS): a medium sized Canadian company that manufactures electronic products and provides supply chain services to companies around the world.

- Arista Networks ((NYSE: ANET): A large cap American company specializing in networking products for global enterprises.

- Palo Alto Networks (NASD: PANW): A large cap American company providing cybersecurity solutions to companies around the world.

- Take-Two Interactive Software (NASD: TTWO): A large cap American company that develops interactive entertainment for consumers around the globe.

As always, these are not buy recommendations – be sure to do your own research and make decisions that align with your personal financial goals!

The Radar Check was last updated March 21, 2025.

Portfolio Updates

Portfolio 2

Bought: Canadian Natural Resources

I first invested in Canadian Natural Resources in August 2022, drawn by its steadily growing dividend and strong position in the energy sector. Since then, the stock has gained 23%, and its dividend—which has been increasing for 25 years—has provided a reliable income stream. This week, I added to my position, locking in a solid 5.3% dividend yield and the potential for 17% earnings growth over the next five years. Not bad for a well-established energy company.

What I’ve come to appreciate about CNQ is its efficiency in turning a profit, even when energy markets face challenges. It is still one of Canada’s biggest and most dependable producers, consistently generating strong cash flow—which it often returns to investors.

With the stock pulling back slightly due to market turbulence caused by the uncertainty of looming tariffs, I saw an opportunity to buy at a discount. Given its history of steady performance, strong cash flow, and dependable, rising dividends, adding to my position felt like a smart move. 😊

Portfolio 3

Sold: Telus international (TSE: TIXT)

I first invested in TIXT back in February 2021, right as the post-COVID bull market was lifting almost every tech stock. At the time, I saw potential for it to become a major Canadian – if not international – tech player. But over time, it started to feel more like a glorified Managed Services Provider (MSP) rather than an industry leader. Things were fine until the 2022 bear market hit, and from there, it was a steady decline – even as broader markets rebounded in late 2022. Fast forward to the end of 2024, and the numbers weren’t looking great. Revenue was down, net income had declined for two straight years, and the company closed out the year with a net loss.

After two years of underperformance, I finally decided to cut my losses and reallocate the funds to better opportunities. Sometimes, it’s just better to move on.

Sold: Enghouse Systems (TSE: ENGH)

I first invested in Enghouse back in January 2020, aiming for long-term growth and steady dividend income. The company delivered strong growth in the first year, so I added to my position in early 2021 after the stock had climbed 20%. While that seemed like a solid move, the stock had already peaked in mid-2020 and was on a steady decline when I bought more (though at the time, I thought it was just a dip – it turned into a prolonged slide). It eventually stabilized around C$30 during the 2022 bear market but never truly rebounded.

Looking at the bigger picture, while the TSX and S&P have surged over the past five years, Enghouse has lagged, drifting lower instead of recovering. As the chart below shows, there’s a clear divergence between Enghouse and the TSX and S&P, which serve as strong benchmarks for the Canadian and US markets. Given that underperformance, I considered selling all my shares but ultimately decided to trim my position instead. Despite the weak stock performance, Enghouse has remained profitable, with revenue, net income, and cash flow all increasing over the last two years. Plus, the dividend still provides some income, and as a small-cap company, there’s always the potential for future growth.

By selling some shares, I’ve freed up cash for better opportunities while keeping a foot in the door in case Enghouse regains momentum. For now, I’ll hold onto a smaller position to collect dividends and see if the company can turn things around.

By selling some shares, I’ve freed up cash for better opportunities while keeping a foot in the door in case Enghouse regains momentum. For now, I’ll hold onto a smaller position to collect dividends and see if the company can turn things around.

That’s a wrap for this week—see you next time! Happy investing!