Economists and analysts have been bringing up the word ‘stagflation’ lately – and that’s not a good thing. It’s an economic scenario no one wants, where growth stalls while prices keep rising. The term might sound complicated but understanding it now can help you avoid surprises later. So this week, I thought I’d go over what stagflation is and explain it in a way that’s easy to understand.

What is Stagflation?

Imagine you’re driving in bumper-to-bumper traffic – moving painfully slow – but at the same time, your car’s engine is overheating. That’s basically stagflation in economic terms: the economy isn’t growing much (or at all), but prices keep rising. Normally, inflation happens when the economy is booming, and a slowdown helps cool things down. But stagflation flips the script, combining slow growth with rising costs – something that can leave consumers squeezed and businesses struggling.

How Stagflation Impacts Markets

Stagflation doesn’t hit every part of the market the same way. Some sectors feel the pressure, while others hold up better:

- Stocks: Companies face rising costs while demand weakens, which can hurt profits. Investors often shift towards defensive sectors like healthcare and consumer staples—industries that sell essentials people need no matter what.

- Bonds: Inflation erodes the value of bond payouts, and if central banks hike interest rates to fight inflation, bond prices can take another hit.

- Commodities: Gold and energy tend to attract investors during inflationary times since their prices often rise along with everything else.

What Can Investors Do?

If stagflation sticks around, investors may want to adjust their approach:

- Diversify across different asset classes to help balance risk.

- Focus on quality – companies with strong financials and pricing power (the ability to pass higher costs onto customers) tend to hold up better.

- Look at inflation-resistant assets like certain commodities or inflation-linked bonds.

- Stay informed – markets shift, and central bank policies can change the game quickly. A steady, long-term perspective usually beats reacting out of fear.

Lessons from the Past, Clues for the Present

The 1970s saw one of the worst stagflation periods, showing that there’s no one-size-fits-all solution. But history also reminds us that economies and markets adapt. While some sectors might struggle, innovation-driven areas – like technology or renewable energy – could still offer opportunities if companies find ways to outpace rising costs.

Stagflation isn’t just a buzzword – it’s a challenge that forces investors to think differently. It might seem like a daunting concept, but by understanding its components and preparing strategically, you’ll be better positioned to navigate turbulent times. Remember, even uncertain times can present new opportunities. 😊

With that in mind, let’s take a look at what’s been happening in the markets this week

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, …

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Bank of Canada minutes

The Bank of Canada released the minutes from its March 12 meeting this past week, offering insight into its decision to cut the policy interest rate by 0.25% to 2.75% – marking the seventh straight cut. Interestingly, the minutes suggest the central bank might have kept rates steady at 3% if not for the uncertainty surrounding US tariffs on Canadian goods.

Despite stronger-than-expected economic growth and inflation hovering near the 2% target, the threat of tariffs and heightened uncertainty had started to weigh on business and consumer confidence, leading to the rate cut. Policymakers also voiced concerns about inflationary pressures linked to trade disruptions and a weaker Canadian dollar, underscoring the tricky balancing act the BoC faces.

Gross Domestic Product (GDP)

After a surprise jump in annualized fourth-quarter growth, Canada’s economy continued its momentum into the new year. Statistics Canada reported that GDP rose 0.4% in January, beating expectations of a 0.3% increase and accelerating from December’s 0.2% gain.

The biggest boost came from goods-producing industries, which surged 1.1% – their strongest monthly gain in over three years. The ‘Mining, quarrying, and oil and gas extraction’ sector led the way with a 1.8% jump, while ‘Manufacturing’ rebounded with a 0.8% increase. Oil and gas extraction remained the economy’s biggest growth driver, expanding 2.6% in January.

On a year-over-year basis, GDP grew 2.4%, reflecting steady economic expansion, largely fueled by resource-heavy sectors. The ‘Mining, quarrying, and oil and gas extraction’ sector saw a notable 7.7% increase from a year ago.

However, the outlook isn’t all rosy. January’s growth may have been driven by a temporary export push to get ahead of tariffs and a short-term boost from the GST tax break that spurred spending. Preliminary February estimates suggest momentum stalled, with GDP flat for the month. Weakness in retail trade and real estate points to softening consumer spending and housing activity, offsetting gains elsewhere. While January’s data is encouraging, mixed signals from February highlight potential headwinds, from sectoral slowdowns to broader economic uncertainties. Trade tensions and looming tariffs could further pressure businesses by raising costs and complicating the growth outlook.

Canadian market volatility

Canada’s Volatility Index (VIXC) had a relatively calm week, starting at 16.07 before dipping into the 14.0 range, where it remained for most of the week, closing at 14.47. There was a brief dip below 12, driven by optimism that US tariffs might be scaled back, but that quickly faded. The real excitement came towards the end of the week, when the index briefly spiked to 17.92 after news of higher-than-expected US inflation data, before settling back into the 14 range.

For those unfamiliar with the VIXC (traded as VIXI on the TSX), think of it as the market’s anxiety gauge. A reading below 10 signals strong investor confidence, while a range between 10 and 20 is business as usual. When it crosses 20, however, it’s a sign that uncertainty is starting to take hold.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Consumer Confidence Index (CCI)

Consumer confidence took another hit in March, with the Conference Board’s index dropping to 92.9 from 98.3 in February – its fourth straight decline. This follows February’s steep drop, which was the sharpest in over three years. Analysts had expected a reading of 94, so this miss adds to concerns about the economic outlook.

The Present Situation Index, which tracks current business and job conditions, slipped to 134.5, but the real worry is the Expectations Index. It tumbled 9.6 points to 65.2 – well below the 80 threshold that often signals a recession, and its lowest level in 12 years.

This decline reflects mounting concerns over the economy and persistent inflation, which remains above the Fed’s 2% target. With consumer confidence fading, consumer spending – which drives 70% of the American economy – could weaken, putting pressure on growth. For us investors, that means more market uncertainty. Sectors reliant on discretionary spending, like retail and travel, may struggle, while defensive industries like utilities could hold up better.

Gross Domestic Product (GDP)

The Bureau of Economic Analysis (BEA) released its third and final report on US GDP, confirming the economy grew 2.4% in the fourth quarter – slightly above both the previous estimate and analysts’ expectations of 2.3%. However, this marks a notable slowdown from the 3.1% growth seen in Q3.

The economy was largely propped up by strong consumer and government spending, though this was partly offset by a drop in investment. A decline in imports, which subtract from GDP, also provided a small boost.

Overall, the report paints a mixed picture – steady consumer spending kept growth afloat, but weaker investment and trade pressures hint at growing challenges. For the full year, the US economy expanded 2.8%, slightly below 2023’s 2.9% pace. Looking ahead to 2025, uncertainty looms. With President Trump’s tariffs set to impact nearly all imported goods, inflation could rise, investment may slow, and businesses could face a tougher climate. Many estimates put first-quarter growth below 1.5%, with a real risk of contraction.

Personal Consumption Expenditures (PCE)

The BEA’s latest inflation report confirmed that price pressures remained stubborn in February. The PCE price index rose 0.3% month-over-month and 2.5% year-over-year, matching January’s increases and meeting expectations.

However, the bigger concern is core PCE—the Fed’s preferred inflation gauge, which strips out the volatile food and energy components. It came in hotter than expected, rising 0.4% for the month (above the 0.3% forecast) and 2.8% year-over-year, exceeding estimates of 2.7%.

This suggests inflation isn’t easing as quickly as hoped, particularly in core categories less affected by short-term volatility. With trade tensions rising and new tariffs looming, inflation risks could intensify, making it harder for the Fed to bring inflation down to its 2% target and start cutting interest rates to support the economy.

Consumer Sentiment Index (CSI)

The University of Michigan’s final Consumer Sentiment Index reading for March came in at 57.0, lower than both the initial estimate of 57.9 and analysts’ expectations. That’s an 11.9% drop from February’s 64.7 and a steep 28.2% decline from a year ago, marking the third straight month of falling sentiment and the lowest reading since November 2022.

Looking at the two major subcomponents, the Current Economic Conditions Index, which measures how consumers feel about their current finances situation, dipped to 63.8 from 65.7 – a 2.9% decline and 22.7% lower than last March. The bigger concern is the Index of Consumer Expectations, which gauges optimism about the next six months. It dropped sharply to 52.6, down 17.8% from last month and 32.0% year-over-year.

This sharp decline in sentiment signals growing economic uncertainty. Consumers are increasingly worried about rising unemployment and inflation, two key factors that could weigh on spending – a major driver of economic growth. Inflation expectations for the next year have surged to 5%, up from 4.3% last month, suggesting that households are bracing for higher costs, which could further strain budgets. At the same time, two-thirds of consumers – across all demographics – now expect unemployment to rise in the coming year, the highest level of concern since 2009.

With confidence slipping, policymakers face a tough challenge: balancing inflation control while supporting economic growth. If consumer pessimism leads to weaker spending, it could slow down the economy even further. The road ahead looks uncertain, and how these concerns play out in the job market and inflation trends will be critical in shaping the next moves by the Fed.

American market volatility

The CBOE Volatility Index (VIX), often called the market’s ‘fear gauge,’ kicked off the week at a moderately elevated 19.13 before steadily trending lower and plateauing in the 17.50 range by midweek. However, the fear gauge started to rise again towards the end of the week, spurred on by tariff concerns, higher inflation data, and plummeting consumer sentiment. The VIX closed the week at 21.65 – signaling that heightened market uncertainty led to increased investor anxiety and volatility in the markets.

For those unfamiliar with the VIX, think of it as a stress meter for stocks. A reading below 12 signals calm conditions, while 12 to 20 reflects typical market fluctuations. Above 20, uncertainty is creeping in, and anything over 30 suggests markets are in turmoil.

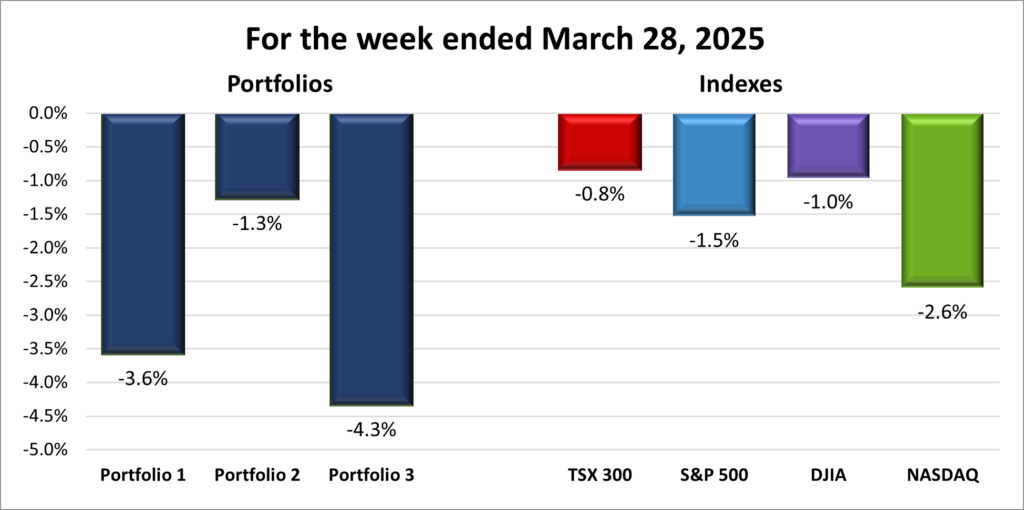

Weekly Market and Portfolio Review

For the week, the TSX (SPTSX) fell 0.8%, the S&P 500 (SPX) slipped 1.5%, the DJIA (INDU) declined 1.0% and the Nasdaq (CCMP) dropped 2.6%.

| Index | Weekly Streak |

| TSX: | 1 – week losing streak |

| S&P: | 1 – week losing streak |

| DJIA: | 1 – week losing streak |

| Nasdaq: | 1 – week losing streak |

![]() The markets had a bumpy ride this week. All four major indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – climbed steadily to start the week, only to plunge sharply by the end, as shown in the chart above. Early on, President Trump hinted at giving “a lot of countries breaks” on upcoming tariffs, suggesting a more targeted approach than initially expected. Investors cheered, sending markets higher. But by midweek, Trump toughened his stance, saying he didn’t want “too many exceptions.” He also accelerated the timeline for copper tariffs, slapped a 25% tax on all auto imports, and threatened further action against Canada and the EU if they retaliated together.

The markets had a bumpy ride this week. All four major indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – climbed steadily to start the week, only to plunge sharply by the end, as shown in the chart above. Early on, President Trump hinted at giving “a lot of countries breaks” on upcoming tariffs, suggesting a more targeted approach than initially expected. Investors cheered, sending markets higher. But by midweek, Trump toughened his stance, saying he didn’t want “too many exceptions.” He also accelerated the timeline for copper tariffs, slapped a 25% tax on all auto imports, and threatened further action against Canada and the EU if they retaliated together.

On the economic front, the final fourth quarter GDP report confirmed a slowing economy, while the latest inflation data showed core inflation rising both monthly and yearly. Investors are increasingly worried about the US economy slipping into recession – or worse, stagflation – especially if tariffs exacerbate stubborn inflation and weak growth.

Trade tensions have fueled a wave of uncertainty, sending consumer sentiment and confidence sharply lower, as reflected in this past week’s CSI and CCI reports. Inflation and job security fears are weighing on consumers, who may cut back on spending, putting pressure on businesses across multiple sectors. Rising inflation expectations are already straining household budgets, while concerns over rising unemployment add to the unease. Even Walmart (NYSE: WMT) – which had a strong 2024 – is warning of lower profits ahead due to tariff-related cost pressures. This growing pessimism could ripple through the economy, leading to weaker investment and slower growth. And if the US economy struggles, Canada won’t be far behind.

Just last week, Fed Chair Jerome Powell reassured markets that the US economy remained strong and the labour market stable. But this week’s data challenges that view, forcing investors to reassess the risks ahead.

In Canada, inflation expectations are rising sharply as consumers brace for trade wars that could push prices higher. If inflation gains traction while the economy weakens, the BoC could find itself in a tough spot – potentially needing to raise rates at a time when the economy might require lower ones instead.

This was not a good week by any measure. Next week isn’t shaping up to be much better, with US tariffs set to take effect and retaliatory tariffs likely to follow. If nothing else, it should be a volatile ride. Or, if you’re a glass-half-full kind of person, a week full of buying opportunities. 😊

| Portfolio | Weekly Streak |

| Portfolio 1: | 2 – week losing streak |

| Portfolio 2: | 1 – week losing streak |

| Portfolio 3: | 1 – week losing streak |

![]() After last week’s surprising gains, the momentum fizzled out, with all three portfolios ending in the red. ☹ One bright spot? President Trump’s 25% tariff on all auto imports sent shares of North American automakers and parts manufacturers tumbling. Selling my General Motors (NYSE: GM) shares earlier over tariff concerns is looking like one of my better decisions. Unfortunately, that was about the only good news this week.

After last week’s surprising gains, the momentum fizzled out, with all three portfolios ending in the red. ☹ One bright spot? President Trump’s 25% tariff on all auto imports sent shares of North American automakers and parts manufacturers tumbling. Selling my General Motors (NYSE: GM) shares earlier over tariff concerns is looking like one of my better decisions. Unfortunately, that was about the only good news this week.

Portfolio 1 extended its losing streak to two weeks, dropping 1.4% as only 31% of its holdings managed a gain. The sell-off in heavyweight tech stocks did the real damage, but also weighing on the portfolio were steep losses from Navitas Semiconductor (NASD: NVTS), down 21%; Celestica (TSE: CLS), down 16%; Magnite (NASD: MGNI), down 14%; Lattice Semiconductor (NASD: LSCC), down 11%; and Shopify (TSE: SHOP), down 10%.

Portfolio 2 was holding onto gains heading into Friday, but the market plunge dragged it down, finishing the week with a 1.3% loss. Still, it fared the best among the three, with 40% of its holdings managing a gain – an achievement in this brutal week.

Portfolio 3 had the roughest week, with only 14% of its holdings finishing in positive territory. On top of that, it suffered some hefty declines, with Vertiv Holdings (NYSE: VRT) down 18%, Magnite down 14%, and Shopify down 10%.

Once again, there’s little to say as the markets await the implementation of tariffs and retalitory tariffs. It was a tough week all around. Next week will see the start of a new month. I don’t have high expectations in this looming tariff environment, but hopefully the rest of April will be better than March with a return to rising markets.

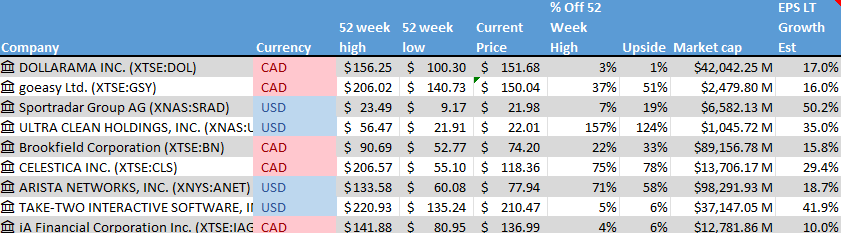

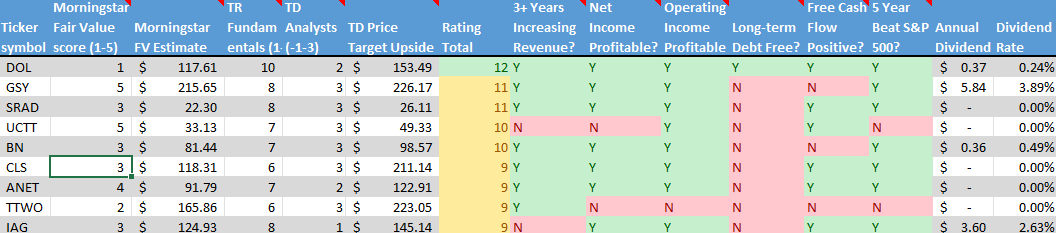

Companies on the Radar

Last week, my radar list had 13 companies—a mix of carryovers, new names, and existing holdings. That’s way too many, so most of the week was spent trimming it down. I’ve since removed four companies – Whitecap Resources (TSE: WCP), Interactive Brokers (NASD: IBKR), Berkshire Hathaway (NYSE: BRK.B), and Palo Alto Networks (NASD: PANW). Even with nine names left, that’s still more than I’d like, and I’m aiming to narrow it down to five or fewer next week.

Last week, my radar list had 13 companies—a mix of carryovers, new names, and existing holdings. That’s way too many, so most of the week was spent trimming it down. I’ve since removed four companies – Whitecap Resources (TSE: WCP), Interactive Brokers (NASD: IBKR), Berkshire Hathaway (NYSE: BRK.B), and Palo Alto Networks (NASD: PANW). Even with nine names left, that’s still more than I’d like, and I’m aiming to narrow it down to five or fewer next week.

With more tariffs set to kick in on April 2, volatility could pick up as the day approaches. If the market dips, I’ll be watching for opportunities to buy quality companies at discount prices.

- Sportradar Group AG (NASD: SRAD): A mid-cap Swiss company specializing in sports data, content, and integrity services that support businesses in sports, media, and betting industries.

- Dollarama (TSE: DOL): A large cap Canadian company that operates a growing chain of discount stores across Canada and is expanding into South America.

- goeasy Ltd. (TSE: GSY): A mid cap Canadian company that provides non-prime leasing and lending services to consumers in Canada.

- Ultra Clean Holdings (NASD: UCTT): A small-cap American company specializing in critical components and ultra-high purity cleaning and analytical services in the semiconductor industry.

- Brookfield Corporation (TSE: BN): A large cap Canadian alternative asset manager and REIT/Real Estate Investment Manager.

- iA Financial Corporation (TSE: IAG): A large cap Canadian company that provides insurance products in Canada and the US.

- Celestica Inc. (TSE: CLS): A medium sized Canadian company that manufactures electronic products and provides supply chain services to companies around the world.

- Arista Networks ((NYSE: ANET): A large cap American company specializing in networking products for global enterprises.

- Take-Two Interactive Software (NASD: TTWO): A large cap American company that develops interactive entertainment for consumers around the globe.

As always, these are not buy recommendations – be sure to do your own research and make decisions that align with your personal financial goals!

The Radar Check was last updated March 28, 2025.

Portfolio Update

Portfolio 3

Sold: Lithium Argentina (TSE: LAR)

I originally bought Lithium Americas (TSE: LAC) in the summer of 2023, back when Lithium Argentina was still part of LAC. At the time, surging electric vehicle (EV) demand made lithium—a key ingredient in EV batteries—seem like a solid investment. Then came the split: LAC became a Nevada-focused miner, while LAR took on operations in Argentina (as the name suggests! 😊).

Since then, it’s been a tough ride. LAR’s share price has steadily declined, down nearly 70%, and demand for EVs has cooled. This year alone, the stock is down 11.2% year-to-date, currently trading around C$3.25—far closer to its 52-week low of C$2.86 than its highs.

The broader lithium sector hasn’t helped. Demand is still unpredictable, competition is fierce, and geopolitical risks—especially in Argentina—add more uncertainty. On top of that, the latest wave of US tariffs could disrupt the industry further. Lithium prices remain volatile, and investor sentiment on the sector has been all over the place.

Lastly, LAR recently restructured and relocated to Switzerland. While this could pay off long-term, it introduces even more short-term uncertainty—something investors tend to avoid, especially with trade tensions heating up.

Given all this, I decided to sell my shares and move on to better opportunities. It’s never easy to walk away from an investment, but sometimes, stepping aside is the smartest move.

That’s a wrap for this week—see you next time! Happy investing!