I am very happy with the nearly 19% gain in Microsoft’s (NASD: MSFT) share price since the start of the year. Normally, that would be a fantastic return for six months. But compared to the performance of another tech giant – Nvidia (NASD: NVDA) – it is modest. Nvidia is experiencing extraordinary times, thanks to its dominant position in the booming artificial intelligence (AI) industry. This year alone, Nvidia’s stock has skyrocketed almost 150%, driven by insatiable demand for its high-end processors. Not a bad problem to have!

Nvidia has seamlessly transitioned from leading the charge in crypto mining and cloud computing data centers to becoming the go-to provider for AI processors. Their chips are making computers faster, more powerful, and more efficient, forming the backbone of modern technology infrastructure. Any company aiming to make a mark in AI relies on Nvidia chips. As Nvidia’s Annual Review highlights, “the Nvidia ecosystem spans nearly 5 million developers and 40,000 companies,” with “more than 1,600 generative AI companies building on Nvidia.”

The AI boom has ignited a sustained chip-buying frenzy, propelling Nvidia’s revenues and stock price to new heights. This surge has elevated Nvidia to one of the world’s most valuable companies. Just two years ago, it was the tenth most valuable, and five years ago, it was not even in the top 20.

Nvidia’s influence is so significant that if its share price stumbles, the market feels the impact. Many stocks that have benefited from Nvidia’s rise could also fall. Since these companies have driven the AI rally, a downturn in Nvidia could drag the market down. Hopefully, other sectors will step up as the tech sector, especially Nvidia and other AI-related companies, return to more sustainable levels and growth rates.

After a recent three-day losing streak that saw Nvidia’s share price drop 12.9% (technically a ‘correction’), wiping out roughly US$ 430 billion in market value, Nvidia bounced back with a 6.8% gain on Wednesday alone.

The beauty of investing is that one winner like Nvidia can supercharge your portfolio, as it has with mine. While Nvidia’s performance has been exceptional, it is important to remember that past performance is no guarantee of future results.

Reflecting on Nvidia’s remarkable ascent to the top of the world’s most valuable companies, its pivotal role in the AI industry, and its market-moving influence, it is evident how powerful individual stocks can be. Now, let’s shift our focus and review the key events and trends that shaped the markets this past week…

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, What I learned, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Consumer price Index (CPI)

Statistics Canada’s CPI data for May threw a curveball at analysts and disappointed anyone hoping for lower interest rates. Inflation, as measured by the CPI, unexpectedly climbed to 0.6% in May, slightly higher than the 0.5% gain reported in April. Year-over-year, inflation rose to 2.9% from 2.7% in April, defying analysts’ expectations of a 0.3% monthly gain and a 2.6% annual increase.

The monthly breakdown revealed that ‘Recreation, education, and reading’ saw the biggest jump, up 2.3%, while the ‘Gasoline’ sub-sector experienced the largest drop, down 1.3%. Annually, ‘Shelter’ costs, encompassing mortgages and rent, were the biggest contributors to the inflation spike, rising 6.4%. On the flip side, ‘Clothing and footwear’ saw the steepest decline, down 3.0%.

Core CPI, which strips out food and energy prices, also came in higher than expected, mirroring the headline, or all items, CPI data with increases of 0.6% monthly and 2.9% annually. When excluding food and energy, the sectors driving core inflation remained largely the same as the headline CPI, except ‘Clothing and footwear,’ which stayed flat and was the only sector not to see monthly price increases.

This latest data is not good news for consumers hoping for price relief and for those hoping the BoC will cut rates at their July meeting. With another CPI report due before the BoC convenes on July 24, all eyes will be on whether the May figures were an anomaly or the start of a troubling trend.

Gross Domestic Product (GDP)

Statistics Canada’s GDP data for April revealed Canada’s economy bounced back with a 0.3% expansion, following a month of stagnation in March. Both goods and services industries contributed to the growth, each increasing by 0.3%.

Within the Goods-producing sector, ‘Mining, quarrying, and oil and gas extraction’ led the growth at 1.8%, while ‘Construction’ dipped slightly by 0.4%. The Services-producing sector was led by ‘Wholesale trade’ with a 2.0% increase, while ‘Management of companies and enterprises’ saw the largest decline of 1.9%.

On an annual basis, GDP rose 1.1%, with a strong showing from the Services-producing industries (up 1.8%) that outweighed a 1.1% decline in Goods-producing industries. Within Goods-producing, ‘Mining, quarrying, and oil and gas extraction’ again led the way with a 4.9% gain, offsetting losses in all other subsectors, particularly ‘Utilities’ which dropped 3.3%. In Services-producing industries, ‘Wholesale trade’ continued its strong performance with a 4.0% annual increase, while ‘Management of companies and enterprises’ experienced a steep decline of 31.6%.

The positive news is that the economy resumed growth after March’s pause. The gains were broad-based, with 15 out of 20 sectors expanding in April. This indicates a healthier economic picture when growth is driven by multiple sectors rather than being reliant on a few. Additionally, the advanced estimate for May shows a further 0.1% expansion, suggesting continued economic momentum.

Canadian market volatility

Canada’s Volatility Index, the VIXC, tracked by the VIXI on the TSX, plummeted by 27% this past week, falling from 11.31 to 8.15. This sharp decline likely signals a more optimistic outlook among investors.

Improved economic growth in Canada and signs of falling inflation in both Canada and the US seem to be key contributors. The lower inflation data has investors thinking about potential rate cuts in Canada and the start of rate cuts in the US.

The VIXC measures expected market volatility, with lower values indicating less uncertainty and a calmer investor mood.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Personal Consumption Expenditures (PCE)

The latest PCE price index showed a pause in price increases for May. The headline, or all items, PCE index remained flat after rising 0.3% in April, marking the first time in six months that prices have not risen. Year-over-year, inflation as measured by PCE, remained steady at 2.6%, meeting analysts’ expectations.

The Fed’s favourite measure of inflation, core PCE, which excludes volatile food and energy prices, also showed a slowdown. The core PCE price index grew at a rate of 0.1% in May, down from 0.3% in April. On an annual basis, core PCE inflation dipped to 2.6% from 2.8% in April. Both the monthly and annual core PCE figures were in line with analyst forecasts.

The recent downward trend in inflation, following a spike in the first quarter, has raised optimism that the Fed might be able to achieve a “soft landing” where inflation eases towards its 2% target without triggering a recession. This data paves the way for the Fed to consider potential rate cuts in the future. Investors are hopeful that a rate reduction could occur as early as the Fed’s meeting on September 4th, but the ultimate decision will depend on how upcoming economic data unfolds.

Gross Domestic Product (GDP)

The Commerce Department’s Bureau of Economic Analysis released its third estimate for the first quarter of 2024, revealing a 1.4% increase in GDP, up slightly from the second estimate of 1.3%. This is a significant drop from the 3.4% surge in the fourth quarter of 2023 but slightly higher than the 1.3% forecast by analysts.

Consumer spending, housing construction and renovation activity, increased business infrastructure investment, and higher spending by state and local governments were the key drivers of GDP growth. However, lower business investment in inventories and a rise in imported goods and services, which represent an outflow of money, weighed on the overall expansion.

Compared to the previous quarter, the pace of consumer spending, exports, and government spending at all levels slowed down. This slowdown was partially offset by a notable increase in housing investment and higher import levels.

Despite strong contributions from consumer spending and investment, the slowdown compared to the previous quarter signals potential challenges ahead. The increase in imports and the decrease in business inventory investment raise concerns about reduced future production and increased capital outflow. In other words, the data indicates a potential slowdown in economic growth, which could lead the Fed to lower interest rates sooner rather than later.

American market volatility

The CBOE Volatility Index (VIX), often called the market’s “fear gauge,” dropped to 12.44 this week from 13.20 last week. This dip likely stems from recent economic data showing a slowdown in inflation and a cooling economy, opening the door for interest rate cuts some time this year, which seems to be calming investor nerves.

At 12.44, the VIX is well below the 20 mark that typically signals higher market volatility. This suggests that investors are feeling more confident about the future direction of the stock market and are currently less worried about near-term market fluctuations.

Consumer Sentiment Index (CSI)

The University of Michigan’s CSI, a key indicator of consumer confidence in the US economy, came in at a final reading of 68.2 for June. This represents a slight decline of 1.3% from May’s reading but remains higher than both the June initial reading of 65.6 and analysts’ expectations of 67.6.

Despite the slight drop, the current reading is still 6.2% higher than June 2023 and a significant 36% above the low point of June 2022. This suggests that consumers are cautiously optimistic about the future. While they believe inflation will continue to moderate, they remain concerned about the impact of high prices and stagnant wage growth on their purchasing power.

Consumer Confidence Index (CCI)

The Conference Board revealed that the CCI for June stood at 100.4, slightly down from the revised 101.3 in May. Analysts had predicted the CCI would dip to 100, so the result was pretty much on target. Although consumer confidence dipped a bit in June, it has remained within a tight range for the past two years.

The Present Situation Index, which gauges how consumers feel about the current business and labour market conditions, climbed to 141.5 from May’s 140.8. This uptick suggests that people are feeling a bit better about their immediate surroundings. However, the Expectations Index, which measures consumers’ short-term outlook on income, business, and labour market conditions, told a different story. It fell to 73.0 in June, down from 74.9 in May, marking the fifth consecutive month it has been below the critical 80 mark—a signal that often hints at a looming recession.

Overall, the combination of the two sub-indexes suggests consumers are feeling slightly better about their present situation, thanks to a robust labour market. But there is a catch: the cooling labour market is dampening expectations for the future.

The CCI is a key measure of current business conditions and potential developments in the months ahead. An overall CCI score above 100 indicates consumer optimism, while a score below 100 suggests pessimism. The Expectations Index is particularly crucial, as a reading below 80 can be a red flag for an economic slowdown.

What I learned

- The European Commission (EC), the European Union’s (EU) antitrust regulator, has levied charges against Apple (NASD: AAPL) concerning its App Store practices. The charges allege violations of the recently enacted Digital Markets Act (DMA).

The EC’s charges focus on Apple’s App Store practices, specifically the 15%-30% commission on purchased apps and restrictions on developer communication about alternative purchasing options. Apple does not allow developers to tell users they can purchase the same subscription for less by using their computer and going to the developer’s website.

If the EC finds Apple in breach of the DMA, the company could face a significant financial penalty. The DMA stipulates fines of up to 10% of a company’s global annual revenue for a first-time offense. Given Apple’s 2023 revenue of $383 billion, a potential fine of $38.3 billion could have a substantial impact on their financial performance.

This case holds significant weight as the first major enforcement action under the new DMA. The outcome will likely establish a crucial precedent for how large technology companies must comply with the act’s regulations. Undoubtedly, other major tech players will be closely monitoring this case, with potential implications for their own practices. - This past week, I encountered the term ‘The Three Horsemen of AI’ to describe three semiconductor companies for the first time. Leading the charge is, of course, Nvidia. Joining Nvidia in this powerhouse trio are Broadcom (NASD: AVGO) and Micron Technologies (NASD: MU). Since the start of 2024, Broadcom and Micron have surged 61% and 80%, respectively. While these impressive gains pale in comparison to Nvidia’s astonishing 173% rise, I would still be thrilled with a 61% gain in just six months! 😊

Weekly Market Review

Monday: the last week of June got off to mixed start with the Toronto Stock Exchange Composite Index (TSX) and the Dow Jones Industrial Average (DJIA) ending higher, while the S&P 500 Index (S&P), and the Nasdaq Composite Index (Nasdaq) ended lower. A slumping Nvidia continues to weigh on the S&P and Nasdaq as investors rotate into other more attractive sectors. The price of oil improved as increased demand is expected during the summer months, coinciding with ongoing supply uncertainty.

In Canada, the TSX benefitted from rising commodity prices and from investors rotating into resource companies. In trading, Energy was the big winner, while Technology was the only sector to end lower.

In the US, the DJIA reached its highest level in a month as investors took some profits after a bull run in AI stocks and move into other sectors that are likely to benefit from a much hoped for interest rate cut. It was broad rally in trading that saw Energy advance the most, while Technology and Consumer Cyclicals were the only sectors to decline.

Tuesday: another mixed day for the indexes, with all four reversing their Monday performance. The S&P and Nasdaq were higher after Nvidia rebounded from losses in the last three sessions. The TSX and DJIA ended lower. Oil prices dropped after a slow start to the summer driving season, leading to concerns about demand for fuel.

In Canada, higher than expected inflation data has investors worried about another rate cut in July. In trading, Technology was the big gainer for the day, while Consumer Cyclicals dropped the most.

In the USA, semiconductors and heavyweight technology companies had a big day, propelling the Nasdaq and S&P higher. The DJIA was weighed down by member Home Depot (NYSE: HD) which fell 3.6% today and has fallen three straight days after announcing it had acquired private roofing products manufacturer and distributor SRS Distribution. In trading, Technology was the only sector to advance, while Basic Materials (miners and fertilizer manufacturers) had the farthest fall.

Wednesday: the markets once again got off to a shaky start, but the indexes were able to crawl above the breakeven point by the end of the day. It has been a while since all four indexes ended higher on the same day. As investors await the latest US inflation data, a Fed official commented that she believes the current US interest rate can afford to remain at 5.5% for a while. Oil prices fell after an unexpected increase in US gas inventories.

In Canada, rising commodity prices helped lift the TSX into the green. In trading, Basic Materials was the big winner, while Telecommunications Services was the biggest loser.

In the US, the heavyweight technology companies helped drag all three indexes into positive territory. In trading, Consumer Cyclicals, Technology and Basic Materials were the only sectors to end higher, Energy suffered the biggest loss.

Thursday: another choppy day in the markets that saw all four indexes edge higher in anticipation of tomorrow’s US inflation report. The price of oil rose on concerns of supply disruptions.

In Canada, it was a day of broad-based gains on the TSX, led by the Technology sector. The Telecommunications Services sector was the only sector not to advance.

In the US, the latest GDP data indicated the economy grew more than originally thought in the first quarter, although considerably slower than in the previous quarter. In trading, Consumer Cyclicals rose the farthest, while Consumer Staples suffered the biggest drop.

Friday: the last day of the week, month, second quarter and first half ended with all four indexes in the red. Investors took some money off the table as the first half of 2024 came to an end. Oil prices fell on lower demand for crude oil.

In Canada, the TSX fell on lower energy and commodity prices. In trading, Consumer Cyclicals was the only sector to end higher, while Healthcare had the biggest decline.

In the US, the rate of inflation remained unchanged in May fueling investor optimism that the Fed could start lowering interest rates as soon as September. This optimism sent the S&P and Nasdaq to record highs before retreating in the afternoon as fund managers rebalanced their portfolios for the start of the third quarter. Also impacting the markets was the regular reconstitution of the Russell 1000, an index that tracks the performance of the 1,000 largest companies by market capitalization in the US. In trading on Wall Street, Financials gained the most while Utilities had the biggest fall.

Weekly Market and Portfolio Review

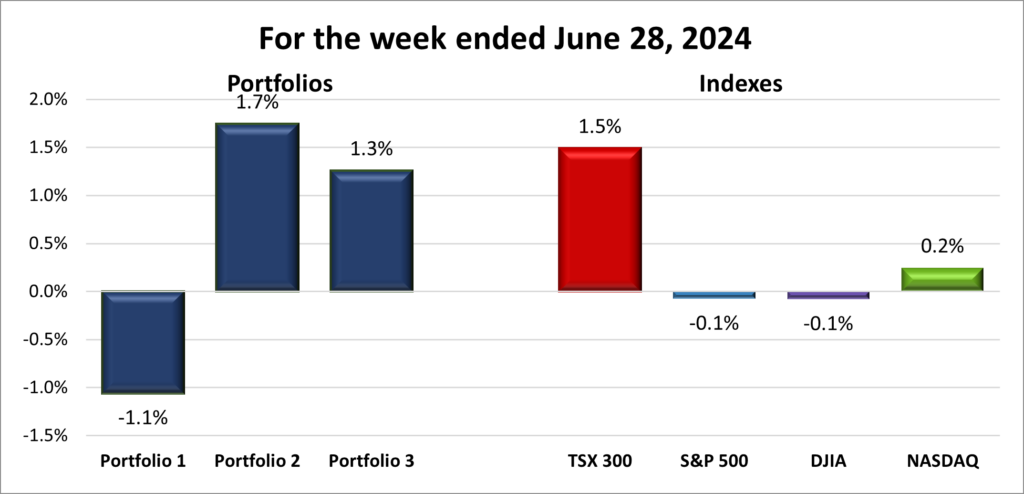

For the week, the TSX (SPTSX) rose 1.5%, the S&P 500 (SPX) lost 0.1%, the DJIA (INDU) slid 0.1% and the Nasdaq (CCMP) gained 0.2%.

| Index | Weekly Streak |

| TSX: | 1 – week winning streak |

| S&P: | 1 – week losing streak |

| DJIA: | 1 – week losing streak |

| Nasdaq: | 4 – week winning streak |

![]()

![]() This week saw a mixed performance across the indexes. The TSX and Nasdaq ended higher, while the S&P and DJIA finished lower, as you can see in the chart above. After an early week divergence due to a decline in Nvidia’s share price, all four indexes gained ground but ultimately the S&P and DJIA were unable to remain in positive territory as investors digested the latest US inflation news.

This week saw a mixed performance across the indexes. The TSX and Nasdaq ended higher, while the S&P and DJIA finished lower, as you can see in the chart above. After an early week divergence due to a decline in Nvidia’s share price, all four indexes gained ground but ultimately the S&P and DJIA were unable to remain in positive territory as investors digested the latest US inflation news.

Economic data in the US played a key role. Inflation continued its downward trend, helped by the Fed holding interest rates steady. However, higher rates are also contributing to a slower economy, a necessary consequence in the fight against inflation. The Technology sector, particularly AI stocks, continued its impressive performance, initially driving the S&P 500 and Nasdaq higher before a late-week pullback.

In Canada, rising commodity prices bolstered the Basic Materials sector, while expectations of lower interest rates buoyed the Financials sector. Together, these two sectors, which comprise approximately 55% of the TSX’s weighting, significantly contributed to the Canadian market’s outperformance. Additionally, positive sentiment from the US further boosted the TSX, leading to the week’s strongest performance among the major indexes.

Overall, it was not the strongest week to end the month, second quarter and first half of the year. Perhaps if fund managers had not been reconstituting their portfolios to match the latest changes to the Russell 1000 index, the week would have ended on an upward note. Hopefully, next week shows a return to upward momentum and the tech rally spreads to other sectors for a more sustainable bull run. 😊

| Portfolio | Weekly Streak |

| Portfolio 1: | 2 – week losing streak |

| Portfolio 2: | 1 – week winning streak |

| Portfolio 3: | 1 – week winning streak |

![]()

![]() As shown in the chart below, it was a mixed week for the Portfolios with two out of three recording a weekly gain, despite the overall lacklustre performance of the overall market.

As shown in the chart below, it was a mixed week for the Portfolios with two out of three recording a weekly gain, despite the overall lacklustre performance of the overall market.

Portfolio 1: This portfolio presents an interesting case where the majority of companies posted weekly gains but the portfolio still lost value. Despite gains from key holdings, this portfolio surprisingly dropped in value by 1.8% this past week. Despite having 60% of its companies advance, including a 29% jump by Rivian (NASD: RIVN), a 16% rise by Hammond Power Supply (TSE: HPS.A), a solid 10% gain by Carnival Cruise Lines (NYSE: CCL), and a decent week from its heavyweight technology companies, it still dropped in value. The significant dollar amount of losses from the remaining 40% of the companies in the portfolio must have outweighed the dollar amount of the gains.

Portfolio 2: This portfolio had a good week, bouncing back into the win column after a losing streak. Over half of the companies posted weekly gains, with notable performances by Hammond Power Supply (+16%) and MongoDB (NASD: MDB) with a 10% gain.

Portfolio 3: Following closely behind Portfolio 2, Portfolio 3, saw the majority of its companies post weekly gains. There were no significant gainers or losers, but the overall performance was positive.

Overall, it was a decent week with two portfolios posting gains, despite a soft week in the markets. Hopefully, next week all three portfolios post weekly gains to get the second half of the year off to a good start.

Monthly Market and Portfolio Review

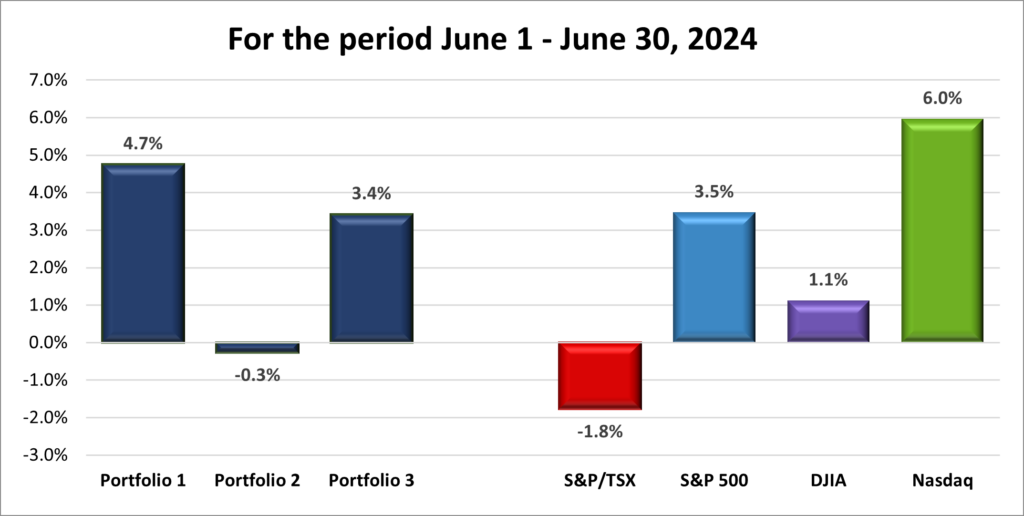

For the week, the TSX (SPTSX) shed 1.8%, the S&P 500 (SPX) gained 3.5%, the DJIA (INDU) rose 1.1% and the Nasdaq (CCMP) added 6.0%.

![]() June 2024 brought a wave of cautious optimism to North American stock markets. All three major American indexes advanced, with the Nasdaq leading the pack with a stellar 6% monthly gain, followed by the S&P 500 at 3.5%, and the DJIA up 1.1%, as shown in the chart above. The TSX, however, ended the month slightly lower despite showing signs of upward momentum towards the month’s end.

June 2024 brought a wave of cautious optimism to North American stock markets. All three major American indexes advanced, with the Nasdaq leading the pack with a stellar 6% monthly gain, followed by the S&P 500 at 3.5%, and the DJIA up 1.1%, as shown in the chart above. The TSX, however, ended the month slightly lower despite showing signs of upward momentum towards the month’s end.

In the US, hopes for a sooner-than-expected rate cut by the Fed fueled the market rally. Initially, mixed labour reports and hawkish comments from Fed officials had caused some concern. However, a better-than-expected May Consumer Price Index inflation report and other positive economic data revived expectations for a potential September rate cut and possibly another cut later in the year.

Nvidia’s impressive performance and the overall AI frenzy played a significant role, driving the tech-heavy Nasdaq and S&P 500 to multiple record highs during the week. However, when the AI enthusiasm cooled, markets experienced a pullback, as seen in the past week.

In Canada, the BoC kicked off the month by lowering the benchmark rate by 0.25%. However, stronger-than-expected labour data led to reduced expectations for a second cut in July, contributing to the TSX’s negative performance for most of June.

The AI rally in the US spilled over into Canada, causing investors to favour tech stocks over resource shares, putting downward pressure on the resource-heavy TSX. It was not until the AI rally began to wane and energy and resource prices rose that the TSX started to rebound.

Overall, June was a positive month for the major North American indexes, marked by AI-driven gains and easing inflation, which boosted investor confidence despite the backdrop of global uncertainties. July has historically been a mixed month but often provides positive returns. June provided a strong lead-in, as the Fed’s preferred measure of underlying US inflation, core PCE, decelerated in May, further supporting the case for lower interest rates later this year.

![]() June was a month of mixed fortunes across the three portfolios, as depicted in the chart below.

June was a month of mixed fortunes across the three portfolios, as depicted in the chart below.

Portfolio 1 started off strongly with two weeks of solid gains. However, it faced headwinds in the latter half of the month, ending with a respectable 4.7% increase overall. The standout performer was Nvidia, whose surge in the AI sector initially lifted the portfolio to new heights. Yet, as the AI rally tapered off, Portfolio 1 felt the downside of being overly concentrated in one company as well, illustrating Nvidia’s pivotal role throughout the month.

Portfolio 2 experienced a more turbulent month, marked by two weeks of losses offsetting two weeks of gains, resulting in a slight monthly loss. The decline was primarily driven by a significant drop in MongoDB shares, which overshadowed gains from other holdings.

Portfolio 3 had a solid showing, with three weeks of gains leading to a healthy 3.4% increase for the month. Unlike Portfolio 1 and 2, no single stock dominated its performance. Shopify’s (TSE: SHOP) recovery from early-month setbacks helped balance losses from investments in Lithium Americas (TSE: LAC) and Lithium Americas (Argentina) (TSE: LAAC).

Overall, it was a positive month for most portfolios, although Portfolio 2 fell short of positive territory. This month highlights the risks of over-concentration in a single holding. Its great when a single stock drives the portfolio higher, but not so great when it drags it down despite a decent performance from the other holdings in the portfolio. This underscores the importance of diversification in managing portfolio risk and ensuring more stable returns over time.

Companies on the Radar

Once again, no new companies caught my attention this past week. However, I did narrow down the companies on my radar list to three. I’ve decided to move on from Quanta Services, Ltd. (NYSE: PWR) and Vistra Corp (NYSE: VST). I might revisit Quanta if the share price drops, but for now, I believe there are better opportunities available. As for Vistra, it is an American utility company that falls outside my ‘circle of competence,’ so I have removed it from my list.

Once again, no new companies caught my attention this past week. However, I did narrow down the companies on my radar list to three. I’ve decided to move on from Quanta Services, Ltd. (NYSE: PWR) and Vistra Corp (NYSE: VST). I might revisit Quanta if the share price drops, but for now, I believe there are better opportunities available. As for Vistra, it is an American utility company that falls outside my ‘circle of competence,’ so I have removed it from my list.

The radar list now comprises these three companies listed below.

- Equitable Bank (TSE: EQB), a mid sized Canadian bank, considered Canada’s 7th bank, that provides financial services to consumers and businesses.

- Vertiv Holdings (NYSE: VRT), an American company that designs and builds infrastructure and continuity solutions to businesses around the world.

- Lumine Group (TSE: LMN), a young Canadian mid sized company that acquires communications and media software companies, and then strengthens and grows those companies.

Please keep in mind that these are only companies that have piqued my interest. This is not a recommendation or financial advice. You should do your own research or contact a professional before making any investment decisions.

The Radar Check was last updated June 28, 2024.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended June 28, 2024: DOWN ![]()

- Rivian Automotive (NASD: RIVN) has retooled its manufacturing process, resulting in a 35% reduction in cost of materials, streamlined the battery making process, and removed over 53 pieces equipment from the body shop and over 500 components from the original R1S SUV. The company believes all these efficiencies will help Rivian turn its first gross profit.

In other Rivian news, after seeing if Rivian’s architecture and software could improve the driving experience of Volkswagen’s (OTCM: VWAPY) Audi brand, Volkswagen invested US$ 5 billion in Rivian. The integration of Rivian technology has led the two companies to form a joint venture to share electric vehicle (EV) architecture and software in various Volkswagen brands, including Audi and Porsche. - Amazon (NASD: AMZN) became the fifth US company to close above US$ 2 trillion in market capitalization (number of outstanding shares X price per share). The other four companies are Microsoft, Apple, Nvidia, and Alphabet (NASD: GOOGL).

- General Motors’ (NYSE: GM) Cruise robotaxi unit named Marc Whitten as its new Chief Executive Officer. Mr. Whitten was one of xBox’s founding engineers.

- Sales of Apple’s iPhones surged almost 40% in May, continuing the rebound that started in April following a sharp decline in March and the first quarter.

Activity

Bought: Celsius Holdings (NASD: CELH) Building on my successful investments in Celsius Holdings back in August 2020 and October 2021, I decided to make a third investment while the share price was down. Celsius continues to demonstrate strong financial performance, with consistent growth in sales, income, earnings per share, and cash flow, while maintaining minimal long-term debt.

I am impressed by Celsius’ ability to achieve brand recognition in the expanding health and wellness market. The recent $550 million investment from PepsiCo (NASD: PEP) provides Celsius with additional financial resources and access to PepsiCo’s vast distribution network, accelerating their customer base expansion. This partnership strengthens Celsius’ position against competitors like Coca-Cola (NYSE: KO) and Monster Beverage (NASD: MNST).

While consumer preferences can shift, Celsius’ track record and strong fundamentals give me confidence in their future. After experiencing a 150% return on my previous investments over four years, I am happy to increase the number of shares in a company that is clearly on a winning trajectory. 😊

Sold: Global-E Online (NASD: GLBE) I invested in Global-E back in July 2021 to capitalize on the e-commerce boom and the increasing need for merchants to ship products worldwide. While e-commerce is still thriving and global shipping remains essential, Global-E’s share price has not lived up to its potential. Since peaking at $80 in September 2021, the stock has languished in the $20-$40 range. I intended for this company to be a high-growth investment, but it has not delivered on that promise. Although it might eventually return to its former glory, I see no signs of that happening anytime soon.

Additionally, I am currently streamlining my portfolio and have grown tired of waiting for a rebound. There are more compelling opportunities available, whether it is increasing my stake in existing holdings or exploring new investments. It is time to move on and allocate my resources to more promising prospects.

Dividends

Dividends Received this week for the following companies:

Canadian $

Hammond Power Supply (TSE: HPS.A)

Canadian National Railway Company (TSE: CNR)

US $

NVIDIA Corp (NASD: NVDA)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended June 28, 2024: UP ![]()

- The EU’s EC continues to flex its newfound DMA muscle. The EC charged that Microsoft engaged in anticompetitive practices by bundling its Teams app with its Office suite, giving it a competitive edge over rivals in the video conferencing business.

The EC is also taking a look at Microsoft’s relationship with OpenAI to ensure it is not blocking smaller AI companies from working with OpenAI.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Canadian $

Hammond Power Supply (TSE: HPS.A)

Brookfield Infrastructure Partners LP (TSE: BIP.UN)

Brookfield Infrastructure Corp (TSE: BIPC)

US $

No US$ dividends this past week.

Quarterly Reports

ATD

Fourth quarter 2024 financial results on June 25, 2024

Portfolio 3

Portfolio 3 for the week ended June 28, 2024: UP ![]()

- Shopify is working with Target (NYSE: TGT) to enable Target “to offer a selection of its popular merchants and their products on Target Plus.” Target also plans to offer some of Shopify’s merchants the ability to sell their products at Target’s physical stores.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Canadian $

Brookfield Asset Management (TSE: BAM)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.