Mr. Powell goes to Washington

In a week of high anticipation, US Federal Reserve (Fed) Chair Jerome Powell took center stage in Congress, providing crucial updates on the future of rate cuts. During his Senate testimony on Tuesday, Powell expressed optimism as inflation approached the Fed’s 2% target, signaling potential for future rate cuts. He emphasized the need for ‘more good data’ to strengthen the case for sustained downward inflation trends. He also noted that Fed officials “have seen considerable softening” of the labour market.

On Wednesday, Powell reiterated this message to the House of Representatives, emphasizing that while the job market is cooling and inflation is trending downward, the Fed wants to see sustained price stability before reducing the benchmark rate. He noted the delicate balance the Fed faces: keeping rates high for too long could harm the economy but lowering them too soon might rekindle inflation.

Adding to the complexity of the rate decision is the looming Presidential election in November. Democrats advocate for rate cuts to reduce housing costs and maintain a strong job market. Meanwhile, Republicans argue that any rate cut before the election could appear as though the Fed is favoring the current administration.

In the end, Powell’s testimony underscored the Fed’s cautious approach to managing the economy. With the intricate dance between maintaining economic stability and navigating the political landscape, the path forward is anything but clear. As the Presidential election draws closer, all eyes will be on the Fed’s next move, as they strive to balance the fine line between fostering growth and preventing a resurgence of inflation. The stakes are high, and Powell’s leadership will be crucial in steering the US economy through these uncertain times.

As we digest this pivotal information from the Fed and ponder its potential impact on us and our investments, let’s look at what unfolded in the markets over the past week.….

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, First Investments: Building Your All-Stock Portfolio….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Canadian market volatility

Canada’s Volatility Index, the CVIX, fell to 7.97 this past week from 8.95 the previous week. This decrease likely stems from the previous week’s labour report indicating a slowing labour market and economy, opening the door for the Bank of Canada (BoC) to reduce the interest rate again this month. Additionally, the latest US inflation report showed cooling inflation in the US, increasing the likelihood of a rate cut in September by the Fed. The CVIX, measured through the VIXI on the Toronto Stock Exchange (TSE), gauges expected market volatility; lower values indicate less uncertainty and a more confident investor sentiment.

US Economic news

This past week’s key data points that the Fed considers when deciding whether to raise or lower the interest rate.

Consumer price Index (CPI)

The Labor Department’s June CPI report, a broad measure of the cost of US goods and services, brought some encouraging news. The all-items index, or headline CPI, fell 0.1% after being unchanged in May, marking the first drop since May 2020. On an annual basis, the CPI rose 3.0% in June, which was lower than analysts’ expectations of 3.1% and down from a 3.3% gain in May. It was also the lowest annual increase since June 2023.

Core CPI, which excludes the more volatile food and energy components, rose by just 0.1%, below the expected 0.2% increase and matching the smallest monthly rise since August 2021. Annually, the core CPI increased by 3.3%, the lowest since April 2021, and below analysts’ expected increase of 3.4%.

In terms of specific categories, the biggest monthly price increase was in ‘Utility (piped) gas service,’ up 2.4%, while ‘Gasoline’ saw the largest drop, down 3.8%. On an annual basis, ‘Transportation services’ had the biggest price increase at 9.4%, while ‘Used cars and trucks’ saw a significant decrease in prices, dropping 10.1%.

This decline in prices is good news for consumers and investors hoping for lower interest rates. The trend of decelerating inflation should also please Fed officials, who are looking for ‘more good data,’ as Fed Chair Powell mentioned. Combined with a softening labour market indicated by last week’s report, this data has boosted investors’ hopes for a rate cut in September. Let us hope the July CPI report continues to show inflation heading towards the Fed’s 2% target.

American market volatility

The CBOE Volatility Index (VIX), often referred to as the market’s “fear gauge,” dropped ever so slightly from 12.48 to 12.46 over the past week. This decrease likely reflects the latest CPI report showing falling inflation, which has increased the chances of an interest rate cut in September. At 12.46, the VIX is currently at its lowest point for a July in the past 5 years, especially during an election year. This low level suggests investors are currently more confident about the future direction of the stock market and the chances of a rate cut.

Consumer Sentiment Index (CSI)

The University of Michigan’s preliminary reading for the July CSI came in at 66.0, lower than the expected 68.2 and down from 68.2 in June. It was the second straight month that consumer sentiment was basically unchanged. On a monthly basis, sentiment dropped 3.2%, while year over year, sentiment is down 7.7%. Consumers were optimistic about the possibility of lower interest rates, but overall sentiment remained largely unchanged for the second month. This suggests a cautious wait-and-see approach, with some optimism about inflation cooling but also concerns due to the upcoming election. Nearly half of consumers are still concerned about high prices, adding to the overall uncertainty.

Overall, the report suggests consumers remain cautious. Inflationary concerns remain present, and upcoming elections are injecting uncertainty into economic outlook.

First Investments: Building Your All-Stock Portfolio

When considering your first investments, focus on those that align with specific types of investments that suit your goals. Whether you are drawn to stable core holdings, income-generating stocks, high-growth opportunities, or even companies that simply bring you enjoyment, building an all-stock portfolio allows you to tailor your investments precisely to your preferences and risk tolerance.

When I first started investing, my choices were all over the place because I had no clear plan. I picked companies I was familiar with, but in hindsight, I wish I had a strategy from the beginning. As I have gotten more serious about investing, I have developed a solid plan for building an initial portfolio. Remember, there is no perfect portfolio, and no one style of investing works for everyone. Your unique situation and personality should drive your portfolio composition.

Here are my thoughts on building an all-stock portfolio from scratch:

1. Diversification: Aim to invest in 15 or more companies across different sectors and categories. This does not mean you need to start with 15 companies immediately, but it is a good target to aim for. Holding 15 to 30 stocks allows you to spread out risk, reducing the impact of any single company or poorly performing sector. Beyond 30 stocks, the benefits of diversification diminish, and managing the portfolio can become complex. Holding between 15 to 30 stocks strikes a balance between diversification and manageability.

2. Company Types: I categorize companies into five groups: Core, Income, Growth, Swing for the Fences (SFTF), and Fun:

- Core Holdings: These are companies you intend to buy and hold for a long time, allowing them to grow and compound over time. They provide long-term growth and stability. Examples include any of the big six Canadian banks like Royal Bank (TSE: RY) or heavyweight technology companies like Microsoft (NASD: MSFT).

- Income Companies: These companies should have a regular dividend that yields 3% or more. I want dividends that are higher than the BoC and the Fed’s target of an inflation rate of 2%. Ideally, these companies will also see steady growth in their share price. This category generates income and can balance the more volatile growth companies. Telecommunications companies like Telus (TSE: T) or Real Estate Income Trusts (REITs) such as Dream Industrial Real Estate Investment Trust (TSE: DIR.UN) are good examples of companies that provide regular income.

- Growth Companies: These are more volatile but offer substantial long-term growth potential. While they are riskier, investing in high-growth companies is where you are likely to achieve substantial long-term capital growth. Look for companies with innovative products or services. It is crucial to identify companies with products or services that are not dependent on unique, fleeting circumstances. For example, Peloton (NASD: PTON) soared during the pandemic when everyone stayed at home but has since seen its share price fall 85% from its late 2020 highs.

- SFTF Companies: Typically, early-stage ventures with high-risk, high-reward potential. Only consider these after establishing a solid foundation. Monitor these closely and be ready to sell part or all of your investment if the price suddenly soars. Most of my SFTF investments have not worked out and I am now very hesitant to invest in riskier companies. An example of this was Voyager Digital (OTCM: VYGVQ). I thought this was a safer way to play the cryptocurrency craze in early 2021. However, I did not pay close attention to that investment and the company collapsed and went bankrupt. ☹

- Fun Companies: These are companies you invest in for personal enjoyment or interest, even if you only purchase one share. For instance, I may never own a Ferrari (NYSE: RACE), but I can say I own the company. 😊 I will also never own a professional sports team, but I’m an owner of the Atlanta Braves baseball team (NASD: BATRK). 😊

3. The Trifecta Company: My favorite type of company fits into multiple categories—offering stability, income, and growth potential. For instance, Microsoft is a core holding of Portfolios 2 and 3 (core), provides income through dividends (income), and has shown robust growth (growth). Sometimes, a company may start in one category but over time expands into multiple categories. This happened with Ferrari. I thought it would be great to say I owned Ferrari (fun), but it provides a dividend (income), and the share price grew so much (growth) that I purchased additional shares.

Now that I have outlined the types of companies to consider, let us delve into some specific companies that may be a good way to start building your portfolio. For your initial investments, prioritize less volatile companies. Typically, these are large Canadian or American companies that are less volatile and lower risk, most of which pay dividends.

Canadian Companies to Consider:

- Any of the big six Canadian banks: Royal Bank, TD Bank (TSE: TD), Bank of Montreal (TSE: BMO), Canadian Imperial Bank of Commerce (TSE: CM) and Bank of Nova Scotia (TSE: BNS)

- Railway companies like CN Rail (TSE: CNR) or Canadian Pacific Kansas City (TSE: CP)

- The big three telecommunication companies (Telus, Bell (TSE: BCE), and Rogers (TSE: RCI.B)) despite their recent price trends

American Companies to Consider:

- Well known, traditional companies such as Berkshire Hathaway (NYSE: BRK.B), Coca Cola (NYSE: KO), Procter & Gamble Company, (NYSE: PG), Exxon Mobil Corporation (NYSE: XOM)

- Big technology companies like Microsoft, Apple (NASD: AAPL), Amazon (NASD: AMZN) and Alphabet (Google) (NASD: GOOGL or GOOG), if you can handle a bit more risk

Since I focus on technology companies, these are the ones I recommend, but there are plenty of other options in sectors you might be more familiar with and comfortable in.

Remember, these are not recommendations or financial advice. You should do your own research or contact a professional financial advisor before making any investment decisions. Good luck and happy investing! 😊

Weekly Market Review

Monday: the indexes bounced up and down over the flatline most of the day before the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), and the Nasdaq Composite Index (Nasdaq) ended on the positive side and the Dow Jones Industrial Average (DJIA) on the negative side. Lifting the markets was last week’s US labour data indicating a weakening labour market. Oil prices edged lower as tensions in the Middle East cooled, reducing supply concerns.

In Canada, the TSX was lifted by positive labour news last Friday that opened the door to further rate cuts in Canada, and an initial rate cut in September for the US. In trading, Healthcare posted the biggest gain while Basic Materials (miners and fertilizers) was the only Canadian sector to end in the red.

In the US, the S&P and Nasdaq continued their record setting ways, establishing higher closes. Driving the markets was investor optimism that the Fed could make it first rate cut as soon as September. In trading, the biggest advance was in Technology, while the Communications Services dropped the most.

Tuesday: a mixed day for the indexes with the S&P and Nasdaq each ending in the green while the TSE and DJIA both ended in the red. The big news of the day was Fed Chair Jerome Powell started the first of 2 days of meetings with Congress to shed light on the Fed’s thinking on interest rates. In today’s meeting with the Senate, he said he was encouraged by falling inflation, but the Fed officials want more data showing inflation continues to fall to the Fed’s 2% target. Oil prices dropped after hurricane Beryl caused minimal damages in Texas.

In Canada, the TSX slid lower on fears of a recession after last week’s labour market report showed an increase in unemployment. In a day of broad-based losses, only the Financials and Consumer Staples sectors were able to post gains, while the Energy sector fell the most.

In the US, by ending higher today, the Nasdaq posted its sixth record high closes and S&P extended their run of record setting closes to five. In trading, Financials was the best performing sector, while Basic Materials fell furthest into the red.

Wednesday: all four indexes each surged over 1% after Fed Chair Powell’s testimony to Congress re-enforced investors’ belief that interest-rate cuts could come as soon as September. Tomorrow’s US CPI report will go a long way into determining the chances of a September rate cut. Oil prices climbed following forecasts of increased demand and news of a substantial drawdown in US oil inventories.

In Canada, higher commodity prices, particularly gold, and the possibility of a second rate cut by the BoC drove the TSX higher. In trading, it was a day of broad gains led by the Basic Materials sector. Communications Services was the only sector not to advance.

In the US, the S&P and Nasdaq, which rose above 5,600 for the first time, continued to set record highs on the strength testimony from Mr. Powell which led to a surge in the big technology companies. In trading, all American sectors gained ground, led by the Technology sector with the Financials sector bringing up the rear.

Thursday: the markets were mixed with the TSX and DJIA ending higher, while the S&P and Nasdaq fell lower. Many investors moved out of technology stocks and into other interest sensitive sectors after the latest US CPI report showed prices had fallen more than expected. Hopes for a September rate cut also lifted oil prices.

In Canada, optimism about a US rate cut helped lift the TSX to its highest level in over a month. In trading, Basic Materials posted the biggest gain, while Consumer Staples was the only Canadian sector to end in the red.

In the US, the ‘Magnificent 7’ group of companies had their worst day in almost a year, weighing heavily on the Nasdaq, and to a lesser extent on the S&P. Many investors rotated out of the heavyweight technology stocks and into smaller companies which have been rallying on news of lower rates. In trading, Utilities advanced the most, while Technology suffered the largest decline.

Friday: a good day in the markets that saw all four indexes end in the green. Investor optimism about cuts to the US interest rate drove the indexes higher.

In Canada, the TSX set a record high close buoyed by the prospects of a rate cut in the US. In trading on Bay Street, the Consumer Staples sector posted the largest gains, while the Energy sector recorded the biggest drop.

In the US, the DJIA closed above 40,000 for only the second time ever, just shy of a record high close. Optimism about a rate cut was tempered by mixed earnings reports from a few of the major US banks. In trading on Wall Street, it was a day of broad-based advances led by the Consumer Staples section. The Telecommunications Services sector was the only sector that did not record a gain.

Weekly Market and Portfolio Review

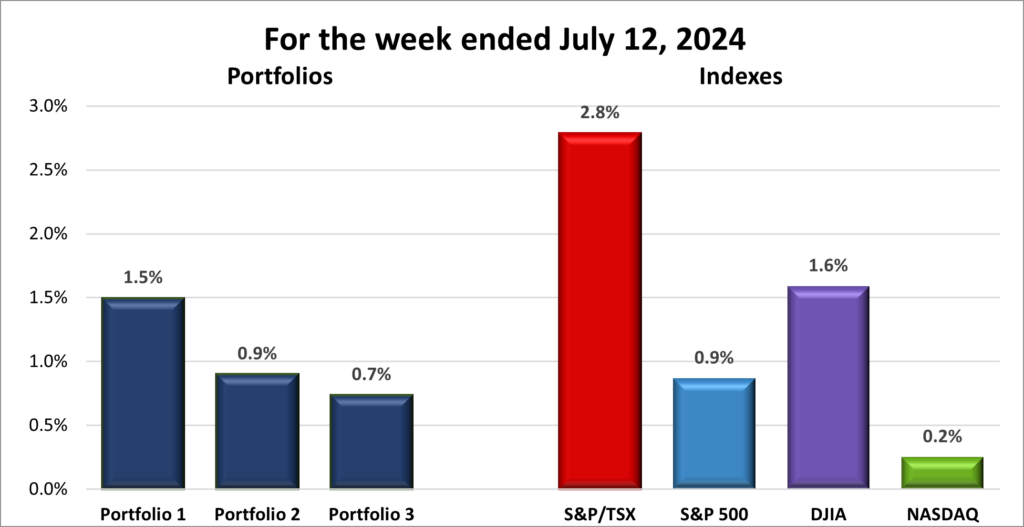

For the week, the TSX (SPTSX) surged 2.8%, the S&P 500 (SPX) added 0.9%, the DJIA (INDU) rose 1.6% and the Nasdaq (CCMP) advanced 0.2%.

| Index | Weekly Streak |

| TSX: | 3 – week winning streak |

| S&P: | 2 – week winning streak |

| DJIA: | 2 – week winning streak |

| Nasdaq: | 6 – week winning streak |

![]() As you can see in the chart above, all four indexes ended higher, extending their weekly winning streaks.

As you can see in the chart above, all four indexes ended higher, extending their weekly winning streaks.

The S&P 500 and Nasdaq experienced their longest winning streaks since January but stumbled on Thursday as investors rotated out of tech giants and into smaller companies that have lagged most of the year, seeking greater potential upside. Meanwhile, the DJIA surpassed the 40,000 mark, achieving its best weekly performance since October 2023. The TSX also set a record close to end the week.

The market’s upward momentum was fueled by positive labour and inflation data. Early in the week the indexes were driven by labour reports from the previous week from both Canada and the US, indicating a cooling job market. Midweek, the US CPI report showed broad inflation cooling in June to its slowest pace since 2021, with the overall measure falling for the first time since the pandemic. Core CPI rose by just 0.1% from May, the smallest increase in three years, dragged lower by cheaper gasoline.

The Fed has held the interest rate at a record high of 5.25%–5.50% for a year now. With inflation declining for two straight months, they may be ready to cut rates in September. Waiting too long to reduce rates could slow the economy further and worsen unemployment, which edged higher in June.

Falling inflation and a cooling labour market provide the Fed with the “more good data” that Fed Chair Powell has been seeking. Slowing inflation should bolster the Fed’s confidence, and unless there is a surge in prices over the next two months, a September rate cut seems likely, with the possibility of another cut before the year ends. Additionally, in his recent testimony, Powell highlighted that a cooling labour market reduces the risk of persistently high inflation, though any further weakening in the job market would be unwanted.

One additional benefit of a US rate cut for Canadian consumers and investors is that it clears the way for a second rate cut by the BoC. The central bank may be hesitant to reduce the Canadian benchmark rate to avoid diverging too far from the American benchmark. Diverging rates can make American imports more expensive, leading to a different source of higher prices.

Let us hope ‘more good data’ continues to come in for both countries, kicking the door open for rates cuts in both Canada and the US. 😊

| Portfolio | Weekly Streak |

| Portfolio 1: | 2 – week winning streak |

| Portfolio 2: | 3 – week winning streak |

| Portfolio 3: | 3 – week winning streak |

![]() As you can see in the chart below, it was another good week for the portfolios, as each one increased in value and extended their respective winning streaks.

As you can see in the chart below, it was another good week for the portfolios, as each one increased in value and extended their respective winning streaks.

Portfolio 1 was the standout performer with a gain of 1.5%. This success was driven by almost twice as many companies posting weekly advances, including an impressive 20% jump by Rivian (NASD: RIVN).

Portfolio 2 saw a solid increase of 0.9%, despite no significant (greater than 10%) movers. This gain was buoyed by 75% of the stocks increasing in value this past week.

Portfolio 3 trailed slightly with an increase of 0.7%, but still managed to record advances in almost 80% of its holdings.

Overall, it was a strong week for the portfolios, with all three showing gains. I am particularly pleased with the broad-based nature of these advances, which did not rely on just one or two stocks to lift a portfolio. A diversified rally like this is much more sustainable because it spreads the risk and reduces the chance of sharp corrections if any single stock faces negative news or performance issues. Hopefully, next week will see all three portfolios continue their winning streaks, driven by similarly broad gains. 😊

Companies on the Radar

After consulting with an accountant, I decided to remove Energy Transfer LP (NYSE: ET) from my radar list. The potential tax implications of a Canadian investing in an American Master Limited Partnership (MLP) were too complex and could result in additional taxes for me. If the tax implications were challenging for an accountant, they were certainly too complicated for someone without cross-border tax expertise like me. For more on MLPs, check out the July 5 Weekly Update, What I learned II.

After consulting with an accountant, I decided to remove Energy Transfer LP (NYSE: ET) from my radar list. The potential tax implications of a Canadian investing in an American Master Limited Partnership (MLP) were too complex and could result in additional taxes for me. If the tax implications were challenging for an accountant, they were certainly too complicated for someone without cross-border tax expertise like me. For more on MLPs, check out the July 5 Weekly Update, What I learned II.

The radar list is back to these three companies below:

- Equitable Bank (TSE: EQB), a mid sized Canadian bank, considered Canada’s 7th bank, that provides financial services to consumers and businesses.

- Vertiv Holdings (NYSE: VRT), an American company that designs and builds infrastructure and continuity solutions to businesses around the world.

- Lumine Group (TSE: LMN), a young Canadian mid sized company that acquires communications and media software companies, and then strengthens and grows those companies.

Please keep in mind that these are only companies that have piqued my interest. This is not a recommendation or financial advice. You should do your own research or contact a professional before making any investment decisions.

The Radar Check was last updated July 12, 2024.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended July 12, 2024: UP ![]()

- Trisura (TSE: TSU) announced a number of changes to their senior management team. Allison Kenworthy will become the chief financial officer, Phillip Shirtliff will become the chief risk officer, while Chris Sekine was appointed as an executive director and Richard Grant will be chief underwriting officer.

- Costco (NASD: COST) announced they were raising their membership fees for the first time since 2017. The new prices will take effect September 1, 2024.

- Apple announced they will open their tap and go mobile payment system to competitors as the company attempts to avoid investigations by the European Union’s anti trust regulator, the European Commission (EC). The EC’s Digital Markets Act seeks to ensure a level playing field for vendors of all sizes and to provide consumers more mobile payment options.

- General Motors (NYSE: GM) is set to receive over US $500 million to upgrade a plant in Michigan to build electric vehicles (EV). The grant is part of a $1.1 billion plan to convert 11 existing conventional engine vehicle factories, across eight states, to factories producing EVs and EV components.

Activity

Sold: Unity Software (NYSE: U) I invested in Unity Software in March 2021 because it was the dominant gaming platform and a leader in augmented reality (AR) and virtual reality (VR) development. Back then, the ‘Metaverse’ was all the rage, and Unity seemed poised to be a major player. I was particularly excited about Unity’s expansion into industries beyond gaming, where it could become the dominant force in commercial and industrial VR/AR applications.

Initially, the investment looked promising, with the share price rising. However, as excitement over the ‘Metaverse’ faded, so did Unity’s stock, plummeting 85% from its peak. I kept hoping for a turnaround, but it never came. The final nail in the coffin was Nvidia’s 2024 Annual Review, which highlighted Nvidia’s rise as a major gaming platform and a key player in commercial AR/VR applications.

To simplify my portfolio and focus on 20-30 companies, selling Unity became an obvious choice.

Sold: Nano-X Imaging (NASD: NNOX) I initially invested in Nano-X Imaging as a Swing For The Fences (SFTF) high-risk, high-reward opportunity back in August 2020. The company touted revolutionary digital imaging X-ray devices and a unique business model where they would essentially give away the devices but charge on a per-use basis. This concept sounded promising, and the share price initially soared over 190%. However, it has since plummeted almost 80% from my investment.

Unfortunately, the company was not as advanced in their technology as they led investors to believe. Nano-X’s core product, the low-cost X-ray device, is still under development and has not achieved widespread commercial adoption. They are also still seeking regulatory approval, causing further delays.

With my goal to streamline Portfolio 1, Nano-X emerged as an obvious candidate to sell.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Telus Corp. (TSE: T) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended July 12, 2024: UP ![]()

- Walt Disney Company (NYSE: DIS) announced they plan to add a ninth cruise ship to their fleet. The ship is a partnership between Disney and the company that operates Tokyo Disneyland, Oriental Land Company (OTCM: OLCLY). The unnamed vessel will have a maximum capacity of 4,000 passengers and is scheduled to sail from Tokyo in the 2028 fiscal year. The new ship is part of Disney’s 10-year, US$ 60 billion parks, and cruises expansion.

- Microsoft has dropped its OpenAI Board of Directors’ observer seat after drawing unwanted attention from regulators in the US and the European Union. Microsoft said the seat was no longer necessary after OpenAI improved its governance.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Telus Corp. (TSE: T) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended July 12, 2024: UP ![]()

- Magnite (NASD: MGNI) announced their SpringServe ad Server and Magnite Streaming SSP has been selected by Telus to be their ad technology solutions platform. Telus will load their streaming and online video inventory onto a SpringServe ad server and use Streaming SSP to manage and monetize that inventory.

- After digesting its acquisition of HSBC’s (NYSE: HSBC) Canadian banking unit, the Royal Bank plans to separate its personal and commercial banking business into two separate units.

Activity

Sold: Unity Software I first bought Unity shares for Portfolio 1 in March 2021. Encouraged by the rapid increase in the share price, I made a second purchase in May 2021, this time for Portfolio 3. Unfortunately, since then, the share price has plummeted. Given the same reasons for selling in Portfolio 1, I decided it was prudent to sell the Unity shares in Portfolio 3 as well.

Dividends

Dividends Received this week for the following companies:

No dividends this past week.

Quarterly Reports

No quarterly reports this past week.