This past week was pivotal for investors. The latest US inflation numbers, measured by the Consumer Price Index (CPI), could swing the door open for a possible US interest rate cut in June – if it indicated that inflation was on the decline. Conversely, flat, or rising inflation rates could extinguish any hopes for a rate reduction in June.

In this week’s edition of our series for new investors, I will cover a few of the risks beginners should be aware of when they start investing. Alongside the latest US inflation report and what it meant for investors, let’s see what else happened this past week….

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, Types of direct investing risks, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Bank of Canada meeting

As expected, the Bank of Canada (BoC) maintained Canada’s benchmark interest rate at 5%. This decision marks the sixth consecutive time the rate has been held steady since July 2023.

The Bank observed that the economy stalled in the latter half of 2024, but they are now forecasting growth of 1.5% this year and 2.2% next year, driven by higher consumer spending and increased immigration. The labour market continues to slow, with unemployment edging higher in March. Regarding inflation, the bank acknowledged signs of subsiding inflation since the start of the year, highlighted by the March CPI report which showed inflation had dropped to 2.8%. The Bank predicts inflation will hover around 3% during the second quarter, falling to 2.5% by the year’s end and returning to their 2% target in 2025. Given these factors, they decided to hold the interest rate at 5% and continue monitoring the downward inflation trend.

At their post-meeting press conference, BoC Governor Tiff Macklem said “Yes, June rate cut is within the realm of possibilities” if the recent cooling trend in inflation continues. BoC officials want to see more data to be confident that the downward trend in inflation will be sustained. The possibility of a future rate cut is positive news for borrowers, as it would lower interest rates on loans and mortgages. However, this is not guaranteed, and a lot can happen between now and the next central bank meeting. It will depend on future economic data and there are two more CPI reports before their June 5 meeting.

Overall, the BoC’s announcement suggests a wait-and-see approach to monetary policy. If inflation continues to slow, there is a chance Canadians could see interest rates start to drop. Keep your fingers crossed. 😊

Canadian market volatility

Over the past week, Canada’s Volatility Index (VIXC), which tracks the TSX 60 VIX, rose over 10% to 12.94, from the previous week’s 11.67. The BoC decision to maintain the interest rate at 5%, combined with the higher-than-expected US inflation report making it more likely that the Fed will delay the first US rate cuts is likely the cause of the increased volatility reading.

The VIXC, often referred to as Canada’s ‘fear gauge,’ provides insights into the expected volatility within the Canadian stock markets. Typically, readings above 20 signify high volatility, while those below 20 indicate low levels. The current reading of 12.94 places it well below the high volatility zone.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Federal Open Market Committee (FOMC) meeting minutes

The minutes from the March 19-20, 2024, FOMC meeting were released this week. At that meeting, FOMC members kept the benchmark interest rate at 5.5%, marking the third consecutive hold. The minutes indicated that Fed officials considered a number of factors before making their decision.

US GDP grew solidly in the first quarter, though slower than the fourth quarter. The job market remained strong with job gains and slightly higher unemployment. Consumer price inflation in the form of Personal Consumption Expenditures (PCE) continued to decline but stayed above 2%. In contrast, foreign economies showed weak growth and high inflation due to higher energy prices.

US financial conditions eased slightly since January, with rising equity (stocks) prices outweighing interest rate hikes. This growth was primarily driven by large-cap tech stocks, while broader markets saw more measured gains.

The FOMC members acknowledged progress towards their 2% inflation target but noted higher-than-expected recent inflation readings. This suggests inflation’s decline might have stalled, potentially requiring higher rates for longer. They anticipated some unevenness in inflation data as it returns to target.

Overall, the FOMC agreed the economy continued to expand, the job market remained strong with low unemployment, and inflation, though down year-over-year, remained above target. They viewed the outlook as uncertain, emphasizing the need to monitor inflation risks.

Consumer Price Index (CPI)

The latest inflation figures from the March CPI showed inflation rose 0.4%, matching February’s pace of 0.4%. Shelter (mortgage and rent) and gas prices accounted for half of the monthly increase. Annually, the CPI increased 3.5%, accelerating from last month’s rate of 3.2%. Both numbers were higher than analysts’ expectations of a 0.3% and 3.4% rise, respectively. The all-items CPI, or headline CPI, has increased monthly since the December 2023 data shoed inflation grew at a rate of 0.2%.

The price of ‘Gasoline’ saw the largest monthly increase, up 1.7%, while the price of ‘Used cars and trucks’ saw the biggest decline, down 1.1%. Annually, ‘Transportation services’ saw the biggest increase, up 10.7%, while ‘Fuel oil’ posted the biggest decrease, down 3.7%

Core CPI, which excludes volatile energy and food prices, increased 0.4%, the same pace as the February increase. Year over year, core CPI growth remained steady at 3.8%, the same as the previous month. Both numbers were higher than analysts’ predictions of a 0.3% and a 3.7% increase, respectively. Core CPI has remained unchanged at 0.4% since January 2024.

Based on this latest report, the rate of inflation has remained constant monthly, however, on a yearly basis, inflation is up. The Fed has said they wanted to see evidence that inflation was falling before they considered lowering the interest rate. This higher-than-expected inflation report, combined with last week’s higher than expected labour report, all but ensures interest rates remain higher through the summer. That is neither good news for consumers nor businesses.

American market volatility

The CBOE Volatility Index (VIX), often referred to as the market’s fear gauge, rose 8% to end the week at 17.31, up from 16.03 the previous week. Although this uptick keeps the VIX below the 20-point threshold commonly associated with heightened volatility, it signals a rise in investor anxiety about potential market fluctuations in the near future. The rise of the VIX is likely driven by the higher-than-expected inflation report, which weakens the possibility of a June rate cut and likely lowers the number of cuts this year from three to two cuts. While investor anxiety remains relatively low, it is clear that there’s growing caution around market volatility.

Consumer Sentiment Index (CSI)

The University of Michigan’s preliminary Consumer Sentiment Index (CSI) registered at 77.9, falling short of analysts’ expectations of 79.0. This figure marks a 1.9% decrease from March’s 79.4 but also represents a significant 22.3% increase from the same period last year. Consumer sentiment continues to hover in a narrow range between 75 and 80, indicating that consumers perceive little change in the economic landscape over the course of this year.

The CSI is a monthly survey that measures consumer confidence in the US economy. A higher CSI indicates greater optimism among consumers.

What type of risks should I be aware of if I’m going to invest directly in companies?

When discussing investments with people considering investing or new to investing, a common concern is the fear of losing everything. While total loss is possible, it is relatively rare. For instance, I once lost an investment in a cryptocurrency company when the company went bankrupt. However, gains from other companies in my portfolio have more than compensated for this loss. So, while the risk of loss is real, there are effective strategies to mitigate it.

Understanding Stock Market Risks

Investing in the stock market inherently involves the risk of losing money. Several factors can lead to a decrease in a company’s share price, including poor management, failure to innovate, industry disruptions, accounting irregularities, or outright fraud. Not all declines happen overnight—many are gradual, barring exceptional circumstances like fraud. If you suspect a company is in decline, you can always sell your shares. Remember, a small loss now can prevent a larger one later. 😊

Effective Risk Mitigation Strategies

- Diversification: Investing in a single company is risky, akin to putting all your eggs in one basket. By spreading your investments across at least 15 companies from varied sectors (e.g., technology, banking, consumables), you reduce the impact of any single company’s failure. This lowers risk significantly, as the successful investments can offset any faltering ones.

- Long-Term Investing: Adopting a ‘Buy and Hold’ strategy—investing in larger, quality companies for the long term, typically over five years—minimizes risk by focusing on company performance rather than short-term share price fluctuations. Periodic portfolio reviews are essential to ensure your investments are on track to help you reach your goals. I consider a ‘quality’ company one that has strong financial health, stable revenue growth, robust profit margins, a clear competitive advantage, good corporate governance, and a proven track record of resilience and growth prospects. Additionally, such companies often offer consistent dividends.

Common Investment Pitfalls to Avoid

- Liquidity Needs During Downturns: One of the biggest risks is the need to liquidate your investments during a market downturn (like in 2022). If you anticipate needing funds in the short term (1 – 2 years), consider safer, more liquid options like Guaranteed Investment Certificates or High Interest Savings accounts.

- Emotional Responses: Decisions driven by short-term market movements can lead to premature selling, resulting in unnecessary fees and taxes. Invest in quality companies and concentrate on the long-term prospects of your investments.

- Chasing Trends: Investments in trendy stocks or sectors, such as meme stocks, can be very volatile and often benefit seasoned players at the expense of less experienced investors.

- FOMO: Avoid the allure of jumping into the latest popular stock. High transaction costs and taxes can erode gains. For instance, in 2020, the metaverse was a ‘hot’ investment. Many who chased this trend experienced significant losses when the market shifted focus. Try to ignore the hype and opt for well-established companies with promising long-term prospects.

Final Thoughts

Remember, selling shares triggers tax implications, so be mindful of capital gains taxes. Additionally, avoid using margin accounts for investment; while they offer more buying power, they also carry the risk of a margin call, potentially forcing you to sell other investments to cover the ‘loan’ from your brokerage.

Investing directly in companies carries various risks, but with careful planning, diversification, and a long-term perspective, you can successfully navigate these challenges. Don’t be afraid to consult with a financial advisor or a tax consultant.

Weekly Market Review

Monday: the markets were up and down like a yoyo today as investors come to grips with the likelihood that strong economic data will likely delay interest rate cuts by the Fed. At the end of the trading session, the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), and the Dow Jones Industrial Average (DJIA) all ended slightly below the baseline, while the Nasdaq Composite Index (Nasdaq) ended slightly higher. Oil prices dropped slightly as tensions eased in the Middle East after Israeli troops reduced their presence in southern Gaza.

In Canada, the markets were relatively quiet as analysts and investors await the BoC interest rate decision on Wednesday. Investors will be looking for clues as to when the BoC could make its first interest rate cut. In trading, Industrials and Utilities advanced the most of the Canadian sectors, while Consumer Cyclicals and Healthcare lost the most.

In the US, investors await this week’s latest news on inflation to see if it has resumed its downward trend. Anything but a drop in CPI could delay cuts to the interest rate. In trading, Basic Materials (miners and fertilizer manufacturers) posted the biggest gains, while Energy and Healthcare declined the most.

Tuesday: another mixed day in the markets with the DJIA down slightly but essentially unchanged, while the other three indexes were each slightly higher.

In Canada, the TSX was in the green most of the day on the way to setting a record high closing because of higher gold and commodity prices. Tomorrow, the BoC will announce its latest decision on the benchmark interest rate. In trading, it was a day of broad-based advances, led by Basic Materials and Telecommunications Services. Healthcare was the only sector to decline.

In the USA, Investors were cautious as they waited for tomorrow’s latest US inflation numbers and the release of the minutes from the Fed’s March meeting. Analysts and investors alike will scrutinize the minutes and inflation data, looking for clues as to when rates might start to fall. In trading, Basic Materials and Consumer Cyclicals posted the biggest gains, while Telecommunications Services had the biggest losses.

Wednesday: it was a pivotal day for the markets, unfortunately it pivoted the wrong way. ☹ The US inflation data for March showed inflation was higher than expected, causing many investors to feel the Fed will not only delay a rate cut, but also reduce the number of rate cuts. The indexes ended sharply lower following the disappointing news. Oil prices rebounded following two days of declines after Middle East peace talks stalled.

In Canada, the BoC left the Canadian interest rate unchanged at 5%, however, it indicated a June reduction was possible if inflation continued to fall. With the Canadian interest rate staying at 5% and the inflation news out of the US, the TSX recorded its biggest decline in two months. In trading, the Energy and Basic Materials sectors were the only sectors to end in the green. Technology and Financials posted the biggest losses.

In the USA, the only positive news of the day was the minutes from the Fed’s last meeting revealed many of them felt a rate cut would be appropriate at some point in 2024. In trading, it was a day of broad-based losses that saw only the Energy sector able to end in positive territory. Financials and Utilities suffered the largest losses.

Thursday: after yesterday’s market plunge, the markets rebounded with the S&P and Nasdaq ending higher, the DJIA was flat while the TSX lost ground for the second consecutive day. Investors are now recalibrating their expectations for when the Fed will start lowering the US interest rate. Oil prices were slightly higher on concerns the Middle East conflict could spread further in the region, offsetting yesterday’s high inflation data.

In Canada, lower oil prices prevented the TSX from joining its American siblings in the win column. In trading on Bay Street, Basic Materials and Technology were the biggest winners of the Canadian sectors, Energy and Industrials suffered the biggest setbacks.

In the US, a bit of good inflation news in the form of lower-than-expected producer prices suggested inflation continues to fall despite yesterday’s high inflation data. The good news led to a rally in the big technology companies that sent the Nasdaq to a record high. In trading on Wall Street, Technology and Consumer Cyclicals led the charge upward, while Financials and Consumer Cyclicals recorded the biggest retreat.

Friday: earnings season got off to an auspicious start with all four indexes ending deeper in the red. Oil prices moved higher after Israel rejected a Hamas proposed ceasefire, renewing Middle East supply disruption concerns.

In Canada, despite higher energy prices, the TSX had its biggest one day drop in almost two months because of lower commodity prices and concerns of sticky US inflation. In trading, it was a day of losses across the board. Industrials and Utilities fell the least while the Healthcare and Technology sectors recorded the biggest losses.

In the US, the big US banks got earnings season off to a rocky start with unimpressive results. The lack of strong results left investors’ focus on sticky inflation, weighing down the markets. As a result, the DJIA had its steepest weekly since March 2023. In trading, all sectors ended lower. The Utilities and Consumer Staples sectors fell the least while Technology and Consumer Cyclicals dropped the most.

Weekly Market and Portfolio Review

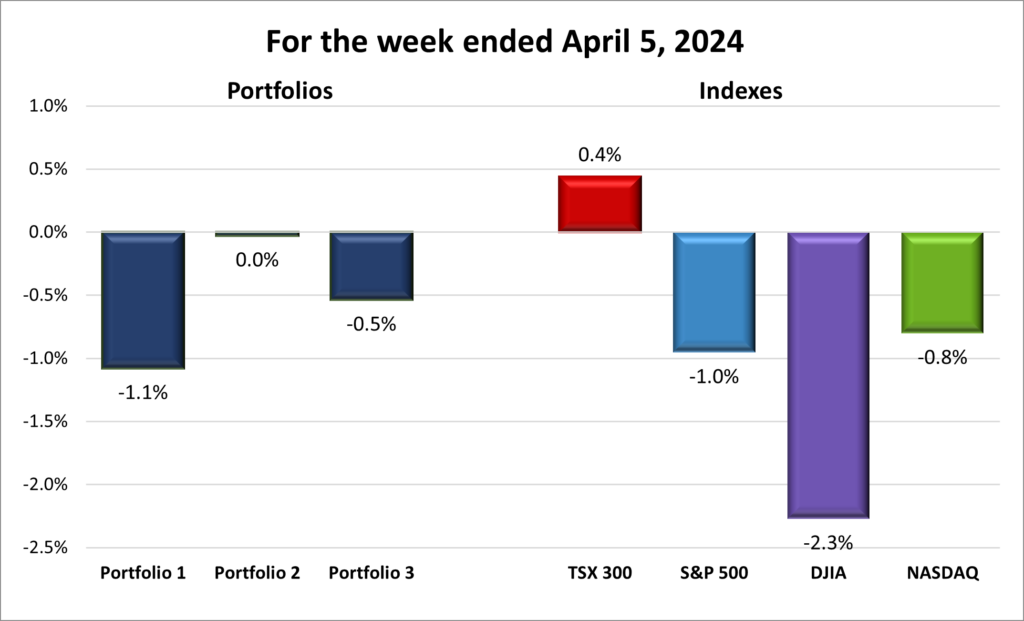

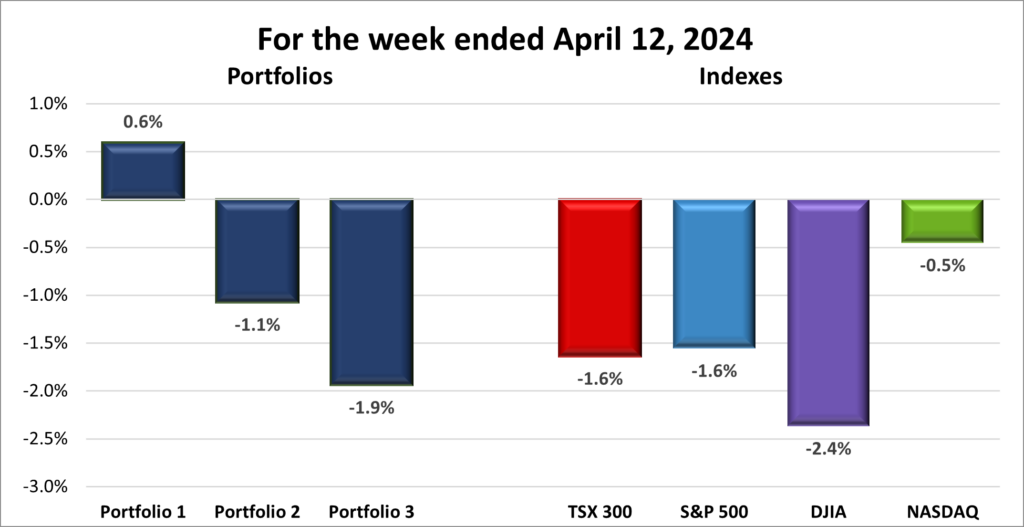

For the week, the TSX (SPTSX) fell 1.6%, the S&P 500 (SPX) dropped 1.6%, the DJIA (INDU) plunged 2.4% and the Nasdaq (CCMP) slipped 0.5%.

| Index | Weekly Streak |

| TSX: | 1 – week losing streak |

| S&P: | 2 – week losing streak |

| DJIA: | 2 – week losing streak |

| Nasdaq: | 3 – week losing streak |

![]() As illustrated in the chart above, it was a challenging week for the indexes. All four major North American indexes recorded weekly losses, despite a rally on Thursday that briefly pushed the Nasdaq into positive territory.

As illustrated in the chart above, it was a challenging week for the indexes. All four major North American indexes recorded weekly losses, despite a rally on Thursday that briefly pushed the Nasdaq into positive territory.

The primary driver behind market fluctuations this week was an unexpectedly high US inflation report. Both headline CPI (which includes all items) and core CPI (which excludes volatile food and energy prices) matched or exceeded estimates on both a monthly and annual bases. Coupled with previous reports showing a robust US economic growth and a strong labour market, this persistent inflation continues to concern investors about about the timing of the Fed’s potential rate cuts. Initially, the Fed had signaled three rate cuts in 2024, with investor expectations of reductions beginning as early as March. However, there has yet to be a rate cut, and following this latest inflation report, investors are reevaluating the timing and extent of these cuts, with current expectations leaning towards one or two cuts of 0.25% each in the second half of this year, signifcantly later and less than the 1.50% total anticipated at the start of the year.

In contrast, the BoC offered a more promising outlook, suggesting a possible rate cut in June should inflation continue to decrease. Despite this positive news, the TSX was also weighed down by a weekly decline in oil prices, though prices remain high enough to keep upward pressure on gasoline prices.

While Canada might see rate reductions as early as June, the scenario in the US appears more inclined towards maintaining “higher for longer” rates.

| Portfolio | Weekly Streak |

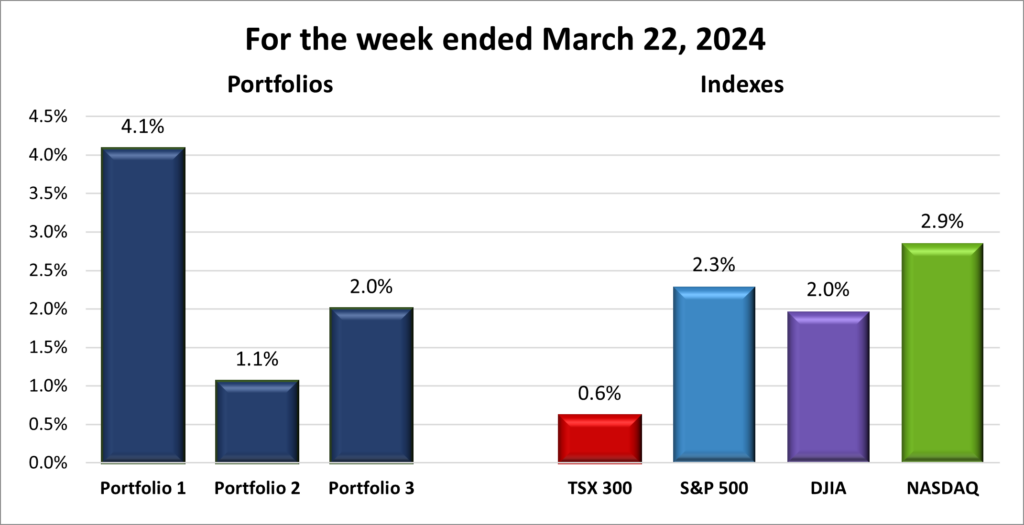

| Portfolio 1: | 1 – week winning streak |

| Portfolio 2: | 2 – week losing streak |

| Portfolio 3: | 4 – week losing streak |

![]() With all four indexes losing ground this past week, it was somewhat surprising to find that Portfolio 1 managed to increase in value. Unfortunately, its gains were not sufficient to offset the losses experienced by the other two portfolios.

With all four indexes losing ground this past week, it was somewhat surprising to find that Portfolio 1 managed to increase in value. Unfortunately, its gains were not sufficient to offset the losses experienced by the other two portfolios.

Portfolio 1 had a busy week with investments in two new companies and the divestment of two others. A review of the holdings revealed a roughly equal split between stocks that increased and those that decreased in value. Many of the technology stocks rose in value, however, gains were seen in other sectors. While no company posted a significant (more than 10%) gain, Rivian Automotive (NASD: RIVN) recorded a sizable loss of 11%.

Portfolio 2 faced a challenging week with over 80% of its holdings declining in value slightly. The most significant drop was seen in Brookfield Infrastructure (TSE: BIPC), which fell by 10%.

Portfolio 3 recorded the weakest performance, with very few stocks advancing. The widespread downturn was so pronounced that stocks which remained flat were considered to have had a good week. ☹

April has started on a challenging note. Despite this, the rebound in Portfolio 1 provides a glimmer of hope. Looking ahead, I am hoping for a week of strong earnings reports to reverse the market’s current downtrend – caused by recent, stronger-than-expected US labour and inflation reports – and see all three portfolios post a weekly win.

Companies on the Radar

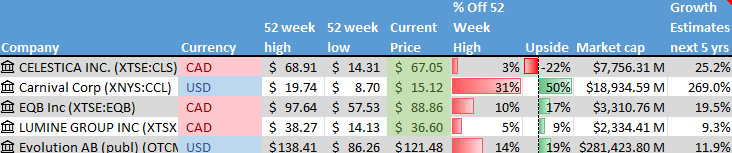

This week brought several changes to my Radar list. Celestica Inc. (TSE: CLS) moved from the list to join Portfolio 1, reflecting its strong past performance and promising future prospects. Similarly, Carnival Cruise Line (NYSE: CCL) advanced to Portfolio 1, buoyed by its potential for nearly 50% growth.

This week brought several changes to my Radar list. Celestica Inc. (TSE: CLS) moved from the list to join Portfolio 1, reflecting its strong past performance and promising future prospects. Similarly, Carnival Cruise Line (NYSE: CCL) advanced to Portfolio 1, buoyed by its potential for nearly 50% growth.

Meanwhile, Arista Networks (NYSE: ANET) came onto my radar. Arista is a large American company specializing in networking products for global enterprises and has shown substantial growth over recent years, with its share price climbing in response to its robust performance. Though Arista has lingered on the outskirts of my radar for some time, it had not fully captured my attention until now. Looking back at the company’s achievements over the last few years, it is clear it deserved a closer examination earlier.

Arista joins the three remaining companies from last week:

- Equitable Bank (TSE: EQB), a mid sized Canadian bank, considered Canada’s 7th bank, that provides financial services to consumers and businesses.

- Lumine Group (TSE: LMN), a young, mid sized Canadian company that acquires communications and media software companies and then strengthens and grows those companies.

- Evolution AB (OTCM: EVVTY), a Swedish company that provides live casino solutions for global gaming operators.

Please keep in mind that these are only companies that have piqued my interest. This is not a recommendation or financial advice. You should do your own research or contact a professional before making any investment decisions.

The Radar Check was last updated April 12, 2024.

NOTE: Morningstar and Thomson-Reuters analysis is unavailable for Evolution from my usual sources because the company’s home stock exchange is the Nasdaq Stockholm in Sweden. While it is possible to invest in Evolution through the Over-the-Counter Market, I do not have access to analysis similar to the data available for companies traded on the major North American stock exchanges (Toronto Stock Exchange, New York Stock Exchange, and Nasdaq Stock market). The Analysts Rating and Price Target for Evolution are from Yahoo! Finance, under the Analysis tab once you have searched for the ticker.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended April 12, 2024: UP ![]()

- Nvidia (NASD: NVDA) is being sued for trademark infringement by Modulus Financial Engineering. The company complains Nvidia’s new artificial intelligence (AI) software Modulus creates confusion with their own AI related software. Since I have never heard of Modulus Financial, I can see how anyone not familiar with the company would think of Nvidia rather than their product.

- Alphabet’s (NASD: GOOGL) announced two new semiconductors. The first is their own Tensor processing units (TPU), used in their datacentres for their AI services. This chip is not for resale and is only available for use through Google’s Cloud services. The other chip is an Arm (NASD: ARM) based central processing unit. This chip, called Axion, is also only available via the Google Cloud. Customers can build and run their application in Google’s cloud on Axion chips or build AI applications and run them on TPUs on the Google cloud.

In other Google news, Epic Games has asked a US federal court to force Google to allow third party app stores on Google’s Android mobile operating system. This decision could go either way. If Google were to lose this challenge it could be a hit to their Google Play Store revenue stream. - General Motors (NYSE: GM) said they will resume their Cruise robo taxi services In Phoenix, AZ after suspending the service in San Francisco, CA about six months ago. However, the vehicles will be manually driven rather than fully autonomous as was the case in San Francisco.

- Apple (NASD: AAPL) announced plans to update all their Mac computers with their new M4 processors, complete with AI capabilities. The new computers should be available towards the end of 2024.

Elsewhere, Apple lost its attempt to have the British Competition Appeal Tribunal (CAT) dismiss a lawsuit that claims it charged over 1,500 British base developers unfair commission fees. The lawsuit is for almost US$ 1 billion. - Amazon (NASD: AMZN) loaded up its AI credentials with the addition of computer scientist Andrew Ng who previously headed up AI projects at Google. Amazon is in a race for market shares with other big AI companies such as Google and the Microsoft/OpenAI combination.

Activity

Bought: Celestica Inc. Celestica is a Canadian multinational in the electronics manufacturing services (EMS) industry, offering comprehensive hardware platform, lifecycle support, and supply chain solutions on a global scale. As a pivotal partner for notable companies like Cisco (NASD: CSCO) and Dell (NYSE: DELL), Celestica plays a critical role in the design, manufacture, and delivery of electronic products. The company’s involvement across diverse markets – ranging from communications and enterprise computing to aerospace, defense, and more – affords a natural hedge against sector-specific downturns, thereby reducing investment risk.

Over the years, Celestica has demonstrated solid growth in revenue, net income, and free cash flow. The company has a robust balance sheet, and they are focused on profitability and capital efficiency. While historical success does not guarantee future outcomes, the increasing demand for advanced technology and the prevailing outsourcing trends present favorable growth opportunities for Celestica.

Potential challenges for Celestica include the impact of sustained high interest rates, which could slow the technology sector’s growth. Furthermore, Celestica’s extensive global operations expose it to a range of political, economic, and supply chain risks. However, the company has successfully navigated these headwinds in the past so they should be able to navigate future headwinds.

A mid-sized ($2 billion – $10 billion) powerhouse, Celestica offers stability and growth potential in the expanding electronics manufacturing market. While it increases the portfolio’s technology focus, Celestica adds a stable and established company with significant growth potential in an expanding market. 😊

Bought: Carnival Corporation Carnival is more than one cruise line, it also owns well known cruise lines Princess Cruises (of Love boat fame), and Holland America Line as well as a number of smaller, regional cruise companies that sail in various parts of the world. As well as cruise ships, the company also operates port destinations and their own private islands that their ships stop at. This provides other sources of revenues for the company

I have never been on a cruise and have no desire to go on a cruise in the future. However, a growing number of others do. The global cruise industry continues to recover from the Covid-19 pandemic and is expected to grow in the coming years, driven by factors like increasing disposable income, pent-up demand after the pandemic, and growing popularity of cruises in Asia.

The pandemic hit Carnival and its share price hard. Many analysts believe the company is undervalued with plenty of upside potential, as much as 50% in the next year. As for the financials, revenues, Free Cash Flow (FCF) and net income are all trending upward. Excess capital from FCF has been used to pay down debt, ahead of schedule, that had jumped during pandemic when cruises were not running.

Risks involved in this investment are many. Cruises are considered a discretionary expense. Higher interest rates or an economic downturn could dampen travel, hurting Carnival’s business. Not only would higher interest rates impact travellers, but servicing this debt could limit their ability to invest in new ships or marketing initiatives. Other concerns include major competitors in the industry and growing concerns about the environmental impact of the cruise industry.

I do not plan to hold this stock for a long time, perhaps up to three years, however, the industry and company appear to be on the upswing. After weighing the pros and cons of an investment in Carnival, I felt the risk was worth the reward. Hopefully, this cruise will enjoy fair winds and a following sea as the investment cruises to higher returns. 😊

Sold: Nuvei Corporation (TSE: NVEI) The company has agreed to be taken private by Advent International. The deal has the support of the majority owners so it is very unlikely the share price will go higher than the original offer of US$ 34.00 per share.

This investment did not turn out as planned. I should have sold my initial investment in late 2021 when the share price was near its all time peak. Instead, I purchased additional shares, only to see the bottom fall out during 2022. The share price has been slowly increasing, but not enough to avoid a loss on this investment.

It is frustrating to miss a peak and see the price fall. However, I decided to take advantage of this buyout and move on to other opportunities, like investing in Celestica. 😊

Sold: Nvidia Corp As I noted in the March 29 Weekly Update [link to March 29], Nvidia had grown to over 40% of the total portfolio value, making it overly sensitive to the share price fluctuations of a single stock. I trimmed the number of NVidia shares because I typically aim to keep individual holdings below 35% of the portfolio. The proceeds will be reallocated to other top performers.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended April 12, 2024: DOWN ![]()

- MongoDB (NASD: MDB) announced expanded integration with Google’s Google Cloud services. This will enable Google Cloud customers to create AI applications using their own MongoDB hosted data.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Telus Corp (TSX: T)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended April 12, 2024: DOWN ![]()

- Microsoft (NASD: MSFT) announced they planned to invest US$ 2.9 billion over the next two years to expand their datacentre infrastructure and AI capabilities in Japan.

In other Microsoft news, the US Cybersecurity and Infrastructure Security Agency said Russian hackers are using credentials stolen from hacked Microsoft email accounts to try and gain access to Microsoft’s customer systems, including government agencies. - Brookfield Asset Management (TSX: BAM) is negotiating to purchase a majority position in private company Castlelake, an alternative investment company.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

TD U.S. Equity Index ETF (TSX: TPU)

Brookfield Asset Management Ltd. (TSX: BAM)

Brookfield Corp (TSX: BN)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.