Inflation jitters sent US markets south, while the TSX extended its weekly winning streak. Let us take a look at what happened and how it impacted the three portfolios. Plus, we will shift gears and explore the hot topic of hybrid electric vehicles – are they a sound alternative to full on electric vehicles or just a pit stop on the road to full electrification? This week I will take look at their gaining popularity and investment potential in this week’s market update!

So, without further ado, let’s see what happened this past week….

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, The rise of hybrids, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Canadian market volatility

This past week, Canada’s volatility index (VIXC), represented by the TSX 60 VIX, remained relatively unchanged at 11.67, compared to 11.63 the prior week. The minimal change comes despite higher-than-expected inflation data from the US. This suggests that investor confidence in the Canadian markets remains strong, possibly due to the rising TSX. The VIXC, also known as Canada’s ‘fear gauge,’ measures volatility within the Canadian stock markets. Readings above 20 are generally viewed as ‘high’ and those below 20 as ‘low’. The current reading of 11.67 sits firmly within the low volatility zone.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Consumer price Index (CPI)

Inflation remained steady in February with overall prices rising 0.4%, following a similar increase in January. Year-over-year, CPI rose 3.2%, exceeding analyst expectations of 3.1%. Higher gas prices (up 3.6%) were the main culprit, while restaurant prices saw the largest annual increase (up 4.5%).

Core CPI, which excludes the more volatile food and gas prices, rose 0.4%, following a similar increase in January. Annually, core cpi rose 3.8%. Both the monthly and annual numbers were higher than expected increases of 0.3% and 3.7%, respectively. The main cause of higher core inflation was shelter, which includes mortgages and rent, and transportation cost which rose due to higher fuel costs.

Fed officials have said they want to see more data showing inflation continues its downward trajectory to 2% before they lower the rate. With this latest data, there is no chance the Fed will lower the interest rate at their meeting next week. Analysts are now pointing to the June meeting as the earliest to expect rate cuts to begin.

American market volatility

The CBOE Volatility Index (VIX), also known as the fear gauge, dropped slightly by 0.2% this week, settling at 14.41 compared to 14.74 last week. While this suggests a cautiously optimistic market, the VIX fluctuated throughout the week between 15.97 and 13.46, highlighting its potential for quick swings. With a current reading of 14.41, the VIX sits comfortably below the 20 mark that typically indicates high volatility. This suggests that investor anxiety is currently relatively low.

Consumer Sentiment Index (CSI)

The University of Michigan’s preliminary mid-March reading of its CSI showed a slight decrease to 76.5, down from 76.9 at the end of February, contrary to analysts’ expectations for it to remain unchanged at 76.9. On a monthly comparison, the CSI experienced a minor decline of 0.5%, yet it has shown a substantial improvement of 23.4% compared to the same period last year. This recent update indicates that consumer sentiment is fairly stable, albeit with slightly tempered expectations due to a sense higher interest rates could remain longer than anticipated.

Retail Sales

The Commerce Department’s Census Bureau reported a modest 0.6% increase in retail sales In February, falling short of the anticipated 0.7% rise and coming after January’s revised decline of 1.1%. Year-over-year, sales grew by 1.5%, slightly below the expected 1.6%. These figures suggest a dip in consumer spending, largely attributed to the dampening effect of higher interest rates on expenditures.

Despite these lower-than-expected sales figures, the Fed is unlikely to shift towards lowering interest rates in the near term. This stance is due to recent reports on the CPI and Producer Price Index (PPI) showing inflation rates higher than anticipated, which overshadow concerns of reduced spending. The Fed remains focused on curbing inflation to meet its 2% target, prioritizing the control of price levels over stimulating an already strong economy.

The rise of hybrids

Why are many motorists turning to Hybrid Electric Vehicles (HEVs) as their vehicle of choice, especially amidst reports of slowing EV sales? The reasons are as varied as they are compelling, marking a significant shift in consumer preferences towards more sustainable and practical transportation solutions. This interest in hybrids, is reflective of a broader market dynamic where the appeal of proven hybrid technology is gaining ground, not just for its environmental benefits, but also for its practical advantages. At the heart of this shift towards an electrified future in the North American automotive industry, several key factors are driving the growing popularity of hybrids.

Originally this was to be a brief summary of HEV benefits but it became longer than anticipated, so I decided to give the topic its own post. To discover why drivers, keen on reducing their carbon footprint, are increasingly choosing HEVs over EVs as they move away from internal combustion engines, click here.

Weekly Market Review

Monday: the markets continued last week’s pullback before a late day surge nudged the value-oriented Toronto Stock Exchange Composite Index (TSX) and the Dow Jones Industrial Average (DJIA) into positive territory at the end of the day. Investors were cautious ahead of Tuesday’s US CPI inflation report that could provide clues to how soon the Fed could start cutting rates. Oil prices rose slightly as demand concerns in China were offset by supply concerns in the Middle East.

In Canada, the TSX benefited from higher oil prices and investors moving into more traditional, value-oriented companies. In trading, the Energy and Basic Materials (miners and fertilizer manufacturers) sectors posted the biggest gains, with Healthcare and Technology dropping the most.

In the US, the more growth oriented the S&P 500 Index (S&P), and the Nasdaq Composite Index (Nasdaq) ended the in negative territory as investors hedged their bets against the last inflation report before the Fed’s next meeting. In trading, Telecommunications Services and Consumer Staple saw the biggest gains, while Technology and Industrials posted the biggest losses.

Tuesday: all four indexes ended higher as investors did not seem bothered by the latest US inflation report that showed core inflation came in higher than anticipated. Despite the CPI numbers, investors still believe the Fed will lower the rates sometime in summer.

In Canada, the TSX closed at its highest point since April 2022. In trading, the Canadian Technology and Industrials sectors advanced the farthest, while losses were only suffered in Utilities, Telecommunications Services, and Basic Materials sectors.

In the US, the S&P set a record high close. In trading, the Technology and Consumer Cyclicals gained the most, while Utilities, Telecommunications Services and Basic materials were the only American sectors to drop.

Wednesday: a mixed day in the markets with the S&P and Nasdaq ending lower in the red, while the TSX and DJIA ended higher in the green. Investors are still digesting yesterday’s higher than expected core inflation data which could provide the Fed with a reason to maintain the current rate for longer. Oil prices edged upward on signs of higher demand from the US.

In Canada, the TSX extended its rally a third day thanks to higher oil and other commodity prices. In trading, the top sectors were Basic Materials and Technology, while the Telecommunications Services and Utilities were the only Canadian sectors to end in the red.

In the USA, investors seemed to be taking more money off the table after Wednesday’s rally in technology companies. In trading, Energy and Basic Materials had the biggest gains, while Technology, Healthcare and Consumer Cyclicals were the only American sectors to end lower.

Thursday: all four indexes ended lower after the US PPI showed wholesale inflation came in twice as high as expected. Another higher-than-expected inflation report has investors considering the Fed could wait longer than expected to lower the US interest rate. Oil prices rose on supply concerns and lower US inventories.

In Canada, the TSX got caught in the downdraft from the US, sending the TSX into the red and ending its three-day winning streak. In trading, Energy was the only Canadian sector to post a gain, otherwise all sectors ended lower with Telecommunications Services and Consumer Staples dropping the farthest.

In the US, higher inflation data from the CPI and PPI reports has investors concerned interest rates cold remain higher, for longer. In trading, the Energy sector was the only American sector to end higher. Financials and Telecommunications Services suffered the biggest losses.

Friday: sticky inflation reports weighed on the markets, with the TSX the only major North American index to make it into positive territory at the end of the day. The thought of interest rates remaining higher for longer whiles the Fed continues to try and drive inflation down to 2% has stalled the markets upward momentum. After a short rally this past week, oil prices fell on some profit taking.

In Canada, the TSX ended the day in the green. Rising commodity prices more than offset the drop in technology stocks. In trading on Bay Street, Healthcare and Basic Materials posted the largest gains, while Technology and Consumer Cyclicals suffered the biggest losses.

In the USA, a pullback in semiconductor stocks contributed to the drop in the American indexes, sending the Nasdaq to its first weekly back-to-back losses in five months. Higher-than-expected inflation numbers pushed up US Treasury yields, and now have investors contemplating the first-rate cut coming in July. In trading on Wall Street, Basic Materials and Industrials were the biggest winners, while Technology and Consumer Cyclicals posted the biggest losses.

Weekly Market and Portfolio Review

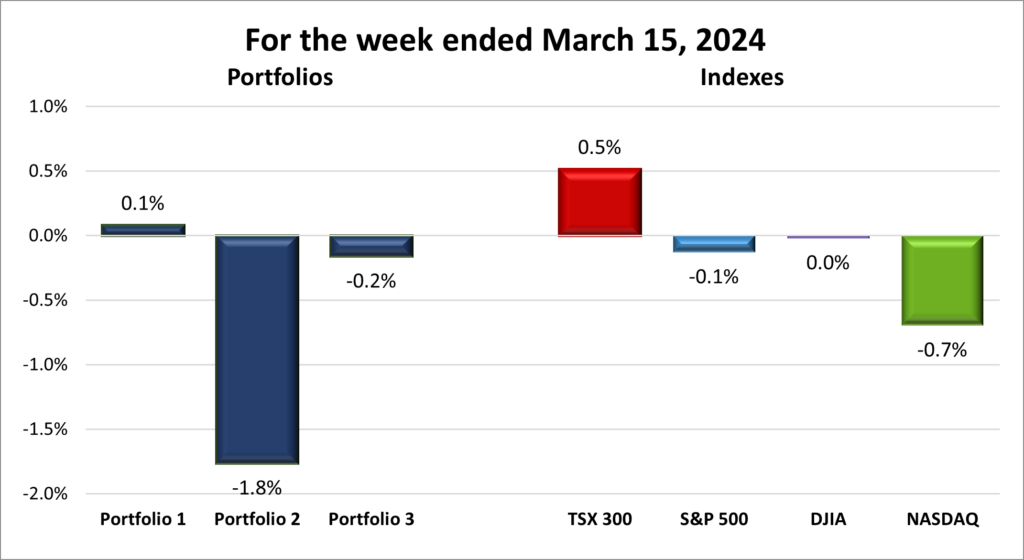

For the week, the TSX (SPTSX) gained 0.5%, the S&P 500 (SPX) fell 0.1%, the DJIA (INDU) slipped 0.02% and the Nasdaq (CCMP) dropped 0.7%.

| Index | Weekly Streak |

| TSX: | 5-week winning streak |

| S&P: | 2-week losing streak |

| DJIA: | 3-week losing streak |

| Nasdaq: | 2-week losing streak |

![]() The TSX stretched its weekly winning streak to five, its longest in eleven months, standing out as the only major North American index to manage a gain this past week, as illustrated in the graph above.

The TSX stretched its weekly winning streak to five, its longest in eleven months, standing out as the only major North American index to manage a gain this past week, as illustrated in the graph above.

In last week’s congressional testimony, Fed Chair Jerome Powell stressed the need for “just a bit more evidence” that inflation is moving towards the Fed’s 2% target before the central bank would consider cutting borrowing costs. The latest CPI data—showing inflation at 3.2% and core CPI rising to 3.8%— was not what investors’ were hoping for. Nevertheless, the market experienced a rally on Wednesday. It seems investors had anticipated these higher figures, judging them insufficient to derail a potential interest rate cut in June.

Investors had been hoping that recent economic, job, and inflation data wouldn’t significantly influence the Fed’s upcoming interest rate decisions. The anticipation is for rate cuts this summer, which could lower borrowing costs for consumers and businesses, potentially stimulating the markets.

However, Thursday brought more US inflation data that was higher than expected, causing investors to reconsider the timeline for the Fed to begin lowering interest rates. This resulted in all three major American indexes finishing the week in negative territory.

After a strong start to the year, market momentum has cooled. Since late October 2023, there has been a healthy bull run with the TSX up 16% and the S&P up 23%, the latter setting a record close 17 times in 2024. Yet, recent strong economic data and unexpectedly high inflation figures have prompted a reassessment of when the Fed might reduce interest rates. While a rate cut is anticipated, the timing has become more uncertain.

Investors are hoping next week’s Fed meeting will provide clues on the outlook for rate cuts, preferably for cuts in June. For now, the market rally has paused, but the anticipation is for the upward trend to resume in due course.

| Portfolio | Weekly Streak |

| Portfolio 1: | 11-week winning streak |

| Portfolio 2: | 5-week losing streak |

| Portfolio 3: | 2-week losing streak |

![]() This week presented a mixed bag for my three portfolios, consistent with the overall downtrend in the markets. Only one managed to climb into the green, while the other two faced setbacks.

This week presented a mixed bag for my three portfolios, consistent with the overall downtrend in the markets. Only one managed to climb into the green, while the other two faced setbacks.

Portfolio 1 stood out, extending its winning streak to an impressive 11 weeks, largely buoyed by gains in four out of the five ‘Magnificent 7‘ companies it holds (Alphabet (NASD: GOOGL), Amazon (NASD: AMZN), Apple (NASD: AAPL), Nvidia (NASD: NVDA) and Tesla (NASD: TSLA))—Tesla being the lone exception. On a side note, Tesla has found itself as the S&P’s worst performer in 2024, down 34% since the start of the year. Otherwise, most companies in the portfolio showed minimal movement, except for Rivian Automotive (NASD: RIVN), which took a notable 13% hit. On a positive note, Nvidia celebrated its tenth consecutive week of gains—its longest streak ever—surging over 80% this year.

Portfolio 2 had a tough week, despite stock price performance almost evenly split between gains and losses. While Microsoft (NASD: MSFT) hit a new all-time high, the positive impact was negated by a significant 10% drop in Guardant Health (NASD: GH), with MongoDB also contributing to the downturn after a $25 drop in share price during the week.

Portfolio 3 had a volatile week. It got off to a promising start, with a 0.7% increase by Thursday. However, Friday’s market downturn, wiped out the gains and left the portfolio in the red for the week. The standout performer was Lithium Americas (TSE: LAC), which soared 19%. Despite this, the majority of companies saw their share prices end the week lower, with a 10% decrease in Enghouse Systems (TSE: ENGH).

Looking forward, investors turn their attention to the upcoming Fed meeting with cautious optimism. Any indication of a favorable shift in interest rate policy could serve as a catalyst for renewed investor confidence and a resurgence in market momentum. Here is to hoping for a positive pivot that reignites the markets’ upward trajectory and our portfolios’ continued success. 😊

Companies on the Radar

This week, no new companies caught my attention, but I have managed to trim my radar list to a more manageable five companies. Walmart (NYSE: WMT) has been added to Portfolio 1. Meanwhile, I’ve decided to part ways with Ulta Beauty (NASD: ULTA), and Monolithic Power Systems (NASD: MPWR). Although both Ulta and Monolithic are commendable companies, I believe the companies that remain on the list provide better opportunities for achieving my investment objectives.

This week, no new companies caught my attention, but I have managed to trim my radar list to a more manageable five companies. Walmart (NYSE: WMT) has been added to Portfolio 1. Meanwhile, I’ve decided to part ways with Ulta Beauty (NASD: ULTA), and Monolithic Power Systems (NASD: MPWR). Although both Ulta and Monolithic are commendable companies, I believe the companies that remain on the list provide better opportunities for achieving my investment objectives.

For now, the radar list consists of:

- Celestica Inc. (TSE: CLS), a medium sized Canadian company that manufactures electronic products and provides supply chain services to companies around the world.

- Equitable Bank (TSE: EQB), a mid sized Canadian bank, considered Canada’s 7th bank, that provides financial services to consumers and businesses.

- Lumine Group (TSE: LMN), a young Canadian mid sized company that acquires communications and media software companies and then strengthens and grows those companies.

- Palantir Technologies (NYSE: PLTR), an American company offering an AI-enabled software platform, primarily serving intelligence agencies for anti-terrorist efforts.

- Evolution AB (OTCM: EVVTY), a Swedish company that provides live casino solutions for global gaming operators.

Please keep in mind that these are only companies that have piqued my interest. This is not a recommendation or financial advice. You should do your own research or contact a professional before making any investment decisions.

The Radar Check was last updated March 15, 2024.

NOTE: Morningstar and Thomson-Reuters analysis is unavailable for Evolution from my usual sources because the company’s home stock exchange is the Nasdaq Stockholm in Sweden. While it is possible to invest in Evolution through the Over The Counter Market, there is no analysis similar to the data available for companies traded on the major North American stock exchanges (Toronto Stock Exchange, New York Stock Exchange, and Nasdaq Stock market). The Analysts Rating and Price Target for Evolution are from Yahoo! Finance, under the Analysis tab once you have searched for the ticker.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended March 15, 2024: UP ![]()

- Apple updated its App Store on iPhones in Europe that will allow third party developers to distribute their apps directly to consumers rather than through the App Store. The changes were made to comply with last week’s new European Union’s Digital Markets Act (DMA). To compensate for the lost revenue from the App Store, Apple has introduced a “core technology fee” of 50-euro cents per user account each year, even if developers opt not to use Apple’s App Store or payment system.

In other Apple news, the company bought Canadian artificial intelligence (AI) startup private company DarwinAI, adding its employees to Apple’s AI unit.

Apple settled a class action lawsuit for US$ 490 million that claimed Chief Executive Officer Tim Cook misled investors about falling iPhone sales in China. Apple denied the claim but settled to avoid costs and the distraction. - Tesla is in talks with a number of Southeast Asian countries about building another factory to handle demand from one of the fastest growing electric vehicles (EV) markets.

In other Tesla news, production has resumed at their German gigafactory after being shut down for a few days due to an arson attack at a nearby electrical pylon that caused a power failure. - Nvidia has sped up the pace of releasing new chips into the market from a two-year cycle to a one-year cycle for its AI data centre line of products. Next week the company is expected to release the B100, also known as Blackwell, the follow up to its successful H100 AI chips.

Activity

Bought: Walmart Inc. Portfolio 1’s technology-centric focus brings inherent volatility. Adding Walmart provides some stability as it consistently performs well during economic downturns, driven by consumer demand for essential goods. This will help mitigate losses when the broader market is struggling, like it did in 2022.

Walmart stands out among Consumer Staples companies for its strong revenue and profit generation, supported by a diversified business model encompassing retail, wholesale, and e-commerce operations. The acquisition of Vizio is particularly interesting, enhancing Walmart’s e-commerce capabilities and digital advertising reach, while leveraging its existing infrastructure and customer base. Additionally, Walmart’s stable cash flow supports a regular dividend, contributing to its appeal.

Financially, Walmart has growing revenues, net income, free cash flow, and earnings per share, complemented by a decreasing share count – indicative of a financially healthy company. Its wide moat, characterized by a brand synonymous with affordability, vast buying power, efficient supply chains, and comprehensive product assortment, strengthens its competitive position.

While risks exist, such as competition from other retailers and e-commerce giants, potential operational disruptions from unforeseen events, and supply chain challenges, Walmart’s proven history of overcoming such hurdles reinforces my confidence in its resilience. Although the share price may be a bit overvalued, I view it as more than offset by the company’s future growth potential.

Ultimately, the addition of Walmart provides Portfolio 1 with diversification, income, and growth potential, aligning with my objective to balance out volatility with established, stable investments. This investment enhances the portfolio’s resilience and positions it for sustained growth.

Sold: Progyny (NASD: PGNY) I initially invested in this company back in December 2019, a time when my approach to selecting stocks was not as selective as it is today. Despite its impressive spike during the 2021 bull run, the stock has since receded and remained stagnant around the mid US$ 30 range for the past 18 months. Although the investment turned out reasonably well, I have decided to sell it as part of a broader strategy to streamline my portfolio. For better management and a clearer picture of the portfolio, I am cutting down on the number of companies in the portfolio to focus on fewer, high-quality companies.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Pulse Seismic Inc (TSE: PSD)

Dream Industrial Real Estate Investment Trust (TSE: DIR.UN)

Yellow Pages Ltd (TSE: Y)

US $

General Motors Co (NYSE: GM)

Skyworks Solutions Inc (NASDAQ: SWKS)

BSR Real Estate Investment Trust (TSE: HOM.U)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended March 15, 2024: DOWN ![]()

- The European Union’s (EU) anti trust regulator, the European Commission (EC) has been ordered to take measures to protect personal data when it is transferred to non-EU countries. The EC was found to have breached privacy rules when it used Microsoft software and the data was transferred to Microsoft and other non-EU countries. The EC was also ordered to stop the transfer of data to countries outside the EU.

- Microsoft told the EU anti trust regulators, the EC, that arch competitor Alphabet’s Google enjoys a competitive advantage because of all the data it has collected over the years from its search engine, and its use of customized AI chips.

- TC Energy (TSE: TRP) announced they have sold their natural gas pipeline to Ksi Lisims LNG, a partnership between the Nisga’a first nations and American company Western LNG. The sale is part of TC Energy’s plan to sell assets to reduce corporate debt.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

SmartCentres Real Estate Investment Trust (TSE: SRU.UN)

iA Financial Corporation Inc (TSE: IAG)

US $

Microsoft Corp (NASD: MSFT)

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended March 15, 2024: DOWN ![]()

- Recently, Lithium Americas Argentina Corp. (TSE: LAAC).] and Lithium Americas Corp. were removed from the TSX by S&P Dow Jones Indices, the index manager. Its likely they were removed from the index as the fall in their respective share prices led to their market capitalizations following below the requirement to be included in the index. The S&P Dow Jones Indices periodically update the TSX, and other indexes, in order to remain relevant, and representative of the companies traded on the Toronto Stock Exchange as a whole to provide investors with accurate benchmarks.

In other Lithium Americas news, the company was granted a conditional commitment loan of US$ 2.26 billion by the US Department of Energy. The money will go towards financing the construction of its Thacker Pass, Nevada project. The mine is expected to become the largest source of lithium in North America when it becomes operational in three years. General Motors (NYSE: GM) is the largest investor in LAC and will receive the majority of lithium produced at the mine. - Brookfield Corporation (TSE: BN) is in negotiations with Singapore Communications, Southeast Asia’s largest telco operator, to acquire a significant stake of their wholly owned Australian unit Optus.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

SmartCentres Real Estate Investment Trust (TSE: SRU.UN)

US $

Microsoft Corp (NASD: MSFT)

Quarterly Reports

Enghouse Systems Limited

First quarter 2024 financial results on March 13, 2024