A friend of mine, let us call him the Stock Swami, jokingly (I think) asked me if it would be safer to keep your money under your mattress to avoid losing money during stock market crashes. This is a question I hear a lot from new investors, and it is a valid concern. There is a fear of losing money during market downturns.

Ultimately, the best place for your money depends on your individual circumstances and financial goals. If you need easy access to your money and want low risk, a savings account might be a good choice. For long-term goals and the potential for higher returns, you might consider stocks or other investments.

This week I compare the returns of a mattress and other places to park your money and get it working for you. But first, there was some good economic news, and Apple is getting ready to join the artificial intelligence field, but not as you might expect. So, without further ado, let’s look back at what else happened this past week….

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, Apple joins the AI race, The stock market versus your mattress, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

BoC meeting minutes

During their meeting on March 6th, the Bank of Canada (BoC) governors gathered to discuss Canada’s monetary policy and to determine the need for any adjustments to the benchmark interest rate.

During this meeting, the six-member council acknowledged a global economic slowdown, with the US as an exception thanks to its robust economy and labour market. Core inflation was easing in both the US and the European Union (EU), despite slight increases in oil prices. Consumer sentiment has improved thanks to a sustained rally in equities markets in Canada and the US.

Despite a rise in January’s GDP, economic growth in Canada remains below its potential, particularly a stagnant latter half of 2023. The labour market is weakening, with job growth unable to keep pace with population increases. Wage growth is slowing down. The Consumer Price Index (CPI) has dipped due to decreasing prices of goods, while the prices of services remain unchanged. Persistent high shelter costs are still applying upward pressure on inflation.

BoC officials noted that the higher interest rate is gradually balancing supply and demand as expected. However, they were concerned that inflation may be proving stubborn and losing its downward momentum. As well, the higher interest rates posed a risk of dampening economic growth and increasing unemployment, although recent GDP data has somewhat alleviated those fears. The members agreed they would need to tread carefully when balancing the risks of delaying rate cuts—potentially weakening economic conditions unnecessarily—against the risks of premature rate cuts that could undermine the progress made in their battle to lower inflation.

The decision was to maintain the current interest rate at 5.0%, and let it continue bringing down inflation. The governors concurred that they would need to see further evidence of a continued decline in inflation, especially core inflation, before considering a reduction in Canada’s benchmark rate.

Consumer Price Index (CPI)

Statistics Canada’s latest CPI report shows a welcome deceleration in the annual inflation rate, settling at 2.8% in February, down from January’s 2.9%. This is better than analysts’ forecasts of a 3.1% increase. On a month-to-month basis, inflation saw a modest uptick of 0.3% in February. Again, better than analysts’ predictions of a 0.6% increase.

While headline inflation, or the cost of all items, saw the biggest annual gains in shelter costs (rents and mortgages) up 6.5%, these were offset by significant declines in telephone and internet access services, down 20.5% and 13.2%, respectively. Travel tours saw the biggest monthly increase at 12.3% due mainly to higher fuel prices. Internet access services also led the monthly decline, dropping 9.4%. Notably, food price increases continue to slow, with grocery prices rising less than inflation for the first time since October 2021.

The core CPI, which excludes the volatile elements of gas and food prices, also showed signs of easing, slowing to 2.8% from January’s 3.1%, marking the lowest rate in two years. Month-over-month core inflation edged up slightly to 0.2% after being flat in January.

The BoC had indicated a desire for core inflation to continue to fall towards their 2% target. This latest report shows both headline and core figures within their 1% – 3% range and trending downward. With inflation showing signs of cooling, this report potentially opens the door for the central bank to lower the benchmark rate in June, if not sooner, which could lead to lower borrowing rates. This latest inflation report is good news for consumers, businesses, and the BoC.

Canadian market volatility

Over the past week, Canada’s Volatility Index (VIXC), which tracks the TSX 60 VIX, fell to 10.92 from the previous week’s figure of 11.67, reflecting a 6% decrease in expected volatility. This could be due to lower inflation figures, potentially paving the way for the BoC to consider interest rate cuts, as well as the US Federal Reserve reiterating their intention to reduce rates three times this year.

The VIXC, often referred to as Canada’s ‘fear gauge,’ provides insights into the expected volatility within the Canadian stock markets. Typically, readings above 20 signify high volatility, while those below 20 indicate low levels. The current reading of 10.92 places it well within the low volatility zone, underscoring a period of relative market stability.

Retail Sales

According to Statistics Canada, January retail sales decreased by 0.3%, following a 0.9% increase in December. This contraction, which was slightly less severe than the anticipated 0.4% decline, marked the most significant drop since March 2023. The decrease was primarily attributed to a 3.0% reduction in new car sales. However, when excluding gas stations, fuel vendors, and motor vehicle and parts dealers, core retail sales actually rose by 0.4% in January. Additionally, an advance estimate from Statistics Canada for February indicates a modest increase in retail sales of 0.1%.

This latest report suggests that consumer spending has begun to stall, likely influenced by the higher interest rates currently impacting the economy. This stagnation, combined with this week’s lower than expected inflation data helps build the case for the BoC to lower the benchmark interest rate in the next few months.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Federal Open Market Committee (FOMC)

In a closely watched decision, the Fed held the US benchmark interest rate steady at 5.5% following its two-day meeting. In his post-meeting press conference, Fed Chair Jerome Powell acknowledged the recent inflation readings were higher than expected. Yet, he reassured that inflation is progressing, albeit on “a somewhat bumpy road,” towards their 2% target.

Looking ahead, despite an uncertain economic outlook, Fed members project the interest rate to fall to 4.6% by year-end, followed by further declines to 3.9% in 2025 and 3.1% in 2026. As always, they emphasized their readiness to adjust rates in response to changes in the economic environment.

The decision to hold rates steady was widely expected. Investors particularly welcomed the Fed’s reiteration of three rate cuts in 2024, suggesting a total decline of 0.75%. This optimism came after recent concerns that higher-than-expected inflation figures might lead the central bank to dial back its rate cut forecasts. While no timeline for the rate cuts was announced, today’s message from the FOMC was well-received by the market.

American market volatility

The CBOE Volatility Index (VIX), often referred to as the market’s fear gauge, has seen a steady decline over the week, closing at 13.06. This represents a 9% drop from the previous week’s figure of 14.41. Currently sitting well below the 20 level, which is commonly associated with high market volatility, the VIX’s latest reading suggests that investor anxiety is comparatively low. This calm in the markets is likely influenced by the Federal Reserve’s renewed expectations to cut interest rates three times within the year.

Apple joins the AI race

In an effort to bolster their artifical intelligence (AI) integration efforts, Apple (NASD: AAPL) has turned to outside sources to jumpstart their efforts. Apple has been in discussions with Google (NASD: GOOGL) about integrating Google’s Gemini AI into the iPhone. They have also been exploring options with OpenAI to potentially use their AI technology, which is the same one that underpins Microsoft’s AI endeavors.

For Google, this could be a significant win. Having their AI on the two most popular smartphones would be quite the achievement. And for OpenAI, working with Apple could further establish their presence in the tech world, pairing them with not just Microsoft but also Apple, two of the titans of the industry. It is interesting to note, Microsoft has a 49% stake in OpenAI, so if Apple decides to go this route, Microsoft will indirectly benefit as well.

This type of partnership would not be without its challenges. Anti trust regulators in the US, the European Union, and to a lesser extent, anti trust regulators in other countries would be concerned about potential dominance in the emerging AI space. Past dealings, like Google paying Apple to make their search engine the default on iPhones, have already drawn scrutiny from regulators. Any new arrangements, especially one involving Google, would likely attract a similar level of attention. And a potential Apple/OpenAI collaboration might also be closely watched, given Microsoft’s (NASD: MSFT) significant investment in OpenAI.

As these discussions are in the early stages, there is still a long road ahead before any concrete decisions are made. It will be interesting to see how these potential partnerships unfold, shaping the future of AI in consumer technology.

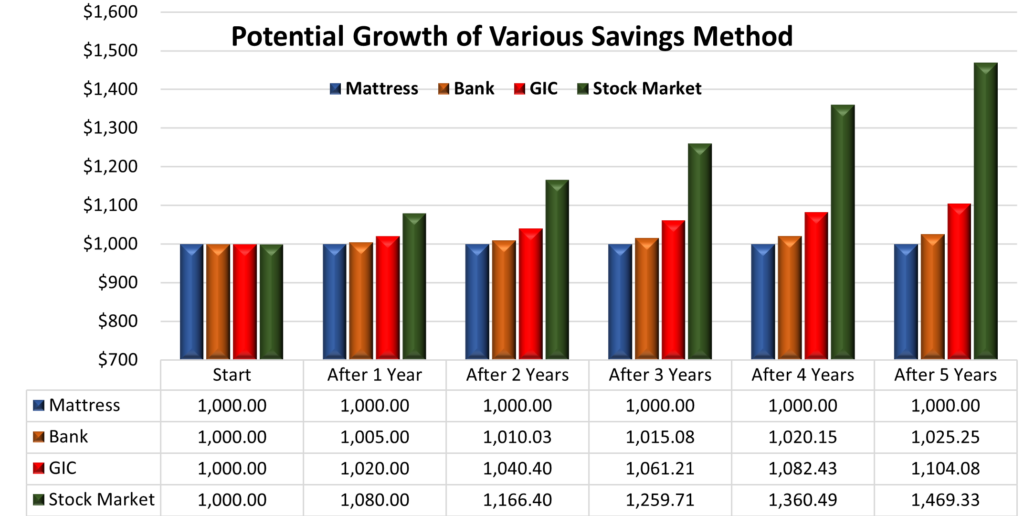

The stock market versus your mattress?

Most mattresses pay 0% interest and are not a very secure way to stash your money. In the event of a robbery or fire the cash could literally go up in smoke and you’ll be left with nothing. Besides a lack of security, a mattress provides no return at all. 😊

While financial institutions (banks, credit unions, etc.) are significantly more secure than a mattress, they currently provide less than 1% interest on standard savings accounts. While they are safer, your money essentially sits idle, losing purchasing power due to inflation. Most financial institutions provide an investment product called a GIC (Guaranteed Investment Certificate) that pays 1 – 4%, depending on the length of term. During the term you may not have access to your money without incurring a withdrawal penalty which could leave you with less than you started.

The other option is to invest in the stock markets which offer the potential for higher returns that outpace inflation. Historically, the stock market has averaged approximately an 8% average annual growth rate. However, unlike the previous options, the stock market fluctuates, and you could experience losses. With that in mind, you can invest in the market in a few ways including mutual funds, index funds, Electronic Traded Funds or by purchasing shares of individual companies directly. The table and chart below illustrate the potential growth of $1,000.00 put into a mattress at 0%, a typical savings account at 1.0%, a GIC at 2% and in the stock market with the average 8% return.

My initial forays into the stock market involved mutual funds. I later transitioned to buying shares of individual companies through a stockbroker and then an online brokerage account. While I do keep some cash in a savings account, I avoid keeping any money under a mattress. 😊

What about Bonds?

While Canada Savings Bonds are no longer available, bonds remain a popular investment option with several types offering different characteristics and risk profiles.

Bonds essentially represent loans you make to a government or corporation. In return, the issuer promises to pay you regular interest and repay the principal amount at maturity. Compared to stocks, bonds generally offer lower potential returns but also lower volatility, making them a good choice for income generation and diversification.

Different types of bonds exist:

- Government bonds: Considered safer due to government backing.

- Corporate bonds: Issued by companies and vary in risk based on the company’s creditworthiness.

- Municipal bonds: Issued by local governments and may offer tax benefits depending on location.

My experience with bonds is limited, but I encourage you to learn more if they align with your investment goals. If you want to learn more about bonds, check out Beginners’ Guide to Investing in Bonds from Wealthsimple, the Securities and Exchange Commission, or check with your financial institution. If you decide to purchase a bond, make sure to speak a reputable financial advisor who can provide you with personalized guidance to meet your needs.

Remember, investing involves risk, including the potential for loss of principal. Past performance is not necessarily indicative of future results. If you are interested in learning more about investing, consult a financial advisor or explore reputable online resources. You can even follow me on my investment journey through my weekly “Weekly Updates” and commentaries. 😊

Weekly Market Review

Monday: investors seem to have gotten over last week’s inflation reports, sending the three major American indexes – the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – higher for the day. Investors now turn their focus to the Fed’s March meeting. It is almost a given the rate will remain unchanged, but investors are waiting for the Fed’s economic projections to see if they still anticipate fewer rate cuts, and when they expect to start lowering the rate. Oil prices rose on lower Middle East exports and signs of growing demand from the world’s two biggest economies – USA and China.

In Canada, the Toronto Stock Exchange Composite Index (TSX) ended lower as investors await the latest inflation data which is expected to be higher than in January. Rising inflation is not good news for companies hoping the BoC will lower the interest rate sooner rather than later. The BoC wants to see consistent signs of inflation falling before it considers lowering the rate. In trading, Healthcare, Industrials and Energy were the only Canadian sectors to end in the green, while Telecommunications Services and Basic Materials (miners and fertilizer manufacturers) dropped the most.

In the US, technology stocks benefitted from buzz around AI created by NVidia’s (NASD: NVDA) annual conference where the company outlined their roadmap for the upcoming year. The surge in big technology companies helped the S&P and the Nasdaq snap 3-day losing skids. In trading, Technology and Consumer Cyclicals had the biggest advances, while Healthcare and Basic Materials were the only American sectors to decline.

Tuesday: the markets got off to a slow start in the morning but rebounded in the afternoon to lift all four indexes into the green as investors await tomorrow’s rate decision from the Fed. The price of oil rose after Ukraine forces attacked Russian refineries leading to possible supply issues.

In Canada, The TSX rose on higher oil prices. On the economic front, the February CPI numbers came in lower than expected, boosting investors expectations of an interest rate cut in the next few months. In trading, Consumer Cyclicals and Energy led the Canadian sectors, while Basic Materials and Utilities suffered the biggest drops.

In the US, the S&P set another new closing high record. It was a day of broad-based gains in the American markets, led by the Energy and Industrials sectors. Telecommunications Services was the only sector to finish lower.

Wednesday: the markets were flat in morning trading awaiting the Fed’s interest rate announcement. Following the announcement the markets surged sending all indexes into the green by the end of the day. The Fed announced they were maintaining the US interest rate at 5.5% and they expected to lower the rate three times in 2024. Oil prices dropped on fears of lower demand.

In Canada, the TSX rose on the news from the Fed, following their American counterparts into positive territory. Lower inflation numbers in Canada has investors thinking the BoC will lower rates in Canada as well. In trading, it was a day of broad-based gains in the Canadian sectors, led by the Technology and Basic Materials sectors. Consumer Staples and Energy were the only two sectors to end lower.

In the USA, investors’ reaction to the good news led to a broad rally that saw all three indexes close at record highs, with the S&P breaking the 5,200 mark for the first time. It was another day of sector wide gains, this time led by Basic Materials and Consumer Cyclicals. Healthcare was the only American sector to decline.

Thursday: the markets continued Wednesday’s rally, fueled by investors feeling the Fed simply delayed rate cuts rather than reduced the number of cuts. Oil prices continue to drift lower as demand continues to falter.

In Canada, the TSX reached a record high close as investors expect the BoC and the Fed to lower interest rates three times this year. In trading, Healthcare and Industrials were the biggest gainers in the Canadian sectors, while Technology, and Telecommunications Services posted the biggest drops.

In the US, lifted by investor optimism of future rate cuts in 2024, all three indexes set record highs for the second straight day. The S&P set a closing record for the 20th time this year, and the DJIA set another as it approached the 40,000 mark. In trading, Financials, and Industrials advanced the most, with Telecommunications Services and Utilities declining the most.

Friday: it was a mixed day in the markets, with only the Nasdaq able to end in positive territory. Oil prices have continued to drop on demand concerns after topping the US$ 80 mark earlier in the week.

In Canada, the TSX ended the day slightly lower as investors took some profits. However, it was not enough to prevent the index from notching a sixth straight weekly win, its longest winning streak since December 2020. In trading, Healthcare, Consumer Staples, and Industrials were the only Canadian sectors to advance, with Telecommunications Services and Consumer Cyclicals suffering the biggest declines.

In the US, the Nasdaq set a new closing high buoyed by investor optimism of rate cuts later this year. Meanwhile, the DJIA and S&P slipped back as investors likely took profits after both posted record highs yesterday. In trading, the Technology and Utilities sectors were the only American sectors to end in the green, while Financials and Telecommunications Services dropped the furthest into the red.

Weekly Market and Portfolio Review

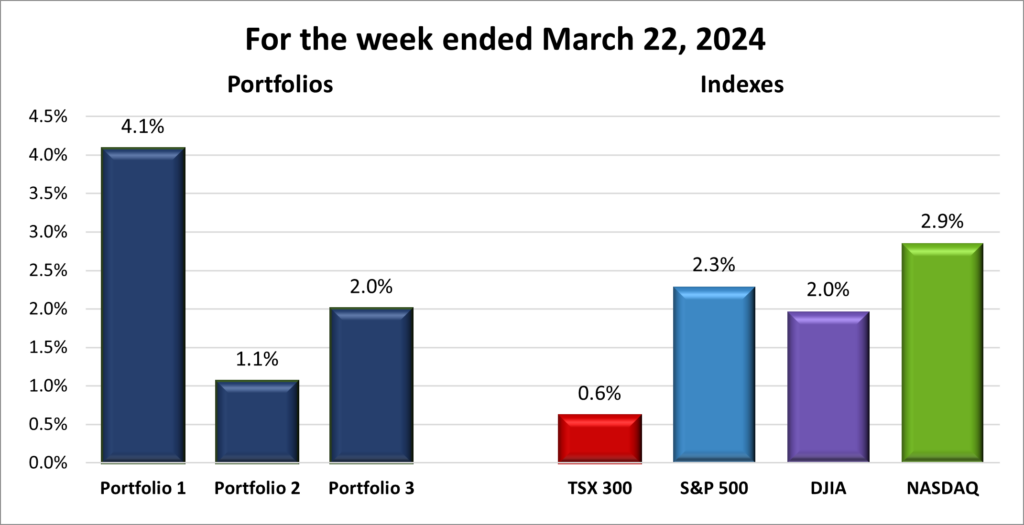

For the week, the TSX (SPTSX) gained 0.6%, the S&P 500 (SPX) rose 2.3%, the DJIA (INDU) advanced 2.0% and the Nasdaq (CCMP) surged 2.9%.

| Index | Weekly Streak |

| TSX: | 6-week winning streak |

| S&P: | 1-week winning streak |

| DJIA: | 1-week winning streak |

| Nasdaq: | 1-week winning streak |

![]() This past week saw a strong performance across North American markets, with each of the four major indexes not only ending the week in positive territory, as illustrated in the accompanying chart. They also set new all-time highs along the way – a testament to the ongoing bullish sentiment.

This past week saw a strong performance across North American markets, with each of the four major indexes not only ending the week in positive territory, as illustrated in the accompanying chart. They also set new all-time highs along the way – a testament to the ongoing bullish sentiment.

Fueling this rally was the eagerly awaited conclusion of the Fed’s FOMC meeting. Fed Chair Jerome Powell’s confirmation of projections for three interest rate cuts by year’s end came as a relief to investors, who had been concerned about potential reductions in anticipated cuts. This announcement has set the stage for a June meeting rate cut, sparking optimism among analysts and investors alike.

This rally was characterized by its overall breadth, marking a departure from last year’s rally where the market gains were predominantly driven by the ‘Magnificent 7’ companies. This shift towards a more inclusive market rally indicates a healthier sentiment, where growth is more evenly distributed across various sectors, enhancing market stability.

Somewhat overlooked, the TSX achieved an all-time high this week, boasting a nearly 7% increase since mid-February—a performance that outshines its American counterparts for the same period. Key contributors to this climb included Canadian Natural Resources (TSE: CNQ) and Shopify (TSE: SHOP), while TD Bank (TSE: TD) and BCE (TSE: BCE), among others, acted as a drag on the index.

I hope this bullish sentiment continues well into the future. 😊

| Portfolio | Weekly Streak |

| Portfolio 1: | 12-week winning streak |

| Portfolio 2: | 1-week winning streak |

| Portfolio 3: | 1-week winning streak |

![]() As shown in the chart below, this week brought encouraging gains across all my investment portfolios. Portfolio 1 outperformed all other portfolios and indexes, without any significant winners or losers. Notably, stocks like Nvidia, with its US$ 34.47 increase, demonstrate how minor percentage gains in high-value stocks can significantly influence overall portfolio performance.

As shown in the chart below, this week brought encouraging gains across all my investment portfolios. Portfolio 1 outperformed all other portfolios and indexes, without any significant winners or losers. Notably, stocks like Nvidia, with its US$ 34.47 increase, demonstrate how minor percentage gains in high-value stocks can significantly influence overall portfolio performance.

Portfolio 2 finally saw a win, albeit the smallest among the three. Its standout was Hammond Power Supply (TSE: HPS.A), which surged 10%. This portfolio’s focus on dividend-paying rather than growth stocks likely tempered its gains relative to the others.

Reviewing Portfolio 3, I noticed a general uptrend in company values, yet no standout winners. I wondered what was preventing the portfolio from posting a similar percentage gain to Portfolio 1 when I came across Alvopetro Energy (TSXV: ALV). The share price had fallen 28% during the week, explaining the difference in performance.

With the Fed’s confirmed expectation to cut US interest rates three times this year, investor optimism is high. I’m hopeful that this positive momentum is just the beginning of a winning streak for all three portfolios. 😊

Companies on the Radar

While no new companies caught my eye this past week for inclusion on my investment radar, I’ve decided to remove Palantir Technologies (NYSE: PLTR) from my watchlist. My mixed feelings about their facial recognition technology played a big part in this decision. Recognizing both the potential benefits and the ethical concerns it presents, I found myself grappling with a key investor question: “Would I be proud to own a part of this company?” Since I could not answer with a firm ‘yes,’ and considering the many other investment opportunities out there, I have opted to move on.

While no new companies caught my eye this past week for inclusion on my investment radar, I’ve decided to remove Palantir Technologies (NYSE: PLTR) from my watchlist. My mixed feelings about their facial recognition technology played a big part in this decision. Recognizing both the potential benefits and the ethical concerns it presents, I found myself grappling with a key investor question: “Would I be proud to own a part of this company?” Since I could not answer with a firm ‘yes,’ and considering the many other investment opportunities out there, I have opted to move on.

For now, the radar list consists of these four companies:

- Celestica Inc. (TSE: CLS), a medium sized Canadian company that manufactures electronic products and provides supply chain services to companies around the world.

- Equitable Bank (TSE: EQB), a mid sized Canadian bank, considered Canada’s 7th bank, that provides financial services to consumers and businesses.

- Lumine Group (TSE: LMN), a young Canadian mid sized company that acquires communications and media software companies and then strengthens and grows those companies.

- Evolution AB (OTCM: EVVTY), a Swedish company that provides live casino solutions for global gaming operators.

Please keep in mind that these are only companies that have piqued my interest. This is not a recommendation or financial advice. You should do your own research or contact a professional before making any investment decisions.

The Radar Check was last updated March 22, 2024.

NOTE: Morningstar and Thomson-Reuters analysis is unavailable for Evolution from my usual sources because the company’s home stock exchange is the Nasdaq Stockholm in Sweden. While it is possible to invest in Evolution through the Over The Counter Market, there is no analysis similar to the data available for companies traded on the major North American stock exchanges (Toronto Stock Exchange, New York Stock Exchange, and Nasdaq Stock market). The Analysts Rating and Price Target for Evolution are from Yahoo! Finance, under the Analysis tab once you have searched for the ticker.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended March 22, 2024: UP ![]()

- Nvidia held their annual GTC developer conference this past week where they unveiled their latest chips and software updates. The company expects to start shipping their new B100 Blackwell chips later this year.

- Alphabet’s Google received a € 250 million euros from France’s competition watchdog for using content from French publishers and news agencies without telling them. As part of the settlement, Google will not contest the facts.

- The US Department of Justice are suing Apple, claiming the company monopolized the smartphone market, driving up prices for consumers. The DOJ says Apple violated anti trust laws by stopping competitors from accessing the features found on iPhones. In the European Union (EU), regulators are investigating Apple to ensure that the company complies with the EU’s Digital Markets Act.

Activity

Sold: Cargojet Inc. (TSE: CJT) I initially invested in Cargojet in 2018, recognizing air freight as an expanding sector. The investment proved exceptionally fruitful during the Covid-19 pandemic, as the surge in e-commerce demand led to an increased need for Cargojet’s overnight shipping services across Canada. This drove the company’s share price to an all-time high in November 2020. However, since reaching that peak, the share price has declined by over 50%, a trend clearly depicted in the five-year chart below. This downtrend prompted me to reconsider my position. The recent market rally presented an opportune moment to exit with a decent profit, a decision I am pleased with given the circumstances. 😊

Sold: Tesla, Inc. (NASD: TSLA) In January 2021, I invested in Tesla, recognizing its leading position in the electric vehicle (EV) market, its expanding customer base, and its diversification into energy solutions. Despite reservations about Elon Musk’s public statements and actions, his pioneering role in the EV industry was undeniable.

However, my investment thesis has changed. My initial optimism has been dampened by several factors: Tesla’s sales momentum is slowing; the broader EV market is experiencing a slowdown in sales growth; and Mr. Musk’s assertion that Chinese EV manufacturers “will pretty much demolish most other companies in the world” has added a layer of uncertainty. Additionally, Mr. Musk’s extensive involvement in his other ventures has led me to question his focus on Tesla’s day-to-day operations.

By selling my shares in Tesla, even at a loss, allows me to invest that money elsewhere in companies I feel will do better in the long run.

Sold: kneat.com Inc. (TSE: KSI) I made several investments in kneat.com across all three portfolios, starting in May 2019, with three additional investments from December 2019 through January 2020, as the price rose to C$3.00 a share. Since then, however, the share price has bounced around the C$ 3.00 level. This lack of movement led to a waning interest in the company. To confirm I was not missing any critical information, I reviewed the financial statements and noticed that, despite increased sales, net income, earnings per share, and free cash flow were all declining. Additionally, the company’s long-term debt had increased over the past year. It appeared the company had not capitalized on its increased sales effectively.

Given my reduced interest and the company’s disappointing financial performance, I viewed the recent rally as an opportune time to divest all my stakes in the company. Fortunately, I was able to make a decent profit in all three portfolios. 😊

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Decisive Dividend Corp (TSE: DE)

US $

Home Depot Inc. (NYSE: HD)

Quarterly Reports

Decisive Dividend Corporation

Fourth quarter 2023 financial results on March 20, 2024

Portfolio 2

Portfolio 2 for the week ended March 22, 2024: UP ![]()

- Alimentation Couche-Tard (TSE: ATD) announced they have signed a deal with Davids Tea Inc (TSXV: DTEA) that will make David’s Tea the exclusive supplier of a premium sachet format tea to ATD’s Circle K and Couche-Tard convenience stores.

In other Alimentation news, former Canadian Prime Minister Stephen Harper has been appointed by the Board of Directors as a new Board member. - The Bank of Nova Scotia’s (TSE: BNS) Wealth management division received six Euromoney Private Banking Awards 2024, including Canada’s Best Private Bank for Sustainability and awards for five other countries in Latin America and the Caribbean.

Activity

Sold: kneat.com Inc. See explanation under Portfolio 1.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSE: DIR.UN) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

Mitek Systems, Inc.

Fourth quarter 2023 financial results on March 19, 2024

Alimentation Couche-Tard Inc.

Third quarter 2024 financial results on March 20, 2024

Portfolio 3

Portfolio 3 for the week ended March 22, 2024: UP ![]()

- Microsoft announced they have appointed DeepMind co-founder Mustafa Suleyman as the head of their new consumer AI unit. They also hired several people from DeepMind.

- Brookfield Asset management (TSE: BAM) announced that Brookfield’s Hadley Peer Marshall will succeed chief financial officer Bahir Manios, effective May 31. He was previously the co-head of Brookfield’s infrastructure debt and structured solutions. Prior to that he was an executive at Goldman Sachs.

- The fourth quarter report for Alvopetro Energy was not a good one. Revenue was down 10%, fourth quarter profits dropped 87%. They also estimated lower production levels in the next quarter, leading to a 36% reduction in the quarterly dividend, from US$ 0.14 to US$ 0.09. Ouch!

Activity

Sold: kneat.com Inc. See explanation under Portfolio 1.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

Alvopetro Energy Ltd.

Fourth quarter 2023 financial results on March 19, 2024