Items that may only interest or educate me ….

Canadian data, Strength of the US dollar, Growth of EV production, but first….

While investing did not bring the joy it did the past two Christmases, may Santa provide you one or two stock tips that become huge winners.

It was a busy week of reports from Statistics Canada. First, they announced Canadian retails sales rose by 1.4% from September to October, but they expect to see a 0.5% decline in November. October sales were the best in five months, but they still came in lower than expected by analysts. Most of the October sales increases were a result of higher prices, especially at the gas pump, rather than consumers buying more products. The lower retail sales are not a good sign for the economy because it indicates the high inflation (goods cost more), and higher interest rates (borrowing cost more) are having a negative impact on Canadian shoppers. That does not bode well for retailers that depend on holiday shoppers to boost their revenues.

Next, Statistics Canada announced the Canadian Consumer Price Index (CPI) for November rose 6.8%, missing analysts forecast of 6.7%. However, it was still down from October’s 6.9%. The core CPI (CPI without the food and fuel costs) grew 5.4%, slightly higher than October’s 5.3%.

The good news is inflation appears to be slowly but surely drifting downward. The bad news is inflation is still too high despite the record pace of increases, opening the door for another increase to the Canadian benchmark interest rate. Analysts are anticipating a 0.25% increase in January. The Bank of Canada (BoC) has said the size of future interest rates will be determined by the data so we will have an idea what to expect when the next Canadian CPI comes out in January.

American based companies with international operations have been feeling the sting of a strong US dollar. The strength of the US dollar is closely tied to the direction of interest rates, and in 2022 US interest rates rose at their fastest pace in 40 years. After Russia’s invasion of Ukraine, investors around the world looked for a safe haven for their money. Many turned to the US dollar thanks to the higher interest payments on US Treasuries, a product of the US Federal Reserve’s interest rate hikes to fight inflation, and because it is considered the most stable of all currencies. While the US dollar surged, other world currencies tumbled, including the Canadian dollar.

As a result of a strong US dollar, the revenues and profits of US multinationals suffer. When an American company rolls up all the revenues from its foreign branches, all the foreign currencies must be converted to the US dollar. The higher US dollar means the foreign currency cannot purchase as many US dollars. The foreign currencies end up being converted to fewer US dollars which appears on the financial statements as lower revenues and lower overall profitability.

For example, say we have a US company with a Canadian subsidiary. Let us call the US company ‘Parent A’ and the Canadian subsidiary ‘Sub A.’ Sub A has C$ 1 million of revenues in each of the last two years. Each year this money must be converted to the currency of the country where Parent A is located (the US in this example).

In the table below, you can see the impact of a weaker Canadian dollar against the US dollar. When Parent A received the C$ 1 million from Subsidiary A, in December 2021, after converting it to US dollars (using the BoC rate of 0.7727), Parent A would have received US$ 772,700 of revenues from Sub A. This year (December 2022), when Parent A received the C$ 1 million in revenues from Sub A, Parent A would receive US$ 732,400 of revenues from Sub A, after converting from Canadian dollars to US dollars (using the BoC rate of 0.7323.)

| Year | Canadian Dollars | Exchange Rate | US Dollars |

| 2022 | 1,000,000 | 0.7342 | 734,200 |

| 2021 | 1,000,000 | 0.7727 | 772,700 |

On Parent A’s Income Statement for 2022, revenues from Sub A would be reported US$ 40,300 lower than what was reported on the Income Statement for 2021. Despite the Canadian revenues being the same for both years, the strength of the US dollar has made it more expensive to buy US Dollars and therefore the same amount of Canadian dollars buys less US dollars. Which in turn appears as lower revenue reported by Parent A.

Now imagine if Parent A had a dozen more subsidiaries located throughout the world. Each of those subsidiaries would have to convert their revenues and earnings into US dollars, many at worse exchange rates than converting Canadian to US dollars. This would cause the big US multinational corporations to see their sales and profits get hammered by currency exchanges. Some analysts estimate the strong US dollar reduced third quarter corporate revenue growth by 4%.

As a strong US dollar leads to lower overall revenues and profits for a US based multinational, a weaker US dollar against the Canadian dollar has the opposite effect. A weaker US dollar would lead to an increase in revenues and earnings from a Canadian subsidiary because the Canadian dollar would be able to buy more US dollars which would show up as higher numbers in the financial statements.

While a strong US dollar is great for American citizens through greater buying power, you can see how its not so great for American multinationals because of lower revenues from foreign offices. When you see a lower, or higher, revenue being reported by any American company that does business abroad, make sure to check the notes to see if foreign currency exchange accounts for the unexpected gain or loss in revenues. Losses or gains due to currency exchange is one area companies have little to no control over.

What started out as a trickle of electric vehicles (EVs) has turned into a steady stream. Tesla (NASD: TSLA) is the name most people recognize, but today there are many EV manufacturers. Well known names such as Hyundai (OTC:HYMTF), General Motors (NYSE:GM), Ford (NYSE:F), and Volkswagen (OTC: VWAGY), together with automotive upstarts such as Rivian (NASD:RIVN), Lucid (NASD:LCID) and numerous Chinese companies, are pouring more than $1 trillion into the move from internal combustion engines to electric vehicles that are controlled by software.

Despite all the competition for EV dominance, Tesla still is the leader in EV sales in North America with over 50% of the market. However, that dominance should fade as GM and Ford roll out more EV models, including trucks and SUVs. The established car companies should be able to make inroads on Tesla’s market dominance easier than the newcomers thanks to their years of experience and very deep pockets. That gives them a big advantage when it comes to scaling up production.

If intense competition was not enough for the start-ups, the past year has not gone well for them. Inflation, higher interest rates and supply chain problems have all had an impact on these companies. Inflation has made components more expensive. More cash has been required to service their debt thanks to the higher interest rates. And supply chain challenges have made it harder to fill their sales orders, leading to lower revenues. Put these together and their quarterly earnings have not inspired investors.

As a result, many of the high-flying start-ups of 2021 have seen their market value plunge dramatically. For example, Rivian and Lucid are each down almost 80%, and Chinese EV company NIO (NYSE:NIO) is down 60%. These losses make Ford’s 40% and GM’s 35% market capitalization losses pale by comparison.

Going forward, inflation and higher interest rates will be around for most of 2023. However, many of the established automakers will debut many of their new EV models. Mass production should begin to ramp up in the later half of 2023 and be in full swing by the end of the year. It will be interesting to see how many of the new companies can survive the current economic environment as well as stiff competition from the incumbents who will not go silently into the night.

Before our thoughts turn to visions of sugar plums, lets see if the markets gave the portfolios a present or a lump of coal….

Weekly Market Review

Monday: The losing streak for all four major North American indexes reached four today with a sell off that spanned every sector in both Canada and the US. The only bright spot was the price of oil ended higher, but barely. The big driver of the market was fear of a recession in 2023, particularly in the world’s largest economy, the US. Not a great way to start the week. ☹

In Canada, on the Toronto Stock Exchange Composite Index (TSX), the Consumer Staples and Energy sectors dropped the least of the Canadian sectors, while the Utilities and Healthcare sectors fell the most.

In the US, the Nasdaq Composite Index (Nasdaq), the S&P 500 Index (S&P), and the Dow Jones Industrial Average (DJIA) all ended lower. The Energy sector just missed getting out of the red by 0.01%. Leading the retreat of the S&P sectors were the interest sensitive Consumer Cyclicals and Technology sectors.

Tuesday: All four indexes got back on the winning track after the US dollar weakened against other major currencies. A weaker dollar means foreign currencies have more purchasing power against the US dollar. For Canadians, it means the Canadian dollar buys more when you visit the US. For us Canadian investors it means it does not cost us as much to buy shares of US companies.

In Canada, investors prepared for tomorrow’s Canadian Consumer Price Index (CPI) report. On the TSX, the Basic Materials (mining companies and fertilizer manufacturers) sector and the Energy sector had the best day of the Canadian sectors, while Consumer Cyclical and Healthcare had the worst day.

In the US, investors were worried about lower spending during the holiday season, leading to poor performance in the retail shopping sector. In the markets, the Energy and Basic Materials sectors led S&P surge that saw all S&P sectors end higher except for the Consumer Cyclicals sector.

Wednesday: Another day in the win column for all for all four indexes thanks to higher oil prices and signs of upbeat consumer confidence going into the Christmas break. In Canada, the Canadian CPI for November came in at 6.8% higher than November 2021, slightly less than the October rate of 6.9%, indicating inflation in Canada was cooling. In trading, all Canadian sectors ended higher, led by the Energy and Consumer Cyclical sectors, with the Consumer Staples and the Telecommunications Services sectors bringing up the rear.

In the US, investors seem to have shaken off last week’s comments from the Fed about ongoing inflation and continue to expect inflation to start coming down in 2023. Consumer confidence has reached its highest point in eight months. Strong quarterly earnings updates from a few big US multinationals did not hurt either. In trading, it was a broad-based rally as all the S&P sectors ended in the black today. Energy and Industrials sectors performed the best while Consumer Staples was the only sector not to gain at least 1%, missing by 0.03%.

Thursday: The stock markets fell sharply in the morning, before regaining some of the ground in the afternoon. Unfortunately, it was not enough as all four indexes ended the day lower. The main story was lower unemployment in the US, which sparked concerns of ongoing aggressive interest rate hikes.

In Canada, thanks to fears of higher interest rates, the TSX gave back gains from the previous two days. Interest sensitive Canadian Technology and Energy sectors had the biggest drop in a broad-based retreat on the TSX. Telecommunications Services and Consumer Staples sectors dropped the least.

South of the border, a recession is in the process of replacing inflation as what concerns investors the most. The US Department of Labor’s recent unemployment data came in lower than expected. As long as there is high employment and inflation remains high, the Fed will keep ratcheting up the US benchmark interest rate. In the US markets, the S&P’s Telecommunications Services was the only sector in the black, avoiding the S&P sectors being shut out of the win column. The interest sensitive Technology and Energy sectors had the worst day.

Friday: The markets were up and down like a yoyo today. The day started with a plunge thanks to ongoing concerns about aggressive interest rate hikes tipping Canada and the US into recessions in 2023. During afternoon trading, good economic news emerged out of the US and the indexes started climbing into positive territory on. The markets were further boosted by news Russia plans to cut their output of crude oil in response to price caps imposed by western governments, pushing oil prices, and the market, higher.

In Canada, thanks to higher oil prices, the TSX ended high enough today to pull the TSX into the black for the week. The Canadian Energy and Utilities sectors led the advance while Technology and Healthcare held the TSX from larger gains today.

In the US, the Commerce Department reported inflation continues to cool. Unfortunately, inflation has not gone down enough to convince the Fed to lower the size of their upcoming interest rate hikes. The Energy and Utilities sectors led the S&P sectors higher while only the Healthcare sector failed to gain ground today.

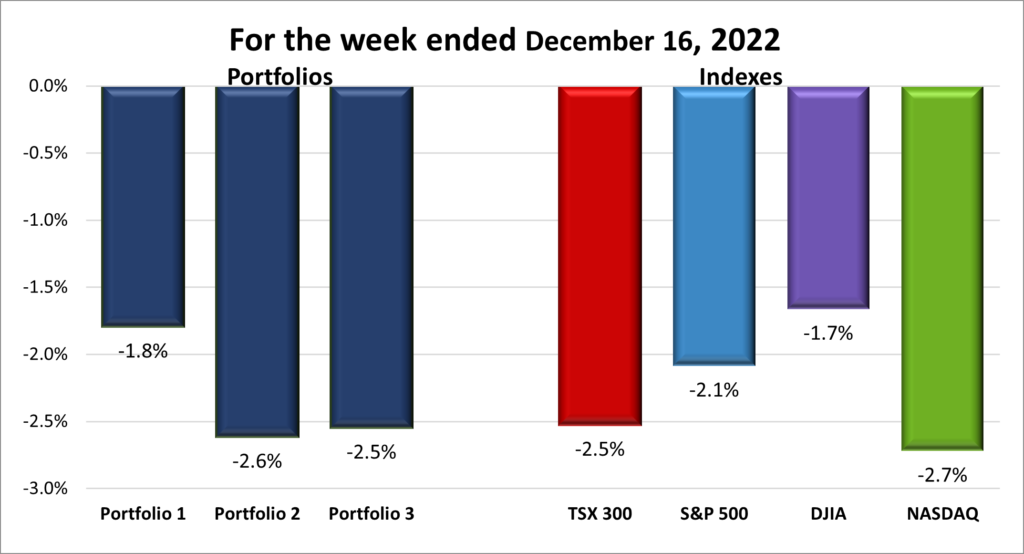

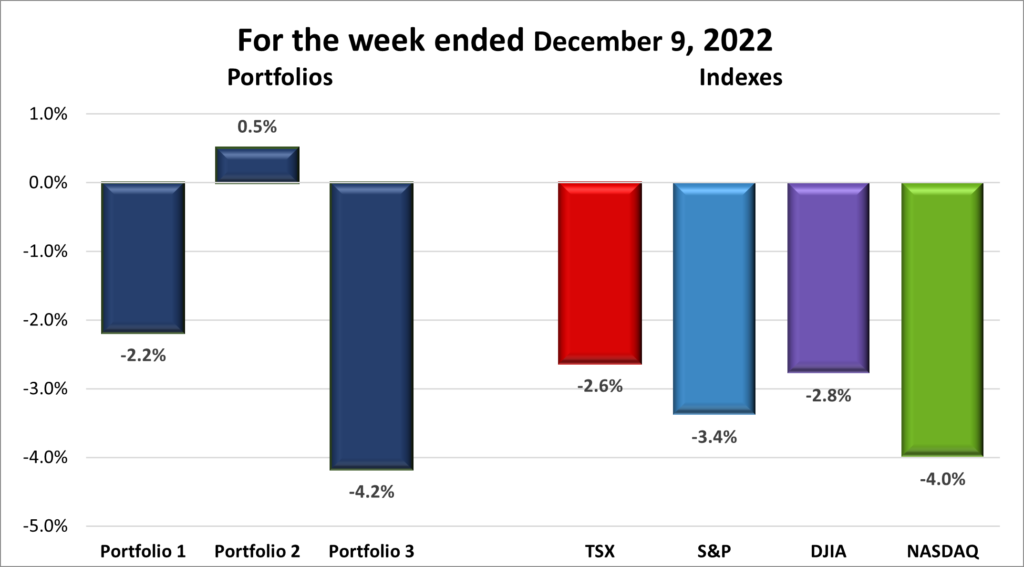

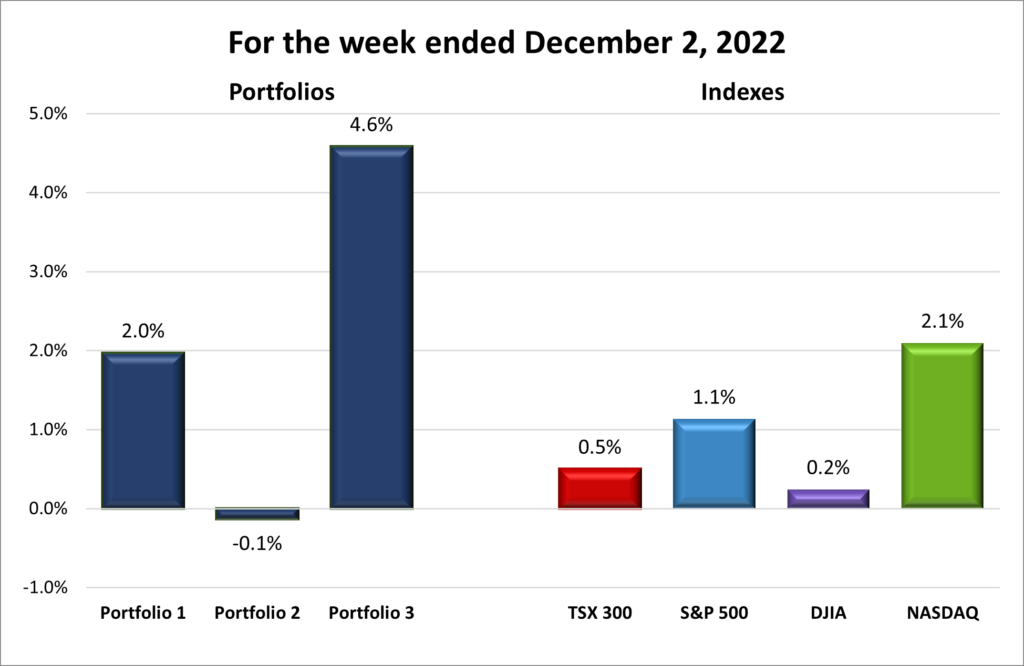

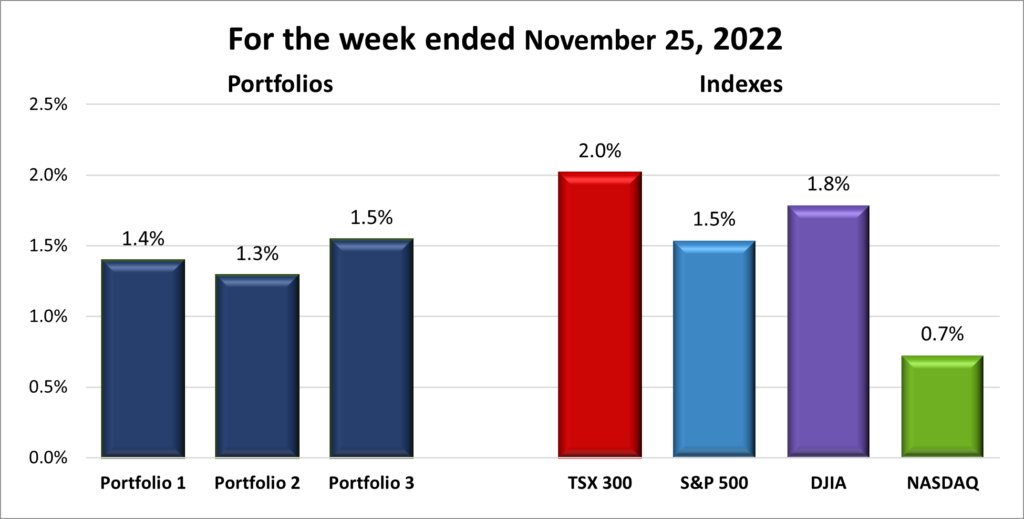

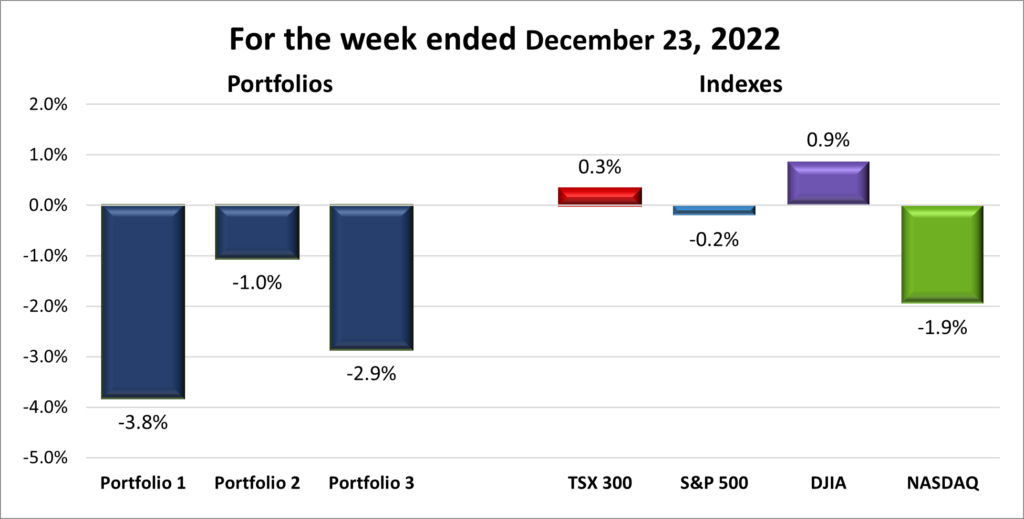

A split decision this past week, with two indexes ending in the black and two ending in the red. For the week, the TSX gained 0.3%, the S&P 500 lost 0.2%, the Dow advanced 0.9% and the Nasdaq dropped 1.9%.

Weekly Portfolio Review

It was a roller coaster ride through the markets this week, before a last-minute rally was able to push the TSX and the DJIA into the black. Once again higher interest rates weighed down the growthier Nasdaq and the S&P.

With the indexes all lower, it appears the Portfolios received a piece of coal from Santa this past week. Once again, the interest sensitive technology companies, were hit the hardest as investors are now looking for companies with profits and minimal debt, something start-ups typically do not have. All three Portfolios are growth oriented, but as you can see in the chart below, Portfolios 1 and 3 contain a higher ratio of high growth companies. Whereas Portfolio 2 has a few growth stocks but it has a higher ratio of mature dividend paying companies.

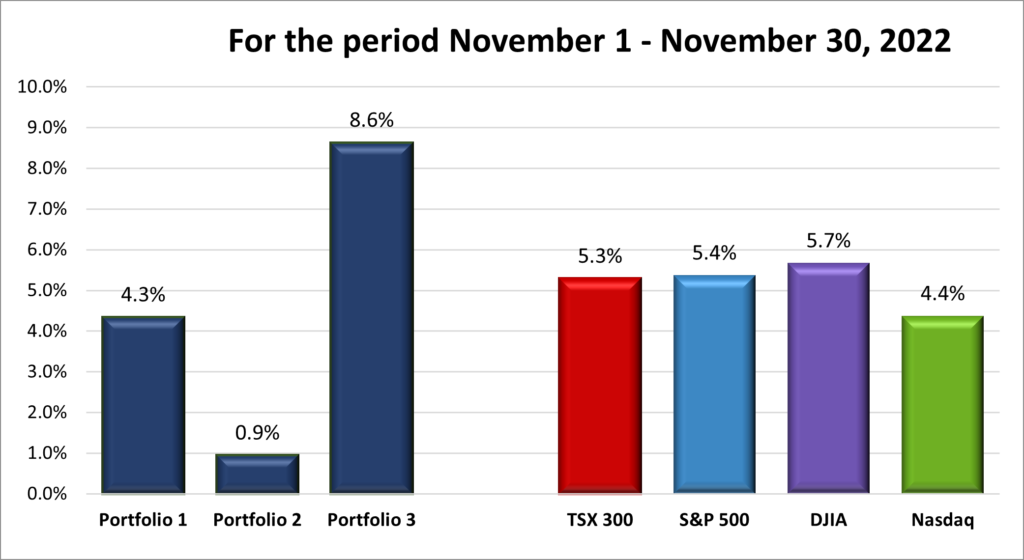

The three portfolios have ridden out the inflation fears of 2022, albeit not very well. Next week we will see how the Portfolios made out in 2022. In 2023 I suspect I will find out if each portfolio can survive a recession, which was not a consideration when they were being built.

Companies on the Radar

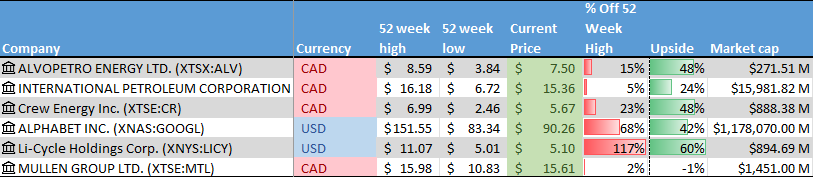

All is quiet on the radar the week before Christmas. The same four companies listed below remain front and centre.

- Alvopetro Energy (TSXV:ALV): A Canadian natural gas company developing natural gas projects in Brazil.

- International Petroleum (TSX:IPCO): A Canadian company with oil and gas assets in Canada, Malaysia, and France.

- Crew Energy (TSX:CR): A Canadian oil and gas company with interests in British Columbia.

- Alphabet (NASD:GOOGL): The leading online search engine and advertising company, dominant mobile operating system.

The Radar Check was last updated December 23, 2022.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended December 23, 2022: DOWN ![]()

- Amazon (NASD:AMZN) was awarded a 5-year contract to supply the US Navy with cloud services from their Amazon Web Services unit. The deal is worth almost US$ 724 million.

Amazon’s share price hit pre pandemic levels, effectively erasing all its gains pandemic gains. When I bought it a few weeks ago, I knew it would go lower but not this much lower (and falling). ☹ I still think it will bounce back once the markets get out of their funk. Unfortunately, I’ve no idea when that might be.

The Court of Justice of the European Union (CJEU) has opened the door for European national courts to hold Amazon responsible for advertising counterfeit products, in this case Christian Louboutin shoes. The CJEU said the way Amazon presents the shoes does not clearly delineate between shoes offered by Louboutin and shoes offered by third party sellers. This confusion may cause online shoppers to believe Amazon is benefitting from the sale of the counterfeit shoes. Hopefully, this will put an end to Amazon mixing brand name products with knock off products. - Last week FuboTV (NYSE:FUBO) was the victim of a cyber attack that came at a most inopportune time. The attack came during the France v Morocco World Cup semi final, preventing many Fubo customers from accessing their accounts to watch the game. It took Fubo two days to fully restore all the accounts, much too late to watch game but more than enough to catch a lot of flack on social media and see its share price punished.

- Slowing demand for Tesla’s electric vehicles, especially in China, has the company set to announce another round of layoffs as well as a hiring freeze. Tesla has also started offering discounts in the US on selected models, and free supercharging for up to 10,000 miles for cars received in December.

Tesla CEO Elon Musk promised not to sell any more of his Tesla shares for two years to calm investors. Mr. Musk had previously sold US$ 40 billion worth of Tesla shares in late 2021. Unfortunately, he said this before, only to sell an additional US$ 15 billion worth of Tesla shares this past spring. It would be nice to have that amount of money available, however, nothing inspires confidence like the founder/CEO selling that many shares. ☹ - To avoid actions from Germany’s cartel office, Alphabet’s Google division updated their news service. All the changes are for the benefit of publishers. Some will be implemented immediately while others will be rolled out gradually.

YouTube has signed a multi-year deal with the NFL to be the exclusive streamer of the NFL’s Sunday Ticket program starting next season. YouTube will pay US$ 2 billion a year to add the NFL to their YouTube TV and YouTube Primetime channels. The NFL now has streaming deals with Amazon (Thursday night football) and YouTube, to go along with broadcast deals from NBC, CBS, and Fox. For each game they are generating two income streams, broadcast, and streaming. Well done NFL! 😊

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

No C$ dividends this past week.

US $

NVIDIA Corp (NASD:NVDA)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended December 23, 2022: DOWN ![]()

- The week did not start well for the House of the Mouse (NYSE:DIS) which saw its share price drop almost 5% on Monday thanks to a weak box office opening by their new “Avatar: The Way of Water” movie. The film brought in US$ 134 million but was expected to bring in US$ 135 – US$ 175 million.

- As part of the process of reopening their Keystone pipeline, TC Energy’s (TSX:TRP) had to submit a plan on what work they were doing to fix the problem, clean up the spill and prevent future spills. This plan was approved by the US Pipeline and Hazardous Materials Safety Administration (PHMSA). TC Energy also sent the damaged segment of the pipeline for metallurgical testing. The spill has become the largest pipeline spill in the US since 2013.

- Guardant Health (NASD:GH) has teamed up with the Susan G. Komen (R) organization to develop clinical studies to help identify early-stage breast cancer patients who are at substantial risk of the cancer reoccurring. The data from these clinical studies will go towards improving Guardant’s Guardant Reveal test for detecting “minimal residual disease in patients with early-stage breast cancer.”

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended December 23, 2022: DOWN ![]()

- Microsoft’s (NASD:MSFT) climate innovation fund recently invested in Group14 Technologies, a private company. Group14 claims it makes better batteries for electric vehicles (EV) and energy storage solutions. The company claims its silicon anode material is more efficient than the standard graphite technology, allowing for better ultra fast charging. Microsoft is one of many companies placing bets on companies in the EV sector as the US moves to renewable energy solutions.

- Enghouse Systems (TSX:ENGH) has agreed to purchase cloud-based video technology company Qumu (NASD:QUMU) in an all-cash deal. This should enhance Enghouse’s enterprise video capabilities.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

No quarterly reports this past week.

As expected, the US Federal Reserve (Fed) did indeed ease off the gas pedal of higher interest rates, however slightly. In an effort to keep a recession at bay while reigning in inflation, the Fed announced an increase of 0.5% to the US benchmark interest rate, bringing the interest rate to 4.25%. Considering the previous four increases were 0.75%, a 0.5% increase was a relief. Another hike for sure, but at least its lower than the previous four increases. The Fed also stated it was no longer “as important how fast we go” indicating additional increases but not as big as recent increases.

As expected, the US Federal Reserve (Fed) did indeed ease off the gas pedal of higher interest rates, however slightly. In an effort to keep a recession at bay while reigning in inflation, the Fed announced an increase of 0.5% to the US benchmark interest rate, bringing the interest rate to 4.25%. Considering the previous four increases were 0.75%, a 0.5% increase was a relief. Another hike for sure, but at least its lower than the previous four increases. The Fed also stated it was no longer “as important how fast we go” indicating additional increases but not as big as recent increases.