Fractional shares….

Despite slumping the week ended August 26, the S&P 500 Index (S&P) had bounced back 15% since its June low and all 11 sectors of the index have been in the black since the start of the third quarter (July 1). Bet you did not know that was the S&P’s best start to a third quarter since 1932? I did not.

A mini summer rally led some to believe the tough times of the first half of 2022 were over. However, analysts and investors were split over whether the market had reached a bottom in June, or if the rally was a bear trap. Going into the start of this past week (August 29), despite the July rally, the S&P remains down about 13% (a market correction), and the Nasdaq is still down more than 20% (a bear market).

Since US Federal Reserve (Fed) Chair Jerome Powell’s speech on August 26, reiterating the Fed’s determination to increase interest rates in their fight against inflation, even in the face of a slowing economy, the S&P has plunged more than 5%. Since then, the markets have turned bearish, and the summer rally is now unravelling as we head into what has historically been the toughest month for the US stock market.

September has been the worst month for the S&P since 1945, averaging a 0.6% loss. One reason is fund managers are back from summer vacations and are looking to polish up their fund’s performance numbers for the end of the third quarter (September 30) and tend to get rid of underperforming companies. This year, as we head into September there does not appear to be much chance the markets will buck that trend. The main reason is the Fed will continue hiking interest rates and keep them above their target inflation rate of 2% longer than anticipated. This in turn will have an adverse effect on consumer demand.

Adding more fuel to the Fed’s fight against inflation, US labour demand in July showed no signs of cooling as job openings rose, and consumer confidence rebounded strongly after falling from May through June. When millions of Americans continue to quit their jobs, this is viewed as a sign of confidence in the labour market. Thanks to a continued demand for workers, salaries have gone up which in turn has led to an ongoing rise in consumer spending, two items that fuel inflation. Unfortunately, the US jobs data released on September 2 was a mixed bag. Job openings continued to rise, although at a lower pace, but wage increases slowed down and unemployment rose indicating more people were returning to the workforce. Prior to the jobs report, analysts believed the Fed was likely to raise the interest rate by 0.75% for a third time. After the jobs report showed signs of a slowing labour market, investors are hoping this could ease the pressure on the Fed to deliver another big rate hike. Unless September data shows the US economy and inflation slowing, I think the Fed will remain aggressive in their next rate increase.

In Canada, the Bank of Canada (BoC) is the Canadian equivalent of the Fed. Like the Fed, its primary mission is to keep inflation in the 1% – 3% range, typically 2%. With inflation in Canada currently over 7%, analysts believe the BoC will make a fourth increase of 0.75% in their fight against rampant inflation. This would leave Canada’s benchmark interest rate at 3.25%, full 3% higher than it was in March 2022. Ouch! Not good for those with loans, mortgages, or companies with significant debt.

Whether you invest in the Canadian or American markets, we are in for higher interest rates and it appears we are in for more tough times. ☹

Enough of about what might happen, lets look at what did happen this past week ……

Weekly Market Review

Monday: The stock markets picked up where they left off on Friday – heading lower. Investors were still digesting comments by the head of the US Federal Reserve (Fed), and the impact of higher interest rates on corporations, especially the high growth, technology companies. All four major North American Indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – ended lower. Higher oil prices helped soften the decline as the Energy sector was the best performer in each country. The Utilities sector, traditionally a defensive sector, was the second-best performing sector in both countries. It was not a good day for growth companies.

Tuesday: The four Indexes kept their respective losing streaks alive for a third straight day. Canada’s TSX fell the most in a sell off that touched every sector. The Canadian Energy and Basic Materials sectors fell the hardest, while Consumer Staples (aka Non-Cyclical Consumer Goods & Services, a defensive sector) was the only sector to gain ground.

In the US, it was a similar story in the US with Energy and Basic Materials sectors dropping the most in a drop that saw all eleven S&P sectors slide backwards.

Wednesday: With another day in the red for all four Indexes, the stock markets ended August on a four-day losing streak. The price of oil futures (U.S. West Texas Intermediate) fell below US$ 90 a barrel on concerns that the global economy will slow further because of the ongoing Covid-19 restrictions in China which will limit China’s productivity and demand for oil.

In Canada, Statistics Canada data showed economic growth lower than anticipated, indicating the Canadian economy may be cooling off faster than projected. However, the Bank of Canada is still expected to raise interest rates by another 0.75%. On the TSX, lower oil prices, combined with lower commodity prices for natural resources, all but guaranteed the TSX would end lower.

In the US, the news was not any better. The three US main Indexes had their largest monthly decline since 2015. Fears of another aggressive interest rate hike by the Fed has continue to plague the markets as once again all eleven S&P sectors ended the day lower.

Thursday: A mixed bag today with 2 Indexes ending higher, two ending lower, and all four Indexes within 1% of yesterday’s close. In Canada, the TSX fell the most of the four Indexes thanks to a drop in oil prices caused by additional Covid-19 lockdown measures in China. The Canadian defensive sectors Consumer Staples, Utilities and Telecommunications Services were the only sectors to gain ground today.

In the US, thanks to a late rally, the DJIA and the S&P ended their respective losing streaks, while the Nasdaq increased its losing streak to five sessions. The Utilities, Healthcare, Consumer Cyclical and Consumer Staples sectors were the only S&P sectors to gain ground. A key US labour market report, the non-farm payroll report, is due Friday. The report is an indicator of trends in economic growth and inflation. If the payroll numbers are increasing too quickly the Fed will likely interpret that as a sign that inflation is not slowing. If that is the case, they will have another reason to raise the benchmark US interest rate.

Friday: Another mixed day with the TSX ending higher and the three US Indexes each dropping over 1%. The big news of the day was the mixed US jobs report. There were more hirings than expected but wage growth was limited, and unemployment was higher than July, indicating some people have re-entered the job hunt. The increase in the number of people returning to the workplace could lead to the further cooling of wage growth, which would in turn help slow inflation. The favourable jobs report eased the pressure on the Fed for another aggressive interest rate hike. However, the odds are still on a 0.75% rate hike.

In Canada, the TSX’s losing streak came to an end thanks to higher energy and commodity prices. Investors in Canadian stocks now await the Bank of Canada’s meeting next week when they will announce the latest hike for Canada’s benchmark interest rate.

In the US, the higher energy and commodity prices helped the S&P Energy and Basic Materials sectors end higher while the other nine sectors ended lower.

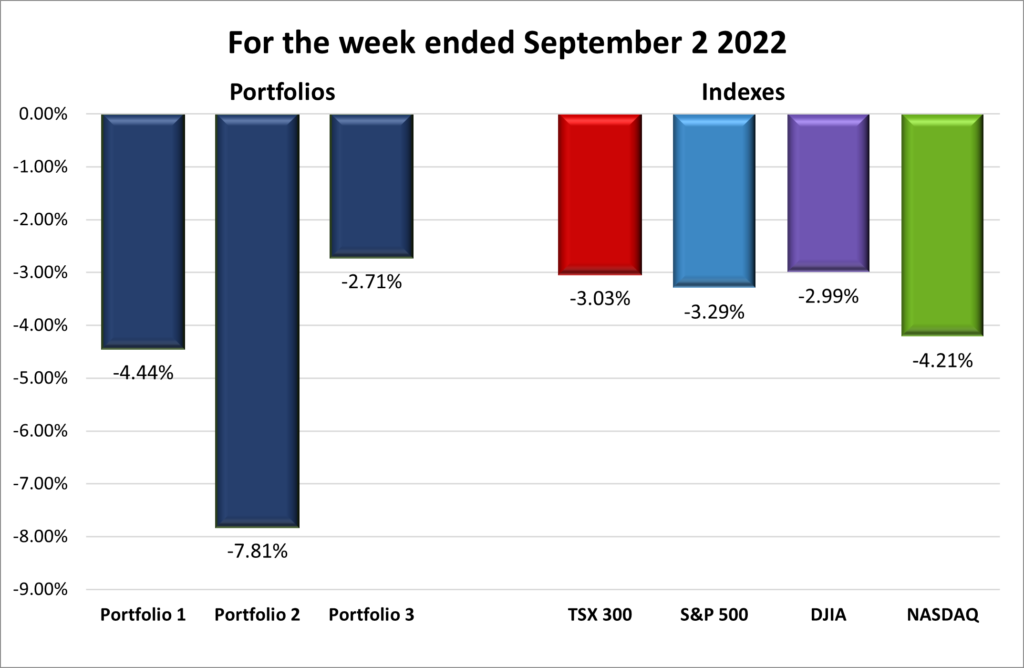

For the week, the TSX dropped 0.37%,the S&P 500 lost 3.28%, the Dow fell 2.99% and the Nasdaq ended 4.21% lower.

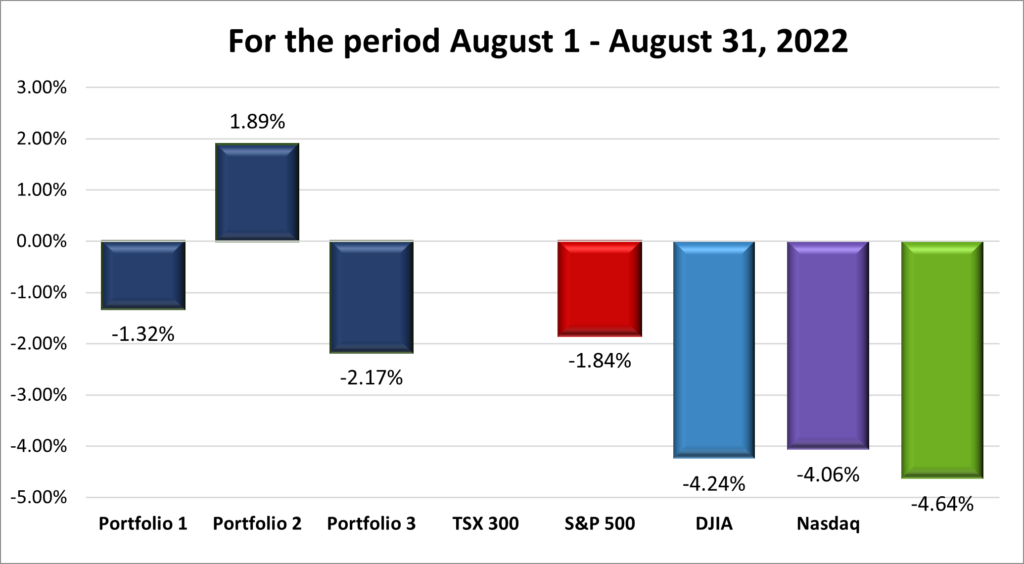

For the month, the TSX dropped 1.2%,the S&P 500 fell 4.24%, the Dow slid back 4.06% and the Nasdaq lost 4.64%.

Weekly Portfolio Review

The Stock Markets came out of July on fire, but ran into a wall of cold water and closed out August with a four-day losing streak. What looked like the start of a rally turned out to be a bear trap when the head of the Fed, Jerome Powell, stated getting inflation under control was the Fed’s #1 priority. Mr. Powell’s speech has become known as the Jackson Hole Jolt because of the sudden drop in the market immediately following his speech to a gathering of the heads of central banks at Jackson Hole.

As for the Portfolios, they followed the same pattern as the Indexes with early gains only to end August on a sour note. The big surprise was Portfolio 2 ended the month higher. I cannot think of any obvious reason for this superior performance other than it is a more balanced combination of proven, reliable companies. As for Portfolio 1 and Portfolio 3, both lost ground in August but at least they did not slide back as far as the American Indexes.

The lingering effects of Mr. Powell’s comments about the Fed’s war on inflation weighed heavily on the stock markets all week long. As you can see from the chart below, this past week has not been good for the Indexes, with drops of more than 4% for the American Indexes.

While it was a bad week for the Indexes, it was a worse week for Portfolio 2 which dropped almost 8%. I cannot remember a Portfolio or Index moving up or down that much in a week. The big anchor in Portfolio 2 was MongoDB (NASD:MDB). MongoDB’s quarterly report showed increasing losses, which had doubled compared to the year-ago quarter which rattled investors causing the share price to drop by 25%. As for Portfolios 1 and 3, they followed the direction of the Indexes but did not drop as much as the Indexes.

Companies on the Radar

It appears fears of a 0.75% interest rate hike by the Fed caused the share prices of both Amazon (NASD:AMZN) and Ferrari (NYSE:RACE) to fall into my price range. Amazon will be a good long-term investment because of its various revenue streams and market dominance in a few areas. Ferrari is more an ego thing, so I can say I own Ferrari. 😊Hopefully, their share prices will continue to drop through September and my patience will be rewarded.

Brookfield Select Opportunities (TSX:BSO.UN) remains on the radar because of its 10% quarterly dividend which is good for small pockets of cash in any of the Canadian accounts within the three Portfolios.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended September 2, 2022: DOWN ![]()

- According to Rivian’s (NASD:RIVN) CEO, the company has over $15 billion of cash on hand as of June 30. More than enough to keep the company producing electric vehicles through 2025, despite recent headwinds caused by rising battery costs and the new Inflation Reduction Act which ties tax incentives to using the raw materials in batteries from North American sources.

- It didn’t take long for Alphabet’s (NASD:GOOGL) Google to come out strongly against Microsoft’s (NASD:MSFT) update licensing agreements (see Portfolio 3 for information) which supposedly make it easier for small cloud providers to compete. Google said, “The promise of the cloud is flexible, elastic computing without contractual lock-ins.” It will be interesting to see how the European Union antitrust committee views these changes as it was their concerns that prompted Microsoft to make the changes.

- Tesla (NASD:TSLA) CEO Elon Musk has set a bold goal of selling 20 million electric vehicles in 2030 as part of Tesla’s pledge to push sustainable energy. If Tesla were to achieve their goal, this would make Tesla twice the size of any other vehicle maker. I am not sure how he would do this without a massive infrastructure build out, not to mention cornering the market in raw materials needed for batteries (lithium and nickel, among others) to power the 20 million vehicles. One small detail, experts say the raw material capacity for those 20 million vehicles currently does not exist. 😊

- Docebo (TSX: DCBO) announced they won seven Human Capital Management awards including six medals in the Learning and Development category and one gold medal in the Sales Performance category.

- Nvidia (NASD:NVDA) said they have been told by US officials stop exporting two of their top semiconductors used in artificial intelligence to China. American officials said this move is to limit the risk the chips will be used for military purposes. Nvidia had expected those chips to generate US$ 400 million in sales this quarter. This ban will put a major crimp in Nvidia’s anticipated revenues.

- General Motors (NYSE:GM) will offer all its Buick franchisees a buyout if they want to end their relationship with Buick as Buick moves to an all-electric line up. For those who retain their Buick dealerships, GM will provide monetary assistance to help dealers make the necessary investments to sell and service electric vehicles.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Shaw Communications Inc (TSX:SJR.B)

Quinsam Capital Corp (CN:QCA)

US $

Visa Inc (NYSE:V)

Quarterly Reports

Crowdstrike Holdings, Inc.

All currency listed in thousands of US dollars

Selected highlights from their second quarter 2023 financial results on August 30, 2022

- Revenue of $535,153 for the three months ended June 30, compared to $337,690 for the same period in 2021. An increase of almost 58%.

- Net loss of $48,313 for the three months ended June 30, compared to net loss of $57,318 in the same period in 2021.

- Diluted loss per ordinary share of $0.21 for the three months ended June 30, compared to $0.25 loss per share for the same period in 2021.

- Revenue of $1,022,987 for the six months ended June 30, compared to $640,533 for the same period in 2021. An increase of almost 60%.

- Net loss of $78,722 for the six months ended June 30, compared to net loss of $140,189 in the same period in 2021.

- Diluted loss per ordinary share of $0.35 for the six months ended June 30, compared to a $0.63 loss per share for the same period in 2021.

- Added 1,741 net new subscription customers in the quarter for a total of 19,686 subscription customers as of July 31, 2022, representing 51% growth year-over-year.

- Named Best Security Company by 2022 SC Awards US and received the Best Emerging Technology Award at SC Awards Europe 2022 for Falcon XDR.

Portfolio 2

Portfolio 2 for the week ended September 2, 2022: DOWN ![]()

- While Disney (NYSE:DIS) lost the streaming rights to the Indian Premier League (IPL), the most-watched cricket group in India, Disney was able to secure a four-year deal to stream International Cricket Council (ICC) events through the end of 2027. The ICC’s Men’s T20 World Cup, last held in 2021, attracted a record television reach of 167 million.

- Guardant Health (NASD:GH) announced an expanded strategic collaboration with Merck. The partnership will focus on leveraging Guardant’s GuardantINFORM platform to help accelerate the development of Merck’s pipeline of potentially transformative cancer medicines.

- MongoDB shares dropped over 25% after the company reported a greater second quarter loss, and forecast greater losses for the current third quarter as well as the fiscal 2023 year. A share price drop of 25% in one day is not a good thing, unless you are confident the company will rebound and take this as a buying opportunity. Hmmm, something to think about.

- Telus (TSX:T) completed the acquisition of LifeWorks Inc, formerly Morneau Shepell, for $2.3 billion. Telus will roll LifeWorks into its Telus Health unit.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Canadian Natural Resources Ltd (TSX:CNQ)

Fortis Inc (TSX:FTS)

US $

No US$ dividends this past week.

Quarterly Reports

Alimentation Touche-Card Inc.

All currency listed in millions of US dollars

Selected highlights from their first quarter 2023 financial results on August 30, 2022

- Revenue of $18,657.7 for the twelve weeks ended July 17, compared to $13,578.9 for the twelve weeks ended July 18, 2021. An increase of almost 37.4%.

- Net income of $872.4 for the twelve weeks ended July 17, compared to net income of $764.4 for the twelve weeks ended July 18, 2021.

- Diluted earnings per ordinary share of $0.85 for the twelve weeks ended July 17, compared to $0.71 for the twelve weeks ended July 17, 2021.

MongoDB, Inc.

All currency listed in thousands of US dollars

Selected highlights from their second quarter 2023 financial results on August 30, 2022

- Revenue of $303,660 for the three months ended June 30, compared to $198,747 for the same period in 2021. An increase of almost 52%%.

- Net loss of $118,865 for the three months ended June 30, compared to net loss of $77,133 in the same period in 2021.

- Diluted loss per ordinary share of $1.74 for the three months ended June 30, compared to a loss of $1.22 for the same period in 2021.

- Revenue of $598,107 for the six months ended June 30, compared to $380,395 for the same period in 2021. An increase of over 73%.

- Net loss of $196,159 for the six months ended June 30, compared to net loss of $141,125 in the same period in 2021.

- Diluted loss per ordinary share of $2.88 for the six months ended June 30, compared to $2.26 for the same period in 2021.

Portfolio 3

Portfolio 3 for the week ended September 2, 2022: DOWN ![]()

- Microsoft announced effective October 1, 2022, they will update their outsourcing and hosting terms. The changes will “support customers’ ability to move their licenses to a partner’s cloud, leverage shared hardware, and have more flexibility in deployment options for their software licenses.” Microsoft hopes these changes will address EU antitrust concerns that Microsoft has an unfair advantage against smaller European cloud service providers.

- In other Microsoft news, Britain’s Competition and Markets Authority (CMA) said Microsoft’s acquisition of Activision Blizzard could harm competition in the gaming industry. Given Microsoft’s Azure cloud platform, leading computer operating system Windows, as well as one of the top gaming consoles in Xbox, the company would be in an enviable position to dominant the gaming industry. The CMA said these strengths in combination with Activision’s industry leading games could damage competition in the emerging cloud gaming services market.

- Shopify (TSX:SHOP) announced a restructuring that led to more layoffs while at the same time increased the pay for remaining staff.

Activity

Bought Brookfield Select Opportunities. With its strong management team (Brookfield Corporation (TSX:BAM.A)) and a 10% dividend, this was bought as an income generator. If the shares can stay near the average cost, I will be happy to collect the quarterly dividend. 😊

Sold

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Enghouse Systems Ltd (TSX:ENGH)

Royal Bank of Canada (TSX:RY)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.