Liberation Day, part 2

President Trump kicked off a new wave of tariffs this week, reigniting global trade tensions. The move came just days after progress with the European Union (EU) and Japan had boosted market optimism – but that optimism is now giving way to concern.

The latest action includes a sweeping 35% tariff on Canadian goods not covered by CUSMA, which caught many by surprise. It also targets exports from Brazil, India, and other trading partners, with tariffs ranging from 10% to 25%. These new duties hit a wide range of products, from industrial parts and electronics to everyday consumer goods, raising fears of a broader trade war.

The White House says the goals are to address “long-standing imbalances,” protect US manufacturing, and penalize countries allegedly benefiting from unfair trade practices. But for investors, it’s a sharp reminder that trade policy can shift quickly and have real ripple effects on markets. Companies that rely on global supply chains may face higher costs, and if other countries retaliate, things could escalate even further.

In short, the trade front just got a lot more complicated. Trump’s tariff blitz marks a major escalation – levying new duties on nearly 70 countries, including key allies like Canada and India. Markets sold off sharply, and global businesses are recalibrating. It’s a volatile pivot into August, with big implications for commodity prices, supply chains, and investor sentiment.

For us investors, it’s a strong reminder that politics and investing go hand in hand. Even if you’re focused on fundamentals, global events like this can shake up entire sectors. Staying informed isn’t just smart, it’s part of being a thoughtful long-term investor.

With so much happening on the global stage, July was a reminder that even during a solid earnings season, big-picture news can take centre stage. From interest rate decisions to trade tensions and shifting market sentiment, there was a lot for us investors to digest. Let’s take a look at how the major indexes performed, what drove them, and how my portfolios held up through it all.

Items that may only interest or educate me ….

Let’s Make a Deal, Canadian Economic news, US Economic news, .…

Let’s Make a Deal

The US and EU struck a major trade deal on July 27 to avoid a full-blown trade war, agreeing to a 15% cap on most tariffs of EU imports instead of the much steeper ones that had been threatened. While not ideal, the deal brings some stability to global markets, especially with the EU pledging to buy $750 billion in US energy and invest another $600 billion into the US economy. Certain industries like aircraft parts and semiconductor equipment were spared from tariffs entirely, but most goods, including cars and branded pharmaceuticals, will still face that 15% rate.

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Bank of Canada Rate Announcement

As widely expected, the BoC held its policy rate steady at 2.75% today, marking the third consecutive hold. Despite solid job growth and resilient consumer spending, the Bank is opting for caution. Core inflation remains stubborn at 3.1%, slightly above the upper end of its 1–3% target range, while uncertainty from US trade policy and elevated tariffs continues to cloud the economic outlook.

Governor Tiff Macklem warned that tariffs are reducing economic efficiency and income, and if left unresolved, could lead to permanently lower growth. While the economy has shown resilience, there’s still too much uncertainty for the BoC to commit to cutting rates just yet.

For now, mortgage rates and borrowing costs are expected to stay where they are. But if the economy loses momentum and inflation continues to ease, the BoC has left the door open to rate cuts later this year. In the meantime, it will continue watching inflation and trade developments closely and adjust policy as needed.

Gross Domestic Product (GDP)

Data from Statistics Canada showed Canada’s economy shrank by 0.1% in May, following a similar 0.1% dip in April, marking two straight months of contraction. The monthly decline was driven by weaker output in sectors like ‘Mining,’ which is more sensitive to higher interest rates, and ‘Retail trade,’ which is feeling the impact of tariff pressures. Gains in ‘Manufacturing’ and ‘Transportation and warehousing’ weren’t enough to offset the broader slowdown. Looking at the past year, the biggest gains came from ‘Retail trade,’ while the steepest decline was in ‘Manufacturing.’

Statistics Canada’s early estimate for June points to a small 0.1% rebound, which would help the economy narrowly avoid a negative second quarter – just enough to sidestep a technical recession. But overall, growth has clearly stalled.

For us investors, this kind of soft data keeps the pressure on the BoC to consider rate cuts later this year in hopes of jumpstarting the economy. At the same time, it’s a reminder that the Canadian economy may be entering a more sluggish phase, so staying focused on resilient businesses that can perform well even in tough times becomes all the more important.

Canadian Market Volatility

Canada’s volatility barometer, the S&P/TSX 60 Volatility Index (VIXC), started the week at 9.97 and hovered between 10.0 and 11.0 until Friday, when it rose above 11, rising as high as 11.92, before settling back to 10.02 by the close. The jump on Friday likely reflected investor reaction to the latest escalation in the US-Canada trade dispute and weaker-than-expected US jobs data.

If you’re new to the VIXC, think of it as Canada’s version of a fear gauge. A reading below 10 suggests investors are feeling relaxed. Between 10 and 20 points to a steady, business-as-usual market. But once it climbs above 20, that’s when investor nerves start to show and market swings tend to get sharper.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Federal Reserve Rate Announcement

At the July 29-30, 2025, meeting of the Federal Reserve Open Market Committee (FOMC), the Fed decided to hold interest rates steady once again, keeping its benchmark rate at 4.25%–4.50%. This marks the fifth straight pause, as policymakers continue trying to ease inflation to their goal of 2% without derailing economic growth. Fed Chair Jerome Powell described the current stance as “moderately restrictive” – tight enough to cool inflation, but not so tight that it risks stalling the economy.

The Fed pointed to signs of slower growth and growing risks from US tariffs as reasons to stay cautious. Interestingly, two of the nine FOMC members – Michelle Bowman and Christopher Waller, both appointed by President Trump in his first term – voted against the decision, calling for an immediate 0.25% cut. That’s the most dissent the Fed has seen in over 30 years, highlighting growing internal debate over the path forward.

While political pressure for rate cuts is building – especially from Trump, who has been openly critical – Powell reaffirmed the importance of the Fed’s independence. He emphasized that monetary policy decisions must remain grounded in economic data, not politics, in order to maintain the confidence of markets and the public. With inflation easing and the labour market still solid, the Fed sees no need to rush and gave little sign of when borrowing costs might be lowered, though it hasn’t ruled out cuts later this year.

For now, borrowing costs stay unchanged. Mortgage rates, credit cards, and business loans tied to Fed policy are likely to stay where they are – at least until the data tells a different story.

Consumer Confidence Index (CCI)

The Conference Board’s CCI ticked up to 97.2 in July, rising from a revised 95.2 in June – a stronger reading than analysts had expected. The Present Situation Index, which reflects how consumers view current business and labour conditions, edged down slightly to 131.5 from last month’s revised 133.0. Meanwhile, the Expectations Index, which tracks sentiment about future business, income, and job prospects, climbed 4.5 points to 74.4. While that’s an improvement from June, it marks the sixth straight month the index has stayed below 80 – a level often seen as a recession warning.

Consumer confidence is still running lower than it was a year ago, and nearly 20% of consumers now say jobs are “hard to get” – the weakest labour sentiment since March 2021. Tariffs are still top of mind for many, as they’re widely associated with higher prices. Overall, while confidence is inching back into more optimistic territory, the rebound is far from dramatic. Sentiment is still well below 2024 levels, and that fits with the broader trend: steady but cautious growth, where people are willing to spend but remain wary of job security and inflation pressures.

Gross Domestic Product (GDP)

According to the Commerce Department’s Bureau of Economic Analysis (BEA), the American economy bounced back in the second quarter of 2025, growing at an annualized rate of 3.0%, according to today’s advance GDP estimate. That was well above analysts’ expectations for a 2.4% increase and a sharp turnaround from the 0.5% contraction in the first quarter. While the headline number looks strong, much of the growth came from a sharp drop in imports, which reduced the trade deficit and gave GDP an artificial boost. In other words, the economy didn’t necessarily produce more – it just bought less from other countries, likely due to higher prices caused by US tariffs.

Consumer spending picked up slightly, rising 1.4% after a soft start to the year, though it remains below the stronger levels seen in 2024. Business investment and housing continued to lag, likely weighed down by high interest rates and ongoing trade uncertainty. A more telling measure of real demand – what households and businesses actually spent – grew just 1.2%, the slowest pace in over two years.

For the Fed, this report supports the case for holding interest rates steady. While headline growth looks encouraging, the underlying data points to a cautious economy. If momentum fades further and inflation continues to ease, rate cuts could still be on the table later this year.

For us investors, it’s a good reminder to look past the headlines. A 3% GDP print might sound like a big comeback, but the fine print shows a recovery that’s still on shaky ground.

Personal Consumption Expenditures (PCE)

The BEA’s latest PCE report shows inflation heating up slightly in June. Headline PCE, which includes food and energy, rose 2.6% year-over-year, up from 2.3% in May, while core PCE – the Fed’s preferred inflation gauge that strips out the more volatile food and energy prices – ticked up to 2.8%, above the expected 2.7%. On a monthly basis, both measures rose 0.3%, matching expectations but still pointing to ongoing price pressures.

This uptick in inflation, especially in core goods (which rose 0.4% in June), suggests that tariffs are starting to push prices higher. That’s likely to keep the Fed’s attention, and it reinforces their latest decision to hold interest rates steady at 4.50%. With inflation proving stickier than hoped, the chances of a rate cut in September are looking slimmer.

For us investors, this latest inflation data means we’ll likely need to wait a bit longer for interest rate cuts. Higher rates for longer can weigh on growth stocks, especially those that rely on borrowing to fund future expansion. At the same time, it may continue to pressure consumer spending and corporate profits, which could slow the broader economy. For those of us investing for the long term, it helps to stay focused on companies built to weather different rate environments and tune out the noise as markets adjust. 😊

Labour data

The latest updates from the JOLTS, the ADP Employment Report, and the ESS offer a snapshot of the US labour market. Together, they point to a job market that’s still standing but showing more cracks beneath the surface.

Job Openings and Labor Turnover Survey (JOLTS)

The US Bureau of Labor Statistics reported job openings fell to 7.43 million in June, down from 7.71 million in May and below the expected 7.55 million. This monthly report gives us insight into labour demand by tracking openings, hiring, quits, and layoffs – offering important clues on whether the job market is heating up or cooling off.

The latest numbers suggest businesses are tapping the brakes on hiring as economic uncertainty lingers. For us investors, this adds to the growing sense that the job market is cooling, not collapsing, which supports the idea that the Fed may continue holding rates steady. But if this softening trend continues, the case for rate cuts later this year could strengthen.

ADP Employment Report

According to ADP, private employers added 104,000 jobs in July – comfortably beating forecasts of around 75,000. This rebound follows June’s revised loss of 23,000 jobs (originally reported as -33,000), suggesting hiring picked up faster than expected.

The upside surprise points to growing employer confidence, likely helped by easing trade headwinds and firmer consumer demand. While the rebound doesn’t scream overheating, it’s enough to reinforce the Fed’s current hold-steady stance, while still leaving the door open for cuts if broader conditions weaken.

Employment Situation Summary (ESS)

The US economy added just 73,000 nonfarm jobs in July – the slowest pace this year and well below the 100,000 consensus estimate. Adding to the disappointment, May and June job gains were revised down by a combined 258,000 jobs. June’s number was slashed from 147,000 to just 14,000, and May from 144,000 to 19,000, completely reshaping the recent hiring picture.

The unemployment rate ticked up to 4.2%, in line with expectations, and has hovered between 4.0% and 4.2% since May 2024. Average hourly earnings rose 0.3% for the month, with year-over-year wage growth likely creeping up to 3.9%.

Altogether, July’s report reveals a labour market that’s clearly slowing – weak job creation, rising unemployment, and deep revisions that erased most of June’s perceived strength.

Summary

This week’s labour data tells a mixed but increasingly cautious story. JOLTS shows weakening demand, ADP reveals a rebound from a soft patch, and the ESS confirms the slowdown with underwhelming job gains and heavy downward revisions. On its own, this data might have supported the case for future rate cuts. But paired with this week’s June PCE report that showed inflation ticking back up to 2.6% and core inflation stuck at 2.8%, it muddies the waters for the Fed. We’re now looking at a cooling labour market and sticky inflation, which keeps rate decisions uncertain and investors on edge.

Consumer Sentiment Index (CSI)

Consumer sentiment ticked up slightly in July, reaching its highest level in five months. The University of Michigan’s Consumer Sentiment Index rose to 61.8 from 60.7 in June, a modest 1.6% increase. While still 7.1% lower than a year ago and well below the long-term average of 84, it marks a small step in the right direction. The reading also came in just shy of expectations, with analysts calling for 62.

Looking closer, the Current Conditions Index – which reflects how people feel about their present situation, including job security and personal finances – climbed to 68.0 from 64.8. That’s a solid 4.9% monthly gain and 8.5% higher than last year, suggesting growing confidence in current conditions. Meanwhile, the Expectations Index, which looks six months ahead, dipped to 57.7 from 58.1, a 0.7% monthly decline and down 16.1% year over year, pointing to continued caution about the future.

Interestingly, sentiment improved among stockholders but fell among non-investors, hinting at a growing divide in how different groups are experiencing the economy. Overall, while people are feeling a bit better about the present, uncertainty about what’s next still looms large. It’s as if the economy is in idle, stable for now, but with no clear sign it’s ready to shift into drive.

For consumer-driven sectors like retail, travel, or discretionary spending, that hesitation could mean a slower recovery—even if the mood on the ground is starting to brighten.

American Market Volatility

Wall Street’s “fear gauge,” the CBOE Volatility Index (VIX), continued drifting lower for most of the week, opening at 15.15 following news that the US had reached a trade framework agreement with the EU. It hovered around the 15 mark until Friday, when it suddenly spiked to 21.90 before settling at 20.38 by the end of the session. The late-week surge appeared to be triggered by a one-two punch: the US imposing tariffs on nearly all of its major trading partners, and a disappointing jobs report that not only missed expectations but also included sharp downward revisions to the prior two months.

If you’re new to the VIX, think of it as a real-time pulse check on investor anxiety. It tends to spike when markets get rattled—whether from geopolitical flare-ups, inflation surprises, or something like the Fed chair getting unexpectedly replaced. When fear rises, so does the VIX.

A reading between 12 and 20 suggests calm conditions. Once it pushes past 20, traders start bracing for bigger swings. The higher it climbs, the more uncertainty is being priced into the market.

Weekly Market and Portfolio Review

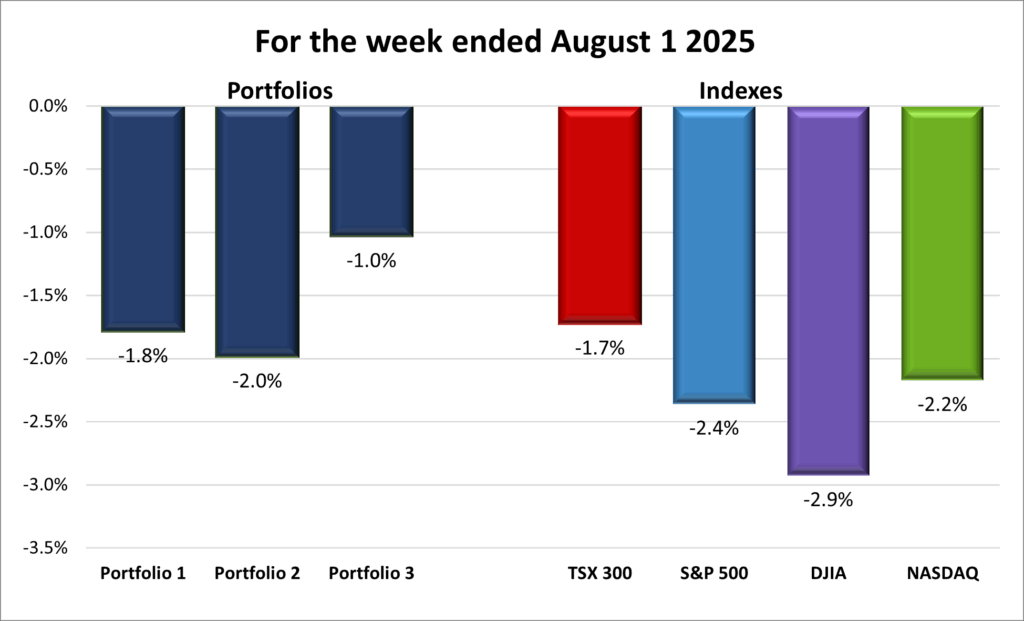

For the week, the TSX (SPTSX) declined 1.7%, the S&P 500 (SPX) fell 2.4%, the DJIA (INDU) dropped 2.9% and the Nasdaq (CCMP) lost 2.2%.

| Index | Weekly Streak |

| TSX: | 1 – week losing streak |

| S&P: | 1 – week losing streak |

| DJIA: | 1 – week losing streak |

| Nasdaq: | 1 – week losing streak |

![]() This past week was packed with market-moving events – central bank rate decisions, a flood of economic data, and earnings from some of the biggest technology names. Even with all that momentum, the major indexes couldn’t quite hold their gains. The S&P 500 Index (S&P), Nasdaq Composite Index (Nasdaq), and Toronto Stock Exchange Composite Index (TSX) all hit fresh record highs during the week, with the S&P notching its sixth straight closing high to begin the week. However, by Friday, all four major indexes, including the Dow Jones Industrial Average (DJIA), finished lower on the week, thanks to a drop of over 1% for each of the American indexes and nearly a 1% drop on the TSX on the last day of the week.

This past week was packed with market-moving events – central bank rate decisions, a flood of economic data, and earnings from some of the biggest technology names. Even with all that momentum, the major indexes couldn’t quite hold their gains. The S&P 500 Index (S&P), Nasdaq Composite Index (Nasdaq), and Toronto Stock Exchange Composite Index (TSX) all hit fresh record highs during the week, with the S&P notching its sixth straight closing high to begin the week. However, by Friday, all four major indexes, including the Dow Jones Industrial Average (DJIA), finished lower on the week, thanks to a drop of over 1% for each of the American indexes and nearly a 1% drop on the TSX on the last day of the week.

In the US, the Fed was front and centre, holding interest rates steady at 4.25%–4.50% as widely expected. Fed Chair Powell struck a patient, data-dependent tone, which markets initially welcomed. But as the week went on, optimism faded. Labour data sent mixed signals – initial jobless claims stayed low, yet announced job cuts jumped. Then came Friday’s employment report, showing weaker-than-expected job growth and sharp downward revisions to hiring over the past two months. That opened the door for a potential rate cut at the Fed’s next meeting in September. Offsetting that, however, was the Fed’s preferred inflation gauge – core PCE – which rose to 2.8% year over year, a reminder that inflation is still proving stubborn.

Following the release of the jobs report, President Trump fired the head of the US Bureau of Labor Statistics (BLS), alleging that the employment numbers had been manipulated for political reasons – though no evidence has been presented to support the claim. The move is extraordinary, especially coming after a weaker-than-expected jobs report, and raises serious concerns about the independence and credibility of US economic data. For investors, it adds a new layer of uncertainty – not just about the Fed’s next move, but about whether we can continue to trust the numbers that shape market expectations.

Big Tech earnings helped keep things afloat. Microsoft (NASD: MSFT) and Alphabet (NASD: GOOGL), both beat expectations, especially in artificial intelligence (AI) and cloud segments, reinforcing the growing excitement around artificial intelligence. Their strong results boosted investor confidence in AI and helped limit the week’s losses – especially for the Nasdaq.

Later in the week, trade took centre stage again. Markets got an early boost on news the US had finalized a deal with the EU, settling on 15% tariffs instead of the previously threatened 30%. Hopes rose further as talks with China resumed. But by midweek, tensions flared. President Trump announced a new wave of tariffs on dozens of trading partners, including India, Brazil, and key copper exports. He also approved a tariff hike on Canadian goods to 35%, though products covered under the Canada-US-Mexico Agreement (CUSMA) are exempt. To allow more time to negotiate deals with other partners, the implementation date was pushed back by a week – but the renewed uncertainty rattled investors.

In Canada, the TSX followed a similar script – rising early on trade optimism and higher oil and gold prices, then losing steam as the week wore on. The index even hit a new all-time high before pulling back. The BoC held its policy rate steady at 2.75%, as expected, but struck a cautious tone. With inflation proving sticky and growth weakening, it signalled that rate cuts aren’t on the table just yet. That view was backed by May’s GDP report, which showed the economy shrank 0.1% – the second monthly dip in a row – raising fresh concerns about a broader slowdown, especially in manufacturing and retail.

Trade tensions also weighed on the TSX later in the week. Despite early optimism, the market pulled back as investors grappled with the uncertainty from new US tariffs and their potential impact on Canadian exports. It was a reminder that even close trading partners can face sudden shifts, keeping markets on edge.

All in all, despite the ups and downs, it was a week that showed just how much investors are juggling – earnings, inflation, central bank decisions, and trade twists all at once. But strong corporate results, especially from tech, and signs of continued resilience in the economy helped keep market optimism alive. As we head into August, investors remain cautiously hopeful that rate cuts are still on the horizon and trade tensions will cool. There’s a lot to keep an eye on, but there’s also plenty of opportunity if you’re in it for the long haul. 😊

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week losing streak |

| Portfolio 2: | 1 – week losing streak |

| Portfolio 3: | 1 – week losing streak |

![]() It wasn’t shaping up to be a great week for the three portfolios heading into Friday. Portfolio 3 was still up 1%, and the other two were only slightly down. But that changed quickly after the release of weak US labour data and the subsequent firing of the head of the BLS, sparking concerns over political interference. All three portfolios fell more than 1% on Friday alone, ending the week in the red. On the bright side, they still outperformed all major US indexes – a small consolation. ☹

It wasn’t shaping up to be a great week for the three portfolios heading into Friday. Portfolio 3 was still up 1%, and the other two were only slightly down. But that changed quickly after the release of weak US labour data and the subsequent firing of the head of the BLS, sparking concerns over political interference. All three portfolios fell more than 1% on Friday alone, ending the week in the red. On the bright side, they still outperformed all major US indexes – a small consolation. ☹

Portfolio 1 dropped 1.8%, with just 14% of its holdings finishing in the green. Steep losses from PayPal (NASD: PYPL) and Ferrari (NYSE: RACE), both down 15%, along with Datadog (NASD: DDOG) and Navitas Semiconductor (NASD: NVTS), each down 10%, weighed heavily. A rare highlight was Celestica ((TSE: CLS), which hit a record high and gained 14%.

Portfolio 2 had the toughest week, falling 2.0% despite posting the highest percentage of gainers at 22%. There were no standouts on the upside, while MongoDB (NASD: MDB) sank 10%, dragging the portfolio lower.

Portfolio 3 held up the best, losing 1%. Although only 18% of its holdings ended higher, it avoided any major winners or losers – except for Lithium Americas (TSE: LAC), which slid 14%.

Overall, it was a rough week. The firing of the BLS chief and continued verbal attacks on the Fed raise serious concerns about political interference, shaking investor confidence in the data that guides monetary policy. Layer on the global trade uncertainty, and it’s no surprise volatility ticked up – especially in the US. That said, the market pullback may offer buying opportunities for us long-term investors in the weeks ahead. 😊

Companies on the Radar

Instead of scouting for new companies to add to the radar this past week, I focused on updating two of the key tools I use when deciding whether to become a part owner in a business: my Quick Test and Deep Dive checklists. I first built these back in 2020–2021, and while they’ve held up well, I’ve learned a lot about investing since then, it felt like the right time for a refresh.

Instead of scouting for new companies to add to the radar this past week, I focused on updating two of the key tools I use when deciding whether to become a part owner in a business: my Quick Test and Deep Dive checklists. I first built these back in 2020–2021, and while they’ve held up well, I’ve learned a lot about investing since then, it felt like the right time for a refresh.

The Quick Test (Step 2 in my process, right after the initial Radar Check, the results shown below in the two tables) is now an 11-question checklist designed to quickly screen out companies that don’t meet my core criteria. If a company passes that stage, it moves on to the Deep Dive (Step 3), where I take a much closer look at its products, customers, moat, management, financials, and long-term potential before deciding if it’s worth owning.

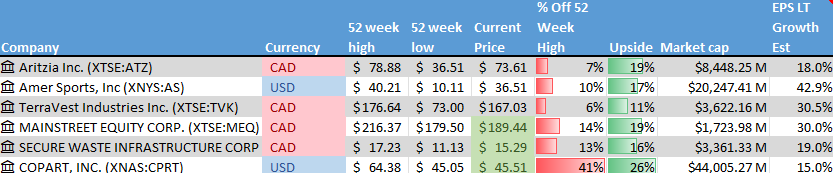

I’m still refining the Deep Dive, so I haven’t had much time this week to look for new opportunities. For now, my radar is still focused on these six companies:

- Aritzia (TSE: ATZ): a fashion retailer and design house known for its upscale in-house brands of women’s clothing and accessories. It controls everything from design to distribution and sells through more than 130 boutiques across North America, along with a fast-growing online platform. Its main markets are Canada and the US, where it continues to expand.

- Amer Sports (NYSE: AS): a Finnish sporting goods company that went public in February 2024. It owns premium global brands like Wilson, Salomon, Arc’teryx, Atomic, and Louisville Slugger, selling in over 100 countries. Revenue comes from both retail partners and a growing direct-to-consumer (DTC) segment through branded stores and online sales. With strong revenue growth, expanding DTC margins, and a valuation below peers, Amer offers an attractive mix of growth and value. As a consumer-focused company riding the health and outdoor trend, it’s definitely caught my eye.

- TerraVest Industries (TSE: TVK): an industrial manufacturer serving the energy, agriculture, and transportation sectors across North America. Its products include propane tanks, ammonia storage vessels used in farming, natural gas transport vehicles, and various energy processing systems. It’s a solid operator in essential industries.

- Mainstreet Equity Corp. (TSE: MEQ): a Calgary-based real estate company focused on mid-market apartment buildings – typically under 100 units – across Western Canada. It buys underperforming properties at below-market prices, renovates them, and increases rental income through improved operations. With strong demand for rental housing, a repeatable value-add strategy, and a solid balance sheet, Mainstreet offers a compelling mix of income and growth. Shares currently trade below net asset value, giving investors a margin of safety alongside steady cash flow and long-term upside.

- Secure Energy Services (TSE: SES): a Canadian industrial company that focuses on environmental and waste management services for energy and industrial clients. It offers recycling, disposal, and infrastructure support across North America.

- Copart (NASD: CPRT): this American company runs one of the world’s largest online vehicle auction platforms, specializing in salvage cars from accidents and natural disasters. It sells on behalf of insurers, dealerships, rental companies, and individuals. Copart earns revenue through transaction fees, storage, transportation, and listing services. Its digital model, global buyer network, and asset-light approach support strong margins and steady growth. With no long-term debt and rising tailwinds from vehicle values and insurance claims, it’s a steady growth story that’s earned a spot on my radar.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated August 1, 2025.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!