Dominoes start to fall

Since President Trump’s April 2 “Liberation Day” announcement – imposing sweeping tariffs on nearly all imports, starting with a universal 10% base and rising to “reciprocal” rates as high as 54% – the US has been scrambling to strike new trade deals. With a 90-day pause in effect for negotiations and court challenges mounting, several countries have already hammered out agreements aimed at easing tariff threats and stabilizing trade ties.

Each deal is tailored to the partner: some offer tariff relief, others open access to key sectors, but all share one goal – softening the blow of a trade war no one wants. Here’s a scorecard of the formal deals signed since April 2, 2025:

Post–Liberation Day Trade Deals

| Partner | Threatened Tariff | Final Tariff | What the US Gains in Return |

|---|---|---|---|

| Japan | ~25% on autos & goods | 15% | $550 billion Japanese investment, increased US access to agricultural and auto sectors |

| Indonesia | 32% | 19% | Removal of critical-mineral export restrictions; 0% on most US goods; Indonesia opens market to Boeing, ag, energy. |

| Philippines | ~19% | 19% on their goods, 0% on US goods | Zero tariffs on US exports, reciprocal tariff maintained. |

| Vietnam | 46% | 10% baseline | US exports spared higher tariffs. |

| United Kingdom | Reciprocal possible (~10–54%) | 10% baseline | Deal restored baseline rate, averting worst-case hikes. |

| China | Up to 54% (34 % + others) | 10% applied during pause | Deal paused further escalation; 10% baseline tariff maintained. |

These deals represent partial retreats from the sweeping tariff plan. Some, like Japan’s, are especially impactful – slashing auto tariffs and securing huge investment commitments that boosted investor sentiment. Markets reacted favourably, with the Toronto Stock Exchange Composite Index (TSX), the S&P 500 (S&P), and Nasdaq Composite Index (Nasdaq) hitting fresh record highs after the Japan deal was announced.

But big players like Canada, the European Union (EU), and Brazil are still staring down potential tariffs of 30–50% if no agreement is reached by the August 1 deadline.

Why Trade Deals Matter (Especially for Investors)

At their core, trade deals are about setting the rules – who can sell what, where, and at what cost. For investors, they reduce uncertainty and help businesses plan across borders. And as we all know: markets hate uncertainty.

Trump’s Liberation Day tariffs introduced more of it. While deals with countries like Japan and Indonesia have calmed some nerves, relationships with major allies – especially Canada and the EU – remain unresolved.

That kind of limbo hits both Canadian and US markets. Canadian exporters in autos, manufacturing, and agriculture rely heavily on US access. Without a deal, they face sudden tariffs, border delays, or retaliation. At the same time, American firms depending on Canadian inputs see rising costs and supply chain snags.

And here’s the real kicker: businesses hate surprises. When they can’t plan ahead, they freeze – delaying hiring, expansions, or new investments. That caution trickles into markets, fuelling volatility and dragging on growth. For us investors, it’s a clear reminder that global politics can shake markets and portfolios just as much as earnings reports.

With the August 1 deadline fast approaching, and key players like Canada, the EU, and Brazil still at the table, the stakes are high. If no deals are reached, hefty tariffs could take effect – rippling across supply chains and rattling markets. Whether this is all tough negotiating or the start of something more fractured, one thing’s for sure: geopolitics isn’t just background noise anymore – it’s front and centre in the market story.

With trade tensions continuing to drive market sentiment, let’s take a closer look at how the major indexes performed this week and how my three portfolios held up.

Items that may only interest or educate me ….

Canadian economic news, US economic news, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Retail Sales

According to Statistics Canada, retail sales in Canada slipped by 1.1% in May, following a modest 0.3% gain in April. The decline didn’t come as a surprise to analysts, but it still points to some softening in consumer spending. The biggest drag came from new car dealers, where sales fell 4.6% – likely because many buyers rushed to make purchases earlier in the year ahead of expected tariffs. On the flip side, jewellery, luggage, and leather goods retailers saw the strongest growth, up 3.8% for the month.

Looking at year-over-year numbers, total retail sales were up 4.9%, slightly below April’s 5.0% pace. Used car dealers led the way with a 15.8% jump compared to last year, while gasoline stations posted the steepest drop, down 8.4%, hinting that consumers may be cutting back on everyday purchases.

Core retail sales, which strip out the more volatile auto and gas categories, were flat in May after a small 0.1% rise in April. Still, they’re up 5.3% from a year ago, an improvement over April’s 3.7% pace. But the overall picture shows momentum cooling, both in headline and core spending.

StatsCan’s early estimate suggests June could bring a 1.6% rebound, which might mean May’s dip was just a temporary pause. Even so, with over 30% of retailers reporting impacts from US trade tensions and consumers still adjusting to higher borrowing costs, the outlook remains uncertain. Slowing retail sales can be an early sign that households are becoming more cautious, which could weigh on economic growth in the months ahead. For investors, this raises questions about the strength of consumer-driven sectors and whether the BoC may have more room, or pressure, to cut interest rates if spending continues to cool.

Canadian Market Volatility

Canada’s volatility barometer, the S&P/TSX 60 Volatility Index (VIXC), opened the week at 9.49 and gradually drifted higher, briefly rising above 10 as investors grew concerned that tariffs could spike to 35% if a trade deal with the US isn’t reached by the August 1 deadline. But by Friday, those worries had eased, and the VIXC dipped back below 10 to close the week at 9.87.

If you’re new to the VIXC, think of it as Canada’s version of a fear gauge. A reading below 10 suggests investors are feeling relaxed. Between 10 and 20 points to a steady, business-as-usual market. But once it climbs above 20, that’s when investor nerves start to show and market swings tend to get sharper.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

American Market Volatility

Wall Street’s “fear gauge,” the CBOE Volatility Index (VIX), continued drifting lower this week. It opened at 16.87 and steadily declined, closing Friday at 14.93 – its lowest level in five months. Dropping below 15 for the VIX is uncommon and signals a market that’s unusually calm. The last time the VIX closed lower than this was back in early 2024, during a more stable stretch before volatility began creeping back.

A few things helped ease investor nerves this week. The announcement of a trade deal between the US and Japan boosted confidence that other agreements might follow before the August 1 deadline. And stronger-than-expected earnings from Alphabet (NASD: GOOGL) reassured investors that big artificial intelligence (AI) bets are starting to pay off.

If you’re new to the VIX, think of it as a real-time pulse check on investor anxiety. It tends to spike when markets get rattled – whether from geopolitical flare-ups, inflation surprises, or something like firing the head of the Fed. When fear rises, so does the VIX.

Generally, a reading between 12 and 20 suggests calm conditions. Once it pushes past 20, traders start bracing for bigger swings. The higher it goes, the more uncertainty is priced in.

Weekly Market and Portfolio Review

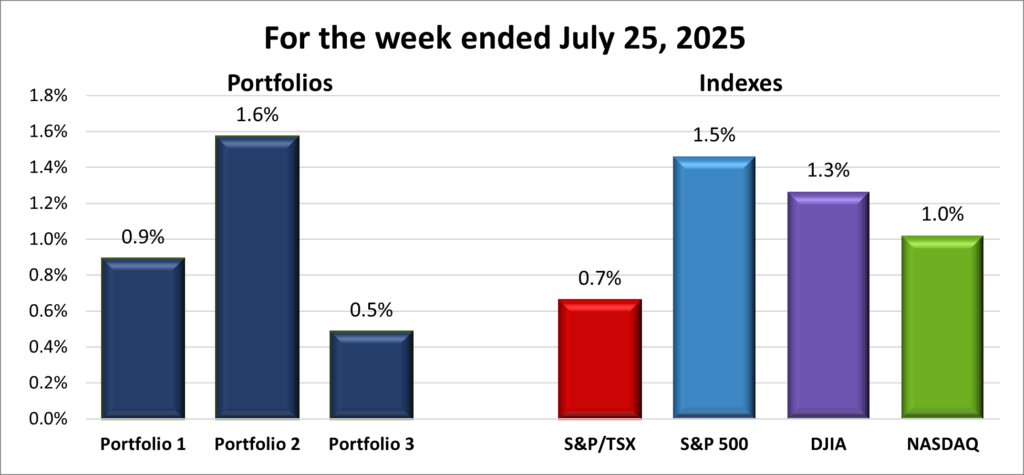

For the week, the TSX (SPTSX) rose 0.7%, the S&P 500 (SPX) surged 1.5%, the DJIA (INDU) climbed 1.3% and the Nasdaq (CCMP) advanced 1.0%.

| Index | Weekly Streak |

| TSX: | 2 – week winning streak |

| S&P: | 2 – week winning streak |

| DJIA: | 1 – week winning streak |

| Nasdaq: | 2 – week winning streak |

![]() Markets stayed in rally mode this week, as you can see in the weekly progress chart above, with the S&P 500 breaking through 6,300 for the first time and not looking back – closing at a new record every single day. The last time the S&P had a week of closing highs was in November 2021. The Nasdaq wasn’t far behind, hitting fresh highs on four out of five trading days, including a three-day streak to wrap up the week. While the DJIA didn’t notch a record, it still delivered a solid gain and came within striking distance of its own all-time high. All three major American indexes finished the week up more than 1%.

Markets stayed in rally mode this week, as you can see in the weekly progress chart above, with the S&P 500 breaking through 6,300 for the first time and not looking back – closing at a new record every single day. The last time the S&P had a week of closing highs was in November 2021. The Nasdaq wasn’t far behind, hitting fresh highs on four out of five trading days, including a three-day streak to wrap up the week. While the DJIA didn’t notch a record, it still delivered a solid gain and came within striking distance of its own all-time high. All three major American indexes finished the week up more than 1%.

Driving the optimism was a mix of trade progress and strong earnings.

On the trade front, the US signed new deals with the Philippines and Indonesia, each including a 19% tariff on imports. A more impactful agreement followed with Japan, a major trading partner, setting a 15% duty on Japanese goods. Markets saw these as signs that more deals could land before the August 1 deadline – possibly including one with the EU that would be similar to the deal struck with Japan. If deals are not struck by the deadline, trading partners risk facing “reciprocal” tariffs, where the US would match the average tariff level those countries place on American exports. In many cases, that would mean significantly steeper costs to sell into the US.

Earnings season also played a major role. Tesla (NASD: TSLA) missed expectations, but Alphabet delivered stronger-than-expected results, easing fears that AI spending might be cooling. Instead, it reinforced the belief that Big Tech’s massive AI investments are starting to pay off. Alphabet’s performance helped lift the mood, and share prices, across the broader AI and technology space, pushing both the S&P 500 and Nasdaq to record territory.

In Canada, the TSX posted two record closes, including a new all-time high on Friday. The rally was driven by renewed trade optimism, a boost from rising gold and copper prices, and a spillover effect from upbeat US earnings. Still, some clouds linger. With the August 1 tariff deadline looming – and President Trump warning he could impose 35% duties unilaterally – there’s still real doubt over whether Ottawa and Washington will strike a deal. Canadian negotiators had hoped to avoid any tariffs but now seem resigned to at least some duties on exports heading south.

Looking ahead, next week could be pivotal. Both the Fed and the BoC are set to hold their final summer meetings, a wave of economic data is on deck, and a flood of earnings, including a few more Magnificent 7 heavyweights, is expected. Add in Trump’s self-imposed August deadline for global trade deals, and markets could be in for a lively ride.

| Portfolio | Weekly Streak |

| Portfolio 1: | 2 – week winning streak |

| Portfolio 2: | 2 – week winning streak |

| Portfolio 3: | 2 – week winning streak` |

![]() After all three portfolios bounced back the previous week, and with all four major indexes posting gains, I was hoping the momentum would carry through. And sure enough, all three extended their weekly win streaks to two with another week of gains, as you can see in the chart below.

After all three portfolios bounced back the previous week, and with all four major indexes posting gains, I was hoping the momentum would carry through. And sure enough, all three extended their weekly win streaks to two with another week of gains, as you can see in the chart below.

Portfolio 1 managed a modest 0.9% gain. The main drag was indie Semiconductor (NASD: INDI), which fell 11%, though it’s a small position. That dip was more than offset by gains in 56% of the holdings, including new all-time highs from Ferrari (NASD: RACE) and Celestica (TSE: CLS).

Portfolio 2 was the standout this week, climbing 1.6%, despite only 51% of its holdings posting gains. There were no big movers in either direction, just steady strength across the board. That was enough to top the week’s leaderboard, even beating out the S&P 500, the top performing index.

Portfolio 3 looked set for a weekly loss heading into Friday, but a strong finish flipped it into the green with a 0.5% gain. While not as eye-catching as the previous week’s 4.9% surge, it was still a solid result and kept the winning streak alive. Interestingly, it had the highest percentage of weekly winners, with 59% of holdings ending the week in positive territory.

All in all, a decent week, nothing too dramatic, but steady progress. With earnings season in full swing and trade talks heating up, I’m expecting more twists and turns ahead. Volatility cooled over the past week, but I’ll be watching how markets respond to upcoming economic data and any new developments on the trade front. Maybe a buying opportunity will present itself.

While the gains weren’t as big as the week before, I’ll gladly take them—and hopefully make it three in a row next week. 😊

Companies on the Radar

Once again, no new companies caught my attention this week, but I did remove one from my radar list: Nordisk A/S (NYSE: NVO). I had been considering becoming a (very small) part-owner, but the company chose not to renew its Canadian patent (CA 2,601,784) covering semaglutide, the active ingredient in Ozempic and Wegovy. That opens the door for generic competitors once data exclusivity ends in January 2026, putting future market share and profits in Canada at risk.

Once again, no new companies caught my attention this week, but I did remove one from my radar list: Nordisk A/S (NYSE: NVO). I had been considering becoming a (very small) part-owner, but the company chose not to renew its Canadian patent (CA 2,601,784) covering semaglutide, the active ingredient in Ozempic and Wegovy. That opens the door for generic competitors once data exclusivity ends in January 2026, putting future market share and profits in Canada at risk.

While the lapse only affects the Canadian market, it’s still Novo’s second largest for these products. Generic launches could drive prices down by 50–80%, hitting local revenues and margins hard. And if generics gain traction here, it could encourage similar challenges in other markets.

This might end up being a non-event if Novo successfully defends its position through other patents or strategies – but with plenty of other promising companies out there, I’d rather focus on opportunities without this kind of uncertainty hanging over them. With Novo Nordisk off the list, I’m down to the six companies below:

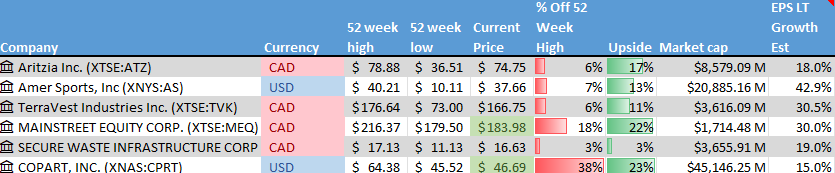

- Aritzia (TSE: ATZ): a fashion retailer and design house known for its upscale in-house brands of women’s clothing and accessories. It controls everything from design to distribution and sells through more than 130 boutiques across North America, along with a fast-growing online platform. Its main markets are Canada and the US, where it continues to expand.

- Amer Sports (NYSE: AS): a Finnish sporting goods company that went public in February 2024. It owns premium global brands like Wilson, Salomon, Arc’teryx, Atomic, and Louisville Slugger, selling in over 100 countries. Revenue comes from both retail partners and a growing direct-to-consumer (DTC) segment through branded stores and online sales. With strong revenue growth, expanding DTC margins, and a valuation below peers, Amer offers an attractive mix of growth and value. As a consumer-focused company riding the health and outdoor trend, it’s definitely caught my eye.

- TerraVest Industries (TSE: TVK): an industrial manufacturer serving the energy, agriculture, and transportation sectors across North America. Its products include propane tanks, ammonia storage vessels used in farming, natural gas transport vehicles, and various energy processing systems. It’s a solid operator in essential industries.

- Mainstreet Equity Corp. (TSE: MEQ): a Calgary-based real estate company focused on mid-market apartment buildings – typically under 100 units – across Western Canada. It acquires underperforming properties at below-market prices, renovates them, and increases rental income through improved operations. With strong demand for rental housing, a repeatable value-add strategy, and a solid balance sheet, Mainstreet offers a compelling mix of income and growth. Shares currently trade below net asset value, giving investors a margin of safety alongside steady cash flow and long-term upside.

- Secure Energy Services (TSE: SES): an industrial company that focuses on environmental and waste management services for energy and industrial clients. It offers recycling, disposal, and infrastructure support across North America. For anyone interested in sustainability and infrastructure, this one’s worth keeping an eye on.

- Copart (NASD: CPRT): this American company runs one of the world’s largest online vehicle auction platforms, specializing in salvage cars from accidents and natural disasters. It sells on behalf of insurers, dealerships, rental companies, and individuals. Copart earns revenue through transaction fees, storage, transportation, and listing services. Its digital model, global buyer network, and asset-light approach support strong margins and steady growth. With no long-term debt and rising tailwinds from vehicle values and insurance claims, it’s a steady growth story that’s earned a spot on my radar.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated July 25, 2025.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!