Inflation and pricing

It was a relatively quiet week for the markets in terms of economic news. In the USA, investors focused on the mid-week release of the minutes from the Federal Reserve’s (Fed) last Federal Open Market Committee meeting and Fed Chair Jerome Powell’s speech at the Jackson Hole Economic Symposium, at the end of the week. These two events are crucial in indicating whether the Fed plans to lower the US benchmark rate at their September meeting.

In Canada, the biggest economic headline was the July Consumer Price Index (CPI) inflation report, which reveals whether inflation is rising or falling. Spoiler alert: it is still falling. 😊 But here is an important point—just because inflation is down does not mean prices are lower. It only means that the pace of price increases has slowed.

For example, if a product costs $10 with inflation at 4%, it will cost $10.40 a year later. If inflation stayed at 4%, it would cost $10.82 in another year. However, if inflation fell to 2% in that second year, the product would cost $10.61. So, while the price is still higher, it is not as high as it would have been if inflation had remained at 4%.

Many people confuse inflation with prices. Price is the amount of money required to purchase a good or service at a specific time, while inflation is the rate at which the general level of prices for goods and services rises over time, leading to a decrease in the purchasing power of money. The key difference is that price is about the cost of individual items, while inflation reflects the overall trend of rising prices across the economy. Inflation impacts most goods and services, but a change in price alone does not necessarily indicate inflation.

So, the next time you hear a friend wonder why prices are higher if inflation is down, you will be able to tell them. 😊

Get comfortable—this week’s update is a bit longer than usual. In addition to discussing a few starter investing strategies, I will explain why I invested in three companies after the market dip triggered the buy orders I placed last week. Now, let’s dive into what happened this past week….

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, The importance of railways, Beginner-friendly investment strategies, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Consumer price Index (CPI)

Statistics Canada’s July CPI data revealed a 0.4% rise in prices, aligning with expectations after a 0.1% decline in June. On a year-over-year basis, inflation slowed to 2.5% from June’s 2.7%, marking the slowest pace since March 2021. Core CPI, which strips out volatile food and energy prices, also saw a 0.4% increase in July after remaining flat in June. Annually, core inflation decelerated to 2.7% from 2.9%.

Gasoline prices led the monthly gains with a 2.4% increase, while the biggest decline was in the ‘Clothing and footwear’ category, down 0.6%. On an annual scale, ‘Shelter’ costs (including mortgages and rent) saw the steepest rise, up 5.7%, whereas ‘Clothing and footwear’ continued to drop, falling 2.7%.

Both headline and core CPI have remained within the Bank of Canada’s target range of 1% to 3%, and this latest data confirms the downward trend in inflation. This trend strengthens the case for another 0.25% rate cut at the central bank’s September meeting, as their focus shifts from battling inflation to supporting a cooling labour market. Best of all, BoC Governor Tiff Macklem has suggested more rates are coming if inflation continues to fall.

Canadian market volatility

Canada’s Volatility Index (CVIX) began the week at 11.62, spiked to 14.91 on Thursday, and ended the week at 11.04, slightly below its starting point. The spike was driven by concerns about a weaker-than-expected US economy, but signals from the Fed about a likely September rate cut quickly eased investor worries, causing the CVIX to drop as swiftly as it had risen.

Tracked as the VIXI on the Toronto Stock Exchange (TSE), the CVIX measures expected market volatility. A reading below 10 indicates a calm, stable market, while a range of 10 to 20 suggests moderate volatility and typical market fluctuations. Readings above 20 point to high volatility and significant market uncertainty.

Retail Sales

June’s retail sales data showed sales were lower in four of nine subsectors, resulting in an overall decline of 0.3%, a slight improvement over May’s 0.8% drop and in line with analyst expectations. On an annual basis, retail sales inched up by 0.2%.

Breaking it down, ‘Food and beverage retailers’ saw the largest monthly increase at 1.2%, while ‘Motor vehicle and parts dealers’ experienced the steepest decline, down 2.1%. Year-over-year, ‘Health and personal care retailers’ led with a 5.1% gain, whereas ‘Sporting goods, hobby, musical instrument, book, and miscellaneous retailers’ faced the largest drop, down 4.3%.

Core retail sales—which exclude gasoline stations and motor vehicle and parts dealers—rose 0.4% in June, mirroring May’s growth. Annually, core sales increased by 1.2%.

Overall, the report suggests consumers are still feeling the pinch of higher interest rates, leading to reduced spending, particularly on high-end and discretionary items. However, there is a silver lining: preliminary estimates hint at a 0.6% retail sales increase for July, and the BoC is expected to cut interest rates by another 0.25%, potentially easing the strain on consumers.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Federal Open Market Committee (FOMC) minutes

The minutes from the July 30-31, 2024, FOMC meeting were released this past week, shedding light on the committee’s discussions and providing key insights into their outlook and plans.

FOMC members observed that financial conditions had eased since their last meeting, with investor optimism about a potential September rate cut fueling a stock market rally. The American economy continued to advance but at a slower pace compared to late 2023, marked by a cooling labour market and a still elevated, though easing, inflation rate. Both the Personal Consumption Expenditures (PCE) index and core PCE were under 3.0%, showing progress toward the FOMC’s 2% inflation target. Globally, economic growth slowed, largely due to a downturn in China.

While inflation has eased over the past year, it remains above target. Recent data indicating progress toward the 2% goal and a slowdown in core PCE components boosted members’ confidence in continued inflation decline. They also noted an easing labour market, with slower wage growth and GDP growth decelerating from late 2023. Although the risk of higher inflation has diminished, employment risks have increased.

Despite some members suggesting that recent inflation progress and higher unemployment might justify an immediate 0.25% rate cut, the consensus was to hold the federal funds rate at 5.25% to 5.5% and continue reducing the Fed’s securities holdings. Officials agreed to closely monitor incoming data, especially on inflation, before considering any rate adjustments.

Overall, the Fed aims to balance controlling inflation with maintaining economic stability. A “vast majority” of Fed members believe that if economic data continues to support their expectations, a rate cut is likely at the September meeting.

Fed ready to lower rates

Fed Chair Jerome Powell strongly hinted at upcoming interest-rate cuts, signaling the Fed’s shift toward supporting the American labour market. In his speech at the Jackson Hole conference, Powell emphasized that the time has come to adjust policy to prevent further weakening of the job market. His remarks immediately impacted the markets, causing all indexes to rise.

Powell’s comments suggest that the Fed’s aggressive inflation-fighting stance may be winding down, paving the way for rate cuts as early as mid-September. Investors are now debating the size of the potential cut, with some expecting a 0.25% reduction, while others anticipate a 0.5% cut. Despite his clear message, Powell remained non-committal about the specifics, leaving the door open for larger cuts if labour market conditions deteriorate further.

As the September meeting approaches, the Fed will continue to closely monitor incoming data, including the August jobs report and inflation readings. Powell’s shift in tone emphasizes the Fed’s readiness to support economic growth and achieve price stability, hinting that the much-anticipated rate cuts are on the horizon.

American market volatility

The CBOE Volatility Index (VIX), often dubbed the market’s “fear gauge,” rose from 14.8 to 18.03 in the middle of the week before ending the week at 15.79. The market was spooked by thoughts of a recession when a revised labour report showing new jobs in March were over 818,000 less than originally reported. However, comments from Chair Powell indicating rate cuts were on the horizon calmed the market.

The VIX measures expected market volatility over the next 30 days, with readings below 12 indicating a calm and stable market, while values between 12 and 20 suggest normal fluctuations. Levels between 20 and 30 reflect heightened volatility and uncertainty, and readings above 30 signal extreme stress, typically seen during crises.

The importance of railways

This past week, Canada’s fragile economy almost took a crippling blow when Canada’s two largest railways – Canadian National Railway (TSE: CN) and Canadian Pacific Kansas City Limited (TSE: CP) – were locked out early Thursday morning. It was the first time both railways have had simultaneous work stoppages. Usually contracts between the union and the companies occur a year apart but CN asked for and received a year long extension of their old contract. I am sure the union was happy to oblige, realizing the leverage this would give them. Both companies’ contracts expired at the end of December and negotiations have been ongoing since then. The main obstacles were scheduling, availability of labour and demands for better work-life balance.

As the second-largest country by territory – Canada relies heavily on rail to ship product across the country. As well, approximately 30,000 commuters in Vancouver, Toronto and Montreal rely on the rail service to get to and from work daily. Not only would a stoppage be hard on Canadians and the Canadian economy, but it would also disrupt the US as CN and CP carry millions of tons of goods and commodities across the border. Both railroads continued to operate in the US and Mexico, but the stoppage in Canada could disrupt North American and global supply chains.

Canada sends 75% of its exports to the US, with C$114 billion in freight moved between the two countries by rail last year. A prolonged stoppage would severely impact key industries like agriculture, mining, energy, retail, automaking, construction, and chemicals, including 60% of the chlorine used by water-treatment plants across the western US. The Canadian Chamber of Commerce warned that halting both railways could disrupt $730 million in goods daily. Analysts estimate that a two-week stoppage could slash C$3 billion from Canada’s GDP, with losses escalating the longer it continues. Even a brief disruption would still cost the economy over C$2 billion per week.

Realizing the risk to the economy and that the union and the company were not close to an agreement, the Canadian government stepped in less than 17 hours after the stoppage began and ordered the Canada Industrial Relations Board (CIRB) to issue a back to work order. CIRB will work with both sides before issuing final binding arbitration. Both companies should be able to resume operations “within days.” Until new contracts are reached, both railways will operate under the current collective agreement.

However, just as the railways were set to resume operations, CN was served with a 72-hour strike notice by the union, adding a new layer of uncertainty. Meanwhile, the union representing CP workers is challenging the legality of the government’s directive to move all parties to final binding arbitration. While both railways plan to resume operations soon, pickets remain in place as the unions review their legal options. For now, the railways appear to be back on track 😊, but the situation remains fluid, and the economy may yet face more than just a glancing blow.

From an investor’s point of view, CN’s importance to Canada’s infrastructure adds another layer of security to the investment. The federal government is likely to support and invest in maintaining and expanding critical infrastructure, including implementing favorable policies and regulations to ensure the railways keep rolling. My investment in CN continues to chug uphill, paying off quarterly dividends along the way. 😊

What are some beginner-friendly investment strategies?

If you are new to investing, here are some straightforward and low-risk investment strategies that you can use to build a solid foundation:

- Index Funds and ETFs:

- Index Funds: These are mutual funds designed to track the performance of a specific index, like the S&P 500.

- Exchange-Traded Funds (ETFs): Like index funds but traded on stock exchanges, ETFs offer flexibility and can track a variety of indexes or sectors.

- Investing in index funds or ETFs can be a low-cost, diversified, and efficient way to participate in the growth of the stock market, making them an excellent choice for building a stable investment portfolio.

- Dollar-Cost Averaging and Automatic Investment Plans:

- Dollar-Cost Averaging: Invest a fixed amount at regular intervals, regardless of market conditions. This strategy helps reduce the impact of market volatility and lowers the average cost per share over time.

- Automatic Investment Plans: Set up automatic contributions to your investment accounts, aligning with the dollar-cost averaging approach. This habit ensures you regularly invest without needing to time the market, helping you build your portfolio consistently.

- Diversification:

- Spread your investments across different asset classes (stocks, bonds, real estate) and sectors to reduce risk. For stocks, consider a mix of growth stocks for high potential returns and dividend stocks for regular income. Diversification helps protect your portfolio from significant losses if one investment underperforms.

- Robo-Advisors:

- Automated platforms create and manage a diversified portfolio based on your risk tolerance and goals. They offer a hands-off approach with typically lower fees compared to traditional financial advisors. While I have not used a robo-advisor personally, they can be effective for some investors.

- High-Yield Savings Accounts:

- For a safe place to park your money, high-yield savings accounts offer better interest rates than traditional accounts. They are liquid and government-insured. For example, I have cash in Portfolio 1 parked in a TD Investment Savings Account with a 4.05% interest rate as of August 23, 2024, while I decide where to invest next.

- Dividend Stocks:

- Investing in dividend-paying stocks can provide regular income and potential for capital appreciation. Focus on well-established companies with a history of stable or growing dividends. It always feels good to see a steady stream of cash coming into one’s account, even when the markets are down like in 2022. 😊

- Bonds:

- Bonds are debt securities issued by governments or corporations, offering regular interest payments and return of principal at maturity. They are generally less volatile than stocks and provide steady income. While I do not currently hold bonds, if I were to add a bond component, I would add a bond ETF for diversification and lower risk.

- Educational Resources and Financial Literacy:

- Invest time in learning about basic investment principles, such as asset allocation, risk tolerance, and market fundamentals. I regularly read investment books and newsletters to gain new perspectives and avoid common mistakes.

These strategies can help you start investing with confidence, minimizing risk while building a diversified portfolio suited to your financial goals.

Weekly Market Review

Monday: Strong economic data from last week helped ease investors’ fears about the health of the US economy, sending all four indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – higher. Investors to appear to be fully recovered from the jitters they had at the start of August. Oil prices edged lower on concerns of lower demand from China, the world’s second largest economy, and the prospect of a ceasefire in the Middle East.

In Canada, the TSX advanced for the eighth straight day and set a record high because of higher commodity prices and investor optimism over potential US rates cuts. In trading, Basic Materials (miners and fertilizer manufacturers) advanced the most, while Consumer Staples dropped the most.

In the US, the S&P and Nasdaq recorded their eighth consecutive day of gains, the longest winning streak this year. The S&P and DJIA are now back to near their record highs set in July. Investors are now looking towards Friday, when Fed Chair Jerome Powell speaks at the annual Jackson Hole meeting of central bankers, economists, financial market participants, and policymakers from around the world to discuss global economic issues. Investors are hoping for signs the Fed is prepared to start lowering interest rates. In trading, all sectors advanced, led by Technology, with Consumer Staples trailing the others.

Tuesday: investors took a breather and booked some profits, sending all four indexes lower after an impressive 8-day win streak by the TSX, S&P and Nasdaq, and a 7-day win streak by the DJIA. Oil prices declined as investor concerns over Middle East supply eased.

In Canada, lower oil prices and the looming threat of a railway strike by both of the nation’s major railways, which could severely impact the fragile economy, weighed heavily on the TSX. In trading, Basic Materials gained the most, while the Energy sector fell the farthest.

In the US, the Consumer Staples sector advanced the most, while Energy lost the most.

Wednesday: after a brief pause yesterday, the markets continued their upward journey, pushing al four indexes into the green. Minutes from the last meeting of the Fed showed a majority of members favoured a rate cut in September. Oil prices fell when a revised US jobs report showed the US added a lot less jobs than originally thought, outweighing news of lower US oil inventories.

In Canada, the TSX closed at a record high as the possibility of a rate cuts in Canada and the US outweighed concerns of a possible rail strike that would cripple the Canadian economy. In trading, the Technology sector advanced the farthest while the Energy sector had the biggest decline.

In the USA, it was a day of broad-based gains, led by the interest rate sensitive Consumer Cyclicals sector. Energy and Financials were the only sectors to fall.

Thursday: a downward revision of US labour data from March 2024 that saw 818,000 fewer jobs than originally reported spooked investors, causing all four indexes to end the day in the red. Oil prices rose on expectations of an interest rate cut and a decline in US oil inventories.

In Canada, the TSX fell as a lockout at Canada’s two biggest railways threatened to severely damage Canada’s already shaky economy as well as disrupt North American supply chains. In trading, the Industrials sector posted the biggest gain, while the Basic Materials sector recorded the biggest loss.

In the US, investors appeared to be taking profits, particularly from technology companies, as they prepare for tomorrow’s speech from the head of the Fed, Jerome Powell. Investors are looking for signs that the Fed will lower rates in September and signal that the Fed will be entering a rate cutting phase. In trading, Financials saw the biggest increase, while Technology suffered the deepest decline.

Friday: ‘the time has come.’ With these four words, Fed Chair Powell signaled the Fed’s decision to begin lowering the US benchmark interest rate – a move that sparked widespread optimism and sent market indexes soaring. Oil prices jumped on news of an upcoming rate cut.

In Canada, the TSX surged to a record high following Mr. Powell’s remarks. Lower rates are especially favorable for the Financials sector, which makes up 29% of the TSX’s weighting. On Bay Street, all sectors were in the green, with Healthcare leading the charge, while Consumer Staples lagged the rest.

In the USA, a rate cut, and the possibility of additional rate cuts this year sent the indexes soaring. In trading on Wall Street, all sectors ended higher, led by Consumer Cyclicals with Consumer Staples trailing the pack.

Weekly Market and Portfolio Review

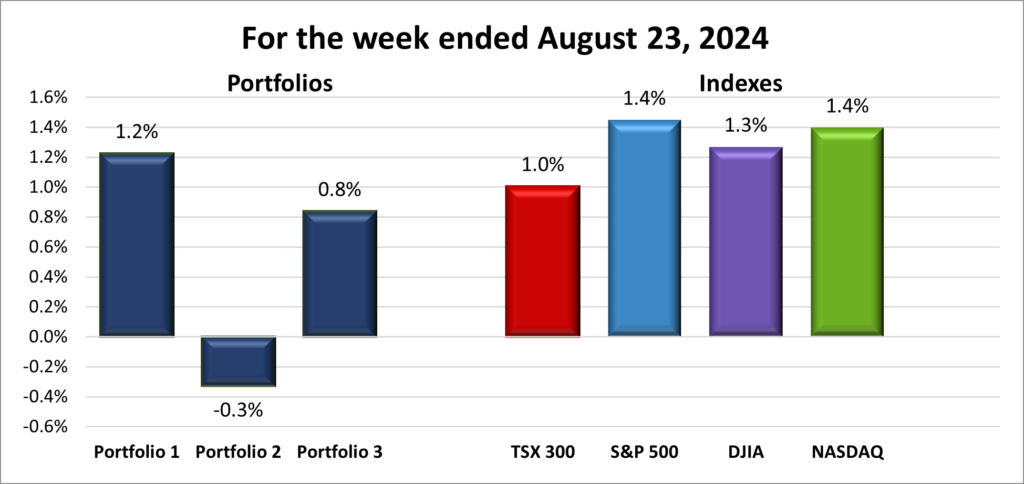

For the week, the TSX (SPTSX) rose 1.0%, the S&P 500 (SPX) advanced 1.4%, the DJIA (INDU) gained 1.3% and the Nasdaq (CCMP) climbed 1.4%.

| Index | Weekly Streak |

| TSX: | 3 – week winning streak |

| S&P: | 2 – week winning streak |

| DJIA: | 2 – week winning streak |

| Nasdaq: | 2 – week winning streak |

![]() After the best week of the year, the markets kept their momentum going, with all four indexes finishing in the green—though not quite matching the previous week’s stellar gains. The indexes moved in sync, driven by the release of the FOMC meeting minutes and Fed Chair Jerome Powell’s much-anticipated speech at the Jackson Hole Economic Symposium.

After the best week of the year, the markets kept their momentum going, with all four indexes finishing in the green—though not quite matching the previous week’s stellar gains. The indexes moved in sync, driven by the release of the FOMC meeting minutes and Fed Chair Jerome Powell’s much-anticipated speech at the Jackson Hole Economic Symposium.

Sifting through the minutes, investors zeroed in on the Fed’s apparent shift in priorities. The minutes revealed a growing focus on maintaining a strong economy and labour market, rather than solely combating inflation. This switch in focus was taken as a clear signal that a rate cut in September is almost certain. Powell further reinforced this outlook during his speech at Jackson Hole, emphasizing the Fed’s commitment to preventing further weakening in the American labour market—a strong indication that their inflation-fighting campaign may be winding down.

As markets positioned themselves for the Fed’s first rate cut in over four years, attention has now turned to the question on everyone’s mind: How deep will that first cut be? And, perhaps more importantly, how many more might follow before the year is out?

| Portfolio | Weekly Streak |

| Portfolio 1: | 2 – week winning streak |

| Portfolio 2: | 1 – week losing streak |

| Portfolio 3: | 3 – week winning streak |

![]()

![]() By the close of Thursday, it looked like all three portfolios were heading for a weekly loss. However, a market rally on Friday lifted two of them out of the red and into the green.

By the close of Thursday, it looked like all three portfolios were heading for a weekly loss. However, a market rally on Friday lifted two of them out of the red and into the green.

Portfolio 1 was the standout performer, with an impressive 76% of its holdings increasing in value. The portfolio’s rise was driven by solid overall performance across its companies, rather than a few significant gains (like those seen in 2023 with Nvidia (NASD: NVDA) and other big technology companies).

Portfolio 2 could not quite bounce back from Thursday’s dip. Even though 56% of its holdings, including the recent additions of Whitecap and Birkenstock, posted gains, it was not enough to lift the portfolio into positive territory. It just goes to show that a majority of companies posting weekly gains does not always guarantee a positive finish for the portfolio.

Portfolio 3 mirrored Portfolio 1’s strong finish, extending its weekly win streak to three. Like the other portfolios, it saw no major gains or losses, but 77% of its companies notched a weekly gain.

Overall, it was a good week – not as strong as the previous one, but as Meatloaf said, “two out of three ain’t bad.” That said, I would still prefer all three ending the week in the win column. 😊

Companies on the Radar

This week, I finally trimmed down my Radar List, making room for new opportunities. Whitecap Resources (TSE: WCP), Birkenstock Holding plc (NYSE: BIRK), and Kelly Partners Group (OTCM: KPGHF) have graduated from the Radar List and found their place in my portfolios. Whitecap and Birkenstock are now comfortably settled in Portfolio 2, while Kelly Partners has joined the ranks of Portfolio 1.

This week, I finally trimmed down my Radar List, making room for new opportunities. Whitecap Resources (TSE: WCP), Birkenstock Holding plc (NYSE: BIRK), and Kelly Partners Group (OTCM: KPGHF) have graduated from the Radar List and found their place in my portfolios. Whitecap and Birkenstock are now comfortably settled in Portfolio 2, while Kelly Partners has joined the ranks of Portfolio 1.

As we bid farewell to these three companies on the radar, a new contender has caught my eye—Payfare Inc. (TSE: PAY). This small-cap Canadian company is making a splash in the gig economy with its instant payment and digital banking solutions for gig workers across North America, giving them immediate access to their earnings. With the gig economy booming, Payfare’s innovative approach has piqued my interest, and I am excited to dive deeper into what they have to offer.

Payfare now joins the three remaining companies on my radar list, which are listed below:

- Equitable Bank (TSE: EQB), a mid sized (when the number of outstanding shares times the shares prices is between $2 billion to $10 billion) Canadian bank, considered Canada’s 7th bank, which provides financial services to consumers and businesses.

- On Holding AG (NYSE: ONON), a medium cap Swiss company, founder-run, sports products company.

- Vertiv Holdings (NYSE: VRT), a large American company that designs and builds infrastructure and continuity solutions to businesses around the world.

The Radar Check was last updated August 23, 2024.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended August 23, 2024: UP ![]()

- General Motors (NYSE: GM) announced they were laying off over 1,000 employees following a review of their operations. The layoffs will be from their software and service units.

in other GM news, the company agreed to recall 1,200 of their Cruise electric vehicle robotaxis to address hard braking problems. By voluntarily recalling the vehicles, the National Highway Traffic Safety Administration agreed to close the investigation into the issue.

With that investigation out of the way, GM and Uber (NYSE: UBER) announced the Cruise robotaxis will be available on the Uber platform starting next year. Uber riders will then be able to select a Cruise vehicle for their trip. - Walmart (NYSE: WMT), the largest shareholder in Chinese e-commerce giant JD.com (NASD: JD), has sold its entire stake after an eight-year investment, choosing to focus on its own Sam’s Club operations in China with the proceeds of the sale.

Elsewhere, Walmart has done a deal with Burger King to offer discounts on Burger King offerings, including a discount of 25% on any order placed via a smartphone or computer. - Rivian (NASD: RIVN) has lost another senior executive as Tim Fallon, the vice president of manufacturing operations, departs for traditional automaker Stellantis (NYSE: STLA). Fallon is the latest in a string of over six high-level departures, including at least four senior executives, who have recently left the company.

- Britain’s competition watchdog, the Competition and Markets Authority (CMA), has closed its ongoing investigations into Apple’s (NASD: AAPL) and Google’s app stores, opting to wait for new legislation governing digital markets. The CMA said once new legislation comes in, they will consider applying new laws to address their concerns.

Activity

Bought: Kelly Partners Group is a small but dynamic Australian accounting firm that has been steadily expanding by acquiring other boutique accounting firms across Australia. Founded and led by Brett Kelly, KPG has carved out a niche in the small to medium-sized enterprise (SME) segment, offering high-quality financial services that these businesses often struggle to access elsewhere. Over the past five years, KPG has consistently grown its revenue and cash flows, achieving profitability each year. This steady financial growth underscores the company’s resilience and effective business strategy, helping it build a loyal client base and a strong market position.

KPG went public on the Australian Securities Exchange (ASX) on June 21, 2017, and made its debut on the American Over The Counter Market (OTCM) on November 3, 2022, under the ticker KLLYF. This move was part of a strategic effort to increase visibility among North American investors and broaden its shareholder base. In June 2023, the ticker was updated to KPGHF to better align with its ASX ticker, “KPG,” reinforcing the company’s identity across different markets. Importantly, the shares are interchangeable, with a 1:1 conversion ratio between KPG on the ASX and KPGHF on the OTCM.

The company benefits from the ongoing demand for professional financial services, particularly among small to medium-sized enterprises (SMEs). By focusing on this niche, KPG has built a competitive edge in Australia, offering specialized accounting, taxation, and audit services. Recently, the company has also ventured into wealth management, opening new growth opportunities, and reducing risk through diversified revenue streams. KPG’s dedication to building long-term relationships with its clients has resulted in high retention rates, providing a stable revenue base and opportunities for cross-selling additional services.

What makes KPG particularly appealing is its ambition for international growth. Brett Kelly’s recent relocation to the United States is a bold move as part of the company’s plan to expand into the American market. This could be a game-changer, positioning KPG to tap into a larger client base and explore new acquisition opportunities. Kelly’s presence in the US underscores the seriousness of KPG’s expansion strategy and could significantly accelerate the company’s global growth.

However, investing in KPG is not without risks. The company’s aggressive growth through acquisitions could lead to integration challenges and financial strain if not carefully managed. As a smaller player, KPG’s limited reach beyond Australia makes it more susceptible to local economic fluctuations. The international expansion introduces new management dynamics, currency risks, and potential regulatory hurdles. Additionally, reliance on key personnel and the economic sensitivity of its SME clients add layers of complexity. Investors should also be mindful of potential concerns about valuation, market liquidity, and the impact of rising interest rates.

Despite these risks, KPG offers a compelling investment opportunity. The company’s consistent revenue growth, strategic expansion efforts, and diversified offerings make it an attractive addition to any portfolio. With a strong founder-led management team and a track record of 23 successful acquisitions, KPG is well-positioned for future growth. If the company can successfully expand its footprint in the US and other English-speaking countries, there’s significant upside potential. As KPG continues to grow, I am excited to be along for the ride. 😊

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSE: DIR.UN) DRIP

Pulse Seismic Inc (TSE: PSD) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

The Toronto-Dominion Bank

Third quarter 2024 financial results on August 22, 2024

Portfolio 2

Portfolio 2 for the week ended August 23, 2024: DOWN ![]()

- Alimentation Couche-Tard (TSE: ATD) has put in a bid to acquire larger convenience store rival Seven & i Holdings Co. (OTCM: SVNDY) of Japan, the owners of 7-Eleven stores. If the deal goes forward, it would be the biggest foreign takeover of a Japanese company and would make Alimentation the owner of roughly 100,000 convenience stores.

- The Walt Disney Company’s (NYSE: DIS) proposed joint venture with Indian media giant Reliance to create a broadcast and streaming TV powerhouse has run into a speed bump. India’s antitrust regulators is concerned that the partnership would effectively corner the market on the broadcasting rights to cricket, India’s national pastime. To close the deal, the two companies may have relinquished some of their rights to cricket broadcasts.

Activity

Bought: Whitecap Resources Inc. is a Canadian mid-cap (valued between $2 billion and $10 billion) oil and gas company, specializing in acquiring and developing petroleum and natural gas properties across Canada. Initially, the company’s attractive 7+% dividend grabbed my attention, but a closer look revealed even more compelling aspects. Despite a challenging year due to a global oil price drop, Whitecap has demonstrated resilience, with impressive revenue, net income, and earnings per share growth in previous years. Notably, it boasts a robust gross profit margin of 71% and a solid net profit margin of 22%.

The company’s strong balance sheet and substantial free cash flow offer flexibility for capital allocation, enabling share repurchases and consistent dividend payouts. Whitecap’s experienced management team, with decades in the industry, has effectively controlled costs and achieved efficient production. The company recently reported record quarterly production and plans to meet the high end of its 2024 production guidance, with further growth anticipated in 2025.

Of course, investing in Whitecap carries some risks. The energy sector’s cyclical nature and dependence on volatile oil and gas prices pose challenges, influenced by global economic conditions and geopolitical events. Additionally, the company’s plans to invest over $1 billion in property development could be impacted by fluctuating interest rates.

However, with Canadian interest rates starting to fall and expectations for a US rate cut in September, Whitecap should benefit from a more favorable financial environment. This could provide the company with the necessary resources to advance its production plans. While the dividend was the initial draw, Whitecap’s strong operational performance and production growth potential suggest that if oil prices rise, the share price could follow suit, making this an investment worth considering. 😊

Bought: Birkenstock Holding plc, a British mid-cap company, boasts a globally recognized brand with over 240 years of history. Known for its iconic sandals, the brand has become synonymous with comfort, durability, and distinctive style. Birkenstock’s ability to stay relevant across generations, appealing to both fashion-conscious consumers and those seeking functional footwear, speaks volumes about its enduring appeal.

The brand enjoys a loyal customer base that values quality and comfort, translating into consistent sales, even during economic downturns. While its sandals are the star, Birkenstock has been expanding into new product categories like boots, shoes, and accessories, opening doors to growth in untapped market segments. The company is also broadening its international presence, particularly in regions where it still has room to grow, offering significant potential for further expansion.

Birkenstock has smartly tapped into fashion trends, gaining favor among influencers, celebrities, and the public alike. This trend-driven demand, coupled with the growing focus on health, wellness, and comfort, positions Birkenstock’s products as both stylish and functional—a winning combination.

As for the financials, despite a dip in net income in 2023 due to increased tax rates and one-time expenses, Birkenstock has shown solid revenue growth, profitability, and earnings per share growth, supported by efficient operations. The management team is highly invested in the company’s success, with the CEO appointed in 2013 being the first non-family leader. Executive management holds over 8.5% of the outstanding shares, aligning their interests with shareholders.

Of course, there are risks, including potential market saturation and fierce competition in the footwear industry. Maintaining its competitive edge will be crucial, especially as consumer spending on discretionary items like footwear can be sensitive to economic conditions.

Birkenstock is a heritage brand with a strong reputation for high-quality, comfortable footwear. Its commitment to sustainability and its iconic footbed design have made it a favorite worldwide. Although the company has been around for over two centuries, it only recently became public, debuting on October 11, 2023, at $46 per share. Since then, the share price has risen by 33% as of August 23, 2024. Given the brand’s strong trajectory, I am excited to be an owner of this iconic brand and look forward to reaping the rewards. 😊

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSE: DIR.UN) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended August 23, 2024: UP ![]()

- Microsoft (NASD: MSFT) announced they will host the Windows Endpoint Security Ecosystem Summit on Sept. 10 with other cybersecurity companies, and government officials to discuss ways to improve resiliency and security for joint customers. Following last month’s network outage caused by a CrowdStrike (NASD: CRWD) software update that brought down tens of thousands of Windows systems, it is critical that these companies work together.

Activity

No significant activity to report this week.

Dividends

No dividends this past week.

Quarterly Reports

The Toronto-Dominion Bank

See report under Portfolio 1.