End of an era

On May 3, during Berkshire Hathaway’s (NYSE: BRK.B) annual general meeting in Omaha, Nebraska, Warren Buffett surprised the crowd by announcing his plan to step down as CEO at the end of 2025. At 94, the legendary investor will stay on as chair of the board, but his long-time successor, Greg Abel, will officially take the reins in 2026. The announcement caught everyone off guard – including Abel himself – with only Buffett’s immediate family in the loop beforehand.

How Buffett Transformed Berkshire Hathaway

Berkshire Hathaway began as a struggling textile business, but after taking control of the company in 1965, he transformed it into one of the most successful investment conglomerates in history, a $1.1 trillion giant. Through decades of disciplined value investing, Buffett expanded the company’s reach into insurance, railroads, utilities, consumer goods, and more. His steady hand and long-term mindset turned Berkshire into one of the most admired and studied companies in the world.

When Buffett took control of Berkshire Hathaway in 1965, Class A shares were trading at approximately $19. As of May 3, 2025, when Buffet retired, the A shares were selling for US$809,350.00 per share, a staggering increase of about 5,500,000% over six decades, vastly outperforming the S&P 500’s gain of approximately 39,000% during the same period.

To make Berkshire accessible to individual investors, class B shares were introduced in 1996. If you had purchased $1,000 worth of BRK.B shares at the IPO you would have seen your investment grow to approximately $19,635 by 2025, reflecting a compound annual growth rate of about 11% over 29 years

Buffett’s legacy as the Oracle of Omaha is built on patience, discipline, and a deep understanding of business fundamentals. His influence on investing will be felt for generations.

Meet Greg Abel, Berkshire’s Next CEO

Greg Abel, 62, was born in Edmonton, Alberta, and got his start as an accountant before rising through the ranks of MidAmerican Energy, which Berkshire acquired in 2000. He became CEO of Berkshire Hathaway Energy in 2008 and later vice chair of Berkshire’s non-insurance businesses in 2018. Known for his operational discipline and capital efficiency, Abel has been managing nearly 190 businesses across sectors like transportation, energy, and retail. Buffett once joked, “He does all the work, and I take all the bows” – a pretty strong endorsement.

Abel has already stated that Berkshire’s core approach won’t change. The company will stick to its long-term, value-driven philosophy and maintain its famously strong balance sheet – backed by over $300 billion in cash.

How the Market Reacted

Berkshire’s stock fell nearly 5% the day after Buffett’s announcement. But a drop like that isn’t unusual when an iconic leader steps away. We’ve seen similar reactions in the past:

- Apple wobbled after Steve Jobs stepped down, but under Tim Cook, it became even more profitable.

- Microsoft flourished after Satya Nadella shifted focus to cloud computing.

- Disney grew its empire under Bob Iger, acquiring Pixar, Marvel, and more.

So, while short-term uncertainty is understandable, Berkshire’s strong foundation and Abel’s experience suggest the company’s next chapter is in good hands.

Why I Finally Bought Berkshire

I initially overlooked Berkshire Hathaway. During the 2020–2021 pandemic boom, when the S&P was flying and Berkshire was lagging, I figured the company was nothing special. But the 2022 bear market humbled all three of my portfolios, while Berkshire held up better than most. That’s when I saw the value of owning a steady, diversified conglomerate that could help cushion the blow during rough patches.

While the A shares – then priced at over US$800,000 – were obviously out of reach, the B shares were within range. So, I jumped in and became a co-owner of one of the most successful companies in history. Not only has Berkshire added stability to Portfolio 1, but it’s also gained 43% in value since I bought in three years ago.

I was late to the party – but at least I saw the light. 😊

With the retirement of the person considered the world’s greatest investor out of the way, let’s shift gears and take a look at what else moved the markets this past week.

Items that may only interest or educate me ….

Canadian Economic news, US Economic news, Oil prices fall, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Labour Force Survey (LFS)

Statistics Canada’s latest Labour Force Survey showed only a modest rebound in April, with the economy adding 7,400 jobs after shedding 32,600 in March. While that slightly beat expectations for a 2,500-job gain, it barely makes a dent in the previous month’s losses. Employment was essentially flat, and although it’s up 1.3% year-over-year, the sluggish rebound highlights how much momentum the job market has lost.

The unemployment rate rose to 6.9% in April, up from 6.7% in March – marking the second consecutive monthly increase and coming in slightly higher than the expected 6.8%. Most of the losses were concentrated in ‘Manufacturing’ (-31,000) and ‘Wholesale and retail trade’ (-27,000), two sectors that often feel the pinch early when the economy starts to cool.

Wage growth held steady, with average hourly earnings up 3.4% year-over-year compared to $36.13. That’s a slight slowdown from March’s 3.6% pace, and wage gains remain uneven across sectors and demographics.

Ongoing uncertainty from US tariffs continues to weigh on a Canadian labour market that was already showing signs of weakness. While the return to job growth in April is a positive sign, rising unemployment and patchy sector gains paint a picture of a fragile recovery. As trade disruptions ripple through manufacturing and supply chains, the labour market remains under pressure. If the current trade war with the US drags on, Canada’s labour market could face its most difficult stretch in years.

Canadian market volatility

Canada’s market stress gauge – the S&P/TSX 60 VIX (VIXC) – kicked off the week on edge, opening at 22.59, just above the normal “business as usual” range of 10 to 20. But nerves settled quickly. By late Monday morning, the VIXC had dipped back below 20, and it kept easing throughout the week. By Friday’s close, it had cooled to 15.79, signalling a return to calmer investor sentiment.

For anyone just getting familiar, the VIXC is Canada’s version of a fear gauge. Readings below 10 reflect strong investor confidence, 10–20 signals normal volatility, and anything above 20 points to growing uncertainty.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

FOMC rate decision

As widely expected, the Federal Reserve held interest rates steady at 4.25% to 4.5% – the third straight meeting of the Federal Open Market Committee (FOMC) with no change. But while the rate pause was no surprise, the tone coming out of the meeting was more cautious than before.

Fed Chair Jerome Powell noted that uncertainty around the economic outlook has increased, with risks mounting on both sides: inflation could rise, but so could unemployment. One key concern? The impact of President Trump’s new tariffs, which may push prices higher while also weighing on economic growth. Some economists are already sounding the alarm on “stagflation” – a tough combination of high inflation and low growth not seen in the US since the 1980s.

Despite political pressure from Trump to lower rates, Powell made it clear that the Fed is in no hurry to adjust the benchmark rate and needs more evidence before making any moves. For now, borrowing costs will stay elevated. That means businesses hoping to expand or invest in new projects will still be staring down expensive loans. Many are expected to focus instead on cutting costs and delaying big decisions.

Higher rates and rising tariffs also mean companies face higher input costs—and unfortunately, many of those increases will likely be passed on to us consumers. If prices keep rising, we could see a pullback in consumer spending, which would slow sales growth and possibly ripple through the broader economy.

For now, Powell says the Fed is taking a “wait-and-see” approach, trying to strike the right balance between fighting inflation and avoiding a deeper economic slowdown.

American market volatility

The CBOE Volatility Index (VIX), often called the market’s “fear gauge,” started the week at 24.35 and stayed choppy from there. Unlike Canada’s volatility index, which steadily cooled, the VIX bounced around in a tight range between 23 and 25 as investors braced for the Fed’s rate decision. It briefly spiked above 25 following the announcement that rates would hold steady – but that jump didn’t last. Markets seemed to breathe a sigh of relief – especially after news of a trade deal between the US and Great Britain – and the VIX drifted lower, closing the week at a still-elevated but calmer 21.87.

For anyone new to the VIX: it’s basically Wall Street’s stress meter. Readings below 12 suggest markets are calm, 12–20 is the “business as usual” zone, and anything above 20 signals heightened anxiety.

Oil prices fall

Oil prices slipped to their lowest level since 2021 after OPEC+ announced it would start phasing out voluntary production cuts sooner than expected. For those new to investing, OPEC+ is a group of oil-producing countries – including Saudi Arabia, Russia, and others – that coordinate how much oil they pump out to help manage global prices. When they cut supply, prices tend to rise. When they open the taps, prices often fall.

OPEC+ stands for the Organization of the Petroleum Exporting Countries Plus. It is an alliance that includes the 12 OPEC members along with 10 other major non-OPEC oil-exporting nations. The group was formed in 2016 to exert greater control over global crude oil production and prices.

Since 2022, OPEC+ had been holding back nearly 5 million barrels per day to support prices. But tensions within the group flared after some members – like Iraq and Kazakhstan – pumped more than their agreed quotas. In response, Saudi Arabia is now moving to increase production, both as a warning shot and to regain control. They’ve even hinted they could raise output further if other members don’t fall back in line.

The news could bring some relief at the pumps for us consumers, but it’s not exactly good news for oil producers. After several weeks of sliding prices, oil and gas stocks started to rebound as bargain hunters stepped in – seeing lower prices as a buying opportunity. Oil prices were also helped by signs of stronger demand in China and Europe, shrinking US inventories, and rising tensions in the always-volatile Middle East.

Weekly Market and Portfolio Review

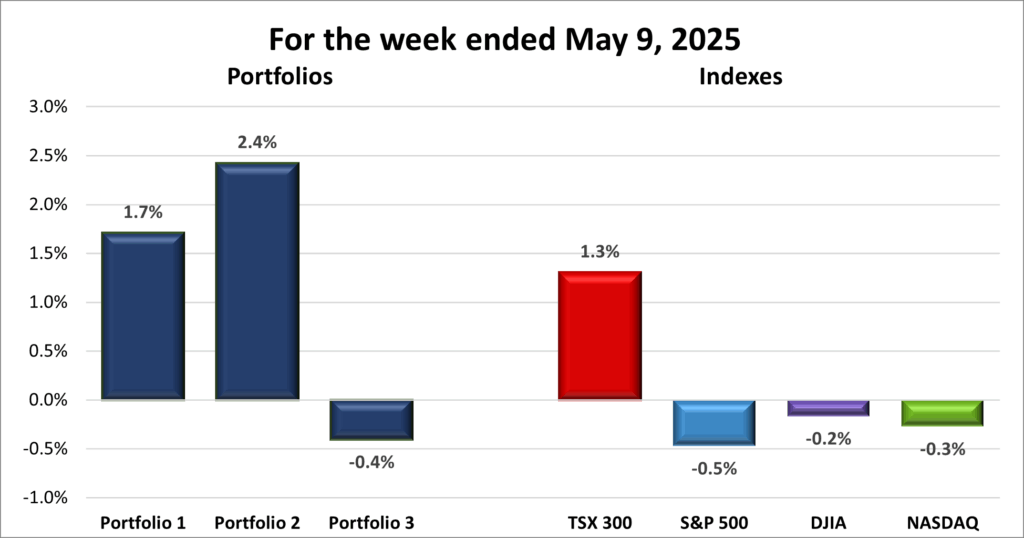

For the week, the TSX (SPTSX) advanced 1.3%, the S&P 500 (SPX) dropped 0.5%, the DJIA (INDU) dipped 0.2% and the Nasdaq (CCMP) slumped 0.3%.

| Index | Weekly Streak |

| TSX: | 5 – week winning streak |

| S&P: | 1 – week losing streak |

| DJIA: | 1 – week losing streak |

| Nasdaq: | 1 – week losing streak |

![]()

![]() To borrow from Dickens: it was a tale of two markets. The Toronto Stock Exchange (TSX) extended its winning streak to five straight weeks, while all three major US indexes – the S&P 500, Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – broke their respective winning streaks and closed the week in the red.

To borrow from Dickens: it was a tale of two markets. The Toronto Stock Exchange (TSX) extended its winning streak to five straight weeks, while all three major US indexes – the S&P 500, Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – broke their respective winning streaks and closed the week in the red.

Volatility returned in full force, fuelled by fresh trade policy shocks and the Fed’s latest interest rate decision. Tariff talk once again took centre stage. President Trump, who had already imposed sweeping tariffs on US trading partners, shifted focus to specific industries. First up: the film industry, with threats of 100% tariffs on all non-US produced movies. That announcement rattled markets, ending daily winning streaks for all three American indexes – including the S&P’s longest run in over 20 years and the DJIA’s longest since late 2023.

The threat was walked back the next day. But just as markets began to stabilize, another curveball hit: Trump said “major” tariffs on pharmaceutical imports were now under consideration – reversing an earlier exemption and injecting more uncertainty. Details are expected within two weeks.

Investor sentiment began to improve toward the end of the week after reports surfaced that senior US and Chinese officials would meet in Switzerland over the weekend. What initially looked like a low-stakes sit-down gained weight after Trump said the talks would be “more substantial than expected” and floated tariffs of 80% on Chinese goods as “about right.” A resolution still looks distant, but the possibility of progress helped ease nerves.

Also boosting sentiment, the US signed a trade deal with Great Britain – the first since the start of the trade war – raising hopes that more agreements could follow and suggesting a potential shift away from the all-out tariff approach.

The other big story was the Fed. As expected, it held its benchmark rate steady at 4.5%, even as April’s CPI showed inflation easing to 2.4%. With rates elevated for more than two years, borrowing remains expensive for households and businesses alike.

But new risks are emerging. Following the FOMC’s rate decison announcement, Fed Chair Powell warned that tariffs could reignite inflation just as growth slows – raising the risk of stagflation, the 1980s-style mix of rising prices and sluggish output. Chair Powell echoed that concern, saying the Fed would stay in “wait and see” mode for now.

If inflation proves stubborn or starts rising again, the Fed may have to choose between its two mandates: maximum employment and low inflation. For now, it’s holding the line and hoping inflation continues to drift to their target of 2%.

One bright spot for the technolgy sector: Trump announced plans to repeal artificial intelligence (AI) chip export restrictions introduced under the Biden administration. If lifted, companies like Nvidia (NASD: NVDA) could expand global sales of advanced AI chips and boost international data centre operations – a potential win for the broader tech sector. It would also help US firms maintain dominance in the global AI chip market, limiting the foothold of Chinese competitors in this rapidly growing space.

Back in Canada, the TSX got a lift from rising commodity prices – especially gold, copper, and oil – and optimism that the trade war may not drag on as long or hit as hard as feared. Some investors also expect that if the outlook worsens, the BoC will respond with rate cuts to support growth. That belief got a boost after April’s unemployment rate unexpectedly rose to 6.9%, raising fresh concerns about a slowdown and further strengthening the case for a rate cut in June.

With markets continuing to ride waves of uncertainty, it’s clear we’re not out of the woods yet. Trade tensions, stubborn inflation, and higher interest rates are all still in play – but with that uncertainty comes opportunity. As Mr. Buffett once said, “Be greedy when others are fearful” – just be smart about it. 😊

| Portfolio | Weekly Streak |

| Portfolio 1: | 3 – week winning streak |

| Portfolio 2: | 4 – week winning streak |

| Portfolio 3: | 1 – week losing streak |

![]()

![]() Despite a down week for the US markets, two of my portfolios ended in the green – a welcome surprise. You can see the full picture in the weekly returns chart below, but here’s a quick snapshot of how each portfolio fared.

Despite a down week for the US markets, two of my portfolios ended in the green – a welcome surprise. You can see the full picture in the weekly returns chart below, but here’s a quick snapshot of how each portfolio fared.

Portfolio 1 led the charge, gaining 1.7% for the week. It also had the highest number of winners, with 69% of holdings finishing in positive territory. A few names really stole the spotlight: The Trade Desk (NASD: TTD) surged 32%, Magnite (NASD: MGNI) jumped 26%, Kelly Partners Group (OTCM: KPGHF) climbed 17%, Indie Semiconductor (NASD: INDI) rose 15%, and Cameco (TSX: CCO) added 10%. The one sore spot was Docebo (TSX: DCBO), which slid 14% following disappointing first quarter earnings and investor unease over its shift toward an “AI-first” strategy.

Portfolio 2 wasn’t far behind, posting a 2.4% weekly gain with 66% of holdings in the green. Standouts included Mitek (NASD: MITK), up 19%, and Walt Disney (NYSE: DIS), up 17% – both riding high after strong earnings reports that reignited some investor enthusiasm.

Portfolio 3 was in the green at the end of Thursday but failed to hold that gain following a down day for the American indexes on Friday, posting a 0.4% weekly loss, and snapping a four-week winning streak. Still, 66% of its holdings advanced – matching Portfolio 2 – including Magnite’s 26% pop. On the flip side, goeasy Ltd. (TSE: GSY) dropped 10% after weaker-than-expected earnings and rising concerns over credit losses tied to higher delinquencies and softening economic conditions.

Overall, a surprisingly good week given the broader market. I’m happy with how the portfolios held up in a choppy stretch – here’s hoping Portfolio 3 gets back on the winning track and the winning streaks for the other two portfolios keep going next week. 😊

Companies on the Radar

It was another quiet week on my investing radar. No new companies caught my eye, and I’m still digging into the two most recent additions – LPL Financial Holdings Inc. (NASD: LPLA) and Main Street Capital Corp. (NYSE: MAIN). For now, my radar list includes just those two, along with three companies already held in one of my three portfolios.

It was another quiet week on my investing radar. No new companies caught my eye, and I’m still digging into the two most recent additions – LPL Financial Holdings Inc. (NASD: LPLA) and Main Street Capital Corp. (NYSE: MAIN). For now, my radar list includes just those two, along with three companies already held in one of my three portfolios.

- goeasy Ltd.: A mid-cap Canadian company offering non-prime leasing and lending services. Higher risk, but high potential if they manage credit cycles well.

- Dollarama (TSE: DOL): A growing large-cap Canadian discount retailer that’s also expanding into South America. With a recession expected in Canada, discount retailers are seeing an increase in business.

- Brookfield Corporation (TSE: BN): A large-cap Canadian heavyweight in alternative asset management and real estate investing.

- LPL Financial Holdings Inc.: A large-cap US firm providing a brokerage and advisory platform for independent financial advisors. Benefiting from long-term trends in wealth management.

- Main Street Capital Corp.: A mid-sized American company that invests in or lends money to smaller private companies to help them grow.

As always, these are not buy recommendations – be sure to do your own research and make decisions that align with your personal financial goals!

The Radar Check was last updated May 9, 2025.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends rising. See you next time!