A Little Less Tension on the Trade Front

Global trade tensions eased a bit this week after US President Trump and China’s President Xi Jinping met face-to-face in Busan ahead of the Asia-Pacific Economic Cooperation (APEC) summit. Trump did not attend the full leaders’ summit, but the bilateral meeting between the two leaders was the main focus for markets anyway. Going in, Trump described it as a “G2” meeting – a nod to the reality that these are the world’s two largest economies and when they talk, everyone else feels the impact. The discussion lasted over an hour and a half, and the tone afterward was surprisingly warm. Trump called it a “12” out of 10, while Xi emphasized cooperation over retaliation, saying a trade deal could bring “peace of mind” not just to their two countries, but to economies around the world.

The goals were straightforward: reduce tariffs, stabilize supply chains, and avoid escalating into something economically damaging. And there were some concrete outcomes. China agreed to resume large US agricultural purchases, including soybeans – good news for American farmers. Beijing also said it would suspend proposed export controls on rare earth minerals for at least a year, easing pressure on industries that depend on them. On the US side, Washington will scale back some tariffs on Chinese goods and hold off on planned increases.

That said, this isn’t a full resolution. Much of what was announced looks more like a temporary truce than a long-term agreement. Major sticking points – Taiwan, restrictions on advanced semiconductor technology (even though Trump did signal he’s open to future discussions about Nvidia’s (NASD: NVDA) artificial intelligence (AI) chips), and long-term control over high-value manufacturing – all are still unresolved. And as always, follow-through matters. Promises in trade talks are one thing, as we’ve seen in past negotiation rounds in Geneva and London, but consistent implementation is another.

For Canada, any easing of US-China tensions is generally positive. Our economy is closely tied to both countries through trade and global supply chains. When the two biggest players step back from conflict, it reduces uncertainty, supports demand for Canadian exports, and helps steady the markets. It doesn’t solve everything – but it does take one potential shock off the table for now.

For us investors, this meeting matters because calmer trade conditions reduce the risk of surprise tariff moves or supply-chain disruptions – both of which can hit markets hard. But the US-China relationship remains complicated, and progress in this area tends to happen in steps rather than big breakthroughs. So, while this is a bit of good news, the story is far from over. For now, though, it’s one less thing weighing on the outlook. 😊

All in all, the tension between the US and China eased off, and that helped calm some of the market nerves we’ve seen over the past few months. Now, let’s take a look at what else moved the markets this past week – and how those moves showed up in the portfolios.

Items that may only interest or educate me ….

Canadian Economic News, US Economic News, ….

Canadian Economic News

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Bank of Canada Rate Decision

As widely expected, the Bank of Canada cut its key interest rate again, lowering it by 0.25% to 2.25%, the lowest level since mid-2022. This marks the second cut in a row. The Bank didn’t commit to further cuts, but it left the door open depending on how economic conditions unfold. Governor Tiff Macklem noted that the current rate is “about right” for balancing inflation control with the reality of slower growth.

The reasoning is fairly straightforward: the Canadian economy has cooled. Exports have weakened, business investment has slowed, and unemployment has been edging higher. Inflation, meanwhile, has continued to drift toward the Bank’s 2% target. With price pressures easing and growth softening, BoC officials felt comfortable offering a bit more support to the economy.

For Canadians, the effects will vary. Those with variable-rate mortgages or loans tied to the benchmark rate may see slightly lower payments. Savers may start to notice softer returns on high-interest accounts and GICs. For investors, lower rates usually provide a modest lift to markets – especially growth-oriented sectors like technology – but it’s worth remembering that rate cuts are also a signal that the economy needs a bit of help. So this isn’t purely a “good news” moment.

What happens next depends on how inflation and growth evolve. If inflation stays contained and economic data is still soft, the Bank may continue to lower rates. If inflation starts to heat up again, the Bank could pause – meaning it would stop cutting rates for a while and hold them steady to see how the economy adjusts. And, as always, developments in the US will shape the timeline – when the America sneezes, we know how it goes. 😊

Gross Domestic Product (GDP)

Statistics Canada released new data this week showing that Canada’s economy shrank by 0.3% in August, which was weaker than expectations for flat growth. This follows an upwardly revised 0.3% increase in July, but the bigger picture is that GDP has now fallen in four of the last five months – a sign the economy is under some pressure.

The weakness came from both sides of the economy in August. Goods-producing industries fell 0.6%, weighed down by manufacturing (-0.5%) and mining, quarrying and oil & gas (-0.7%). Only agriculture and related sectors managed to hold steady. On the services side, activity dipped 0.1%, although there were some bright spots: retail trade rose 0.9%, however, management and holding companies dropped sharply.

Looking year-over-year, goods-producing industries have slipped 0.5%, with manufacturing down 3.2%, while mining and energy sectors are still holding up relatively well. Meanwhile, services are up 1.1% compared to a year ago, led by strong growth in retail (+3.8%) – though that big drop in management companies stands out there as well.

There is a bit of good news: early estimates suggest GDP may have inched up by 0.1% in September, which could mean the economy avoids a technical recession (two quarters of contraction in a row). It’s not a strong rebound, but it does hint that things may be stabilizing rather than spiraling.

Although the BoC suggested they’re finished lowering rates for now, the weaker GDP numbers make it more likely they’ll keep rates lower for longer – and if the slowdown continues, another cut could be back on the table. For us investors, a softer economic backdrop means quality matters more than ever. Companies with resilient business models, steady cash flow, and less reliance on global demand tend to hold up better when growth slows.

Canadian Market Volatility

Canada’s volatility gauge, the S&P/TSX 60 Volatility Index (VIXC), opened the week at 15.77 and spent most of the time hovering in a fairly calm range between 15.5 and 16.0, finishing at 15.55. There were a couple of quick dips, though. The index briefly fell to 13.35 after US–China trade tensions cooled, and later touched 12.32 following rate cuts from both the Bank of Canada and the Fed. But in both cases, that calm didn’t stick – the VIXC quickly moved back into the mid-15s.

For anyone new to it, the VIXC acts like a barometer of investor nerves in Canada. Lower readings (generally in the low teens) signal calmer markets, while higher levels suggest investors are bracing for more volatility. Ending the week around 15.5 suggests a bit of caution remains – but no sign of fear taking over.

US Economic News

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Federal Reserve Rate Decision

As expected by most analysts, following the conclusion of the Federal Open Market Committee (FOMC) meeting, the Fed cut interest rates by 0.25%, bringing the US benchmark rate to 3.75%–4.00%. This is the second consecutive cut. The Fed cited a slowing economy – job growth has cooled, and businesses are becoming more cautious. Inflation has been easing, but not in a straight line, and with the government shutdown still disrupting some economic data, the Fed is trying to support growth without overdoing it.

The decision wasn’t unanimous. One Fed member wanted a larger 0.50% cut to give the economy more support, while another argued for no cut at all, saying inflation isn’t where they’d like it. This is the first time since September 2019 that there were dissents on both sides, showing the Fed isn’t fully aligned on the path forward.

And that brings us to the key question investors care about: Will the Fed cut again in December? Chair Jerome Powell made it clear that another cut is possible but “not a foregone conclusion – far from it.” In other words, the Fed is watching incoming data carefully and isn’t committing to a set path.

For us investors, lower interest rates generally make borrowing cheaper for companies and consumers, which can boost spending, investment, and economic growth – a positive for markets, especially growth-focused sectors like technology. Stocks may get a short-term lift as cheaper financing improves corporate profits and makes bonds slightly less attractive. But the rate cut also signals caution: the Fed is acknowledging the economy is slowing, which can keep some investors wary.

Consumer Confidence Index (CCI)

The Conference Board’s latest CCI suggests consumer confidence is still on the cautious side. The overall index came in slightly above expectations (94.6 versus 93.4 forecast) but dipped from 95.6 last month – signalling households are treading water. The Present Situation Index moved higher to 129.3, which shows consumers generally see current business conditions and the labour market as okay for now. The flip side is the forward-looking Expectations Index, which slipped to 71.5 – well below the “80” level that often lines up with tougher economic periods ahead.

In general, people are relatively comfortable about today, but less confident about the future. Since consumer spending drives a large share of the US economy, that gap – steady present sentiment but shaky outlook – could hint at slower activity in the months ahead.

American Market Volatility

The CBOE Volatility Index (VIX) – often called the market’s “fear gauge” – began the week at 15.65 and remained fairly steady, trading mostly between 16 and 17. It ticked higher mid-week after the Fed signaled that another rate cut isn’t a sure thing and a few of the heavyweight technology companies delivered mixed earnings results. Anxiety continued to build, pushing the VIX above 18, before easing back and closing at 17.44 by week’s end.

Think of the VIX like the market’s mood ring – it shows how nervous or relaxed investors are feeling. Readings below 20 generally mean things are calmer, and that’s what we’re seeing now. Investors aren’t panicking, but they’re not overly confident either. It’s a cautious, “wait-and-see” kind of mood.

Weekly Market and Portfolio Review

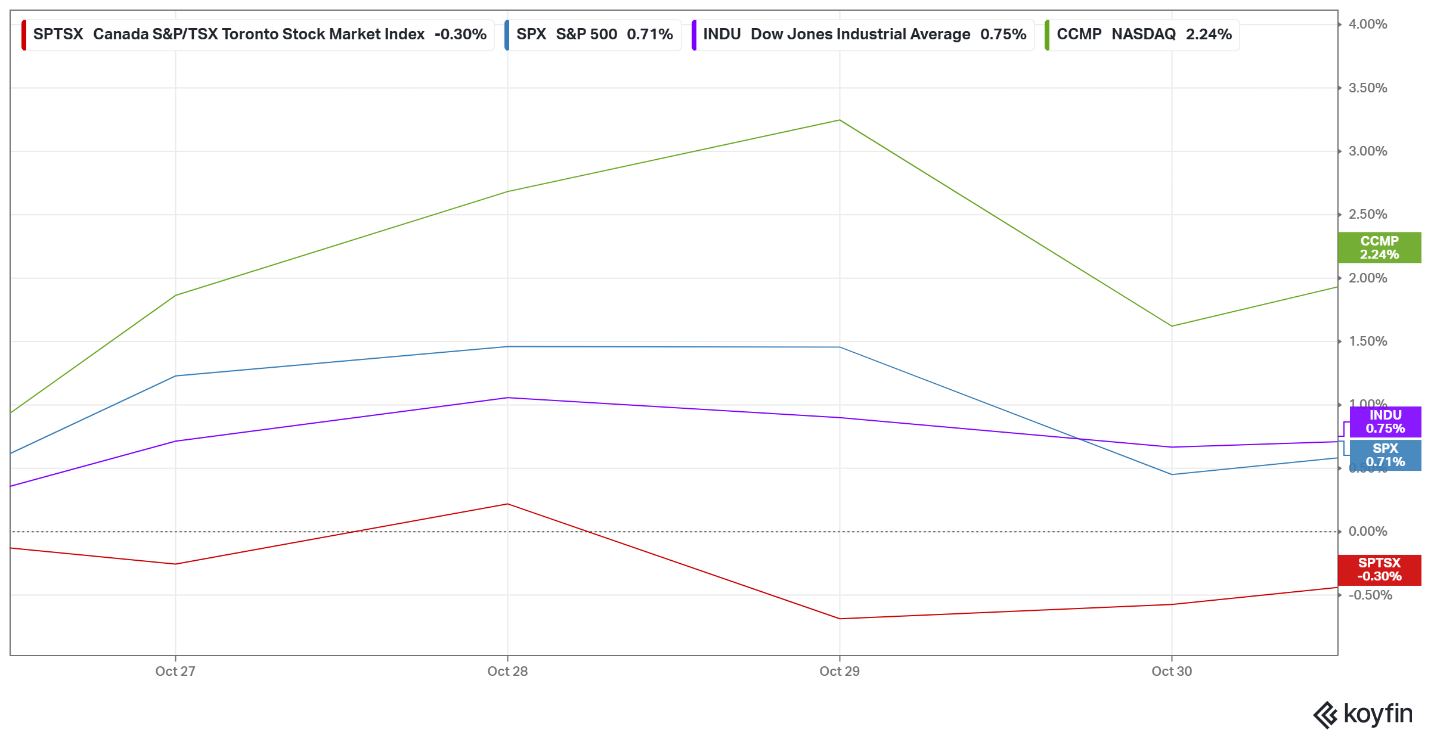

For the week, the TSX (SPTSX) slipped 0.3%, the S&P 500 (SPX) gained 0.7%, the DJIA (INDU) advanced 0.8% and the Nasdaq (CCMP) climbed 2.2%.

| Index | Weekly Streak |

| TSX: | 1 – week losing streak |

| S&P: | 3 – week winning streak |

| DJIA: | 3 – week winning streak |

| Nasdaq: | 3 – week winning streak |

![]() Overall, it was a strong week for the markets. The three major US indexes – the S&P 500 (S&P), Dow Jones Industrial Average (DJIA), and Nasdaq Composite (Nasdaq) – continued their climb, hitting multiple new record highs, with the S&P pushing above 6,800 for the first time. That strength helped offset the softer performance of the Toronto Stock Exchange Composite Index (TSX). Investors began the week on an upbeat note, looking ahead to the Fed’s latest interest rate decision and earnings from several heavyweight technology companies.

Overall, it was a strong week for the markets. The three major US indexes – the S&P 500 (S&P), Dow Jones Industrial Average (DJIA), and Nasdaq Composite (Nasdaq) – continued their climb, hitting multiple new record highs, with the S&P pushing above 6,800 for the first time. That strength helped offset the softer performance of the Toronto Stock Exchange Composite Index (TSX). Investors began the week on an upbeat note, looking ahead to the Fed’s latest interest rate decision and earnings from several heavyweight technology companies.

A cooler-than-expected US inflation report paved the way for the Fed to cut rates by another 0.25%, as widely expected. The vote wasn’t unanimous, hinting at some internal debate. While the cut was welcomed, the Fed’s message that future cuts aren’t guaranteed added a bit of caution, especially for sectors sensitive to interest rates, even as the broader market pushed higher.

Earnings were mixed. Some of the heavyweight technology companies delivered solid revenue growth but tempered their results with cautious guidance. A few large industrial and consumer companies also flagged slower demand, reinforcing the idea that the economy is still cooling.

Nvidia grabbed the spotlight, announcing it will build AI supercomputers for the US Department of Energy and reporting over US$500 billion in demand for its AI chips. This pushed its market cap past US$5 trillion, the first company to do so, and cemented its central role in the ongoing AI boom. There was also talk that President Trump would raise Nvidia’s advanced AI chips during his upcoming meeting with China’s President Xi. Meanwhile, Amazon (NASD: AMZN) reassured investors with strong growth in its cloud computing business, showing that AI-related investments by tech giants are starting to pay off. Microsoft (NASD: MSFT) also restructured its deal with OpenAI (the developer of ChatGPT), paving the way for OpenAI to go public while Microsoft keeps a 27% stake, keeping it deeply involved in the AI boom.

Globally, the tone between the US and China improved ahead of the Trump–Xi meeting. Easing trade tensions helped calm some market nerves and discussions about rolling back tariffs lifted globally exposed sectors like semiconductors and advanced manufacturing. Still, nothing has been formally agreed to, so markets are still sensitive to headlines.

In Canada, the TSX didn’t get the same boost. Gold, which had driven much of the index earlier this year, cooled below US$4,000 per ounce as easing trade tensions reduced demand for safe-haven assets such as gold. Investors shifted toward riskier bets like tech, performing strongly in the US.

The Bank of Canada also cut its benchmark rate by another 0.25% to 2.25% and hinted that this might be the last cut for a while. At the same time, it lowered its growth outlook, which added a bit of caution to the mood. With the federal budget coming next week, investors are now watching to see whether the deficit comes in higher than last year’s C$43 billion shortfall.

On the corporate front, there were bright spots. Canadian companies Cameco (TSE: CCO) and Brookfield Asset Management (TSE: BAM) announced plans to build at least US$80 billion in new nuclear reactors in the US, giving energy investors a boost.

All in all, it was a constructive week. US markets closed at record highs in four out of five sessions, while the TSX lagged a bit due to softer gold prices. Lower interest rates in both countries offered some relief to consumers and businesses. Even with a mix of optimism and caution in the air, confidence held up and the markets continued to drift higher. And with talk of OpenAI possibly going public, I’ll definitely be keeping an eye on that – it has the potential to be one of the more interesting IPOs we’ve seen in a while. 😊

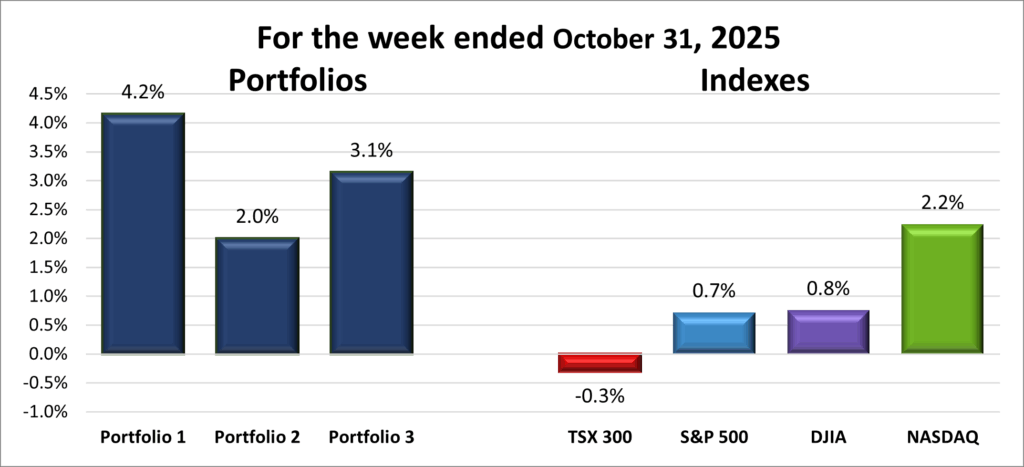

| Portfolio | Weekly Streak |

| Portfolio 1: | 3 – week winning streak |

| Portfolio 2: | 3 – week winning streak |

| Portfolio 3: | 3 – week winning streak |

![]() Despite a generally positive week in the markets, it turned out to be an especially strong week for the portfolios. Interestingly, the gains weren’t driven by broad strength across all holdings. In fact, in each portfolio, fewer than half of the companies finished the week in the green. Instead, the main driver was that many of the largest holdings had big weeks – and when your biggest positions move higher, the portfolio moves with them.

Despite a generally positive week in the markets, it turned out to be an especially strong week for the portfolios. Interestingly, the gains weren’t driven by broad strength across all holdings. In fact, in each portfolio, fewer than half of the companies finished the week in the green. Instead, the main driver was that many of the largest holdings had big weeks – and when your biggest positions move higher, the portfolio moves with them.

Portfolio 1 led the way, rising 4.2%. It also had the highest share of weekly winners at 48%. Standout performers included Cameco (+17%), Hammond Power Solutions (TSE: HPS.A) (+16%), Cloudflare (NYSE: NET) (+14%), and Celestica (+13%). On the downside, Pulse Seismic (TSE: PSD) fell 14% and Magnite (NASD: MGNI) slipped 11%, though both are smaller positions, so the impact was limited.

The real story in Portfolio 1 was the strength among its largest holdings. Seven of the top eleven positions hit new record highs, including Nvidia, CrowdStrike (NASD: CRWD), Alphabet (NASD: GOOGL), Amazon, Shopify (TSE: SHOP), Apple (NASD: AAPL), Celestica (TSE: CLS), and Cloudflare. TD Bank (TSE: TD), and Cameco also it record highs. Strong earnings, ongoing enthusiasm around AI, and positive sentiment around cloud computing all helped push those leaders higher.

Portfolio 2 came in on the lighter side this week but still gained 2.0%, just behind the Nasdaq’s 2.2% move, the top performing index. About 46% of holdings rose, with the clear standout being Guardant Health (NASD: GH) (+29%) after reporting stronger-than-expected earnings and raising full-year guidance.

Portfolio 3 landed in the middle, gaining 3.1%. Only 42% of its holdings were weekly winners, but there were still some strong performances. Cloudflare (+14%), while Vertiv Holdings (NYSE: VRT), and Shopify all set new record highs. On the other side, Lithium Americas (TSE: LAC) fell 13% and Magnite declined 11%.

Overall, this week capped off what turned out to be a surprisingly strong month – especially for a period that’s often known for volatility. The takeaway is simple: when your best companies (your strongest, highest-conviction holdings) are also your largest positions, good things happen. This week, that alignment was clear.

Here’s hoping the market momentum continues as we head into the final stretch of 2025 – historically two of the stronger months for investors. 😊

Companies on the Radar

After three new companies joined my radar list last week, there was more movement again this week – with a newcomer joining, a familiar face returning, one name moving to the back burner, and one company graduating into a portfolio.

After three new companies joined my radar list last week, there was more movement again this week – with a newcomer joining, a familiar face returning, one name moving to the back burner, and one company graduating into a portfolio.

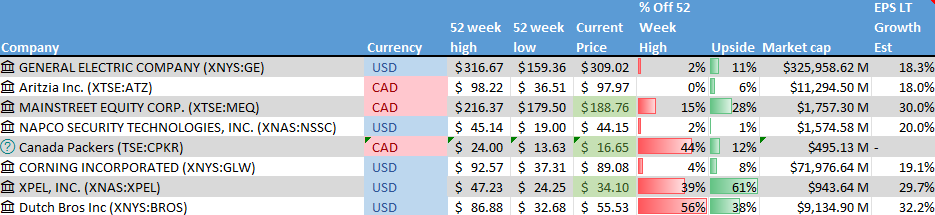

The newest addition is Canada Packers (TSE: CPKR), a small-cap Canadian company spun off from Maple Leaf Foods’ (TSE: MFI) pork business. Now standing on its own, Canada Packers is a vertically integrated pork producer focused on premium, value-added products. Maple Leaf still holds a 16% stake and has a long-term supply agreement for Canada Packers to supply its prepared-meats division. The company also plans to pay a healthy, sustainable dividend. While it’s not likely to have tech-style growth, Canada Packers could bring some welcome stability, diversification, and income potential – especially once that dividend kicks in.

Note: Because CPKR only began trading on October 2, 2025, my usual data sources (TD Direct Investing, fiscal.ai, and Yahoo! Finance) are still a bit thin – so I haven’t been able to run my full Quick Test on it just yet.

Returning to the radar is Aritzia (TSE: ATZ), the Canadian fashion retailer known for its “everyday luxury” approach – stylish, well-made women’s fashions that doesn’t hit luxury-brand price tags. Aritzia first appeared on my radar in June 2025, and it’s starting to look interesting again. After a slower period last year, the company seems to be regaining momentum, particularly in the US, where sales now account for more than half of total revenue. Strong growth from new boutiques and a thriving online channel, along with improving margins, suggests the business is back on the upswing.

With the recent pullback in gold prices, Kinross Gold (TSE: K) is moving off the radar list for now. I’ve always found gold difficult to assess – it’s heavily influenced by global factors that don’t always follow clear fundamentals. I may revisit this space later, but for the moment, I’m stepping back.

Meanwhile, Arista Networks (NYSE: ANET) has officially found a new home in Portfolio 1 (see the Portfolio 1 section below for the full write-up). It always feels good when a company makes the transition from the radar list into an actual holding. It will feel even better if it performs like Celestica. 😊

With these changes – and the remaining holdovers from last week – my radar list stays at eight. I was hoping to trim it, but when interesting companies show up… they show up. 😊

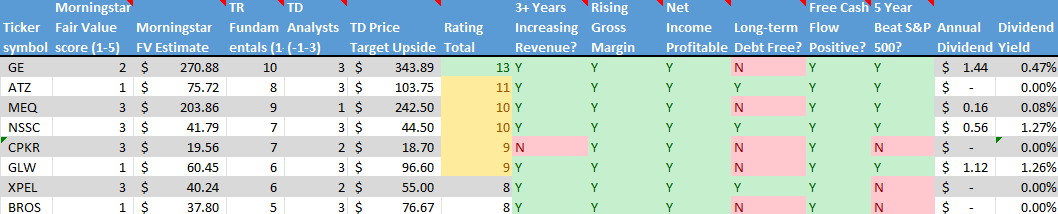

- GE Aerospace (NYSE: GE): a large American company that emerged after General Electric split into three separate businesses in 2024, and it’s been flying high ever since. The stock has surged thanks to strong demand for commercial jet engines as global air travel continues to rebound. GE Aerospace focuses on propulsion systems and services for both commercial and military aircraft and is even expanding into the fast-growing drone market. As a global leader in jet engines, aircraft systems, and MRO (maintenance, repair, and overhaul) services, it offers exposure to aviation growth, defence spending, and cutting-edge technology – a nice mix of stability and long-term growth potential.

- Mainstreet Equity Corp. (TSE: MEQ): a Calgary-based real estate company focused on mid-market apartment buildings – typically under 100 units – across Western Canada. It buys underperforming properties at below-market prices, renovates them, and increases rental income through improved operations. With strong demand for rental housing, a repeatable value-add strategy, and a solid balance sheet, Mainstreet offers a compelling mix of income and growth. Shares currently trade below net asset value, giving investors a margin of safety alongside steady cash flow and long-term upside.

- Napco Security Technologies, Inc. (NASD: NSSC): a small American owner/operator security firm that provides electronic locks, intrusion and fire alarms, access control systems, and video surveillance solutions for homes, businesses, and institutions. With a broad network of distributors and installers, growing recurring service revenue, and smart home integrations, the company has several avenues for growth. The company is riding the tailwind of an increasing demand for security products.

- Corning Incorporated (NYSE: GLW): a large cap American company that is a leader in specialty glass, optical fiber, environmental technology, life sciences, and other specialty glasses. They have been the supplier of the glass used in Apple’s iPhones since 2007, and they are riding the tailwind of an AI-driven fiber optic boom.

- XPEL, Inc. (NASD: XPEL): a growing American founder run company that produces high-quality protective films, coatings, and related products, primarily for cars but increasingly for architectural and other applications, such as paint protection film (PPF), window tint, and ceramic coatings. The company sells through multiple channels giving it both reach and control.

- Dutch Bros Inc. (NYSE: BROS): a mid-cap American company rapidly expanding its drive-thru coffee chain. Known for high-quality, hand-crafted beverages and top-notch customer service, Dutch Bros plans to open at least 160 new locations across the US by the end of 2025, aiming for over 2,000 stores by 2029. With strong brand loyalty, especially in the Western US, this is a high growth, aggressively expanding company with the potential for significant gains.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated October 31, 2025.

Portfolio Update

Portfolio 1

Bought: Arista Networks (NYSE: ANET) Arista Networks is essentially building the “highways” of the internet – especially for the big cloud and AI players. Their networking hardware and software power the massive data centres behind cloud computing, streaming, and now the AI boom. As more companies shift their operations and AI workloads into the cloud, the need for fast, reliable, and scalable networking keeps rising – and that’s exactly where Arista excels. What stands out to me is that Arista doesn’t just sell equipment once and move on; it also earns ongoing revenue through software and support contracts, which helps keep profits steady and predictable. The company has built a strong reputation for performance and reliability, and once customers adopt Arista’s systems, switching away becomes difficult – giving it a real competitive edge. Combine that with a strong balance sheet, solid profitability, and a long runway for growth as cloud and AI infrastructure continue to expand, and Arista becomes a classic “picks-and-shovels” play in one of the biggest technology trends of this decade – supplying the essential tools behind the scenes.

Of course, there are risks. A large portion of Arista’s revenue comes from just a few major customers like Microsoft and Amazon. If any of them reduce spending or shift to another vendor, the impact would be noticeable. The networking market is also highly competitive, and companies like Cisco Systems (NASD: CSCO) have the resources to push hard for market share. On top of that, Arista is viewed as a high-quality growth stock, which means the share price can be sensitive to broader market sentiment – even if the business itself continues to perform well.

After taking the time to review the fundamentals and understand the business model, I felt comfortable investing. Arista may not be the flashiest name in AI, but it plays a critical role behind the scenes – powering the infrastructure that makes AI possible. It’s a financially strong company with solid execution and a clear role in the long-term growth story of cloud and AI. For me, it’s a well-positioned, durable addition to the portfolio with lots of upside.

Sold: Skyworks Solutions (NASD: SWKS) I bought this radio-frequency (RF) semiconductor manufacturer back in January 2019, when the 5G network rollout was ramping up and smartphone demand looked unstoppable. These chips are the components that let your phone (and other wireless devices) communicate with cell towers, Wi-Fi networks, Bluetooth devices, and so on. The stock performed really well – even climbing to nearly US$200 during the pandemic – but since peaking in mid-2021, it’s been trending downward. Smartphone growth has cooled, and Skyworks remained heavily dependent on just a handful of very large customers, which made its revenues less flexible than I’d like.

As I’ve been tightening and optimizing my portfolio, Skyworks ended up near the bottom of the list in terms of long-term growth potential and compound annual growth rate. So I decided to lock in profits and redirect that capital toward areas with stronger, more durable tailwinds – such as cloud infrastructure and AI-driven networking.

And of course – right after I sold, Skyworks announced a deal to acquire a rival and become a supplier of RF chips for iPhones, just as Apple is seeing stronger sales. Sometimes timing really is everything. 😊

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!