Items that may only interest or educate me ….

US Economic news, Another thing to worry the markets, Alphabet goes to court, New Kid on the block ….

Canadian Economic news

No major Canadian economic news this past week.

US Economic news

Consumer Price Index

The Labor Department’s Consumer Price Index (CPI) Summary for August reveals that the inflation picked up the pace in August, registering a 0.6% increase compared to July’s 0.2% rise. On an annual basis, inflation accelerated to 3.7% from the 3.2% recorded in July. These increases were primarily fueled by the higher prices of oil. Meanwhile, Core CPI, which excludes the volatile food and energy components, showed a 0.3% monthly increase, slightly exceeding July’s 0.2% rise. Yearly figures for Core CPI indicate a 4.3% increase, down from the 4.7% increase reported in July.

Given that inflation remains significantly above the Federal Reserve’s (Fed) 2% target, analysts anticipate that the Fed will maintain the rate at 5.5%. However, they expect the Fed to adopt a hawkish stance on potential rate increases prior their upcoming session in November.

Consumer Sentiment Index

In its preliminary reading for September, the University of Michigan reported a Consumer Sentiment Index (CSI) reading of 67.7, marking a decline from August’s 69.5. This reading is the lowest in two and a half years but still reflects improved consumer confidence compared to a year ago when the CSI stood at 58.6. On a positive note, inflation rates have been gradually decreasing throughout 2023.

Another thing to worry the markets

A looming US government shutdown at the end of September is raising concerns in the North American stock markets. If the US Congress fails to pass a new budget by September 30 for the fiscal year starting on October 1, many government agencies could shut down or operate at reduced capacity.

The budget dispute between Democrats and Republicans revolves around spending levels, especially on social programs, with opposing views on the extent of expenditures. Contentious provisions, like those related to abortion access, add complexity to the negotiations, exacerbated by internal party politics.

The potential consequences of a government shutdown on the stock market are a cause for concern, with the extent of the impact dependent on several factors, including the shutdown’s duration and the overall economic outlook. Analysts estimate that each week of a shutdown could cut US economic growth by 0.2%.

Historically, stock markets have fared poorly during government shutdowns. The uncertainty and economic disruption they entail can lead to decreased corporate profits and declining stock prices. Moreover, a shutdown often results in reduced consumer spending, potentially causing an economic slowdown.

For us investors, we should be aware of the potential risks and prepare accordingly for potential market volatility during a government shutdown. While trying to time the market is not a good strategy, I might just sit on cash and see how this plays out. 😊

Alphabet goes to court

Recently, the Department of Justice (DOJ) opened a second antitrust case against Google (NASD: GOOGL). This case alleges that Google has unlawfully maintained a monopoly in the search engine market through exclusive agreements with device manufacturers like Apple (NASD: AAPL) and Samsung (KSE: 005930.KS), as well as internet browser makers like Mozilla, effectively making Google’s search engine the default option. The DOJ further contends that Google’s 90% share of the search market has been leveraged to impede competitors and stifle innovation. Google’s defense argues that consumers naturally choose its search engine for its quality.

The first case focuses on Google’s alleged monopoly in the digital advertising market. Here, the DOJ asserts that Google has unfairly maintained this dominance by exploiting its control over Google’s Android mobile operating system to grant its advertising products an unfair competitive advantage.

Google’s strong presence in both the search engine and digital advertising markets enables it to amass significant consumer data, giving it an edge over competitors and allowing it to charge higher advertising fees. Consequently, Google captures a substantial portion of global ad revenue displayed alongside search results.

Should Google be found in violation of antitrust regulations, it could face substantial fines and be compelled to adjust its business practices. In the most severe scenario, Google might be subject to breakup. The outcome’s implications are far-reaching, impacting Google’s business endeavors and the future of the internet. As the case unfolds, the final verdict remains uncertain.

New Kid on the block

Arm Holdings (NASD: ARM), a British-based chip design firm, this past week made its debut on the public market at a share price of US$51. Japan’s the SoftBank Group (OTCM: SFTBY), owners of Arm, made 95.5 million shares, or 10%, available to the public. This strategic move generated a substantial cash inflow of at least US$4.87 billion (calculated as 95.5 million shares multiplied by US$51 per share) to fuel Arm’s future growth even before its first share traded on the open market. This initial public offering (IPO) was the biggest and most hyped IPO since Rivian (NASD: RIVN) went public in November 2021. At the end of the first day, Arm’s share price closed up 25% at US$ 63.59, giving Arm a market value of US$ 65 billion.

Arm Holdings specializes in the design, development, and licensing of high-performance, energy-efficient semiconductors. These chips are licensed to various companies for customization and production to cater to their specific needs. Arm’s semiconductor technology played a pivotal role in the evolution of smartphones, and its applications span across mobile computing devices, artificial intelligence (AI), data centers, automobiles, and a wide array of innovative technologies. Many of the technology industry’s giants heavily rely on Arm’s chips for their innovations.

A new hot technology made its public debut this past week, a knock down court battle started and a possible US government shutdown looms just over the horizon. Let’s see what else happened this past week….

Weekly Market Review

Monday: The four indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – got the week off to a good start by ending the day in positive territory. Investors are gaining more confidence that the Fed will not raise the interest rate when they meet next week. As well, the latest economic data out of China suggested the world’s second largest economy has started to recover after a sluggish last few months.

In Canada, higher prices for commodities such as gold and copper trended higher, boosting the resource heavy TSX. In trading, the Healthcare and Technology sectors were the best performers while the Energy sector was the only sector to lose ground.

In the USA, Treasury Secretary Janet Yellen gave investors a reason to celebrate when she said she was “feeling very good” about the US avoiding a recession while continuing to bring inflation down. In trading, the top performing sectors were Consumer Cyclicals and Telecommunications Services. The only sector to end in the red was the Energy sector.

Tuesday: the TSX was the only one of the four major North American indexes to make it into positive territory. Investors are growing concerned that rising oil prices could lead to inflation remaining high, causing interest rates to remain high.

In Canada, energy companies were boosted by reports global oil supplies were tighter than thought. In trading, the Energy and Telecommunications Services sectors posted the biggest gains, while Healthcare and Technology suffered the biggest losses.

In the US, all three indexes sank as investors wait for Wednesday’s CPI data to see if consumer spending slowed down in August. In trading, the biggest gains in the American sectors came from the Energy and Financials sectors, while the biggest drops were the Technology and Consumer Staples sectors.

Wednesday: Another mixed day in the markets, with the indexes bouncing up and down before a late rally left only the DJIA in the red. Investors were focused on the latest US CPI report that showed inflation was up from last month. Investors still believe the Fed will hold steady on the key interest rate but are concerned what they might do at their next session. Oil continues its upward climb as supplies shrink thanks to recent production cutbacks by Saudi Arabia and Russia.

In Canada, the biggest gains were posted by the Consumer Staples and Utilities sectors, while the biggest declines were the Technology and Energy sectors.

In the US, the biggest IPO since Rivian in November 2021 takes place tomorrow when Arm Holdings starts trading. Arm makes many of the chips in mobile devices, including Apple and Samsung devices. In trading, leading the American sectors were Utilities and Consumer Cyclicals, while Energy and Basic Materials (miners and fertilizer manufacturers) suffered the biggest losses.

Thursday: It was a good day for the indexes, with all four sharply higher. Driving the markets higher were stronger than expected US retails sales, indicating the US economy remains strong, easing concerns of a recession in the US. Despite the higher retail sales, investors anticipate the Fed will keep the benchmark interest rate flat at their meeting next week. Tighter oil supplies and higher energy prices through 2023 and beyond have reignited fears of inflation and higher interest rates.

In Canada, higher commodity prices lifted the TSX to its highest close in six weeks. In trading, Basic Materials and Industrials led all Canadian sectors higher, while Telecommunications Services and Consumer Staples brought up the rear of the pack.

In the US, the Nasdaq received a nice bump from the debut of Arm Holdings. Otherwise, it was a day of broad-based gains in the American sectors with Basic Materials and Utilities leading the way. Trailing the pack were the Healthcare and Technology sectors.

Friday: The week ended with mixed results. Canada’s TSX was the only index to end in positive territory thanks to a late day rally. The American indexes started lower and drifted lower throughout the day, driven by concerns of slowing demand for semiconductors, as well as a strike by US auto workers. The lone bright spot was positive economic news from China that showed the world’s second largest economy gained strength in August. The good news out of China lifted energy and commodity prices.

In Canada, higher commodity prices lifted many resource companies to the benefit of the resource heavy TSX. In trading, Basic Materials and Financials posted the biggest daily gains of the Canadian sectors, while Consumer Cyclicals and Technology had the biggest losses.

In the US, the start of a strike in the US against General Motors (NYSE: GM), Ford (NYSE: F) and Chrysler owner Stellantis (NYSE: STLA) drove the three American indexes lower. Investors were concerned a prolonged strike could weaken the US economy while at the same time increase the price of cars, putting upward pressure on inflation. In trading, it was a day of declines across every American sector. The Telecommunications Services and Utilities had the shortest drop, while the Technology and Consumer Cyclicals sectors had the biggest declines.

Weekly Market and Portfolio Review

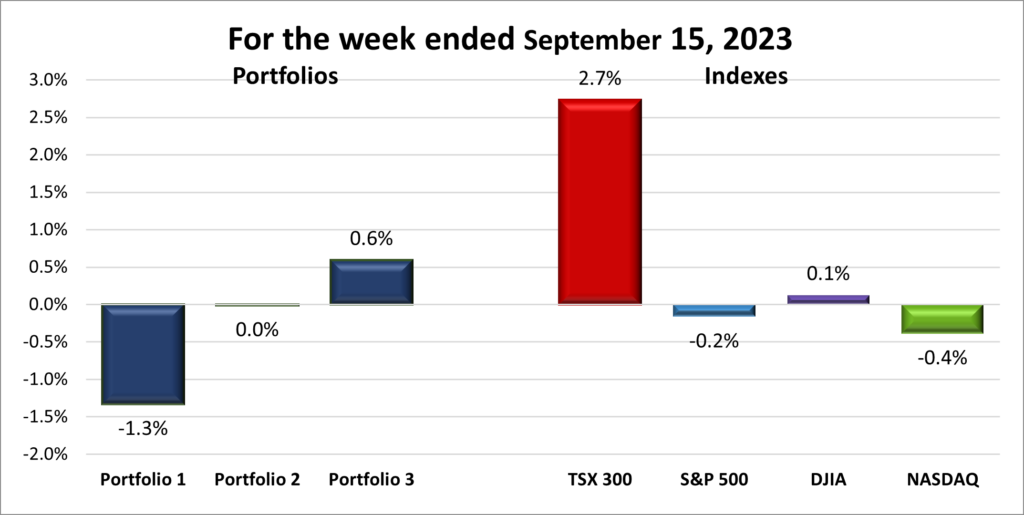

For the week, the TSX (SPTSX) gained 2.7%, the S&P 500 (SPX) lost 0.2%, the DJIA (INDU) rose 0.1% and the Nasdaq (CCMP) fell 0.4%.

![]()

![]() It was a mixed week for the major North American stock indexes. The TSX and DJIA, which lean more toward value-oriented stocks, closed the week in positive territory, while the growth-focused S&P and Nasdaq ended in the red on Friday. Several factors contributed to the market’s movements throughout the week, including an improving Chinese economy, which drove up commodity prices, optimism regarding the US economy’s ability to avoid a recession, and a mid-week boost from the Arm IPO.

It was a mixed week for the major North American stock indexes. The TSX and DJIA, which lean more toward value-oriented stocks, closed the week in positive territory, while the growth-focused S&P and Nasdaq ended in the red on Friday. Several factors contributed to the market’s movements throughout the week, including an improving Chinese economy, which drove up commodity prices, optimism regarding the US economy’s ability to avoid a recession, and a mid-week boost from the Arm IPO.

However, toward the end of the week, headwinds emerged. An autoworkers’ strike and a downturn in the semiconductor industry weighed on the three major American indexes. The semiconductor sector faced a significant setback when Taiwan Semiconductor (NYSE: TSMC) asked its suppliers to delay deliveries in anticipation of a slowdown in chip orders.

![]()

![]() When reviewing the weekly results of the indexes, I expected that all three portfolios would end the week in the red, with Portfolio 2 possibly breaking even. To my surprise, it turned out to be a mixed bag, with a positive twist to the story. 😊 Portfolio 2 held steady, as predicted. As for Portfolio 1, it ended lower as anticipated. Had the week concluded on Thursday, Portfolio 1 would have posted a decent gain. Unfortunately, the portfolio’s fortunes reversed on Friday, sending it into the red. The sharp drop in the Nasdaq knocked many of the technology companies lower, dragging down the portfolio.

When reviewing the weekly results of the indexes, I expected that all three portfolios would end the week in the red, with Portfolio 2 possibly breaking even. To my surprise, it turned out to be a mixed bag, with a positive twist to the story. 😊 Portfolio 2 held steady, as predicted. As for Portfolio 1, it ended lower as anticipated. Had the week concluded on Thursday, Portfolio 1 would have posted a decent gain. Unfortunately, the portfolio’s fortunes reversed on Friday, sending it into the red. The sharp drop in the Nasdaq knocked many of the technology companies lower, dragging down the portfolio.

The positive story was Portfolio 3 which finished the week in the green. Lifting the portfolio were strong performances from the bank stocks, Lithium Americas (TSX: LAC), and the suite of Brookfield companies. While it was not an outstanding week by any measure, it did not turn out as bad as I had anticipated. I will gladly accept the win for Portfolio 3. Let us hope that the coming week brings positive results for all three portfolios.

Companies on the Radar

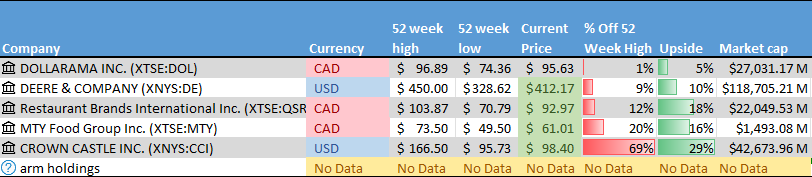

This past week, a new company briefly entered and quickly exited my radar list to a home in Portfolio 1. Arm Holdings, as mentioned in the “New Kid on the Block” section earlier, had a much-hyped initial public offering. Initially, I had not decided whether to purchase shares, but after it began trading, I found it reasonably priced for a highly rated chip company, prompting me to acquire a few shares. Aside from this addition, the same five holdovers from last week continue to remain on my radar:

This past week, a new company briefly entered and quickly exited my radar list to a home in Portfolio 1. Arm Holdings, as mentioned in the “New Kid on the Block” section earlier, had a much-hyped initial public offering. Initially, I had not decided whether to purchase shares, but after it began trading, I found it reasonably priced for a highly rated chip company, prompting me to acquire a few shares. Aside from this addition, the same five holdovers from last week continue to remain on my radar:

- Dollarama (TSX: DOL), a large Canadian company that operates dollar stores across Canada.

- Deere & Company (NYSE: DE), a large American company that manufactures and sells agricultural equipment worldwide.

- Restaurant Brands International Inc. (TSE: QSR), A large cap Canadian consumer cyclical company that operates in the North American quick serve restaurant industry. The company owns Tim Horton’s, Burger King, and Popeye’s Louisiana Kitchen, among others.

- MTY Food Group Inc. (TSE: MTY), A small cap Canadian consumer cyclical company that operates and franchises quick service and casual dining restaurants throughout North America and internationally.

- Crown Castle Inc. (NYSE: CCI), a large cap American company that owns and operates cell towers throughout America. The company is currently at its lowest price in five years and offers a 6+% dividend.

The Radar Check was last updated September 15, 2023.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended September 15, 2023: DOWN ![]()

- Tesla’s (NASD: TSLA) share price got a nice bump when it was learned that the company was building a supercomputer to facilitate artificial intelligence models for self driving cars. Investors believe the supercomputer will help Tesla expand their market reach “well beyond selling vehicles at a fixed price.”

- Apple announced their latest products this past week. Joining the Apple lineup are the new iPhone 15 and the Apple Watch Series 9. Besides more powerful processors, the company highlighted new materials, camera upgrades and new processors for improved performance to convince consumers to upgrade their smartphones. The iPhone 15 devices are the first iPhones to utilize a USB-C connector for charging, reflecting European Union regulators requirements.

- General Motors upped its offer to autoworkers to a 20% wage increase to avoid a strike, however that was not enough to stop workers from walking out from selected factories.

- France ordered a stop to the sales of Apple’s iPhone 12 after they found the devices emitted higher than acceptable radiation exposure. Apple maintains their phone are safe and are certified by multiple international agencies that the phones are compliant with radiation standards and no ill effects have been shown to be caused by them.

Activity

Bought: Arm Holdings: As introduced in the ‘New Kid on the Block’ section, Arm Holdings is a British-based semiconductor company that specializes in designing high-performance, energy-efficient semiconductors. These chips can be found in various industries, including information technology and automotive. Arm dominates the smartphone industry, powering approximately 95% of smartphones.

Financial information gathered from the prospectus shows Arm is a profitable company with a healthy balance sheet. This financial strength enables it to engage in ongoing research and development in chip designs, and strategic acquisitions if deemed necessary.

On the risk side, Arm’s revenues are heavily concentrated in a few key customers, such as Apple, although the number of customers is growing rapidly. Additionally, Arm faces competition from other chip design companies, which could pose a threat to its market share. Finally, Arm’s current high valuation leaves the door open for short-term price volatility.

Normally, I use a buy-and-hold strategy for a minimum of five years. However, my experience with Rivian, which initially saw its shares surge to $175 only to settle in the $20 to $25 range, has caused me to adopt a more cautious stance. If Arm’s share price spikes significantly, my plan is to sell. Subsequently, if there is a notable decline in share price, I would consider re-purchasing shares of Arm. If there is no substantial spike in the share price, I am content with holding the shares and watching them grow in value.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSX: DIR.UN)

BSR Real Estate Investment Trust (TSX: HOM.U)

Yellow Pages Ltd (TSX: Y)

US $

Home Depot Inc (NYSE: HD)

General Motors Co (NYSE: GM)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended September 15, 2023: FLAT ![]()

- Disney (NYSE: DIS) and Charter Communications (NASD: CHTR) came to an agreement that will see Disney’s ESPN and Disney+ services available through Charter’s subscription packages. Disney held exploratory talks with Nexstar Media Group (NASD: NXST) about Nexstar acquiring Disney’s ABC network. Separately, Media baron Byron Allen made a US$10 billion offer for ABC, including the FX and National Geographic cable channels.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

iA Financial Corporation Inc (TSX: IAG)

US $

Microsoft Corp (NASD: MSFT)

Quarterly Reports

Mitek Systems, Inc.

All currency listed in thousands of US dollars.

Selected highlights from their second quarter 2023 financial results on September 14, 2023.

- Revenue of $45,314 for the three months ended March 31, compared to $33,510 for the same period in 2022. An increase of over 35%.

- Net income of $4,448 for the three months ended March 31, compared to net income of $435 in the same period in 2022.

- Diluted earnings per ordinary share of $0.10 for the three months ended March 31, compared to earnings of $0.01 per share for the same period in 2022.

- Revenue of $91,017 for the six months ended March 31, compared to $65,982 for the same period in 2021. An increase of almost 38%.

- Net earnings of $9,178 for the six months ended March 31, compared to net earnings of $3,559 in the same period in 2022.

- Diluted earnings per ordinary share of $0.20 for the six months ended March 31, compared to earnings of $0.08 per share for the same period in 2022.

Portfolio 3

Portfolio 3 for the week ended September 15, 2023: UP ![]()

- Brookfield Asset management (TSX: BAM) has partnered with French money lender Societe Generale to create a private debt fund of ten billion Euros. Funding will be aimed at the power, transportation, and finance sectors, among others.

- European Union antitrust regulators have requested feedback from Microsoft’s (NASD: MSFT) gaming rivals regarding Microsoft’s sale of its cloud streaming rights to gain approval of Britain’s antitrust regulators for Microsoft’s acquisition of Activision Blizzard (NASD: ATVI).

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

SmartCentres Real Estate Investment Trust (TSX: SRU.UN) DRIP

US $

Microsoft Corp (NASD: MSFT)

Quarterly Reports

No quarterly reports this past week.