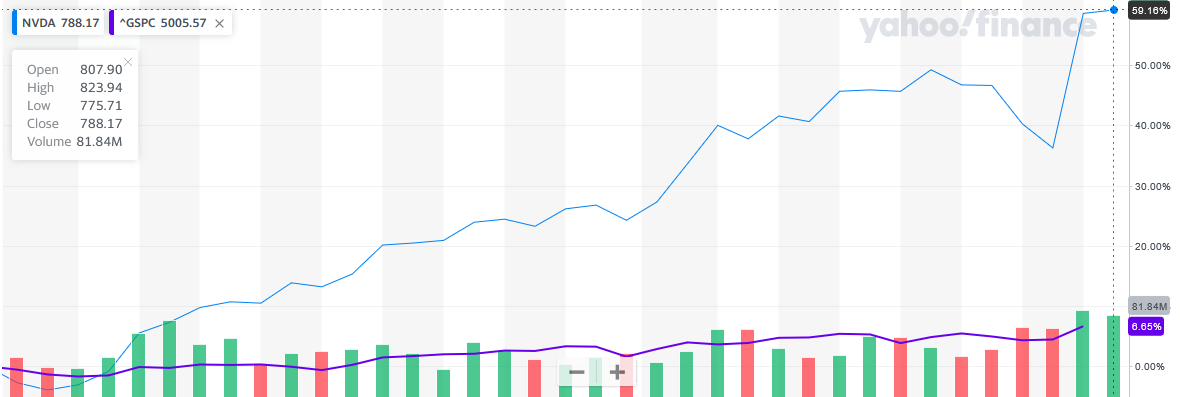

Nvidia (NASD: NVDA) had itself quite the week. Following an impressive earnings presentation, Nvidia not only surpassed revenue and net income forecasts but also offered future earnings guidance that exceeded analyst predictions. Consequently, Nvidia’s stock surged by 17% in just two days, reaching a new all-time high and increasing its market value by about $277 billion. This was the largest single-session market value gain in history. At one point, Nvidia’s valuation briefly exceeded $2 trillion, before settling just under the $2 trillion mark. This made it the third largest company by market capitalization, surpassing giants like Alphabet (NASD: GOOGL) and Amazon (NASD: AMZN).

This performance not only cements Nvidia’s status as a stock market favorite, with a 60% increase since the year began, as shown in the chart below, but also highlights the broad market enthusiasm for artificial intelligence (AI). Nvidia’s latest earnings underscore the massive demand for AI chips, as companies eager to expand their AI capabilities and catch the AI tailwind turn to Nvidia to supply the advanced chips required to run AI applications. This trend is lifting almost every company associated with AI, confirming the sector’s vibrant growth potential.

Nvidia was the principal driver of the markets this past week, but let’s see what else moved the markets this past week….

Items that may only interest or educate me ….

Canadian Economic news, American Economic news, What is Beta?, Changes ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Consumer Price Index

Canada’s January inflation rate, as indicated by the Consumer Price Index (CPI), dropped unexpectedly to below 3%, marking the first decline in seven months. With a rise of just 2.9% year-over-year, according to Statistics Canada, this slowdown from December’s 3.4% increase was below the anticipated 3.2% growth. On a monthly basis, inflation was unchanged in January after falling 0.3% the previous month.

Annually, the biggest increase was in the cost of ‘Shelter’ (rent and mortgages) which increased 6.2%, while the biggest decrease was in the ‘Gasoline,’ down 4.0%. Lower gas prices was the primary driver of the drop in CPI. Month over month, ‘Alcoholic beverages, tobacco products and recreational cannabis’ prices saw the biggest increase, up 1.1%, and the biggest decline was in ‘clothing and footwear,’ down 3.2%.

Core CPI, useful for identifying the underlying inflation trends, excludes volatile food and energy prices to offer a more stable view of inflation. This measure came in at 3.1% for the year, providing insight into the economy’s health beyond the temporary swings in food and energy costs. ‘Alcoholic beverages, tobacco products, and recreational cannabis’ had the largest annual increase within core CPI at 4.2%, while ‘Clothing and footwear’ experienced the biggest drop, decreasing by 1.3%. Month-to-month, core CPI declined slightly by 0.1% in January, indicating a stable inflationary environment when excluding these volatile categories.

This latest CPI report is a positive indicator for the central bank and the broader economy, as it brings inflation within the BoC’s target range of 1% – 3%, raising hopes for potential rate cuts. For consumers, this could translate to lower borrowing costs. For investors, it suggests that companies might have more funds for reinvestment or to return to shareholders through higher dividends and share buybacks, potentially boosting share prices. Although the next BoC meeting on March 6 is unlikely to change the current 5% rate, the door is open for adjustments in future meetings, with many eyes on June 5 as a possible date for a rate reduction.

Canadian market volatility

In Canada, the TSX 60 VIX, also known as Canada’s volatility index (VIXC) or ‘fear gauge,’ closed the week at 11.76, a slight increase from the previous week’s 10.46.

A rise in the VIXC suggests that investors are feeling a bit more nervous or uncertain about future market movements. It does not necessarily predict a downturn; it just means people are expecting stocks to be more erratic.

The VIXC gauges volatility within the Canadian stock markets, with readings above 20 generally viewed as ‘high’ and those below 20 as ‘low.’ The current reading of 11.76 sits on the lower end of the spectrum, indicating a prevailing sense of confidence among investors in the Canadian markets.

Retail sales

Statistics Canada reported a 0.9% increase in December retail sales, exceeding analysts’ expectations of 0.8%. This follows a 0.2% drop in November and reflects the typical holiday season boost. Core retail sales (excluding cars and gas) also grew by 0.5% in December, further highlighting mixed signals in the economy. However, it is too early to declare an economic rebound as preliminary January data shows a 0.4% decline, suggesting continued pressure from interest rates and inflation hovering around 3%.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Federal Open Market Committee (FOMC) minutes

The Federal Reserve released the minutes from its January 30-31 monetary policy meeting this past week. The minutes indicated that Fed officials were primarily concerned about the risks of cutting rates too soon and remained uncertain about how long to keep interest rates at their current level of 5.5%.

Reviewing economic conditions, Fed members noted that foreign growth remained sluggish, domestic Gross Domestic Product (GDP) growth slowed in Q4 2023, and the labor market remained tight while showing signs of easing. Consumer inflation had declined significantly, with both Personal Consumption Expenditures (PCE) and core PCE falling well below previous year levels, but still exceeding the 2% target.

While acknowledging progress on lowering inflation, the Fed expressed concerns that ongoing economic growth could reignite inflationary pressures. They worried that the resilient economy was limiting the effectiveness of higher interest rates in bringing inflation down to their target. Fed officials indicated they would closely monitor incoming data to assess whether inflation was on a sustainable path towards 2%. Subsequent to the meeting, recent data has shown continued job market strength and persistent inflation.

Despite slightly raising their economic outlook, the Fed remained uncertain about the future. They were concerned that lowering rates prematurely could boost demand, potentially hindering the downward trend of inflation. They forecast PCE and core PCE to decline in 2024 and return to 2% by 2026.

The minutes reinforced comments subsequently made by Fed officials in separate speeches that the Fed saw no urgency in lowering the benchmark interest rate. This cautious stance aligns with subsequent comments from Fed officials, suggesting the Fed will not start rate cuts until their June meeting.

American market volatility

Wall Street’s ‘fear gauge,’ the CBOE Volatility Index (VIX), settled at 13.75 at the end of this week. While a decrease in the VIX to 13.75 from 14.24 is not a dramatic change, it is a sign that investors are slightly less worried about market volatility than they were previously. A lower VIX value suggests that investors are feeling more confident about the stability of the market and are less concerned about significant fluctuations in the near future.

What is Beta?

No, not the Greek letter B. 😊

In the world of investing, understanding risk is crucial. Beta can be used by investors as part of their analysis to understand the risk profile of a stock or other investment compared to the overall market. But beta can seem confusing, especially for new investors. I will try to explain it in simple terms to help you understand what beta means and how to use it in your investment decisions.

I like to think of the stock markets as a bit of a rollercoaster, so I will stick with that analogy for this discussion of beta. Imagine the stock market as a giant rollercoaster. Sometimes it climbs smoothly, offering steady returns (think of a scenic uphill climb). Other times, it plunges and dips dramatically, causing sharp losses (like a wild downhill drop). Beta tells you how closely an individual investment’s ride mirrors the overall market’s rollercoaster.

Here is a break down of what the different beta values mean:

- Beta of 1: This means the investment moves roughly in line with the market. A 10% market increase translates to a similar 10% change in the investment’s value.

- Beta greater than 1: This indicates the investment is more volatile than the market. It might rise faster during market upswings but also fall sharper in downturns.

- Beta less than 1: This suggests the investment is less volatile than the market, offering potentially lower returns but also greater stability during market fluctuations.

- Beta of 0: This means the investment’s returns are not perfectly correlated with the market, like government bonds.

- Negative Beta: This is rare but indicates the investment moves opposite the market, like some inverse Exchange Traded Funds (ETFs) designed to profit when the market falls. However, negative beta also comes with its own risks, potentially underperforming during market upswings.

As well, beta can change over time, influenced by company performance, market conditions, and other factors.

If you are risk-averse, prioritizing investments with lower betas might be suitable strategy. On the other hand, if you tolerate higher risk for the potential of higher returns, consider investments with higher betas alongside lower-risk options for a diversified portfolio.

Changes to Weekly Update

In the Portfolio update section, under Quarterly Reports, revenue, net income/loss, and EPS information were included for each company’s quarterly reports. However, this lacked context and did not provide a comprehensive overview of the company’s performance.

Going forward, you will see the company name, the quarter being reported, and a link to the press release (if it contains the financial statements) or directly to the financial statements. This will allow you to gain a more complete understanding of the company’s operations beyond just the numbers.

Weekly Market Review

Monday: the Canadian markets were closed for Family Day and the American markets were closed for George Washington’s Birthday.

Tuesday: the markets started this short week off on a sour note with all four major North American indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – ending lower. This week, all eyes are on market darling Nvidia when it presents its quarterly earnings. If it misses its estimates, or provides forward guidance below analysts’ expectations, it could trigger a drop in the broader market, the technology sector in particular. Oil prices slipped lower on concerns of lower demand.

In Canada, the rate of inflation dropped more than anticipated, giving investors hope for a sooner rather than later rate cut. This good news was offset by concerns that US inflation has stalled, dashing hopes for an early rate cut. In trading, Telecommunications Services and Utilities advanced the most, while Technology and Industrials declined the most.

In the US, this week in earnings its time for many of America’s biggest retailers to show their quarterly earnings. Walmart (NYSE: WMT) got the ball rolling by beating expectations and forecast sales higher than expected. In trading, Consumer Staples and Telecommunications Services gained the most, while Technology and Basic Materials (miners and fertilizer manufacturers) dropped the most.

Wednesday: it appeared all four indexes would end in the red after minutes from the Fed’s last meeting indicated the bank was committed to not lowering the interest rate too early. However, a late rally in anticipation of Nvidia’s earnings reports lifted the S&P and DJIA into the green. Oil prices edged higher on Middle East supply concerns.

In Canada, the TSX was dragged lower by the interest sensitive Technology companies that were negatively impacted by the news the Fed was concerned about lowering the rate too soon. In trading, Energy and Consumer Cyclicals performed the best while Technology and Financials were the biggest losers.

In the USA, in aftermarket trading Nvidia did not disappoint. Revenues and earnings beat analysts estimates. As well, the company’s forecast for current quarter revenue was higher than analysts estimated. Nvidia’s share price soared, along with other AI related companies. At the end of the regular trading session, Energy and Utilities posted the biggest daily gains while Technology and Financials were the only American sectors to end lower.

Thursday: following on the heels of Nvidia’s blow out earnings report yesterday, all four indexes ended firmly in the green today. The amazing earnings report was a result of the demand for AI chips and reassured investors that the demand for AI remained strong. The upbeat mood spread throughout the North American markets, lifting markets around the world as well. Oil prices dipped after a build up of US crude oil inventories.

In Canada, the rally in technology companies in the US spread to Canadian technology companies, helping lift the TSX to a 22-month high. In trading, Consumer Staples and Industrials posted the biggest gains, while Basic Materials and Telecommunications Services were the only sector to fall back.

In America, the S&P and the DJIA closed at all time highs, with the Nasdaq just short of an all time high. The smaller sibling of the Nasdaq, the Nasdaq 100, gained 3% to close at a record high. The last time that occurred was in March 2000. Powered by Nvidia and other AI associated technology companies, the Technology sector was the big winner, followed by Consumer Cyclicals. The Utilities and Telecommunications Sectors were the only sector to end lower.

Friday: the markets ended the day mixed as the AI rally started to lose momentum in afternoon trading, causing the Nasdaq to sink into the red. Oil prices dropped after the Fed signalled it would be at least two more months before the interest rate might start to drop.

In Canada, the rally in technology companies helped the TSX overcome the drag of slumping oil companies as the TSX closed at its highest point since April 2022. In trading, Technology and Basic Materials were the top performers in the Canadian sectors, while the Utilities and Energy sectors dropped the most.

In the US, investors appeared to lock in some of the gains after the 2-day AI inspired rally. Once again, the S&P and DJIA both set new closing highs. In trading, Industrials and Utilities posted the biggest gains of the American sectors, while the Energy and Technology sectors suffered the biggest losses.

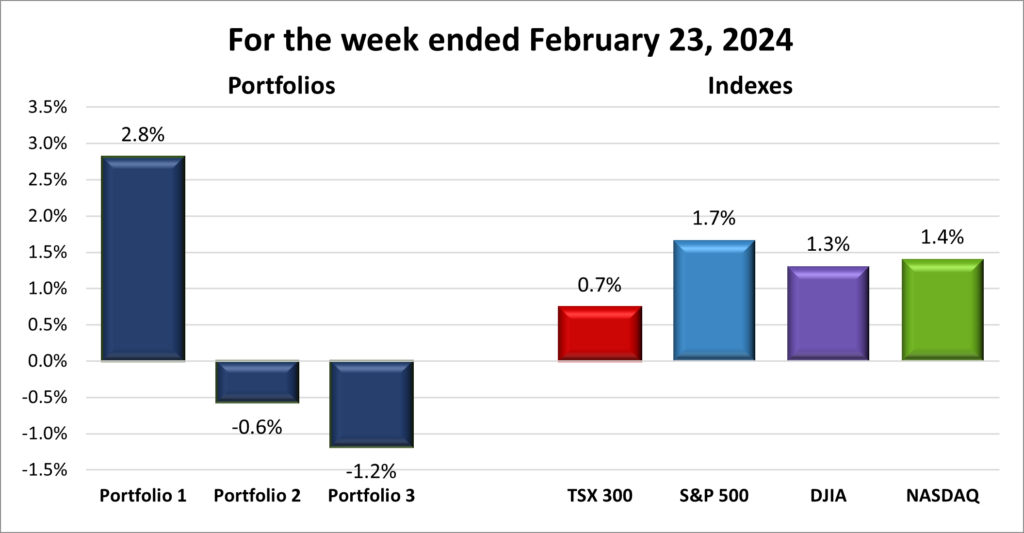

Weekly Market and Portfolio Review

For the week, the TSX (SPTSX) rose 0.7%, the S&P 500 (SPX) surged 1.7%, the DJIA (INDU) added 1.3% and the Nasdaq (CCMP) gained 1.4%.

| Index | Weekly Streak |

| TSX: | 2-week winning streak |

| S&P: | 1-week winning streak |

| DJIA: | 1-week winning streak |

| Nasdaq: | 1-week winning streak |

![]() Looking at the chart above, it’s evident the four major North American indexes had a rocky start this week, each closing below the bar on Wednesday. This downtrend was triggered by the release of the minutes from the latest FOMC meeting and comments from Fed officials that suggested the Fed saw “no need to rush” rate cuts, dampening hopes for an early interest rate cut. However, the market sentiment shifted dramatically after Nvidia announced its fourth-quarter earnings post-market closure. The company’s stellar report and optimistic forecast ignited a rally, propelling all four indexes into positive territory by week’s end.

Looking at the chart above, it’s evident the four major North American indexes had a rocky start this week, each closing below the bar on Wednesday. This downtrend was triggered by the release of the minutes from the latest FOMC meeting and comments from Fed officials that suggested the Fed saw “no need to rush” rate cuts, dampening hopes for an early interest rate cut. However, the market sentiment shifted dramatically after Nvidia announced its fourth-quarter earnings post-market closure. The company’s stellar report and optimistic forecast ignited a rally, propelling all four indexes into positive territory by week’s end.

Nvidia’s earnings not only exceeded expectations but also confirmed a burgeoning demand for AI chips among technology companies, fuelling a surge in technology stocks. This excitement drove the S&P and DJIA to new highs, with the Nasdaq nearing its record peak. Turning to Canada, the rally extended to the TSX, influenced by Nvidia’s ripple effect. However, the gains were not as large as its American neighbors because the Canadian technology sector is a much smaller component of the TSX (5.4%) than the American technology sector is in the S&P, DJIA, and Nasdaq (27.6%, 17.6%, and 48.4%, respectively).

This week, Nvidia was the star, single-handedly boosting the markets with its success. While Nvidia’s big win shines a light on the exciting possibilities in AI, I am hoping this excitement spreads beyond the technology sector and leads to broad rally across the entire market.

| Portfolio | Weekly Streak |

| Portfolio 1: | 8-week winning streak |

| Portfolio 2: | 2-week losing streak |

| Portfolio 3: | 2-week losing streak |

![]()

![]() Despite a strong performance from all four major indexes this week, the three portfolios experienced mixed results, as you can see in the chart below. Portfolio 1 managed to overcome significant losses, thanks to a stellar performance by Nvidia, while Portfolios 2 and 3 saw overall declines, hampered by a few underperformers and the absence of offsetting gains.

Despite a strong performance from all four major indexes this week, the three portfolios experienced mixed results, as you can see in the chart below. Portfolio 1 managed to overcome significant losses, thanks to a stellar performance by Nvidia, while Portfolios 2 and 3 saw overall declines, hampered by a few underperformers and the absence of offsetting gains.

Portfolio 1 experienced significant declines in several holdings, including Rivian (NASD: RIVN) down 38%, Teladoc Health (NYSE: TDOC) down 31%, Global-E Online (NASD: GLBE) down 19%, indie Semiconductor (NASD: INDI) down 19%, and Navitas (NASD: NVTS) down 14%. Docebo (TSE: DCBO) was the lone company to register a significant gain this past week, up 16%. However, Nvidia’s impressive 7% gain this week, as the portfolio’s largest holding, significantly offset these losses, demonstrating the influence a single stock can have on overall portfolio performance.

Unfortunately, Portfolio 2 did not have a Nvidia-like savior. It suffered notable declines, particularly with Supremex (TSE: SXP) down 14% and Guardant Health (NASD: GH) down 10%, without any significant gains to counterbalance these losses.

Much like Nvidia’s impact on Portfolio 1, Shopify’s (TSE: SHOP), movement tends to dictate the direction for Portfolio 3. Despite no dramatic declines, a slight downturn in Shopify, alongside minor losses across technology holdings, contributed to an overall decrease in portfolio value this week.

The Nvidia-induced rally was the highlight of the week. This week’s performance underscores the significant impact individual stocks can have on one’s portfolio. That is why its important to have a diversified portfolio. Looking forward, I am hoping the rally continues, obviously, but for it to broaden beyond the technology sector. A broad-based rally is much more sustainable than a narrow rally, especially when it is only one company driving the surge. Here is to all three portfolios posting weekly gains once again soon. 😊

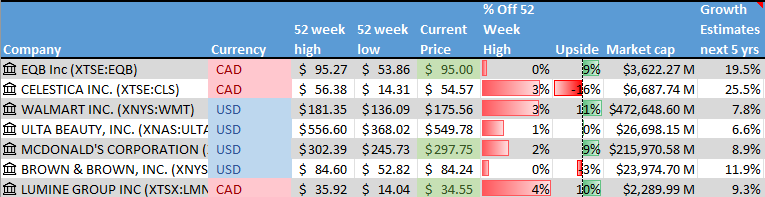

Companies on the Radar

Walmart originally caught my eye in September 2023, but it was not quite the right fit for my investment strategy at the time. That changed this week with Walmart’s acquisition of Vizio (NYSE: VZIO), pulling the retail giant back into my focus. This strategic move transforms Walmart from a traditional, low-growth consumer staples company into a potential powerhouse in the streaming and e-commerce sectors. By acquiring Vizio, Walmart not only enters the digital advertising industry but also positions itself to boost growth through ecommerce. Analysts have suggested Walmart intends to compete against Amazon in the online retail industry, indicating a possible shift towards a growth-oriented strategy. This makes it an interesting time to consider a stake in Walmart. 😊

Walmart originally caught my eye in September 2023, but it was not quite the right fit for my investment strategy at the time. That changed this week with Walmart’s acquisition of Vizio (NYSE: VZIO), pulling the retail giant back into my focus. This strategic move transforms Walmart from a traditional, low-growth consumer staples company into a potential powerhouse in the streaming and e-commerce sectors. By acquiring Vizio, Walmart not only enters the digital advertising industry but also positions itself to boost growth through ecommerce. Analysts have suggested Walmart intends to compete against Amazon in the online retail industry, indicating a possible shift towards a growth-oriented strategy. This makes it an interesting time to consider a stake in Walmart. 😊

Walmart joins the six holdovers from last week:

- Equitable Bank (TSE: EQB), a mid sized Canadian bank that provides financial services to consumers and businesses.

- McDonald’s (NYSE: MCD), the large sized American global fast-food chain.

- Ulta Beauty (NASD: ULTA), a major American beauty product retailer, with over 25,000 products from 600 brands.

- Celestica Inc. (TSE: CLS), a medium sized Canadian company that manufactures electronic products and provides supply chain services to companies around the world.

- Brown & Brown (NYSE: BRO), a major American firm, specializing in insurance and reinsurance products and services to a wide range of clients around the world.

- Lumine Group (TSE: LMN), a young Canadian mid sized company that acquires communications and media software companies and then strengthens and grows those companies.

Please keep in mind that these are only companies that have piqued my interest. This is not a recommendation or financial advice. You should do your own research or contact a professional before making any investment decisions.

The Radar Check was last updated February 23, 2024.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended February 23, 2024: UP ![]()

- In an effort to attract more AI developers, Alphabet’s Google is making its AI models available to outside developers. These AI models will be free of charge as Alphabet hopes to encourage developers to utilize Google’s cloud services and Google technology.

- Apple (NASD: AAPL) is upgrading its iMessage messaging platform to protect against iMessage hacking.

- Nvidia had a knockout earnings report that lifted global markets. Nvidia reported demand for their specialized AI chips continued to outpace their production capabilities.

- Unlike Nvidia, Rivian Automotive (NASD: RIVN) did the opposite and fell to an all time low after the company indicated growth would be flat for the rest of the year. Higher interest rates and slowing demand for electric vehicles (EVs) were the cause guidance provided by the company.

- General Motors (NYSE: GM) announced their Cruise self driving vehicle unit was preparing to resume testing their robotaxis. Initially the vehicles will be manually driven and supervised, graduating to self driven after rebuilding “trust with regulators and the public.”

Activity

Sold: Roku (NASD: ROKU) Roku thrived as streaming surged during the pandemic. However, with the sector’s growth stabilizing in the post-pandemic landscape, Roku is encountering mounting challenges. These include the necessity for price reductions to maintain market share, a downturn in advertising revenue, and stiff competition from industry titans such as Apple and Amazon. Further complicating Roku’s position is Walmart’s recent acquisition of Vizio, introducing a powerful new competitor to the streaming platform. With Walmart expected to shift its focus and potentially its in-house product’s operating systems to Vizio and away from Roku, the company’s challenges are likely to intensify. Given these headwinds, and in line with my strategy to streamline the portfolio by focusing on fewer, more promising investments, I have decided to divest from Roku.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

Home Depot, Inc.

Fourth quarter 2024 financial results on February 20, 2024

Rivian Automotive, Inc.

Fourth quarter 2023 financial results on February 21, 2024

Nvidia Corporation

Fourth quarter 2024 financial results on February 21, 2024

Global-E Online Ltd.

Fourth quarter 2023 financial results on February 21, 2024

kneat.com, inc.

Fourth quarter 2023 financial results on February 21, 2024

indie Semiconductor, Inc.

Fourth quarter 2023 financial results on February 22, 2024

Docebo Inc.

Fourth quarter 2023 financial results on February 23, 2024

Berkshire Hathaway Inc.

Fourth quarter 2023 financial results on February 23, 2024

Portfolio 2

Portfolio 2 for the week ended February 23, 2024: DOWN ![]()

No significant news to report this week.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSE: DIR.UN) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

Kneat.com

See report under Portfolio 1.

iA Financial Corporation Inc.

Fourth quarter 2023 financial results on February 21, 2024

Supremex Inc.

Fourth quarter 2023 financial results on February 22, 2024

Chorus Aviation Inc.

Fourth quarter 2023 financial results on February 22, 2024

Guardant Health, Inc.

Fourth quarter 2023 financial results on February 23, 2024

Portfolio 3

Portfolio 3 for the week ended February 23, 2024: DOWN ![]()

- Intel (NASD: INTC) announced they will create a custom semiconductor for Microsoft (NASD: MSFT).

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

Kneat.com

See report under Portfolio 1.