Trump vs. the Fed: Why Investors Are on Edge

US markets took another body blow at the start of this past week, once again set off by a tweet from President Trump. He renewed his public attacks on Federal Reserve (Fed) Chair Jerome Powell, calling him a “major loser” and demanding immediate rate cuts to juice the economy. Trump even floated the idea of firing Powell – a move that, while legally difficult, has rattled investor confidence.

The Fed’s independence isn’t just critical for the US economy – it’s a cornerstone of global financial stability. It gives the American central bank the freedom to make long-term decisions aimed at keeping inflation near 2% and supporting maximum employment, free from political interference. Undermining that independence risks throwing markets into turmoil and casting doubt – among global investors, businesses, and governments – on the credibility of both the US government and the Fed’s ability to manage the economy.

If Powell were removed, the shock to global markets could be severe. In the short term, we’d almost certainly see steep declines. The Dow Jones Industrial Average (DJIA) dropped over 1,000 points on Powell-related headlines, while the S&P 500 (S&P) and Nasdaq Composite Index (Nasdaq) have also seen sharp swings. The US dollar recently hit a three-year low, and rising Treasury yields are flashing warning signs that investors are getting anxious.

The longer-term fallout could be even more damaging. Borrowing costs might rise as investors demand higher yields to offset perceived risk. Inflation could become harder to control if rate decisions start looking politically motivated. And a broader loss of investor trust could push foreign capital out of US markets, undermining their reputation as a global safe haven.

It could also shift the investing landscape. If confidence in central banks starts to waver, we might see growing interest in alternative assets like Bitcoin and gold – stores of value outside the traditional system.

For Canadian investors, the ripple effects would hit close to home. With our deep trade and financial ties to the US, any disruption there tends to land quickly on the Toronto Stock Exchange Composite Index (TSX) and the Canadian dollar. Higher borrowing costs, weaker investor sentiment, and slower trade flows could all follow.

Globally, a move against Powell could spark widespread volatility. Markets in Europe and Asia would likely sell off, and emerging economies with heavy US dollar debt loads could face real pressure. Central banks around the world might be forced into reactive measures to stabilize their own markets.

This is a high-stakes moment. It’s not just about one central banker – it’s about confidence in the institutions that underpin long-term economic planning and global financial stability.

While President Trump’s attacks on the Fed dominated headlines early in the week, they weren’t the only thing that moved markets this week. First-quarter earnings season got underway, and global jitters over trade wars continued to unsettle investors. Let’s take a look at how the major indexes fared, and what drove the daily moves.

Items that may only interest or educate me ….

Canadian economic news, US economic news, Inflation isn’t gone…

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Retail sales

Statistics Canada reported a 0.4% drop in retail sales for February, matching expectations and marking the second monthly decline in a row after January’s 0.6% slide. While the monthly numbers were soft, the year-over-year picture looked much brighter – sales rose 4.7% compared to last February, improving on January’s 4.2% pace.

The monthly decline was mostly due to weaker auto sales, with new car dealers seeing a 3.0% drop – likely a result of ongoing tariff pressures in the auto sector. But if you strip out autos, gas stations, and fuel vendors, core retail sales actually rose 0.5%, bouncing back after January’s 0.2% dip. That strength came mainly from higher food and beverage sales. On a year-over-year basis, core sales jumped 4.9%, well ahead of the expected 3% gain.

Looking ahead, early estimates from Statistics Canada suggest a rebound in March, with retail sales projected to rise 0.7% – a promising sign that consumer spending may be picking up again.

Canadian market volatility

Canada’s market stress meter – the S&P/TSX 60 VIX (VIXC) – started the week elevated at 28.39 and briefly spiked into the 30 range after President Trump’s sharp criticism of the Fed Chair for not cutting interest rates. But as the week progressed, signs that the US might be softening its stance on tariffs helped settle investors’ nerves. The VIXC steadily drifted lower, ending the week at 22.68 – still elevated, and a reminder that uncertainty hasn’t left the building. Investors are uneasy, and caution is in the air.

For anyone just getting familiar, the VIXC is essentially Canada’s version of a fear gauge. Readings below 10 reflect strong investor confidence, 10–20 signals business as usual, and anything above 20 suggests uncertainty is creeping in.

US Economic news

This past week’s key data points that the Fed considers when deciding whether to raise or lower the interest rate.

Consumer Sentiment Index (CSI)

The University of Michigan’s final CSI reading for April came in at 52.2 – lower than the early estimate of 57.9 but still above analysts’ expectations of 50.8. That’s an 8.4% drop from March’s reading of 57.0 and a staggering 32.4% plunge compared to a year ago. It also marks the fourth straight monthly decline and the lowest reading since June 2022, when it fell to 50.8 – just shy of the all-time low of 50.0 recorded back in June 1980.

Digging into the details, consumers are feeling the pressure on both fronts. The Current Conditions Index, which looks at how people feel about their present financial situation, fell to 59.8 from 63.8 – a 6.3% monthly drop and 24.3% lower than a year ago. But the bigger red flag is the Expectations Index, which reflects how consumers view the next six months. That number dropped sharply to 47.3, down over 10% from March and nearly 38% lower year-over-year. Since January, expectations have nosedived 32%, the steepest three-month slide since the 1990 recession.

Inflation worries are front and centre, too. Year-ahead inflation expectations jumped from 5.0% to 6.5% – the highest level since 1981. The drop in consumer sentiment was widespread, cutting across all age groups, income levels, and political stripes. Ongoing uncertainty around trade policies, tariffs, and inflation is clearly weighing heavily on consumer confidence.

American market volatility

The CBOE Volatility Index (VIX), often called the market’s “fear gauge,” opened the week at 32.75 and briefly spiked above 35.0 after President Trump stirred the pot again – this time by suggesting he might remove Fed Chair Jerome Powell, raising fresh concerns about the Fed’s independence. A day later, he backtracked and said he never intended to fire Powell, which helped calm things down. Add in a dose of optimism around potential trade deals with key partners, and the VIX continued to drift lower, finishing the week at 24.84.

That means once again, the VIX ended lower than where it started – a small win for investor nerves. Still, it’d be nice to see it kick off next week lower than 25 and keep heading toward calmer territory.

For those new to the VIX: think of it as the market’s stress meter. A reading below 12 means investors are feeling relaxed, 12–20 is the “normal” range, and anything above 20 signals rising uncertainty and market jitters.

No, Mr. President, Inflation Isn’t Gone

Fresh off attacking all of America’s trading partners, President Trump has set his sights on a new target – Fed Chair Jerome Powell. Earlier this week, Trump took to social media to declare that “There is virtually no inflation,” while slamming Powell as “Mr. Too Late” and “a major loser.”

However, his remarks oversimplify how inflation is measured – and reveal a possible misunderstanding of the Fed’s approach. When setting policy, the Fed focuses on core inflation metrics like Core CPI and Core PCE, which exclude volatile items like food and energy – the very categories Trump claimed were falling. Those prices swing wildly from week to week, making them a poor guide for long-term decisions.

🧺 Think of inflation like a grocery basket. Some items, like eggs and gas, bounce around in price every week – that’s headline inflation. But to get a clearer picture, the Fed filters out those volatile items and looks at more stable prices like rent, clothing, and services. That’s core inflation – and it’s a better signal of where things are really heading.

And right now, it’s still running high. March’s core CPI came in at 2.8% year-over-year, and the Fed’s preferred measure – core PCE – was also sitting at 2.8% in February. It’s been hovering there for five months. The March PCE report, due next week, could offer the first solid glimpse at how tariffs are feeding into price pressures.

With inflation still well above the Fed’s 2% target, the Fed policymakers are staying cautious. They want to see how the tariff drama plays out before making any rate moves. From their perspective, cutting too soon could risk pouring more fuel on the inflation fire.

Weekly Market and Portfolio Review

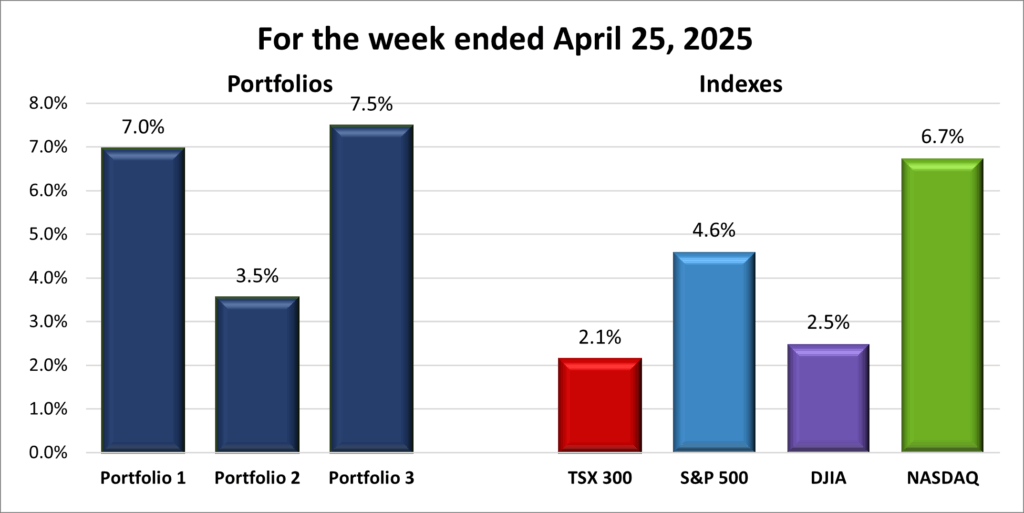

For the week, the TSX (SPTSX) rose 2.1%, the S&P 500 (SPX) climbed 4.6%, the DJIA (INDU) advanced 2.5% and the Nasdaq (CCMP) surged 6.7%.

| Index | Weekly Streak |

| TSX: | 3 – week winning streak |

| S&P: | 1 – week winning streak |

| DJIA: | 1 – week winning streak |

| Nasdaq: | 1 – week winning streak |

![]() After weeks of choppiness and volatility, the markets finally pulled off a rare feat – all four major indexes posted gains. The TSX, S&P, the DJIA, and the Nasdaq all closed the week in the green, as shown in the chart above. The Nasdaq and the S&P led the pack, thanks to a four-day rally fueled by a rebound in heavyweight technology companies.

After weeks of choppiness and volatility, the markets finally pulled off a rare feat – all four major indexes posted gains. The TSX, S&P, the DJIA, and the Nasdaq all closed the week in the green, as shown in the chart above. The Nasdaq and the S&P led the pack, thanks to a four-day rally fueled by a rebound in heavyweight technology companies.

After a relatively quiet stretch the week before, market drama returned in full force at the start of the week – and once again, it kicked off with a tweet. Investors were already on edge over President Trump’s escalating tariff battles with key trading partners. Then things got even more chaotic: Trump called for the Fed to slash interest rates and hinted that he might fire Fed Chair Jerome Powell. That kind of political interference is a big red flag – the idea of undermining the Fed’s independence rattled markets immediately.

Markets didn’t stay down for long, though. Comments from Trump and US Treasury Secretary Scott Bessent that tariff tensions might ease gave the markets some hope. That optimism was reinforced when Trump walked back his comments about firing Powell, helping calm fears about the Fed’s autonomy. Then came a one-two punch of good news: stronger-than-expected corporate earnings and comments from a few Fed officials about a potential rate cut, possibly as soon as June. That mix of strong earnings, Fed independence, trade optimism, and dovish Fed signals lit a fire under the markets.

That said, it wasn’t all sunshine. Consumer sentiment in the US took a steep 32% hit, shaken by inflation and fears of a slowing economy.

In Canada, markets rode the wave of easing US–China trade tensions, lifted further by improved sentiment from south of the border and anticipation of next week’s federal election, which is expected to usher in a more business-friendly government.

All in all, a strong week for North American markets. But one thing is clear: we’re in a new market reality where shifting economic policies out of Washington are taking the lead. Earnings reports and traditional economic data are often taking a backseat to political headlines – and sometimes even a single tweet. In today’s market, uncertainty rules. And when even a stray comment can send stocks soaring or tanking, it’s no wonder volatility remains high. For us investors, it’s a reminder that we’re navigating a market where policy and politics can matter just as much – if not more – than the fundamentals.

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week winning streak |

| Portfolio 2: | 2 – week winning streak |

| Portfolio 3: | 3 – week winning streak |

![]() A strong week in the markets usually spells good news for the three portfolios – and this week definitely delivered, as shown in the weekly performance chart below. For the first time in nine weeks, all three portfolios posted a gain at the same time.

A strong week in the markets usually spells good news for the three portfolios – and this week definitely delivered, as shown in the weekly performance chart below. For the first time in nine weeks, all three portfolios posted a gain at the same time.

Portfolio 1 had a strong showing, with 81% of its holdings finishing in the green and a total weekly gain of 7.0%. Leading the charge was Andlauer Healthcare Group Inc. (TSE: AND), which surged 29% on news of a takeover bid by UPS (NYSE: UPS). Other standout performers included Lattice Semiconductor (NASD: LSCC) up 23%, Shopify (TSE: SHOP) up 18%, Grab Holdings (NASD: GRAB) up 16%, CrowdStrike (NASD: CRWD) up 15%, Cloudflare (NYSE: NET) and Magnite (NASD: MGNI) up 13%, Datadog (NASD: DDOG) and Skyworks Solutions (NASD: SWKS) up 12%, and both Amazon.com (NASD: AMZN) and the portfolio’s largest holding, Nvidia (NASD: NVDA), up 11%.

With so many companies posting strong gains this week, I was a little surprised the portfolio didn’t climb even higher.

Portfolio 2 trailed the others but still delivered a respectable 3.5% gain, with 96% of its holdings in positive territory. Notable movers included MongoDB (NASD: MDB) up 10%, and Take-Two Interactive (NASD: TTWO), which hit an all-time high.

Portfolio 3 came out on top with a 7.5% gain, as 95% of its holdings – all but one – posted gains. Big contributors included Vertiv Holdings (NYSE: VRT) up 22%, Shopify up 18%, Magnite and Cloudflare both up 13%, and Real Matters (TSE: REAL) up 10%.

After weeks of uncertainty and volatility, it was refreshing to see the portfolios and markets finally moving in sync – and in the right direction. With all three portfolios posting gains and some standout performances across the board, I’m cautiously optimistic heading into next week. While uncertainty is still very much part of the investing landscape, this week was a reminder that staying invested through the noise can pay off. Here’s hoping we get a quiet week on social media and the upward momentum keeps rolling!😊

Companies on the Radar

It was a pretty quiet week on my radar, with not much movement – until one new company caught my eye: Main Street Capital Corp (NYSE: MAIN). They’re a mid-sized American firm known as a business development company (or BDC for short), which basically means they invest in and lend money to smaller private companies that are looking to grow. Think of them as part investor, part lender, helping businesses with things like management buyouts, expansion plans, and acquisitions.

It was a pretty quiet week on my radar, with not much movement – until one new company caught my eye: Main Street Capital Corp (NYSE: MAIN). They’re a mid-sized American firm known as a business development company (or BDC for short), which basically means they invest in and lend money to smaller private companies that are looking to grow. Think of them as part investor, part lender, helping businesses with things like management buyouts, expansion plans, and acquisitions.

On my radar test, MAIN doesn’t score particularly high. In fact, it’s the lowest-scoring company currently on my list. But I’m still curious. I suspect its recent share price drop has more to do with the broader market volatility tied to tariff tensions than anything company specific.

What really caught my attention is MAIN’s 7.2% dividend yield (as of the week ending April 25, 2025), which is pretty generous. Even more encouraging is the company’s 50% dividend payout ratio – that means they’re paying out only half of their earnings as dividends, leaving the other half to reinvest in the business. For a BDC, that kind of balance is a good sign. It suggests they’re focused on long-term sustainability, not just handing out big dividends to look good in the short term.

So, while MAIN isn’t a top contender (yet), it’s officially earned a closer look—and now joins the five companies listed below on my radar list.

- goeasy Ltd. (TSE: GSY): A mid-cap Canadian company offering non-prime leasing and lending services. Higher risk, but high potential if they manage credit cycles well.

- LPL Financial Holdings Inc. (NASD: LPLA): A large-cap US firm providing a brokerage and advisory platform for independent financial advisors. Benefiting from long-term trends in wealth management.

- Dollarama (TSE: DOL): A growing large-cap Canadian discount retailer that’s also expanding into South America. With a recession expected in Canada, discount retailers are seeing an increase in business.

- Brookfield Corporation (TSE: BN): A large-cap Canadian heavyweight in alternative asset management and real estate investing.

- iA Financial Corporation (TSE: IAG): A large-cap Canadian financial services firm with a solid insurance business in both Canada and the US.

As always, these are not buy recommendations – be sure to do your own research and make decisions that align with your personal financial goals!

The Radar Check was last updated April 25, 2025.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!