Items that may only interest or educate me ….

Canadian interest rate pause, global central banks, impact of US rate increases, Canadian GDP stalls, share buybacks, …

Analysts believe the BoC will hold Canada’s benchmark interest rate at 4.5% for the remainder of the year. Economic data has shown Canadian inflation has been heading downward so the Bank of Canada (BoC) has adopted a ‘wait and see’ attitude before making any changes to the interest rate. Many believe that the rate will remain at 4.5% unless the US Federal Reserve (Fed) raises the US key interest rate to far from the Canadian interest rate. If the two benchmark rates diverge too much, Canada risks importing inflation through the exchange rate.

Canada stands alone when it comes to pausing interest rate hikes. In February, the central banks responsible for the most widely traded currencies all raised their respective key interest rates. As has been mentioned in earlier blog posts, the Fed raised their benchmark rate by 0.25% and plan to raise the rate higher and maintain it there longer. Elsewhere around the globe:

- The Reserve Bank of Australia raised its rate by 0.25% to 2.35%, the highest in over ten years.

- The Bank of England raised their benchmark rate by 0.5% bringing the rate to 4.0%, its highest since the financial crisis.

- The European Central Bank raised interest rates 0.5% to 2.5% and suggested there would be at least one more similar sized increase in March.

- The Reserve Bank of New Zealand raised their benchmark rate by 0.5% to 4.75%, reaching levels last seen during the global financial crisis. They too said they expect there to be additional rate hikes coming as they battle with inflation.

- Sweden’s Riksbank raised its key borrowing rate by 0.5% to 3% and hinted there could be at least two more 0.25% increases coming.

The BoC would appear to be the only major central bank to hold the line on interest rates. Good on them for following the data rather than the crowd.

The BoC has said they will pause further increases to Canada’s benchmark interest rate while the past rate increases have a chance to work through the Canadian economy. Currently inflation in Canada is headed lower, allowing the BoC to stay true to its plan to freeze hikes. However, recent US economic data indicates the American economy is still running too strong. As a result, the Fed is likely to raise the US benchmark interest rate a few more times, then keep it high until inflation in the US starts declining.

What does that have to do with us Canadians, you ask? As American interest rates climb, the value of the US dollar rises at the expense of foreign currencies, including the Canadian dollar. When US interest rates rise, it makes US financial markets more attractive to investors, which increases the demand for US dollars, leading to a stronger US currency. As the Canadian dollar falls against the US dollar, products coming from the US become more expensive. If the gap between the Canadian and US interest rates gets too wide, the BoC will be forced to raise the Canadian interest rate to prevent the cost of importing American goods and services becoming too high.

As I mentioned in the article on Central Banks this is how Canadians are affected by US interest rates and the actions of the Fed. I just didn’t see this real-world example coming so soon.

According to Statistics Canada, the Canadian economy, measured by Gross Domestic Product (GDP), stalled the last three months of 2023, ending a string of five straight quarterly gains. This was well below analysts’ expectations of a 1.5% increase from the previous quarter. The BoC’s itself had projected a 1.3% improvement.

Declines in business investment in equipment, housing starts and a slower buildup of inventory, offset by greater household and government spending, all contributed to zero economic growth. The flat GDP would seem to indicate the higher interest rates are acting as a brake on the Canadian economy and suggests the BoC made the right call in suspending future increases to the Canadian interest rate.

Recently, Warren Buffet, considered by many to be the greatest investor of all time, published his latest annual letter to shareholders. In it, he took a shot those who were critical of companies that bought back their own shares.

“When you are told that all repurchases are harmful to shareholders or to the country, or particularly beneficial to CEOs, you are listening to either an economic illiterate or a silver-tongued demagogue (characters that are not mutually exclusive).”

So, what exactly are share buybacks? As the term suggests, share buybacks are when a company chooses to buy back some of its own shares on the open market. This is considered a shareholder friendly action because it can increase the value of the remaining shares. In his letter, Mr. Buffet provides a great example of how share buybacks benefit all shareholders of the company.

“Imagine, if you will, three fully-informed shareholders of a local auto dealership, one of whom manages the business. Imagine, further, that one of the passive owners wishes to sell his interest back to the company at a price attractive to the two continuing shareholders. When completed, has this transaction harmed anyone? Is the manager somehow favored over the continuing passive owners? Has the public been hurt?”

Without doing anything, or costing you a penny, the value of your shares has increased in value. That is fairly friendly! 😊

When I take a deep dive on a company, one of the things I check is to see if the number of outstanding shares is increasing or decreasing. Generally, if the share count is stable or shrinking, I view that as a positive sign. The company is acting in shareholders’ interest or at worst, they are not hurting shareholders interests by diluting the value of the existing shares.

On the other hand, if the number of shares is increasing, I want to know why. A bit of growth is acceptable, however, if the shares are growing rapidly (say, greater than 5% per year), I take that as a yellow flag. I want to know why the shares are growing so fast. If the company is increasing the outstanding shares to raise cash, that concerns me, as they may be tight on cash. At that point I’ll most likely move on from the company.

Let’s see what moved the market this past week….

Weekly Market Review

Monday: The markets got off to a hot start today before ending the day with modest gains. After last week’s losses, any gains were good gains. Once again, concerns about higher interest rates held back all four major North American indexes.

In Canada, the Toronto Stock Exchange Composite Index (TSX) was lifted by higher energy and commodity prices. In the Canadian sectors, the Basic Materials (miners and fertilizer manufacturers) and the Consumer Cyclical sectors gained the most while Consumer Staples and Healthcare fell the farthest.

In the US, the three American indexes – the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – ended the day marginally higher. Investors were looking for some bargains after last week’s beat down. In the American sectors, the Consumer Cyclicals and Industrials advanced the most, with Utilities and Consumer Staples dropped the most.

Tuesday: A lumpy day for the indexes was a fitting way to close out a volatile February. The TSX and DJIA spent the day bouncing around in negative territory while the S&P and Nasdaq bumped along in positive territory before diving below the bar at the end of the day. Concerns about the likelihood of higher interest rates continues to cast a shadow over all the indexes. Oil prices ended higher as hopes for strong demand out of China won the tug of war with fears of higher US interest rates.

In Canada, the TSX was dragged lower by the Financials sector. Banks must set aside more money for tougher economic conditions that could lead to more loan defaults caused by the higher interest rates. This has led to lower profits as well as forecasts for lower profits going forward. Of the Canadian S&P sectors that advanced, Basic Materials and Technology led the way, while Energy and Utilities lost the most ground.

In the US, of the American S&P sectors, only Basic Materials and Financials were able to gain ground, while the Utilities and Energy sectors dropped the most.

Wednesday: Strong talk from the Fed sent the growth-oriented Nasdaq and S&P lower while the TSX ended higher and the DJIA ended on the positive side of flat. In Canada, news of China’s manufacturing sector growing at its fastest pace in 10 years lifted the TSX. The Basic Materials and Energy sectors were the main beneficiaries of the news and were the best performers of the Canadian sectors. At the other end of the spectrum, Technology and Healthcare dropped the most.

In the US, weak domestic manufacturing data indicated inflation was remaining high. Add in talk from the Fed about a possible 0.5% raise to the interest rate and its no wonder the Nasdaq and S&P fell for a second day. In trading across the three American indexes, Basic Materials, Energy, and Industrials were the only American sectors to end higher, while falling the farthest were Utilities and Consumer Cyclicals.

Thursday: Despite a shaky start to today’s session, all four indexes rallied in the afternoon to end in the green. The rally was started when the Fed said it might be able to suspend interest rate hikes in the summer. After all the tough talk from the Fed about the need for higher, longer interest rates, this was music to investors’ ears. Oil prices continue to climb on signs of economic growth in China.

In Canada, the talk of a pause in US interest rate hikes was enough to send the TSX to its highest close in two weeks. The Technology and Energy sectors had the biggest gains of the Canadian S&P sectors, while the Consumer Staples and Telecommunications Services dropped the most.

In the US, once again weekly jobless claims were lower. The good news for workers, bad news for investors was more than offset by the comments from the Fed about slow and steady increases with a possible mid summer pause. In trading, the Utilities and Technology sectors were the biggest gainers of the American S&P sectors. The Financials and Telecommunications Services were the only two sectors to end lower.

Friday: It was a bullish day for all four indexes as each ended the day sharply higher, finishing the week in the green. Economic data out of the USA showed healthy economic growth, coupled with slowing price increases. Oil price continued to rise on growing demand from China.

In Canada, strong economic data from China and the US, and rising commodity prices boosted the resource heavy TSX to its highest point in a few weeks. All the Canadian sectors ended higher with the Technology and Basic Materials sectors rising the most and Consumer Staples and Healthcare gaining the least.

South of the border, the three American indexes were up sharply on the positive economic news. Comments from the Fed that they were open to a 0.25% increase rather than a feared 0.5% raise but would let the data guide them. In the markets, it was an upbeat day as all American sectors finished in the green. Technology and Consumer Cyclicals advanced the most while Consumer Staples and Telecommunications Services had the smallest gains.

Weekly Portfolio Review

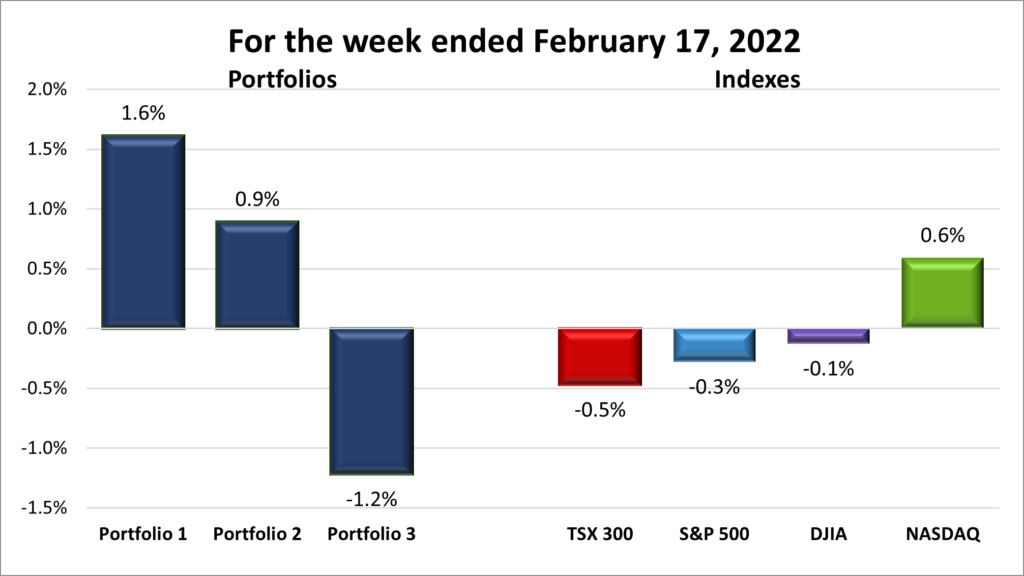

For the week, the TSX advanced 1.8%, the S&P got back in the win column gaining 1.9%, the DJIA returned to positive territory gaining 1.7% and the Nasdaq jumped 2.6%.

![]() The stock markets closed the week on an upswing, with each index back in the win column. Looking at the chart above, its almost like once February was over the stock markets, represented by the indexes, snapped out of their funk. It was a week of good news coming out of America where employment remains strong while inflation is drifting downward. It seems investors have come to grips with higher interest rates for a longer duration but now feel the next increase by the Fed will be 0.25% rather than a feared 0.5% increase. In the current high interest rate environment, the thought of a lower interest rate hike is enough to get investors back into the markets but that seems to be what happened this past week.

The stock markets closed the week on an upswing, with each index back in the win column. Looking at the chart above, its almost like once February was over the stock markets, represented by the indexes, snapped out of their funk. It was a week of good news coming out of America where employment remains strong while inflation is drifting downward. It seems investors have come to grips with higher interest rates for a longer duration but now feel the next increase by the Fed will be 0.25% rather than a feared 0.5% increase. In the current high interest rate environment, the thought of a lower interest rate hike is enough to get investors back into the markets but that seems to be what happened this past week.

Investors moved back into technology companies, lifting the Nasdaq and S&P. It seems on any good news investors pile back into technology companies, not wanting to miss out on any upward momentum. On the TSX, many investors moved back into companies with large amounts of long-term debt, like the amounts that are often associated with energy, mining, and technology companies (long term debt is typically used by energy and mining companies to invest in expensive machinery and equipment while technology companies use debt to keep the company running).

As with the indexes, the three Portfolios were happy to see the end of February as all three posted another weekly gain. Portfolios 1 and 3, both technology company heavy, benefited from the rally in technology companies. Portfolio 2 is like my tortoise in the tortoise and hare race – slow and steady. As long as it keeps growing, I’m happy. 😊

Monthly Portfolio Review

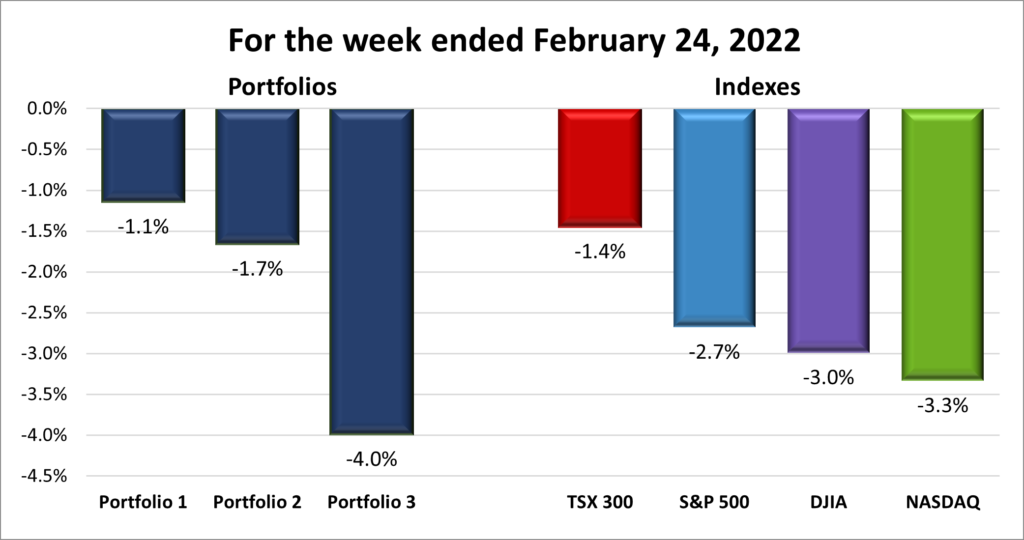

For February, each of the four indexes ended the month lower. The TSX dropped 2.6%, the S&P fell 2.6%, the DJIA sank 4.2% and the Nasdaq declined 1.1%.

![]() After two steps forward in January to start the year with a bang, the markets and indexes took a step back in February. Fortuntely, three of the four indexes are still ahead on a year to date basis. The DJIA is the only index that is lower in 2023. Economic data and comments from Fed drove the markets as skittish investors weighed the chances the Fed would hike rates to a higher level and then keep them there longer than initially expected. In January analysts and investors were hoping for a 0.25% increase, with the optimistic hoping for a pause in increases. This led to a strong January. With the February US economic data, investors feared an interest rate hike of 0.5% and a higher overall interest rate that would remain longer and pushed the three American indexes lower. The Canadian TSX, with its many energy and natural resource companies with their high amounts of long-term debt, also felt the sting of concerns about higher interest rates.

After two steps forward in January to start the year with a bang, the markets and indexes took a step back in February. Fortuntely, three of the four indexes are still ahead on a year to date basis. The DJIA is the only index that is lower in 2023. Economic data and comments from Fed drove the markets as skittish investors weighed the chances the Fed would hike rates to a higher level and then keep them there longer than initially expected. In January analysts and investors were hoping for a 0.25% increase, with the optimistic hoping for a pause in increases. This led to a strong January. With the February US economic data, investors feared an interest rate hike of 0.5% and a higher overall interest rate that would remain longer and pushed the three American indexes lower. The Canadian TSX, with its many energy and natural resource companies with their high amounts of long-term debt, also felt the sting of concerns about higher interest rates.

As for the three Portfolios, I am surprised Portfolio 1 was able to post a gain in February. I think the mega cap technology companies in Portfolio 1 kept the portfolio in the green. Portfolio 2’s less risky companies limited its losses. These companies do not grow as fast as riskier technology companies, but they don’t fall as hard. Portfolio 3’s losses were highlighted by Shopify’s 20% drop in share price during the month. In today’s environment, its amazing Portfolio 3 did not drop farther.

Companies on the Radar

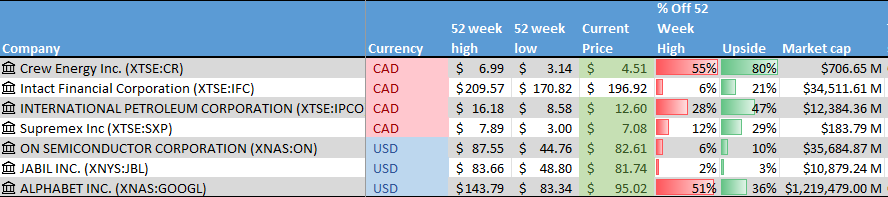

This past week I dropped ON Semiconductor (NASD:ON) from my Radar List because there are already three semiconductor companies in Portfolio 1 – Nvidia (NASD:NVDA), Lattice Semiconductor (NASD:LSCC) and Skyworks Solutions (NASD:SWKS). If I wanted to put more money into semiconductors, I would add to one of those companies. Otherwise, the five companies listed below currently are on my radar.

This past week I dropped ON Semiconductor (NASD:ON) from my Radar List because there are already three semiconductor companies in Portfolio 1 – Nvidia (NASD:NVDA), Lattice Semiconductor (NASD:LSCC) and Skyworks Solutions (NASD:SWKS). If I wanted to put more money into semiconductors, I would add to one of those companies. Otherwise, the five companies listed below currently are on my radar.

On a side note, companies on the radar are companies not owned in any of the three portfolios. When it comes to investing in a company, it may be from the list below or a company in one of the Portfolios.

- Intact Financial (TSX:IFC): a mid size insurance company supplying home, car and business insurance in Canada, the US, and the UK.

- Hammond Power Solutions (TSX:HPS.A): a Canadian company manufacturing transformers used throughout the world in a wide variety of industries.

- Supremex (TSX:SXP): a small cap company selling packing solutions throughout Canada and the USA.

- Jabil Inc. (NYSE:JBL): an American company with global operations that specializes in providing manufacturing services and solutions.

- Kits Eyecare (TSX:KITS): a Canadian company operating an online eyeglass platform.

The Radar Check was last updated March 3, 2022.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended March 3, 2023: UP ![]()

- Tesla (NASD:TSLA) announced they will build another Gigafactory assembly plant in the northern Mexico industrial hub of Monterrey. It has yet to be determined which vehicles will be produced at the facility. This will be Tesla’s sixth gigafactory (a term coined by Tesla to refer to factories producing electric vehicles at large scale) and third outside the US.

At Tesla’s Investor Day, the company unveiled ‘Master Plan 3’. Unfortunately, there were no big announcements. They did say their Cybertruck should start shipping later this year, and they are attempting to lower their vehicle assembly costs by 50% (good plan but not big news). - In January, General Motors (NYSE:GM) announced they planned to reduce cost by US$ 2 billion without resorting to layoffs. Fast forward and GM announced they would be reducing the headcount of executive level and salaried employees. GM said these were not layoffs, but rather a reduction in structural costs. Hmmm. For those who lost their jobs, I doubt they see the difference.

A few weeks ago GM announced a major investment in Lithium America Corp (TSX:LAC) to help fund the development of a major lithium mine in Nevada. In return for the investment, GM has exclusive rights to 40,000 tonnes of lithium per year. Not only does this provide a secure supply of lithium, but because the mine is in the US it will qualify for electric vehicle subsidies in the Inflation Reduction Act. Two birds, one stone. Well done GM. 😊 - Rivian (NASD:RIVN) received the highest marks for customer satisfaction from JD Power. Unfortunately, I do not own a Rivian so I cannot attest to the quality of their vehicles or how Rivian treats its customer. However, I do own a part of the company and it has become a black hole for cash. Rivian has set a new standard for burning through cash, ending 2022 with a negative cash flow of US$ 6.4 billion. Ouch! I knew Rivian’s share price would fall back after shooting up after the IPO, but I never thought the share price would fall so far.

- Visa (NYSE:V) has decided to delay the launch of their crypto related products and services. After being all the rage in 2020 – 2021, cryptocurrency fell on very tough times in 2022, taking down several cryptocurrency companies. While not abandoning their crypto plans, the company has decided it would be better to wait until the crypto market and the regulations surrounding the industry improve.

- Alphabet (NASD:GOOGL) announced a second round of layoffs at its Waymo self driving vehicle unit as the company seeks to reduce costs. Driverless cars appear to have surrendered the spotlight to the latest technology – artificial intelligence (AI). After the recent stumble of Google’s Bard chat bot, Google has shifted its focus to AI to maintain its lead in online search.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Shaw Communications Inc (TSX:SJR.B)

US $

Visa Inc (NYSE:V)

Quarterly Reports

Innovative Industrial Properties, Inc.

All currency listed in thousands of US dollars.

Selected highlights from their fourth quarter 2022 financial results on February 27, 2023

- Revenue of $70,461 for the three months ended December 31, compared to $58,943 for the same period in 2021. An increase of over 19%.

- Net income of $41,168 for the three months ended December 31, compared to net income of $28,292 in the same period in 2021.

- Diluted earnings per ordinary share of $1.46 for the three months ended December 31, compared to earnings per share of $1.14 for the same period in 2021.

- Revenue of $276,359 for the year ended December 31, compared to $204,551 for the same period in 2021. An increase of over 35%.

- Net earnings of $153,034 for the year ended December 31, compared to net earnings of $112,638 in the same period in 2021.

- Diluted earnings per ordinary share of $5.52 for the year ended December 31, compared to earnings per share of $4.55 for the same period in 2021.

fuboTV Inc.

All currency listed in thousands of US dollars.

Selected highlights from their fourth quarter 2022 financial results on February 27, 2023

- Revenue of $319,315 for the three months ended December 31, compared to $231,077 for the same period in 2021. An increase of over 39%.

- Net loss of $152,082 for the three months ended December 31, compared to net loss of $111,892 in the same period in 2021.

- Diluted loss per ordinary share of $0.76 for the three months ended December 31, compared to a loss per share of $0.76 for the same period in 2021.

- Revenue of $1,008,696 for the year ended December 31, compared to $638,370 for the same period in 2021. An increase of over 58%.

- Net loss of $561,919 for the year ended December 31, compared to net loss of $382,963 in the same period in 2021.

- Diluted loss per ordinary share of $3.08 for the year ended December 31, compared to a loss per share of $2.78 for the same period in 2021.

Progeny, Inc.

All currency listed in thousands of US dollars.

Selected highlights from their fourth quarter 2022 financial results on February 27, 2023

- Revenue of $214,321 for the three months ended December 31, compared to $127,553 for the same period in 2021. An increase of over 68%.

- Net income of $3,408 for the three months ended December 31, compared to net income of $15,080 in the same period in 2021.

- Diluted earnings per ordinary share of $0.03 for the three months ended December 31, compared to earnings per share of $0.15 for the same period in 2021.

- Revenue of $786,913 for the year ended December 31, compared to $500,621 for the same period in 2021. An increase of over 57%.

- Net earnings of $30,358 for the year ended December 31, compared to net earnings of $65,769 in the same period in 2021.

- Diluted earnings per ordinary share of $0.30 for the year ended December 31, compared to earnings per share of $0.66 for the same period in 2021.

Marqueta, Inc.

All currency listed in thousands of US dollars.

Selected highlights from their fourth quarter 2022 financial results on February 28, 2023

- Revenue of $203,805 for the three months ended December 31, compared to $155,414 for the same period in 2021. An increase of over 31%.

- Net loss of $26,326 for the three months ended December 31, compared to net loss of $36,807 in the same period in 2021.

- Diluted loss per ordinary share of $0.05 for the three months ended December 31, compared to loss per share of $0.07 for the same period in 2021.

- Revenue of $7748,206 for the year ended December 31, compared to $517,175 for the same period in 2021. An increase of over 44%.

- Net loss of $184,780 for the year ended December 31, compared to net loss of $163,929 in the same period in 2021.

- Diluted loss per ordinary share of $0.34 for the year ended December 31, compared to loss per share of $0.45 for the same period in 2021.

Scotiabank

All currency listed in millions of Canadian dollars.

Selected highlights from their first quarter 2021 financial results on February 27, 2023

- Revenue of $7,980 for the three months ended January 31, compared to $8,049 for the same period in 2022. A decrease of less than 1%.

- Net income of $1,172 for the three months ended January 31, compared to net income of $2,740 in the same period in 2021.

- Diluted earnings per ordinary share of $1.36 for the three months ended December 31, compared to earnings per share of $2.14 for the same period in 2021.

Rivian Automotive Inc.

All currency listed in millions of US dollars.

Selected highlights from their fourth quarter 2022 financial results on February 28, 2023

- Revenue of $663 for the three months ended December 31, compared to $54 for the same period in 2021. An increase of over 1,227%.

- Net loss of $1,795 for the three months ended December 31, compared to net loss of $2,461 in the same period in 2021.

- Diluted loss per ordinary share of $1.87 for the three months ended December 31, compared to a loss per share of $4.83 for the same period in 2021.

- Revenue of $1,658 for the year ended December 31, compared to $55 for the same period in 2021. An increase of over 3,014%.

- Net loss of $6,752 for the year ended December 31, compared to net loss of $4,688 in the same period in 2021.

- Diluted loss per ordinary share of $7.40 for the year ended December 31, compared to a loss per share of $22.98 for the same period in 2021.

Trisura Group Ltd.

All currency listed in thousands of Canadian dollars.

Selected highlights from their fourth quarter 2022 financial results on February 28, 2023

- Revenue of $149,320 for the three months ended December 31, compared to $106,549 for the same period in 2021. An increase of over 40%.

- Net loss of $40,340 for the three months ended December 31, compared to net income of $10,295 in the same period in 2021.

- Diluted loss per ordinary share of $0.86 for the three months ended December 31, compared to earnings per share of $0.24 for the same period in 2021.

- Revenue of $526,102 for the year ended December 31, compared to $349,877 for the same period in 2021. An increase of over 98%.

- Net earnings of $24,651 for the year ended December 31, compared to net earnings of $62,559 in the same period in 2021.

- Diluted earnings per ordinary share of $1.87 for the year ended December 31, compared to earnings per share of $1.47 for the same period in 2021.

Celsius Holdings, Inc.

All currency listed in thousands of US dollars.

Selected highlights from their fourth quarter 2022 financial results on March 1, 2023

- Revenue of $177,964 for the three months ended December 31, compared to $104,254 for the same period in 2021. An increase of almost 71%.

- Net loss of $21,223 for the three months ended December 31, compared to net income of $11,942 in the same period in 2021.

- Diluted loss per ordinary share of $0.37 for the three months ended December 31, compared to earnings per share of $0.15 for the same period in 2021.

- Revenue of $653,604 for the year ended December 31, compared to $314,272 for the same period in 2021. An increase of over 73%.

- Net loss of $187,282 for the year ended December 31, compared to net earnings of $3,937 in the same period in 2021.

- Diluted loss per ordinary share of $2.63 for the year ended December 31, compared to earnings per share of $0.05 for the same period in 2021.

GDI Integrated Facility Services Inc.

All currency listed in millions of Canadian dollars.

Selected highlights from their fourth quarter 2022 financial results on March 1, 2023

- Revenue of $588 for the three months ended December 31, compared to $433 for the same period in 2021. An increase of almost 37%.

- Net income of $10 for the three months ended December 31, compared to net income of $7 in the same period in 2021.

- Diluted earnings per ordinary share of $0.40 for the three months ended December 31, compared to earnings per share of $0.29 for the same period in 2021.

- Revenue of $2,172 for the year ended December 31, compared to $1,597 for the same period in 2021. An increase of over 36%.

- Net earnings of $36 for the year ended December 31, compared to net earnings of $43 in the same period in 2021.

- Diluted earnings per ordinary share of $1.53 for the year ended December 31, compared to earnings per share of $1.84 for the same period in 2021.

Viemed Healthcare, Inc.

All currency listed in thousands of US dollars.

Selected highlights from their fourth quarter 2022 financial results on March 3, 2023

- Revenue of $37,508 for the three months ended December 31, compared to $31,962 for the same period in 2021. An increase of over 17%.

- Net income of $2,438 for the three months ended December 31, compared to net income of $4,087 in the same period in 2021.

- Diluted earnings per ordinary share of $0.06 for the three months ended December 31, compared to earnings per share of $0.10 for the same period in 2021.

- Revenue of $138,832 for the year ended December 31, compared to $117,062 for the same period in 2021. An increase of almost 19%.

- Net earnings of $6,222 for the year ended December 31, compared to net earnings of $9,126 in the same period in 2021.

- Diluted earnings per ordinary share of $0.16 for the year ended December 31, compared to earnings per share of $0.22 for the same period in 2021.

TD Bank Group

All currency listed in millions of Canadian dollars.

Selected highlights from their first quarter 2023 financial results on March 2, 2023

- Revenue of $12,226 for the three months ended December 31, compared to $11,281 for the same period in 2021. An increase of over 8%.

- Net income of $1,582 for the three months ended December 31, compared to net income of $3,733 in the same period in 2021.

- Diluted earnings per ordinary share of $0.82 for the three months ended December 31, compared to earnings per share of $2.02 for the same period in 2021.

Andlaeur Healthcare Group Inc.

All currency listed in thousands of Canadian dollars.

Selected highlights from their fourth quarter 2022 financial results on March 2, 2023

- Revenue of $165,772 for the three months ended December 31, compared to $133,025 for the same period in 2021. An increase of almost 25%.

- Net income of $19,824 for the three months ended December 31, compared to net income of $53,104 in the same period in 2021.

- Diluted earnings per ordinary share of $0.46 for the three months ended December 31, compared to earnings per share of $1.26 for the same period in 2021.

- Revenue of $648,423 for the year ended December 31, compared to $440,115 for the same period in 2021. An increase of over 47%.

- Net earnings of $76,275 for the year ended December 31, compared to net earnings of $89,954 in the same period in 2021.

- Diluted earnings per ordinary share of $1.79 for the year ended December 31, compared to earnings per share of $2.25 for the same period in 2021.

Portfolio 2

Portfolio 2 for the week ended March 3, 2023: UP ![]()

- Microsoft (NASD:MSFT) started rolling out an AI enhanced Bing to its Windows 11 operating system. After you install the latest updates from Microsoft, a Bing logo appears on the Taskbar. When you click the logo, it launches an updated Bing search page in Microsoft’s Edge browser. When you ask a question the response comes back with a typical list of websites, plus a new chat window on the right side with an answer.

It seems the ten year licensing deals Microsoft is signing with video game rivals will be enough for the European Commission to approve Microsoft’s acquisition of Blizzard Activision (NASD:ATVI). This is a big win for Microsoft since they will not have to divest any assets to gain the European Commission’s approval. - Walt Disney’s (NYSE:DIS) almost 50 years of self rule in Florida is coming to an end. Next week the new oversight board will meet for the first time. Among other tings the board will consider is Disney’s plans for an additional three theme parks over the next five years.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Dream Industrial Real Estate Investment Trust (TSX:DIR.UN) DRIP

US $

No US$ dividends this past week.

Quarterly Reports

Scotiabank

All currency listed in millions of Canadian dollars

Selected highlights from their first quarter 2021 financial results on February 27, 2023

- Revenue of $7,980 for the three months ended January 31, compared to $8,049 for the same period in 2022. A decrease of less than 1%.

- Net income of $1,172 for the three months ended January 31, compared to net income of $2,740 in the same period in 2021.

- Diluted earnings per ordinary share of $1.36 for the three months ended December 31, compared to earnings per share of $2.14 for the same period in 2021.

Canadian Natural Resources Ltd.

All currency listed in millions of Canadian dollars.

Selected highlights from their fourth quarter 2022 financial results on March 2, 2023

- Revenue of $9,689 for the three months ended December 31, compared to $9,213 for the same period in 2021. An increase of over 5%.

- Net income of $1,520 for the three months ended December 31, compared to net income of $2,534 in the same period in 2021.

- Diluted earnings per ordinary share of $1.36 for the three months ended December 31, compared to $2.14 for the same period in 2021.

- Revenue of $42,298 for the year ended December 31, compared to $30,057 for the same period in 2021. An increase of over 40%.

- Net earnings of $10,937 for the year ended December 31, compared to net earnings of $7,664 in the same period in 2021.

- Diluted earnings per ordinary share of $9.52 for the year ended December 31, compared to $6.46 for the same period in 2021.

Portfolio 3

Portfolio 3 for the week ended March 3, 2023, 2023: UP ![]()

- TD Bank (TSX:TD) has agreed to pay US$ 1.2 billion for its alleged part in a US$ 7 billion Ponzi scheme run by Allen Stanford of Stanford International Bank Ltd. The money will be used to pay people who had unknowingly participated in the program.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Enghouse Systems Ltd (TSX:ENGH)

US $

No US$ dividends this past week.

Quarterly Reports

Royal Bank of Canada

All currency listed in millions of Canadian dollars.

Selected highlights from their first quarter 2023 financial results on March 1, 2023

- Revenue of $15,094 for the three months ended December 31, compared to $13,066 for the same period in 2021. An increase of over 15%.

- Net income of $3,214 for the three months ended December 31, compared to net income of $4,095 in the same period in 2021.

- Diluted earnings per ordinary share of $2.29 for the three months ended December 31, compared to earnings per share of $2.84 for the same period in 2021.

GDI Integrated Facility Services Inc.

All currency listed in millions of Canadian dollars.

Selected highlights from their fourth quarter 2022 financial results on March 1, 2023

- Revenue of $588 for the three months ended December 31, compared to $433 for the same period in 2021. An increase of almost 37%.

- Net income of $10 for the three months ended December 31, compared to net income of $7 in the same period in 2021.

- Diluted earnings per ordinary share of $0.40 for the three months ended December 31, compared to earnings per share of $0.29 for the same period in 2021.

- Revenue of $2,172 for the year ended December 31, compared to $1,597 for the same period in 2021. An increase of over 36%.

- Net earnings of $36 for the year ended December 31, compared to net earnings of $43 in the same period in 2021.

- Diluted earnings per ordinary share of $1.53 for the year ended December 31, compared to earnings per share of $1.84 for the same period in 2021.

TD Bank Group

All currency listed in millions of Canadian dollars.

Selected highlights from their first quarter 2023 financial results on March 2, 2023

- Revenue of $12,226 for the three months ended December 31, compared to $11,281 for the same period in 2021. An increase of over 8%.

- Net income of $1,582 for the three months ended December 31, compared to net income of $3,733 in the same period in 2021.

- Diluted earnings per ordinary share of $0.82 for the three months ended December 31, compared to earnings per share of $2.02 for the same period in 2021.

Viemed Healthcare, Inc.

All currency listed in thousands of US dollars.

Selected highlights from their fourth quarter 2022 financial results on March 3, 2023

- Revenue of $37,508 for the three months ended December 31, compared to $31,962 for the same period in 2021. An increase of over 17%.

- Net income of $2,438 for the three months ended December 31, compared to net income of $4,087 in the same period in 2021.

- Diluted earnings per ordinary share of $0.06 for the three months ended December 31, compared to earnings per share of $0.10 for the same period in 2021.

- Revenue of $138,832 for the year ended December 31, compared to $117,062 for the same period in 2021. An increase of almost 19%.

- Net earnings of $6,222 for the year ended December 31, compared to net earnings of $9,126 in the same period in 2021.

- Diluted earnings per ordinary share of $0.16 for the year ended December 31, compared to earnings per share of $0.22 for the same period in 2021.

Amazon (

Amazon (

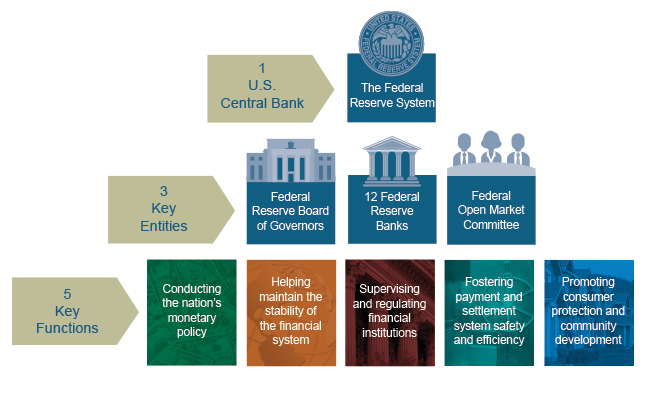

The BOC is located in Ottawa, Ontario. It came into existence in 1935 with the mission to “regulate credit and currency in the best interests of the economic life of the nation.”

The BOC is located in Ottawa, Ontario. It came into existence in 1935 with the mission to “regulate credit and currency in the best interests of the economic life of the nation.”