Items that may only interest or educate me ….

Canadian economic stats, oil production cutbacks, American jobs cooling, but first ….

Last Thursday, Statistics Canada reported the Canadian economy remains strong, adding 34,700 jobs in March, higher than the 12,000 jobs analysts predicted. Employment has been trending upward since September, with March being the seventh straight month of higher job numbers. Meanwhile, for the fourth straight months unemployment remained at 5%, barely above the record low of 4.9%. Finally, average hourly wages rose 5.3% on a year over year basis, down slightly from February’s 5.4%.

In global trading, despite a strong start in January, Canada’s trade surplus for February fell to C$422 million, down from January’s C$1.2 billion surplus. Analysts had been expecting the surplus to come in at C$1.80 billion. On a yearly basis, exports were down 2.4% and imports decreased 1.3%. Exports were down for all but two of the thirteen classified sectors. On the import side, five of the classifications posted gains, with eight sectors falling back.

Canada’s manufacturing activity shrank in March after two months of growth. In March, the Canadian Manufacturing Purchasing Managers’ Index (PMI) fell to 48.6, its lowest level since June 2020. On the PMI scale, anything below 50 indicates contraction in the manufacturing sector, whereas a reading above 50 indicates growth in the sector.

The Bank of Canada (BoC) is scheduled to meet next week where they will announce any changes to Canada’s benchmark interest rate. They must balance inflationary data such as continuing strong jobs growth, rising wages, and a growing Gross Domestic Product (GDP) against a cooling manufacturing sector and a shrinking trade surplus. They also must consider the uncertainty of a recession, along with the global banking crisis, which has made it more challenging to borrow money. As a result, companies are hesitant to place large, costly orders. Overall, I suspect the BoC will maintain their pause on interest hikes, holding it at 4.5%, but they will warn they are prepared to act if the data indicates inflation does not continue to fall.

In a case of bad news is good news, many of the oil producing countries announced they would reduce oil production by 1.65 million of barrels per day (bpd), with Saudi Arabia having the biggest cutback of 500,000 bpd. The 21 member OPEC+ nations previously cut production in late 2022 by two million bpd, and they were expected to keep production steady through 2023.

Saudi Arabia said the cuts were a “precautionary move” to stabilize the oil market. I read that as keeping the price of oil high. As I mentioned in the October 28 Weekly Update, the Saudis plan to use the oil revenues to finance a number of mega-projects to overhaul their economy as part of their Vision 2030. Imagine, using oil revenues instead of taxpayers’ dollars to finance government priorities.

From a consumer viewpoint, the reduction in oil production could lead to higher prices at the pumps this summer. ☹ From an investing perspective, higher oil prices should lead to higher revenues for oil producers. The higher revenues should lead to rising share prices and dividends. 😊

The US Labor Department’s March employment data (nonfarm payroll employment) showed the country added 236,000 jobs in March, down from the 326,000 added in February. Unemployment fell to 3.5%, down slightly from February’s 3.6%. This indicates the American job market is starting to cool off, and in turn will slow down consumer demand for products and services. This would be the result the US Federal Reserve (Fed) has been waiting for since they started raising the benchmark interest rate.

Along with the higher interest rate, the banking crisis may be having the same effect as an interest rate hike and function as a brake on the economy. Since the collapse of two regional banks, it has become harder to borrow money because banks have become more cautious with their lending practices’ which in turn has made it harder to access credit. The combination of higher interest rates and the slowdown caused by the banking crisis are cooling the US economy but is it enough for the Fed to stop increasing the interest rate. We shall see come May 2.

Its interesting how a few months ago investors were happy when data indicated a slowing economy. It seemed as if the Fed’s interest rate hikes were working, and they could ease up on the interest rate hikes they were using in their battle to get inflation back to their target of 2%. Today, investors no longer are cheering similar economic data because instead of showing inflation falling, it indicates a recession may be on the horizon.

It was a short week as investors prepare for the arrival of the Easter Bunny this weekend. It was not a great week but at least the markets did not lay an egg this past week. 😊 With that weak attempt at humour out of the way, let’s see what happened this past week….

Weekly Market Review

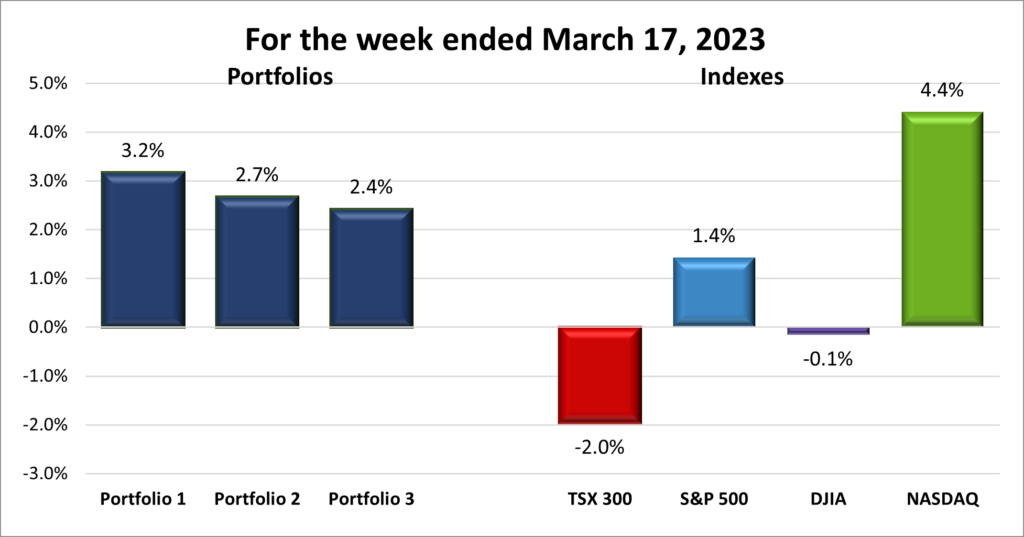

Monday: The second quarter got off to a good start with three of the four major North American indexes climbing higher. An unexpected cut to oil supplies sent oil prices surging as well as the share prices of many oil companies.

In Canada, the Toronto Stock Exchange Composite Index (TSX) got a boost from the higher oil prices, helping it extend its winning streak to seven straight days of gains. The Energy sector was the best performing sector in Canada, followed by Basic Materials (miners and fertilizer manufacturers) and Financials. All the other sectors ended the day lower, with the Technology and Healthcare sectors dropping the most.

In the US, the S&P 500 Index (S&P) and the Dow Jones Industrial Average (DJIA) ended higher, while the Nasdaq Composite Index (Nasdaq) ended the day slightly lower. Economic data showed a decrease in US manufacturing activity for the fifth straight month suggesting inflation in the US continued to fall. However, the good news was offset by expected higher oil prices this summer. Energy costs are a big driver of inflation so inflation could inch back up. In the American markets, the Energy sector had a great day (up 5%), more than five times higher than the second place Healthcare sector. The Utilities and Consumer Cyclicals had the biggest falls.

Tuesday: Winning streaks were broken today as the markets slipped lower on economic news that the US economy could suffer a sharp downturn. At the same time, the weaker data gave investors hope the Fed would pause future rate hikes. Oil prices managed a slight increase despite fears of falling demand for oil caused by a recession.

In Canada, the TSX started the day higher but quickly fell into the red. A last-minute rally fell short of running its winning streak to eight. On Bay Street, despite ending the day in the red, most Canadian sectors gained ground, led by Telecommunications Services and Basic Materials. However, the declines, led by Consumer Cyclicals and Financials were too much to overcome.

In the US, a selloff in bank shares pushed the indexes lower, ending the winning streaks of the S&P and DJIA. In economic news, the number of job openings in February fell to the lowest since May 2021 indicating the demand for labour was falling. Not great news for workers but a step in the right direction in the Fed’s battle with inflation. As well, factory orders dropped by 0.3%, the second straight month orders had fallen. On Wall Street, only two of the American sectors end higher, Telecommunications Services and Utilities. Leading the indexes lower were Industrials and Basic Materials.

Wednesday: A mixed day in the markets that saw the DJIA as the only index to end in the green. Lower US payroll, a slowing service sector, and slowing employment growth numbers suggest the Fed’s interest rate increases are beginning to dig in as the US economy slows. Fear of a recession is replacing the banking crisis as investors’ biggest concern. Oil prices fell victim to the poor economic news, as well.

In Canada, fresh off a 7-day winning streak, the TSX fell for the second straight day. In trading in the Canadian sectors, the defensive sectors Utilities and Telecommunications Services advanced the most, while the Technology and Industrials sectors had the biggest drops.

In America, both the S&P and the Nasdaq fell on lower-than-expected economic data. The news has investors on edge as they are concerned that the Fed might raise rates again which could push the US economy into a recession. In the American sectors, Utilities and Healthcare had the biggest gains, while Consumer Cyclicals and Technology declined the most.

Thursday: The short week comes to an end with all four indexes scratching out small gains as investors digested weak US labour data ahead of Friday’s US jobs report. On one hand, higher jobs could lead to the Fed increasing the US benchmark rate. On the other hand, a lower number of jobs could signal the world’s largest economy is heading towards a recession. Investors are hoping for a ‘just right’ number that will not prompt the Fed to act while not signalling a recession. Oil prices gave back at bit of gains as analysts believe a recession would lead to lower demand for oil, despite the production cutbacks announced by OPEC+ nations.

In Canada, the economy added 34,700 jobs and unemployment remained at record low levels for March. In the Canadian sectors, the Utilities and Industrials had the biggest gains, while the Energy and Telecommunications Services were the only two sectors to fall back.

In the US, unemployment benefits rose by 228,000 the previous week, suggesting a softening of the American labour market. In the American sectors, the Technology and Utilities sectors had the largest gains, while the Energy and Basic Materials sectors had the biggest drop.

Friday: All North American markets are closed for Good Friday.

Weekly Market and Portfolio Review

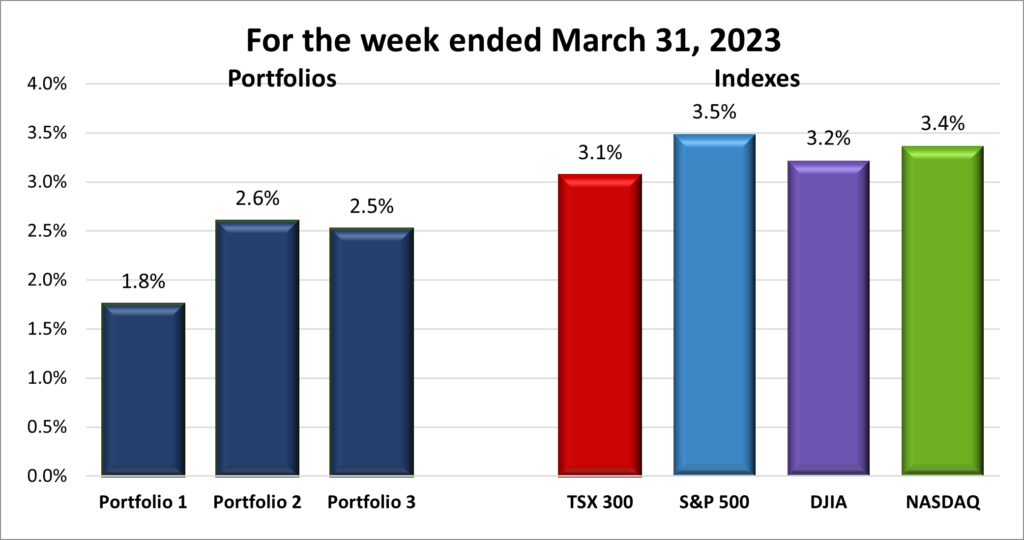

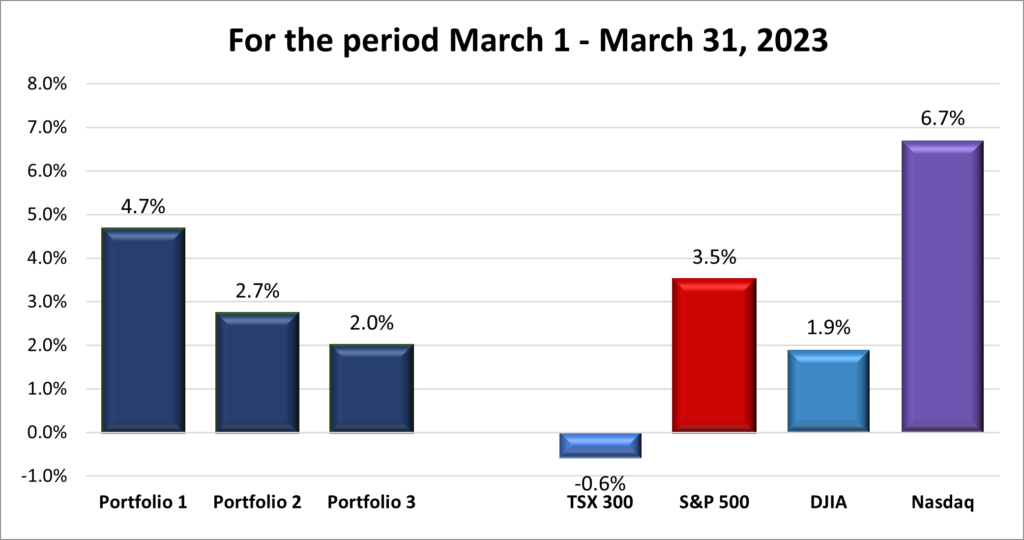

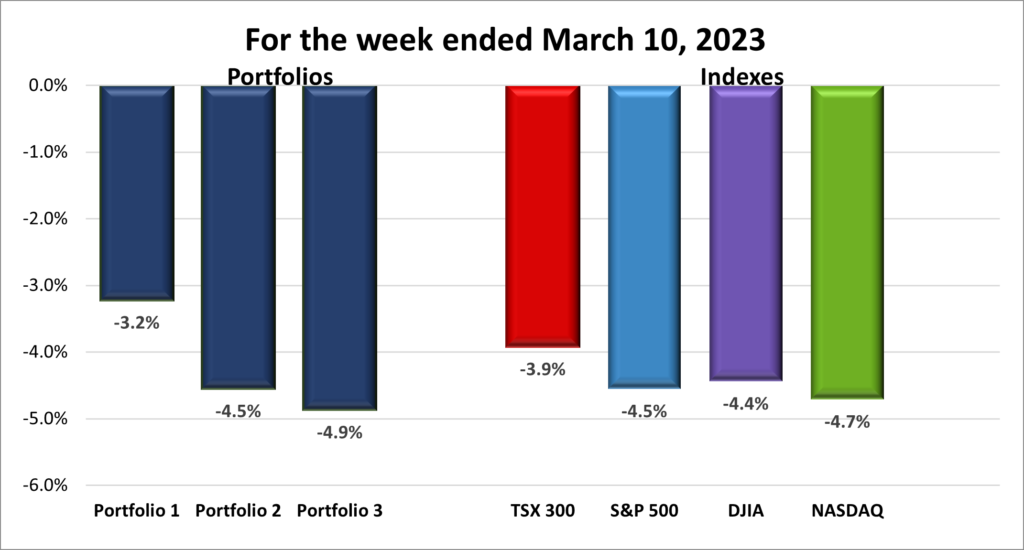

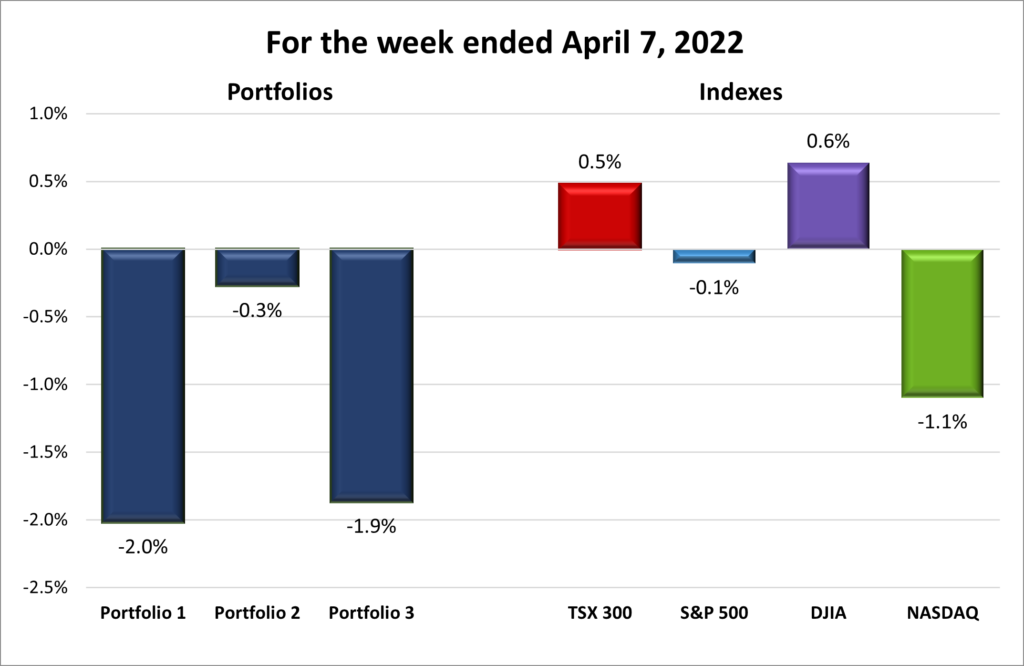

For the week, the TSX (SPTSX) added 0.5%, the S&P 500 (SPX) declined 0.1%, the DJIA (INDU) gained 0.6% and the Nasdaq (CCMP) fell 1.1%.

![]() It was a mixed bag for the four major North American indexes this past week, with the more growth-oriented S&P and Nasdaq both ending lower while the more traditional TSX and DJIA both posted modest gains. An unexpected cut to global oil production sent the indexes higher, especially the TSX and DJIA. Weak US economic news caused the indexes to fall as investors feared the US economy could be headed for a recession. With the threat of a recession on the horizon, the price of oil dropped as a recession meant there would be less demand for oil. Finally, the indexes drifted higher thanks to a late rally in the big technology companies, sending investors off for the Easter weekend cautiously upbeat.

It was a mixed bag for the four major North American indexes this past week, with the more growth-oriented S&P and Nasdaq both ending lower while the more traditional TSX and DJIA both posted modest gains. An unexpected cut to global oil production sent the indexes higher, especially the TSX and DJIA. Weak US economic news caused the indexes to fall as investors feared the US economy could be headed for a recession. With the threat of a recession on the horizon, the price of oil dropped as a recession meant there would be less demand for oil. Finally, the indexes drifted higher thanks to a late rally in the big technology companies, sending investors off for the Easter weekend cautiously upbeat.

In an unusual occurrence, the North American stock markets were closed for Good Friday but not the US government. As a result, the much anticipated (at least by economists and investors) US jobs report was released but the markets were closed, leaving investors three days to consider the data before they can react to the information.

![]()

If it was a mixed bag for the indexes and Nasdaq was one of the indexes that declined, it was unlikely to be a good week for the three Portfolios. It was definitely not a good week for Portfolios 1 and 3 thanks to TD Bank (TSX: TD) and its planned acquisition of US regional bank First Horizon Corporation (NYSE: FHN). TD’s share price is under pressure from short sellers who think TD could be adversely affected by their exposure to US regional banks, where the recent bank crisis originated. Portfolio 2 was the best of a bad lot, a solid week from Microsoft (NASD: MSFT) was not enough to offset the overall decline in technology companies.

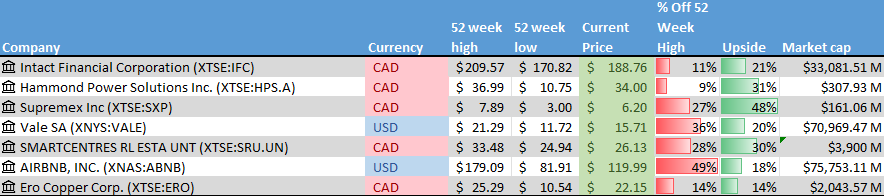

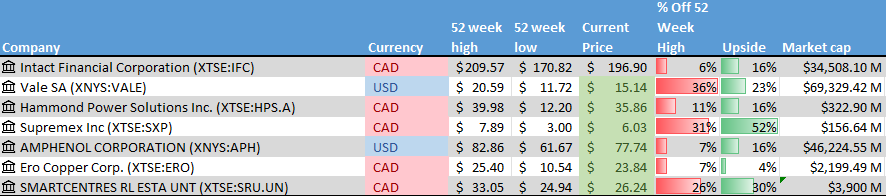

Companies on the Radar

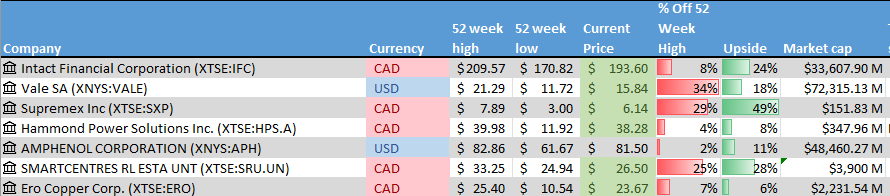

No new companies came across my radar this past week. After running Amphenol (NYSE: APH) through the Quick Test, I added it to the existing companies on my radar. Amphenol and Hammond Power Solutions sound similar so it will be interesting to see how they compare. For now, the radar list consists of:

No new companies came across my radar this past week. After running Amphenol (NYSE: APH) through the Quick Test, I added it to the existing companies on my radar. Amphenol and Hammond Power Solutions sound similar so it will be interesting to see how they compare. For now, the radar list consists of:

- Intact Financial (TSX: IFC): A Canadian mid size insurance company supplying home, car and business insurance in Canada, the US, and the UK.

- Vale (NYSE: VALE): A global mining company that extracts various metals and rare earth elements such as nickel, cobalt, gold, copper, that are used in electric vehicles.

- Hammond Power Solutions (TSX: HPS.A): A small cap Canadian company manufacturing transformers used throughout the world in a wide variety of industries.

- Supremex (TSX: SXP): A small cap company selling packing solutions throughout Canada and the USA.

- Amphenol: Producer of a high-tech interconnect, sensor, and antenna solutions for the automotive, aerospace, industrial and various technology industries.

- Ero Copper Corp. (TSX: ERO): A small cap Canadian copper mining company with mines in Brazil.

- Smartcentres Real Estate Investment Trust (TSX: SRU.UN): Owns and manages a number of income producing malls and retails spaces throughout Canada.

The Radar Check was last updated April 6, 2023.

Portfolio Update

Portfolio 1

Portfolio 1 for the week ended April 7, 2023: DOWN ![]()

- Tesla (NASD: TSLA) saw electric vehicle sales rise 4% in the first quarter 2023 over the previous quarter. Its great that Tesla continues to grow their sales, but one must wonder what the price cuts of up to 20% on some models have done to their profit margins.

- Rivian (NASD: RIVN) delivered over 7,900 vehicles in the first quarter, beating estimate of 7,090 deliveries. Unfortunately, production was 600+ units below the 10,000 estimated. Rivian needs to get their pickups and SUV into the market before competition from Ford (NYSE: F), GM (NYSE: GM) and Tesla heats up. Rivian does not want to get in a price war with its deep pocketed competitors.

- General Motors moved closer to its target of US$2 billion cost savings as 5,000 GM workers took buyouts. On a positive note, GM grew first quarter deliveries by 17.6% on an annual basis. All four GM brands saw growth, led by Buick which saw an increase of 99.2%. GM expects to produce 150,000 electric vehicles in 2023 for the North American market, with a target of one million EVs for 2025.

- Rogers (TSX: RCI.B) closed their merger with Shaw (TSX: SJR.B). At the same time Quebecor (TSX: QBR.B) closed their acquisition of Freedom Mobile from Shaw.

- Britain’s Competition and Markets Authority will take a closer look at Amazon’s (NASD: AMZN) acquisition of iRobot Corp (NASD: IRBT) to determine what impact the deal will have on the smart devices market. The deal is already under investigation by the US Federal Trade Commission.

- The US environmental Protection Agency is set to announce big cuts to vehicle emissions that will spur the conversion to electric vehicles (EV). This is good news for EV manufacturers such as GM, Tesla, and Rivian.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Telus Corp (TSX: T)

Cargojet Inc (TSX: CJT)

US $

ZIM Integrated Shipping Services Ltd (NYSE: ZIM)

Quarterly Reports

No quarterly reports this past week.

Portfolio 2

Portfolio 2 for the week ended April 7, 2023: DOWN ![]()

- Microsoft and Amazon are facing an antitrust investigation by the Ofcom, the British communications regulator. British officials are concerned the two market leaders are using their size and market dominance to create barriers to prevent users from switching to competitors.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

Canadian $

Canadian Natural Resources Ltd (TSX: CNQ)

Alimentation Couche-Tard Inc (TSX: ATD)

Brookfield Renewable Partners LP (TSX: BEP.UN)

US $

No US$ dividends this past week.

Quarterly Reports

No quarterly reports this past week.

Portfolio 3

Portfolio 3 for the week ended April 7, 2023: DOWN ![]()

- A few shareholders have suggested TD Bank should cancel or renegotiate its $13.4 billion acquisition of US regional bank First Horizon. The shareholders are pointing at the unknown risk in US regional banks that sparked the recent banking crisis. TD should be cautious about proceeding with the deal or even walking away and looking for a better deal now that prices for regional banks have fallen.

The deal has also put TD Bank shares under pressure from short sellers after analysts expressed concern about TD’s exposure to US regional banks, particularly their purchase of First Horizon. - Magnite (NASD: MGNI) announced it opened a new office in Stockholm, which will operate as its base across Sweden, Denmark, Norway, and Finland. It is good to see Magnite has a enough business in northern Europe to open an office.

Activity

No significant activity to report this week.

Dividends

Dividends Received this week for the following companies:

Companies followed by DRIP (Dividend Re-Investment Plan) indicate additional shares were purchased with the dividend. Any cash leftover was added to the cash balance.

No dividends this past week.

Quarterly Reports

No quarterly reports this past week.