An Ominous Start to a Historically Volatile Month

Well, August didn’t waste any time making waves. Both the Canadian and US markets opened the month with sharp declines on August 1, but the storm clouds actually started forming the day before. President Trump signed an executive order imposing new import duties, ranging from 10% to 41%, on about 90 countries. Canada was hit with a hefty 35% rate, alongside India, Taiwan, and others. The tariffs didn’t take effect until August 7, but the announcement alone rattled markets, fuelling worries about renewed trade tensions and rising inflation risks.

Then came Friday’s US jobs report, which landed with a thud. Payroll growth in July came in roughly 25% below expectations, and to make matters worse, May and June were revised down by a combined 258,000 jobs. That raised fresh concerns about a slowing economy.

Instead of addressing the slowdown, Trump turned on the messenger by firing the head of the US Bureau of Labor Statistics (BLS) shortly after the report was released. Markets didn’t immediately panic, but the move raised red flags about the credibility of official economic data. Analysts warned that if investors lose trust in key numbers like inflation or employment, it could shake market confidence and eventually lead to higher borrowing costs.

Unfortunately, this wasn’t a one-off. The President has also taken repeated shots at Fed Chair Jerome Powell, including public threats and calls for the Fed to “do as it’s told.” That kind of political pressure puts the central bank’s independence into question, and when trust in both the data and the Fed starts to crack, volatility tends to follow.

We’re only one week into August, and markets are already facing the kind of turbulence the month is known for. It’s not usually the worst month for investors, but it’s often choppy thanks to low trading volume, with many investors on vacation. That leaves markets more vulnerable to headlines – and if there’s one thing this US administration isn’t short on, it’s headlines.

So far, August is shaping up to be every bit as volatile as its reputation suggests.

With all that in mind, let’s take a closer look at what caused the markets to rebound this past week, and how it affected each of my portfolios as we move further into what’s already shaping up to be a volatile August.

Items that may only interest or educate me ….

Canadian Economic news, American Economic news, ….

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Labour Force Survey (LFS)

The latest Statistics Canada labour data showed that Canada’s labour market stumbled in July, shedding 41,000 jobs, the first monthly decline since March and a sharp reversal from June’s 83,100 gain. Analysts had expected a modest increase of 13,500 jobs, making the drop all the more surprising. Most of the losses were in full-time roles and heavily concentrated among youth aged 15 to 24, where employment fell by 34,000. That age group is now facing its highest unemployment rate since 2010 (excluding the pandemic), jumping to 14.6%, with many returning students still struggling to find summer work.

Despite the decline in jobs, the unemployment rate held steady at 6.9%, slightly better than the 7% analysts had forecast, but only because fewer people were actively participating in the labour force. A more troubling trend is the rise in long-term unemployment: nearly one in four job seekers has been unemployed for 27 weeks or more, the highest proportion (outside of COVID years) since 1998.

On the wage front, average hourly pay for permanent employees rose 3.3% year-over-year, slightly higher than June’s 3.2% and above expectations. The average hourly wage ticked up to $36.16 from $36.01.

All in all, July’s report adds to the growing signs that Canada’s economy is losing momentum, especially among younger workers and in consumer-driven sectors. While modest wage growth might give the BoC reason for caution, rising unemployment and weak participation could tip the scales toward a rate cut later this year, hopefully as early as the next BoC meeting in September, assuming inflation stays under control.

Canadian Market Volatility

Canada’s volatility gauge, the S&P/TSX 60 Volatility Index (VIXC), opened the shortened week at 11.01 and traded mostly between 10.0 and 11.0. It briefly dipped to 9.5 midweek as investors grew hopeful that soft US labour data might prompt the Fed to cut interest rates. But that optimism faded quickly, and the VIXC bounced back to the upper 10s before closing the week at 10.63.

If you’re new to the VIXC, think of it as Canada’s version of a fear gauge. A reading below 10 suggests investors are feeling relaxed. Between 10 and 20 points to a steady, business-as-usual market. But once it climbs above 20, that’s when investor nerves start to show and market swings tend to get sharper.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

American Market Volatility

After opening at 20.56, Wall Street’s “fear gauge” – the CBOE Volatility Index (VIX) – drifted lower for most of the week, trading between 18 and 16. A brief jump to 19 came on news of a potential 250% tariff on pharmaceuticals, but the VIX quickly resumed its downward journey to end the week at 15.15.

If you’re new to the VIX, think of it as a real-time pulse check on investor anxiety. It tends to spike when markets get rattled – whether from geopolitical flare-ups, inflation surprises, or something like the Fed chair getting unexpectedly replaced. When fear rises, so does the VIX.

A reading between 12 and 20 suggests calm conditions. Once it pushes past 20, traders start bracing for bigger swings. The higher it climbs, the more uncertainty is being priced into the market.

Weekly Market and Portfolio Review

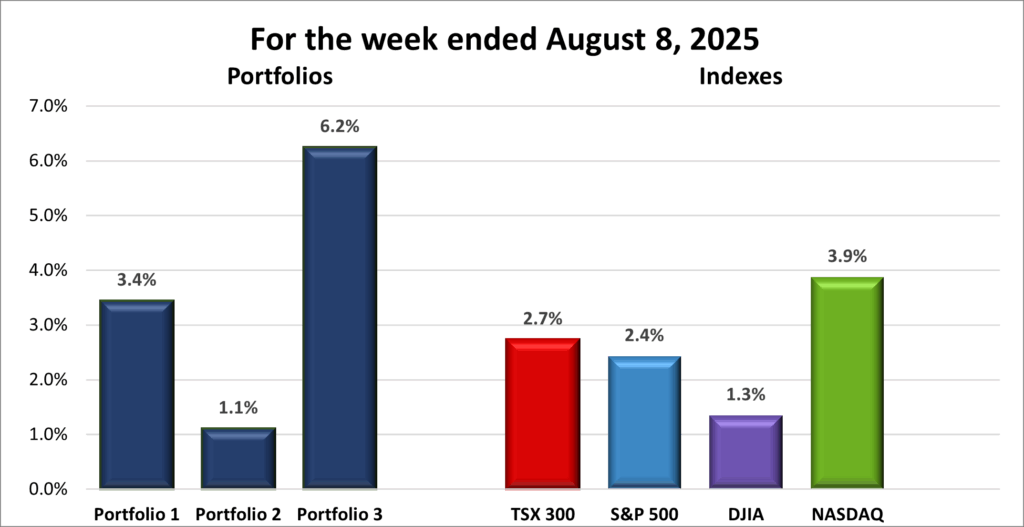

For the week, the TSX (SPTSX) gained 2.7%, the S&P 500 (SPX) rose 2.4%, the DJIA (INDU) rose 1.3% and the Nasdaq (CCMP) surged 3.9%.

| Index | Weekly Streak |

| TSX: | 1 – week winning streak |

| S&P: | 1 – week winning streak |

| DJIA: | 1 – week winning streak |

| Nasdaq: | 1 – week winning streak |

![]() After ending the prior week on a sour note, markets started this one cautiously before powering higher, with the Toronto Stock Exchange Composite Index (TSX) and the Nasdaq Composite (Nasdaq) each notching record highs twice this past week.

After ending the prior week on a sour note, markets started this one cautiously before powering higher, with the Toronto Stock Exchange Composite Index (TSX) and the Nasdaq Composite (Nasdaq) each notching record highs twice this past week.

Monday saw all three major American indexes bounce back sharply from the previous week’s selloff, which was caused by weak job data and fresh tariff announcements. The S&P 500 (S&P), Dow Jones Industrial Average (DJIA), and Nasdaq each rose at least 1.3%. With Canadian markets closed for the civic holiday, the TSX made up for lost time Tuesday, surging more than 2% to a record high, then topping it the very next day.

Analysts and Investors spent the early part of the week digesting President Trump’s shooting of the messenger of a weak labour market, as well as his continuing attacks on Fed Chair Jerome Powell, stoking concerns about the credibility of US government data and Fed decision-making. Trump appointed Stephen Miran, current chair of the Council of Economic Advisors, to temporarily fill a Fed vacancy, while Fed Governor Christopher Wallace appeared as the frontrunner for the chairmanship. Both are considered to favour lowering interest rates.

Ironically, the softer US jobs data provided a silver lining for markets: it boosted hopes for a rate cut in September. Investors bet that a cooling labour market would outweigh the inflationary risks from Trump’s latest round of tariffs, which came into effect this week. The measures covered nearly 200 trading partners, with rates ranging from 10% to 50%, pushing the average US import duty to its highest in a century. Trump also threatened steep new tariffs on India for buying Russian oil, along with massive duties on pharmaceuticals and foreign-made semiconductors – while exempting companies manufacturing in the US or planning to.

Midweek, technology companies took the wheel. Apple (NASD: AAPL) soared after announcing a US$100 billion US manufacturing investment – sidestepping a 50% tariff on goods made in India and lifting the broader tech sector higher. The rally helped push the major indexes back into positive territory despite ongoing trade jitters.

In Canada, the TSX posted its strongest week since September 2024, powered in part by Shopify’s (TSX: SHOP) blowout second quarter results and upbeat third quarter outlook. Shares jumped 21%, making it the most valuable company on the TSX, overtaking Royal Bank of Canada (TSX: RY). I’m happy to report both names are in Portfolio 3. 😊

On the down side, Canada’s labour market showed strain, shedding 41,000 jobs in July – more than had been added in June – driving employment to an eight-month low. The weakness reinforced expectations for a potential BoC rate cut. Meanwhile, new US tariffs on Canadian goods took effect Thursday, though most trade between the two countries is still protected under Canada-US-Mexico Agreement.

In short, the week was a tug-of-war between tariff tensions and weak job data on one side, and surging technology stocks, corporate investment, and growing optimism for rate cuts on the other – with the bulls ultimately coming out on top.

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week winning streak |

| Portfolio 2: | 1 – week winning streak |

| Portfolio 3: | 1 – week winning streak |

![]() A rising tide really did lift all boats last week – and all three of my portfolios sailed higher. Just like in the broader market, it was a tech-driven rally doing most of the heavy lifting.

A rising tide really did lift all boats last week – and all three of my portfolios sailed higher. Just like in the broader market, it was a tech-driven rally doing most of the heavy lifting.

Portfolio 1 climbed 3.4%, with 64% of holdings finishing the week in the green. Standouts included Shopify soaring 27%, Lattice Semiconductor (NASD: LSCC) up 25%, Celsius Holdings (NASD: CELH) jumping 15%, and Apple adding 12%. On the flip side, Navitas Semiconductor (NASD: NVTS) slid 17%, and The Trade Desk (NASD: TTD) plunged over 38% after guiding that third-quarter revenue would likely come in only slightly above expectations – a dramatic fall that clipped what could have been an even better week.

Portfolio 2 was the laggard, up 1.1%, with 51% of holdings posting gains. Guardant Health (NASD: GH) led the charge with a 29% surge, followed by Mitek Systems (NASD: MITK) up 11%. Microsoft (NASD: MSFT) and Fortis (TSE: FTS) both reached record highs during the week, but Microsoft couldn’t maintain the momentum and slid lower to record a weekly loss. ☹

Portfolio 3 took top honors, jumping 6.2%. Gains were spread across 59% of holdings, highlighted by Shopify’s 27% pop and goeasy (TSE: GSY) rising 10%.

All told, it was another enjoyable week across the board, with each portfolio delivering gains in line with its goals and strategy. Strength in the technology sector provided a welcome tailwind, while solid contributions from other sectors added extra lift. With all three portfolios moving higher together, we head into the new week more confident than after the prior week’s slide of more than 1% in all indexes and portfolios, and ready for whatever twists and turns August brings.

Companies on the Radar

No new companies appeared on my radar this past week, but I did remove three: Aritzia ((TSE: ATZ), Amer Sports (NYSE: AS), and TerraVest Industries (TSE: TVK). It might seem surprising to drop the top three names from my Radar Test, but after running them through my updated Quick Test, all three scored below 70%. That doesn’t mean they’re bad companies – they just don’t meet my current criteria.

No new companies appeared on my radar this past week, but I did remove three: Aritzia ((TSE: ATZ), Amer Sports (NYSE: AS), and TerraVest Industries (TSE: TVK). It might seem surprising to drop the top three names from my Radar Test, but after running them through my updated Quick Test, all three scored below 70%. That doesn’t mean they’re bad companies – they just don’t meet my current criteria.

They may still be solid picks for other investors, but I’m looking for companies that check more of my boxes. Fortunately, a few did: the three remaining stocks on my radar all scored above 80%, which means they’re moving on to the next phase – my Deep Dive analysis (once I finish refining that checklist!).

So after a bit of pruning, my radar list is now made up of these three companies:

- Mainstreet Equity Corp. (TSE: MEQ): a Calgary-based real estate company focused on mid-market apartment buildings – typically under 100 units – across Western Canada. It buys underperforming properties at below-market prices, renovates them, and increases rental income through improved operations. With strong demand for rental housing, a repeatable value-add strategy, and a solid balance sheet, Mainstreet offers a compelling mix of income and growth. Shares currently trade below net asset value, giving investors a margin of safety alongside steady cash flow and long-term upside.

- Secure Energy Services (TSE: SES): a Canadian industrial company that focuses on environmental and waste management services for energy and industrial clients. It offers recycling, disposal, and infrastructure support across North America.

- Copart (NASD: CPRT): this American company runs one of the world’s largest online vehicle auction platforms, specializing in salvage cars from accidents and natural disasters. It sells on behalf of insurers, dealerships, rental companies, and individuals. Copart earns revenue through transaction fees, storage, transportation, and listing services. Its digital model, global buyer network, and asset-light approach support strong margins and steady growth. With no long-term debt and rising tailwinds from vehicle values and insurance claims, it’s a steady growth story that’s earned a spot on my radar.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated August 8, 2025.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!