From Wild West to Launchpad: The Story of the TSXV

A few weeks ago, I took a look at the history of Canada’s premier stock market – the Toronto Stock Exchange (TSX). Also known as the big board, it’s the top rung on the TSX ladder. I also mentioned its junior counterpart, the TSX Venture Exchange (TSXV). This week, I thought I’d follow up with a closer look at this often overlooked but essential part of Canada’s market ecosystem. So, without further ado, in the words of Daenerys Stormborn – “Let’s begin.”

TSX Venture Exchange (TSXV)

The story of the TSX Venture Exchange actually starts long before its 2001 launch. For decades, the Vancouver Stock Exchange (VSE) was the beating heart of Canada’s junior markets – a place where early-stage mining, exploration, and resource companies tried to raise their first rounds of public capital. Through the boom-and-bust decades of the 70s, 80s, and especially the 90s, the VSE built a reputation for fast-moving, high-risk speculation. At its best, it helped launch companies that later became major players. At its worst, it was known for volatility, lightly capitalised issuers, and the occasional scandal – all of which gradually eroded investor confidence, earning it the moniker ‘the Wild West,’ where anything could happen.

By the late 1990s, Canada’s capital markets were split across four regional exchanges – Toronto, Montreal, Vancouver, and Alberta – each running independently. With electronic trading becoming standard and markets becoming more global, that patchwork system started to feel dated. Regulators and the exchanges agreed a more modern structure was needed.

In 1999, a national restructuring plan was announced: Toronto would take over senior equities, Montreal would handle derivatives, and the Vancouver and Alberta exchanges would merge to form a unified, modern home for early-stage companies. That new exchange officially debuted in 2001 as the TSX Venture Exchange (TSXV).

The TSXV inherited the entrepreneurial spirit of the VSE but paired it with stronger governance, national oversight, and clearer listing rules. Its purpose was straightforward: provide a home for Canada’s small-cap and micro-cap companies – especially those in mining, energy, technology, and emerging sectors – while giving them a clear pathway to “graduate” to the main TSX once they demonstrated financial strength, liquidity, and stability.

In other words, the TSXV took the adventurous DNA of the old Vancouver market and blended it with the credibility and structure of the modern TMX Group (owners of the TSX) ecosystem. Today, it remains one of the most active junior markets in the world and an essential starting point for companies aiming to grow into future leaders on the big board. Kraken Robotics (TSXV: PNG), which ranked #1 on the TSXV’s 2025 Venture 50 list, is a great example of the type of early-stage firm that often eyes that next step.

Together, the TSX and TSXV form a pretty unique ecosystem: a place where brand-new, high-potential companies can get their start, and where the most successful eventually grow into some of Canada’s biggest names. It’s a ladder that supports every stage of the journey — from the first raise to the big board. For investors, it offers both ends of that spectrum — speculative early-stage opportunities on one side and mature, stable companies on the other.

So, as you follow the markets each week, it’s worth remembering that Canada’s investing landscape isn’t just about the giant blue-chips on the TSX. The TSXV is where a lot of those stories actually begin – long before they hit the headlines. After all, today’s small-cap company (a smaller, early-stage firm with a market value under about $2 billion) could be tomorrow’s market heavyweight (one of the big, established leaders on the TSX, often valued in the tens of billions), and becoming an early owner of one of those future leaders is one of the most exciting parts of investing. With that quick tour of how Canada’s junior market went from the Wild West to a proper launchpad, let’s shift back to what’s been happening in the markets this past week.

Items that may only interest or educate me ….

Walmart Reveals Its Inner Tech, Canadian Economic News, US Economic News, ….

Walmart Reveals Its Inner Tech

As of Tuesday, Walmart (NASD: WMT) no longer trades on the New York Stock Exchange (NYSE) – but don’t worry, it didn’t go private or pull any dramatic stunts. Instead, it’s now officially a Nasdaq-listed company, marking a symbolic shift in how it wants the world to see it. After more than half a century on the NYSE, Walmart says the move better matches what it’s becoming: a “people-led, technology -powered omnichannel retailer,” as CEO Doug McMillon puts it.

The switch isn’t just a change of scenery. It’s Walmart raising its hand and saying, “We don’t want to be seen as old-school retail anymore.” Nasdaq is home to the world’s biggest technology and growth names – Apple (NASD: AAPL), Microsoft (NASD: MSFT), Amazon (NASD: AMZN), Nvidia (NASD: NVDA) – and by joining them, Walmart is signaling that its future is tied to technology and innovation just as much as store aisles and rollback stickers. With major investments in automation, artificial intelligence (AI) tools, logistics technology, e-commerce, and its fast-growing advertising business, Walmart is clearly angling for a perception shift toward higher-growth territory.

For investors, the move is really about reframing the story. The day-to-day business didn’t suddenly change, but the narrative around the stock might. Trading alongside technology leaders puts Walmart in a brighter, more growth-focused spotlight, which helps underline the direction the company is already heading. It’s also a practical move: some index funds and ETFs only hold Nasdaq-listed companies, so the switch naturally broadens the pool of potential investors. More visibility can translate into more demand over time.

At the end of the day, the fundamentals still matter most – revenue, margins, execution – but this exchange change reinforces Walmart’s long-term transition into a technology enabled retail powerhouse. It’s a small tweak with the potential for a big perception lift as the company keeps pushing further into digital growth.

Canadian Economic News

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Bank of Canada Rate Decision

As expected, the BoC held its benchmark interest rate at 2.25%, marking its first pause after two straight cuts. The Bank didn’t commit to more easing, but it kept the option open depending on how the economy plays out.

The decision to stay put comes down to one thing: the Canadian economy has been handling global uncertainty better than many expected. Even with the drag from US tariffs, recent data showed stronger-than-expected Gross Domestic Product (GDP) growth in the third quarter and steady job gains, suggesting the slowdown isn’t as heavy as feared. Still, the Bank sees the economy as being in a slump overall. Officials noted that the third quarter bump “largely reflected volatility in trade” as Canada adjusts to the new global backdrop shaped by President Trump’s trade policy. They also expect fourth-quarter GDP to come in weak, with net exports likely to decline because of tariff fees. Inflation is edging closer to the Bank’s target, even though some underlying pressures are still sticking around. Taken together, BoC officials feel the current rate is “about the right level” to keep inflation moving in the right direction while giving the economy enough support heading into 2026.

For now, holding steady brings a bit of stability – borrowing costs should stay roughly where they are, giving households and businesses a clearer path to plan ahead. But with global risks still swirling and economic signals mixed, all eyes will be on the BoC’s next decision on January 28, 2026, and on how inflation, jobs, and trade develop in the months ahead.

Canadian Market Volatility

Canada’s VIXC – basically the TSX’s own “fear gauge” – started the week at 12.15 and stayed pretty much in a tight band between 12.5 and 13 heading into the BoC and the Fed’s rate decisions. The reaction to the Canadian central bank’s decision was largely anticlimactic and barely moved the fear gauge’s needle. However, following the Fed’s announcement the needle dropped as low as 11.57 from 12.9. Once the decision passed, the fear gauge returned to the 12.5 range before drifting lower to end the week at 11.75.

Think of the VIXC as Canada’s market mood ring: the low teens mean things are steady and watchful, not tense – investors are keeping an eye on the road, but there’s no panic in the cabin.

US Economic News

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Federal Reserve Rate Decision

The Fed wrapped up its last meeting of the year with a move most people saw coming: another 0.25% rate cut. That brings the US benchmark rate down to 3.5%–3.75%, marking the third cut in a row. The vote wasn’t unanimous, though – it came in at 9–3, the most disagreement the Fed has seen in years. Two officials wanted to keep rates where they were, and President Trump’s newly appointed member pushed for a much larger 0.5% cut. With this move, the Fed has now lowered rates by 1.75 percentage points over the past 15 months.

During his press conference, Fed Chair Jerome Powell explained the reasoning behind the move. The economy is still growing, but at a slower, steadier pace. Hiring has cooled, unemployment has edged a bit higher, and inflation is still above where the Fed wants it. With those factors in mind, policymakers feel the job market is becoming more vulnerable, and this rate cut is meant to give the economy a bit of support and help prevent a deeper slowdown in hiring.

Powell’s term ends in May 2026, which means he has only three more rate decisions left. With that in mind, this cut could very well be the final one he oversees, depending on how the economy evolves in the months ahead.

For consumers, lower rates basically mean borrowing becomes a bit cheaper. Things like mortgages, car loans, and business loans could see slightly lower costs, which can help support spending and hiring. But because inflation is still a concern, the Fed doesn’t expect to keep cutting at the same pace. Officials signalled they expect only one cut in 2026, and Powell repeated that future moves will depend on what happens with inflation, the job market, and overall economic momentum.

Labour data

The recent US government shutdown has thrown a wrench into the usual flow of labour data, delaying several key reports the Fed and investors typically lean on. This week we finally got the October Job Openings and Labor Turnover Survey (JOLTS) report, with the Employment Situation Summary (ESS) set to follow next week. Things should settle down in January, when the release schedule returns to normal and we get JOLTS, the ESS, and the ADP Employment Report all in the first week of the month like usual.

Job Openings and Labor Turnover Survey (JOLTS)

The Bureau of Labor Statistics (BLS) finally released the delayed October JOLTS report, showing 7.670 million job openings – just barely above September’s 7.658 million. Because of the recent government shutdown, BLS cancelled the September report and folded that data into the October release, so this update is doing double duty.

At first glance, the headline number looks steady enough, but the details tell a softer story. The quits rate – basically how confident workers feel about leaving a job for something better – slipped to 1.8%, the lowest (outside the pandemic) since 2014. Layoffs also ticked higher, hinting that employers are becoming more cautious and more willing to trim staff than take on new hires.

So, while the openings number looks fine, the underlying trends suggest a labour market that’s losing some momentum. A cooling job market can mean weaker consumer spending ahead, which puts pressure on profits, especially for companies tied to retail, services, and other interest-rate-sensitive areas. With inflation still hanging around and job growth showing cracks, reports like this add fuel to the fire that the Fed will lower rates at this week’s meeting.

American Market Volatility

The CBOE Volatility Index (VIX) – the market’s “fear gauge” – had a pretty relaxed week. It opened at 16.15 and inched up toward 17.5 as traders braced for the Fed’s rate decision. But the moment the cut was announced, the VIX let out a sigh of relief, slipping back under 16 and finishing the week at 15.74.

Think of the VIX as the market’s pulse. A few weeks ago it was racing, signalling nerves, but this week it settled into a steady, healthy rhythm. Investors aren’t totally carefree, but they’re definitely breathing easier as borrowing costs edge lower.

Weekly Market and Portfolio Review

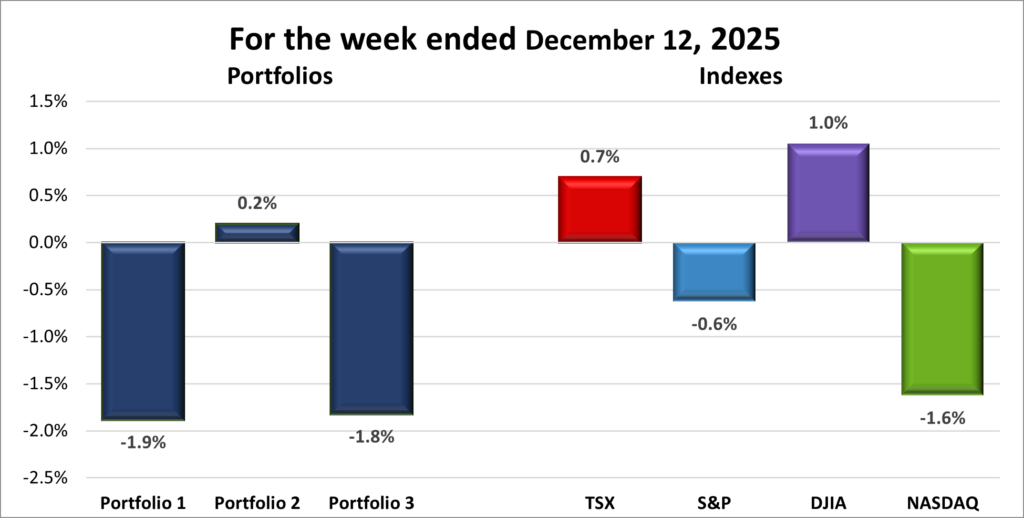

For the week, the TSX (SPTSX) gained 0.7%, the S&P 500 (SPX) slipped 0.6%, the DJIA (INDU) climbed 1.0% and the Nasdaq (CCMP) declined 1.6%.

| Index | Weekly Streak |

| TSX: | 1 – week winning streak |

| S&P: | 1 – week losing streak |

| DJIA: | 3 – week winning streak |

| Nasdaq: | 1 – week losing streak |

![]()

![]() Once again, the week opened on a soft note, leaving the four indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – each starting out in a small hole. From there, the indexes steadily climbed their way back as the days went on. The rebound was strong enough to push the TSX, S&P, and DJIA to fresh record highs midweek, but some late week selling trimmed those gains. By Friday’s close, only the TSX and the DJIA managed to hang on to gains, while the S&P and Nasdaq slipped back into the red.

Once again, the week opened on a soft note, leaving the four indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – each starting out in a small hole. From there, the indexes steadily climbed their way back as the days went on. The rebound was strong enough to push the TSX, S&P, and DJIA to fresh record highs midweek, but some late week selling trimmed those gains. By Friday’s close, only the TSX and the DJIA managed to hang on to gains, while the S&P and Nasdaq slipped back into the red.

With earnings season essentially wrapped up, central banks took centre stage. The BoC’s decision to hold rates was important to Canadians, but all eyes were on the Fed’s final rate decision of 2025. Slower job growth ultimately overshadowed stubborn inflation, and the Fed lowered its benchmark rate to 3.75%. Many analysts now see one, maybe two, cuts in 2026. One isn’t ideal, but it’s better than none, and the overall tone was positive enough to lift market sentiment.

After the announcement, Fed Chair Jerome Powell said the reduction leaves policy “well positioned” and back in a neutral zone, meaning interest rates aren’t holding the economy back the way they were before. He emphasized that the Fed wants to give these cuts time to work through the economy before making any further moves.

In Washington, President Trump said he’s leaning toward either National Economic Council Director Kevin Hassett or Fed Governor Kevin Warsh as the next Fed chair once Powell’s term ends in May. Both are generally viewed as more open to rate cuts than Powell, and Trump has been clear he wants a chair more aligned with his push for looser policy. No decision has been made yet, but markets are already watching closely since the next chair will help shape the policy outlook for years.

Late in the week, the technology sector ran into fresh wobbles. Oracle (NASD: ORCL) missed earnings expectations and announced plans to pour an additional US$15 billion into new datacentres. Broadcom (NASD: AVGO) then added pressure by warning that its margins could shrink going forward. Together, these updates revived concerns about an AI bubble and whether the massive investment pouring into the sector will pay off quickly enough to justify today’s lofty price tags. The sharp pullback in Oracle and Broadcom spilled over into the rest of the AI-related names, weighing on the Nasdaq and, to a lesser extent, the S&P.

In Canada, the TSX dipped early in the week as investors took profits and waited for the BoC and Fed decisions. Once the BoC held rates at 2.25% and pointed to the economy’s better-than-expected resilience, and the Fed followed with its cut, confidence returned. Strong trade data and rising gold and silver prices gave the TSX an extra lift, helping it outperform its American counterparts by the week’s end.

All told, it was a week shaped by central-bank decisions, supported by commodities, and briefly unsettled by another round of AI spending worries. The selling pressure was largely confined to the technology sector, rather than a sign of broader market weakness. With only a few weeks left in the year, Santa and his rally are welcome to show up anytime now. 😊

| Portfolio | Weekly Streak |

| Portfolio 1: | 1 – week losing streak |

| Portfolio 2: | 3 – week winning streak |

| Portfolio 3: | 1 – week losing streak |

![]()

![]() If the markets had shut down on Thursday, all three portfolios would have looked much healthier. Instead, a full five-day week brought renewed fears of an AI bubble, dragging Portfolios 1 and 3 lower. That headwind offset some good news for those two portfolios when the US Commerce Department cleared Nvidia to sell its H200 AI chips in China. The H200 is currently the most powerful chip Nvidia can sell in the Chinese market and was specifically designed for it, though it doesn’t match the capabilities of the Blackwell chips. With China representing a US$50 billion opportunity for Nvidia, this is a major win for the company and its shareholders (of which I’m one 😊).

If the markets had shut down on Thursday, all three portfolios would have looked much healthier. Instead, a full five-day week brought renewed fears of an AI bubble, dragging Portfolios 1 and 3 lower. That headwind offset some good news for those two portfolios when the US Commerce Department cleared Nvidia to sell its H200 AI chips in China. The H200 is currently the most powerful chip Nvidia can sell in the Chinese market and was specifically designed for it, though it doesn’t match the capabilities of the Blackwell chips. With China representing a US$50 billion opportunity for Nvidia, this is a major win for the company and its shareholders (of which I’m one 😊).

Portfolio 1 had the roughest week, tumbling 1.9%. Still, the overall performance was better than expected, with 43% of holdings posting gains. With less than half the holdings in positive territory, the portfolio needed a lift from its largest positions. Unfortunately, seven of the ten biggest holdings lost ground, and a 13% drop by Navitas Semiconductor (NASD: NVTS) basically locked in the weekly loss. The one bright spot was TD (TSE: TD), which set a record high and provided a rare highlight.

Portfolio 2 was the only portfolio to finish the week higher, posting a modest 0.2% gain. Interestingly, it had the lowest percentage of winners at just 42%, but that didn’t stop it from outpacing the others. Record highs from Aritzia (TSE: ATZ) and Dollarama (TSE: DOL) were early-week highlights, even though both eased back slightly by Friday.

Portfolio 3 also had a tough week. It had the best winning percentage at 45% of holdings in positive territory, but losses from Nvidia, the largest holding, and a 13% drop in Vertiv Holdings (NYSE: VRT) outweighed the gains, leaving the portfolio down 1.8% for the week. Shopify (TSE: SHOP), the second-largest holding, posted a weekly gain that helped limit the damage. As with Portfolio 1, TD reaching a record high was a rare but welcome bright spot.

All in all, it was a week of mixed results. The AI stocks that powered the markets, and my portfolios, for much of the year took a step back as AI bubble concerns resurfaced, prompting a rotation toward more value-oriented names. I’ve been riding the tailwinds of the AI theme for nearly two years now, so it’s hard to complain when the portfolios run into a bit of headwind. As the band Trooper put it, every now and then, a little rain has to fall. 😊

Companies on the Radar

Once again, no brand-new names landed on my radar this week, but there was some movement. After giving Corning Incorporated (NYSE: GLW) a closer look – the glassware and fibre-optics company – I decided to move it to the back burner. I was really hoping it would score above 80% on my Quick Test and give me the green light to invest, but a few things held it back. The stock looks a bit expensive right now, and a couple of other companies on my list scored noticeably better, including GE Aerospace (NYSE: GE), which has stronger recurring revenue and a more durable moat. On top of that, all three of my portfolios are already fairly technology-heavy, so I’m reluctant to add another technology-leaning name at the moment.

Once again, no brand-new names landed on my radar this week, but there was some movement. After giving Corning Incorporated (NYSE: GLW) a closer look – the glassware and fibre-optics company – I decided to move it to the back burner. I was really hoping it would score above 80% on my Quick Test and give me the green light to invest, but a few things held it back. The stock looks a bit expensive right now, and a couple of other companies on my list scored noticeably better, including GE Aerospace (NYSE: GE), which has stronger recurring revenue and a more durable moat. On top of that, all three of my portfolios are already fairly technology-heavy, so I’m reluctant to add another technology-leaning name at the moment.

Corning not gone for good, though. It’s still on my radar, just not front and centre. If the share price pulls back and the valuation becomes more reasonable, I’d happily take another look. I’d love to be an owner someday – just not at today’s price. For now, my focus stays on the five companies below.

- GE Aerospace: This is the large American aviation and defence business that remained after General Electric split into three separate companies in 2024. It has been on a strong run thanks to high demand for commercial jet engines as global air travel continues to recover. The company focuses on aircraft propulsion systems and services for both commercial and military customers, and it’s also moving into drones. As a global leader in jet engines and aircraft systems, GE Aerospace offers exposure to long-term trends in travel, defence spending, and emerging aviation technology.

- Napco Security Technologies, Inc. (NASD: NSSC): A small US company that provides security hardware and systems like smart locks, intrusion alarms, fire alarms, and access control solutions. It sells through a network of distributors and installers, and has been increasing its recurring service revenue – something investors usually like to see. As demand for security and smart home products grows, Napco has multiple avenues for expansion.

- Mainstreet Equity Corp. (TSE: MEQ): A Calgary-based real estate company focused on mid-market apartment buildings across Western Canada. Their business model is straightforward: buy underperforming buildings, renovate them, improve operations, and increase rental income. With strong demand for rentals, a disciplined approach, and shares that trade below the estimated value of the properties, Mainstreet offers a combination of income, stability, and long-term upside.

- Dutch Bros Inc. (NYSE: BROS): A rapidly expanding drive-thru coffee chain in the US, known for its energetic customer service and customizable drinks. The company is aiming to open at least 160 new locations by the end of 2025 and has long-term goals of surpassing 2,000 stores. Strong brand loyalty, especially in the Western US, makes this an interesting high-growth story – though still in an aggressive build-out phase.

- XPEL, Inc. (NASD: XPEL): A growing, founder-led maker of protective films, coatings, and related products – best known for automotive paint protection film. XPEL has been expanding into window films and architectural applications, and sells through multiple channels, giving it both reach and control. It’s a company with a focused niche and strong brand recognition in that niche.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated December 12, 2025.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!