Will Santa Show Up for the Markets This Year?

Typically, September and October are considered two of the softer months for the markets, while November and December are traditionally stronger. This year has been the opposite, with a surprisingly solid September and October. By the end of October, I was feeling optimistic – with two of the more volatile months in the rear-view mirror, a strong finish to the year seemed likely. Unfortunately, that optimism didn’t pan out, as November came in weaker than usual and barely avoided slipping into the red.

Now December is here, and I’m not sure what to expect. December is usually a strong month for stocks, thanks to what’s known as the Santa Claus Rally. But some analysts are suggesting we may not see Santa’s visit this time around, which got me wondering why a month that’s typically upbeat might fall short. So why do analysts think Santa may sit this year out? Let’s take a brief look – but first, what makes December a strong month?

A Santa Claus Rally is a stretch of time when markets tend to drift higher during the last week of December and the first couple of trading days in January. It’s not guaranteed, but historically this period has shown a fairly strong pattern of positive returns. There isn’t one official reason why it happens, but there are a few popular theories: lighter trading volumes around the holidays, investors feeling more optimistic heading into the new year, and portfolio managers making final adjustments before closing the books. Over time, this seasonal bump showed up often enough that it earned the nickname “Santa Claus Rally.”

Some analysts think a Santa Claus Rally might not show up this year, and it mostly comes down to uncertainty and caution in the markets. If investors are worried about slowing economic growth, sticky inflation, or what the Fed might do next, that usual year-end optimism can fade pretty quickly. On top of that, if markets already made a strong run earlier in the fall, there may simply be less momentum left. And with holiday trading volumes typically thin, even minor negative headlines can have an outsized impact, making it harder for that seasonal rally to take shape.

So, will Santa make an appearance this year? It’s impossible to know for sure. December has historically been a strong month for stocks, but with lingering economic uncertainties and a market that’s already had a good run, this year could be different. With that in mind, let’s take a look at what actually happened in the markets this past week and see how things are shaping up as we head into the end of the year.

Items that may only interest or educate me ….

ChatGPT Turns 3, Cyber Weekend, Canadian Economic news, US Economic news, ….

ChatGPT Turns 3: From Experiment to Must-Have Tool

It’s hard to believe it’s already been three years since ChatGPT made its public debut. What started as an experiment in conversational artificial intelligence (AI) has grown into a tool millions of people use every day, yours truly included, – for writing, learning, brainstorming, coding, and even managing complex projects. Along the way, each new version has brought smarter, faster, and more reliable capabilities, and the journey isn’t stopping anytime soon. Let’s take a quick look back at how ChatGPT has evolved and what the future might hold.

November 2022 – ChatGPT (GPT-3.5)

The first public release of ChatGPT was based on GPT-3.5, and it made waves for being able to have surprisingly human-like conversations. Users could ask questions, get explanations, write content, or brainstorm ideas. While it was powerful, it sometimes gave inaccurate answers, struggled with very long conversations, and didn’t fully understand context in complex discussions.

March 2023 – GPT-4

GPT-4, available to ChatGPT Plus users, was a big step forward. It could handle more complex prompts, keep track of longer conversations, and generate more accurate, nuanced responses. It also improved reasoning skills, creativity, and context understanding, making it more useful for both casual users and professional tasks.

2023 – GPT-5 mini (current version)

GPT-5 mini focuses on speed, reliability, and conciseness, while keeping high-quality responses. It’s designed to be more aware of subtle context cues and follow nuanced instructions better than previous versions. This makes it great for tasks like writing, research summaries, code, and interactive Q&A.

Looking Ahead – Future Versions

Looking ahead, GPT‑6 is shaping up to be a big step forward. One of the biggest goals is memory and personalization, so the AI can remember your preferences, writing style, and past conversations – making it feel more like a long-term assistant than a series of one-off chats. It’s also expected to handle multi-step tasks more intelligently, break projects into parts, fetch data, and even plan complex workflows.

On top of that, GPT‑6 should be smarter, more reliable, and more versatile. We’re talking improved reasoning, fewer mistakes, better explanations, and stronger multimodal skills – including images, video, and other dynamic inputs. Faster performance and more efficient responses are also in the works, so it could feel snappy even when tackling complicated tasks. If these features arrive, GPT‑6 may finally feel less like a tool and more like a true personal assistant, guiding projects, offering continuity, and anticipating your needs in a way today’s AI can’t quite match.

In short, ChatGPT started as a surprisingly capable conversational AI and has steadily improved in accuracy, reasoning, and usability – and the future promises even smarter, more helpful, and more adaptable versions.

Cyber Weekend Shows Consumers Still Have Some Spark

This year’s Cyber Weekend was a strong reminder that consumers are still willing to open their wallets when the deals are good enough. In the US, online spending from Thanksgiving through Cyber Monday reached an impressive US $44.2 billion, up 7.7% from last year. Cyber Monday alone brought in US $14.25 billion, making it the biggest online shopping day ever recorded. In Canada, national spending totals are harder to pin down, but we did get a solid hint from Block, Inc. (NYSE: XYZ), which processed over 6.15 million transactions during the long weekend – an 18% jump compared to last year.

At first glance, this record spending seems to contradict last week’s Consumer Confidence Index, which suggested Americans were becoming more cautious and cutting back. But this mix of signals actually lines up with how consumers behave when money feels tight. Instead of stopping spending altogether, many people simply wait for major sales and hunt for the best deals – and Cyber Weekend is basically the Super Bowl of discounts. Even when confidence is low, a few days of aggressive markdowns can still spark a buying frenzy.

For us investors, this tells an important story. Strong holiday sales don’t necessarily mean consumers feel great about the economy, but they do show that demand is still there, at least when prices are right. That can give retail, e-commerce, and consumer-focused companies a short-term lift. But it also suggests a bit of fragility underneath – if economic pressures keep building, spending could cool quickly once the holiday bargains disappear.

Canadian Economic news

This past week’s key economic data that the Bank of Canada (BoC) considers when deciding whether to raise or lower the interest rate.

Labour Force Survey

Statistics Canada’s latest employment report surprised to the upside, showing a gain of 53,600 jobs in November – well above expectations of a 5,000-job decline. This follows a 66,600-job increase in October, marking the third consecutive month of employment gains.

The unemployment rate also came in better than expected, dropping to 6.5% from October’s 6.9%, the lowest level in 16 months. Analysts had forecast a rise to 7.0%. This follows two months of declines after a peak of 7.1% in September, which was the highest reading since May 2016, excluding the pandemic years of 2020 and 2021. Wage growth edged up slightly, reaching 3.6% year-over-year, compared with 3.5% in October.

On the surface, November’s labour numbers are encouraging. Employment is rising, unemployment is falling, and young workers saw a particularly strong boost. For consumers and investors, stronger employment usually supports spending, which helps corporate revenues and economic momentum – especially heading into the holiday season.

That said, there’s a subtle yellow caution flag. Most of the new jobs were part-time, not full-time, suggesting employers are still hesitant to make long-term commitments. Wage growth is still modest, which helps keep inflation in check but may limit additional consumer spending if paycheques aren’t rising meaningfully. In other words, the job market is healthy, but not all gains are equally strong in driving sustained economic momentum.

For the BoC, this hotter-than-expected labour data effectively rules out a rate cut at next week’s meeting. The trend of an improving labour market also dampens expectations of a rate reduction next year, likely keeping the benchmark rate at 2.25% for the foreseeable future.

Canadian Market Volatility

Canada’s VIXC – basically the TSX’s own “fear gauge” – started the week at 14.99 and steadily drifted lower, finishing at 11.77. That’s a pretty calm reading, showing investors are feeling relaxed after strong earnings from the Big 6 banks and growing hopes of a rate cut in the US.

Think of the VIXC as Canada’s market mood ring: the low teens mean things are steady and watchful, not tense – investors are keeping an eye on the road, but there’s no panic in the cabin.

US Economic news

This past week’s key data points that the Federal Reserve (Fed) considers when deciding whether to raise or lower the interest rate.

Labour data

Because of the recent US government shutdown, several key labour reports that the Fed and investors normally rely on have been delayed. Job Openings and Labor Turnover Survey (JOLTS), and the Employment Situation Summary (ESS) were supposed to arrive this week, but they’ve been pushed back until the government fully reopens. That leaves everyone, especially the Fed, working with less visibility into how the job market is actually holding up. For now, the ADP Employment Report is essentially the only fresh labour data we have to go on.

ADP Employment Report

The November ADP National Employment Report came in weaker than expected. Instead of adding the forecasted 10,000 jobs, the private sector shed 32,000 positions – a sharp reversal from October’s 42,000 gain. The decline was broad, but small businesses (those with fewer than 50 employees) were hit the hardest, suggesting they’re tightening their belts as economic uncertainty drags on.

This points to a job market that may be starting to cool. When smaller firms pull back on hiring, it often signals a broader shift toward caution. The silver lining is that softer labour data raises the odds the Fed could lean toward cutting interest rates at next week’s meeting to help support the economy.

It’s also worth keeping in mind that ADP is just one piece of the labour picture. Once the government fully reopens, the delayed labour reports will provide a more complete read on how the labour market is holding up. Until then, visibility is limited, and the ADP numbers are the best guide available.

Consumer Sentiment Index (CSI)

The University of Michigan’s preliminary consumer sentiment index for December surprised to the upside, rising to 53.3 from November’s 51.0 and topping forecasts of 52. Even with that improvement, sentiment remains well below where it stood a year ago, sitting 28% under December 2024’s 74.0. The lift was broad-based across demographics, but younger consumers were the biggest drivers of the rebound, showing an uptick in confidence heading into the new year.

The two sub-indexes offered a more mixed read. The Current Economic Conditions gauge – essentially how people feel about their jobs, income, and day-to-day finances – slipped to 50.7, a modest decline from last month and roughly one-third lower than a year ago. The Expectations Index, which captures what consumers anticipate over the next six months, edged up to 55.0, a 7.8% improvement from November but still 25% weaker than last December. This blend of softer current views and a slightly better outlook points to a cautious shift in sentiment: things still feel tough, but people are a bit more hopeful about what comes next.

On the inflation front, consumers expect prices to rise about 4.1% over the next year and 3.2% over the next five. These readings reflect what people believe the inflation rate will be – and both are down from November, suggesting consumers see inflation easing a little. Even so, expectations remain higher than they were a year ago.

Personal Consumption Expenditures (PCE)

The Commerce Department’s latest PCE report showed that inflation in September barely moved. Headline PCE, which includes all components, rose 0.3%, the same as in August, while the year-over-year increase ticked up slightly to 2.8% from 2.7%, right in line with expectations.

Looking at the core PCE, which strips out the often-volatile food and energy costs, prices rose 0.2% for the month, matching forecasts. On an annual basis, the core index came in at 2.8%, just below the expected 2.9%, but still above the Fed’s 2% target. In other words, inflation is steady, but it hasn’t yet cooled to the level the Fed wants to see.

As we head into the Fed’s meeting next week, the picture is mixed. The PCE report for September is already two months old, so it probably won’t play a key role in the debate. Still, it shows that inflation was stable, if elevated, back then in the early fall. The softer labour market could make the Fed more open to cutting rates to support the economy, but with inflation still above their target, they’re likely to remain cautious. In other words, the door for a rate cut is slightly ajar, but it’s not wide open.

American Market Volatility

The CBOE Volatility Index (VIX) — often dubbed the market’s “fear gauge” — opened the week at 18.05 and steadily drifted lower, dipping below 16 near week’s end before settling at 15.41. The drop reflects growing investor confidence that the Fed is likely to follow through with another 0.25% rate cut. Think of the VIX as the market’s mood ring: in recent weeks it was flashing bright red, signaling worry, but now it’s a calm shade of blue. This reading suggests investors are feeling relatively relaxed, keeping a watchful eye on the markets while anticipating slightly lower borrowing costs.

Weekly Market and Portfolio Review

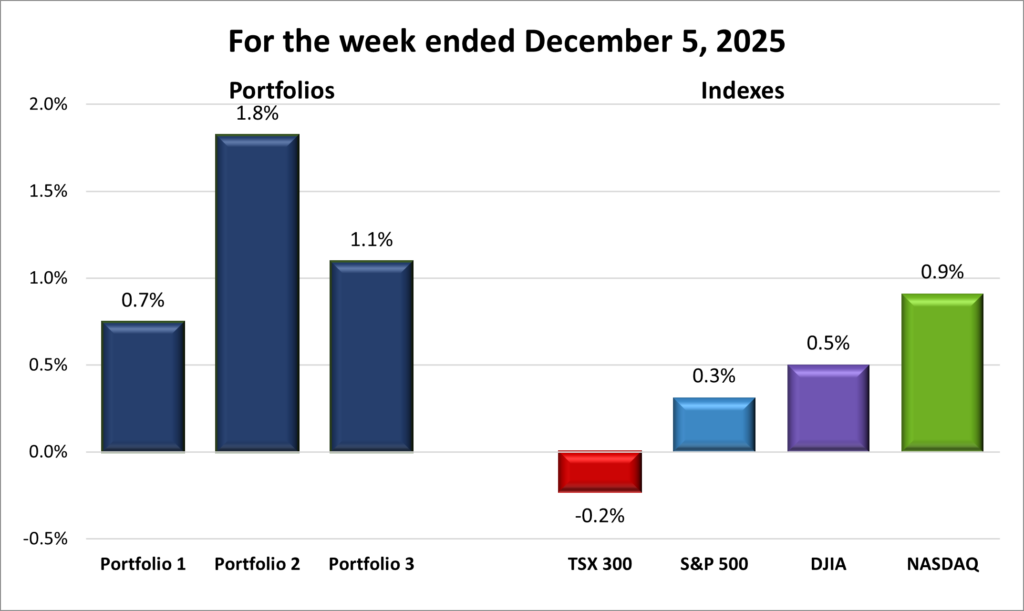

For the week, the TSX (SPTSX) declined 0.2%, the S&P 500 (SPX) rose 0.3%, the DJIA (INDU) advanced 0.5% and the Nasdaq (CCMP) climbed 0.9%.

| Index | Weekly Streak |

| TSX: | 1 – week losing streak |

| S&P: | 2 – week winning streak |

| DJIA: | 2 – week winning streak |

| Nasdaq: | 2 – week winning streak |

![]() After last week’s furious rally that erased most of November’s losses, the markets eased into December with more of a sigh than a sprint. All four major North American indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – stumbled out of the gate but eventually shook off the early dip and all but the TSX had climbed back into the green. By the end of the week, the S&P and Nasdaq had run their win streak to four, bringing the S&P close its a record high. Meanwhile, the TSX had pushed to a new all-time high multiple times during the week before pulling back as investors took some profit after the run up.

After last week’s furious rally that erased most of November’s losses, the markets eased into December with more of a sigh than a sprint. All four major North American indexes – the Toronto Stock Exchange Composite Index (TSX), the S&P 500 Index (S&P), the Dow Jones Industrial Average (DJIA), and the Nasdaq Composite Index (Nasdaq) – stumbled out of the gate but eventually shook off the early dip and all but the TSX had climbed back into the green. By the end of the week, the S&P and Nasdaq had run their win streak to four, bringing the S&P close its a record high. Meanwhile, the TSX had pushed to a new all-time high multiple times during the week before pulling back as investors took some profit after the run up.

With earnings season essentially wrapped up and the Fed in its pre-meeting blackout period, investors were left leaning on economic data for direction. Softer labour and manufacturing numbers pointed to a cooling economy, while the September PCE inflation data came in as expected and hinted that inflation is finally stabilizing. Taken together, this latest batch of reports sparked renewed hope that the Fed would trim rates at its next meeting. That shift in expectations helped revive interest in tech and other growth names, which tend to benefit most when borrowing costs start moving lower.

There was also no shortage of speculation about who will lead the Fed next. Chair Jerome Powell’s term runs until May 2026, but President Trump has made it clear he wants someone new in the role. This week he said he’s already made his choice, and many analysts think Kevin Hassett, his top economic adviser, is the favourite. Whoever ends up in the chair is widely expected to take a more dovish approach, reinforcing the idea that rates could trend lower in 2026.

In Canada, the TSX shook off its early-week stumble and powered to all-time highs twice, helped along by a solid set of earnings from the Big Six banks. Strong results from the country’s financial heavyweights gave the index some welcome momentum just when it needed it.

Commodity strength added even more lift, with oil prices pushing higher and giving energy stocks a noticeable boost. Canada’s latest labour data also surprised to the upside for a third straight month, giving analysts a bit more confidence that the economy may finally be picking up steam heading into the new year. On top of that, growing optimism that the US might cut rates soon encouraged investors to take on a bit more risk, pushing money into sectors that tend to shine when sentiment improves. That positive mood spilled into Canada and helped fuel gains in energy, resources, and financials, rounding out the week for the TSX.

As we head into next week’s big rate decisions, it feels like investors are collectively holding their breath. Everyone knows the next move by the Fed will shape the final stretch of the year, and even small changes in expectations have been enough to sway the markets lately. For now, the mood leans cautiously optimistic. Earnings have held up, the Canadian labour market appears to be gaining momentum, US economic data is cooling just enough to keep hopes for lower borrowing costs alive, and both the American and Canadian markets seem to be finding their rhythm again after a choppy November. If the Fed delivers an early Christmas present for investors, December could still finish on a high note and a late-year rally. 😊

| Portfolio | Weekly Streak |

| Portfolio 1: | 2 – week winning streak |

| Portfolio 2: | 2 – week winning streak |

| Portfolio 3: | 2 – week winning streak |

![]() The week started off a bit sluggish, but as markets found their footing, all three of my portfolios moved higher as well. Strong fourth-quarter results from Canada’s Big Six banks gave things an extra lift across the board.

The week started off a bit sluggish, but as markets found their footing, all three of my portfolios moved higher as well. Strong fourth-quarter results from Canada’s Big Six banks gave things an extra lift across the board.

Telus (TSE: T) also made headlines. The company said it will maintain its dividend at 41.84 cents per share but won’t raise it again until the share price better reflects its growth prospects. It’s also phasing out its discounted DRIP (Dividend Re Investment Plan), which lets investors buy shares at a discount using their dividends. Analysts generally liked the move, but the stock price still pulled back – and that weighed slightly on Portfolios 1 and 2 where it’s held. With that said, here’s how each portfolio performed…

Portfolio 1 lagged the others with a 0.1% gain, but it still saw 56% of its holdings finish the week in positive territory. Lattice Semiconductor (NASD: LSCC) jumped 13%, Navitas Semiconductor (NASD: NVTS) added 12%, and several big names – Apple (NASD: AAPL), Bank of Nova Scotia (TSE: BNS), Walmart (NYSE: WMT), and TD (TSE: TD) – all hit fresh record highs.

Portfolio 2 led the pack with a solid 2.0% gain, handily beating the other portfolios and even doubling the Nasdaq’s 0.9% return, the strongest of the major indexes. About 57% of holdings ended the week higher, helped by a massive 26% surge in MongoDB (NASD: MDB) after strong earnings and an upgraded outlook. Bank of Nova Scotia also reached a new high, riding momentum from its impressive fourth-quarter results.

Portfolio 3 landed in the middle with a 0.3% rise, despite only 45% of its holdings posting weekly gains. The difference-maker was its two giants – Nvidia (NASD: NVDA) and Shopify (TSE: SHOP) – which now make up nearly 55% of the portfolio. Both moved higher this week, easily offsetting losses elsewhere. It’s great when they’re both up… though not nearly as fun when they drop together! 😊 The Royal Bank (TSE: RY) and TD also hit new highs after strong earnings, adding to the portfolio’s momentum.

All in all, it was a solid week across the board. Strong earnings, improving sentiment, and a bit of year-end optimism helped push things in the right direction, and it was great to see all three portfolios moving higher together. With markets entering the final stretch of the year, I’m hopeful this momentum carries through the rest of December and into the new year. 😊

Companies on the Radar

Once again, no new companies made it onto my radar this week, which gave me the chance to take a deep dive into GE Aerospace (NYSE: GE). The more I dug, the more impressed I was: this is arguably one of the highest-quality industrial businesses in the world today. It dominates the narrow-body engine market, runs a recurring revenue model that consistently prints cash, and benefits from elite leadership under CEO Larry Culp, who previously led parent GE before the aerospace division was spun out as GE Aerospace in June 2022.

Once again, no new companies made it onto my radar this week, which gave me the chance to take a deep dive into GE Aerospace (NYSE: GE). The more I dug, the more impressed I was: this is arguably one of the highest-quality industrial businesses in the world today. It dominates the narrow-body engine market, runs a recurring revenue model that consistently prints cash, and benefits from elite leadership under CEO Larry Culp, who previously led parent GE before the aerospace division was spun out as GE Aerospace in June 2022.

That said, the stock is priced for perfection. Its current P/E multiple sits well above both the industry and broader-market averages, making it sensitive to potential setbacks – from aviation and defense demand cycles, to costly new engine development, to macroeconomic or geopolitical turbulence.

I’m very interested in owning a piece of this company, but the current valuation makes me want to wait. For now, I’ll stay patient, keep it on my radar, and watch the price closely – re-evaluating if a dip brings it into a more reasonable range. When that happens, I could see myself becoming an owner.

So, once again, my radar list remains the same six companies:

- Napco Security Technologies, Inc. (NASD: NSSC): A small US company that provides security hardware and systems like smart locks, intrusion alarms, fire alarms, and access control solutions. It sells through a network of distributors and installers, and has been increasing its recurring service revenue – something investors usually like to see. As demand for security and smart home products grows, Napco has multiple avenues for expansion.

- GE Aerospace: This is the large American aviation and defence business that remained after General Electric split into three separate companies in 2024. It has been on a strong run thanks to high demand for commercial jet engines as global air travel continues to recover. The company focuses on aircraft propulsion systems and services for both commercial and military customers, and it’s also moving into drones. As a global leader in jet engines and aircraft systems, GE Aerospace offers exposure to long-term trends in travel, defence spending, and emerging aviation technology.

- Mainstreet Equity Corp. (TSE: MEQ): A Calgary-based real estate company focused on mid-market apartment buildings across Western Canada. Their business model is straightforward: buy underperforming buildings, renovate them, improve operations, and increase rental income. With strong demand for rentals, a disciplined approach, and shares that trade below the estimated value of the properties, Mainstreet offers a combination of income, stability, and long-term upside.

- Corning Incorporated (NYSE: GLW): A large US company known for specialty glass and optical technologies. Corning is the longstanding supplier of the glass used in iPhones and is also benefiting from the surge in demand for high quality fiber optics as datacentres expand to support AI and cloud computing. The company is riding several tailwinds with long-term growth potential.

- Dutch Bros Inc. (NYSE: BROS): A rapidly expanding drive-thru coffee chain in the US, known for its energetic customer service and customizable drinks. The company is aiming to open at least 160 new locations by the end of 2025 and has long-term goals of surpassing 2,000 stores. Strong brand loyalty, especially in the Western US, makes this an interesting high-growth story – though still in an aggressive build-out phase.

- XPEL, Inc. (NASD: XPEL): A growing, founder-led maker of protective films, coatings, and related products – best known for automotive paint protection film. XPEL has been expanding into window films and architectural applications, and sells through multiple channels, giving it both reach and control. It’s a company with a focused niche and strong brand recognition in that niche.

As always, these are not buy recommendations. Make sure to do your own research and choose investments that fit your personal financial goals.

The Radar Check was last updated December 5, 2025.

That’s a wrap for this week, thanks for reading – may your portfolio stay green and your dividends steady. See you next time!